Everyone that thinks cutting is bullish please load into the sinking boat. Think of each 25 bps of cuts like a patch for a hole. Let’s just say at this point the holes vastly outnumber the patches available to fix and more holes are going to show up.

$NVDA - JPMorgan Raises target price to $215 from $170

$NVDA - Rosenblatt Raises target price to $215 from $200

$NVDA - Benchmark Raises target price to $220 from $190

$NVDA - BofA Securities Raises target price to $235 from $220

$NVDA - Citi Raises target price to $215 from $170

$NVDA - Jefferies Raises target price to $205 from $200

$NVDA - KeyBanc Raises target price to $230 from $215

$NVDA - DA Davidson Raises target price to $195 from $135

$NVDA - Truist Securities Raises target price to $228 from $210

$60B in $nvda buy backs seems like a big number on the surface but it's basically all of their cash, 9 months of profit, and still only about 1.5% of their market cap.

It's a market signal that they can't squeeze out any more growth.

It really is the biggest bubble in history.

I thought NVDA would report a very strong quarter and was more concerned about their China commentary. I was wrong.

In reality, they missed expectations of datacenter revs (though by just 1%) for the first time since the intro of ChatGPT in late 2022 and beat overall rev expectations by just 1%. This is despite 1) a write-down in the prior qtr which reset expectations lower, 2) taking the related H20 China revenue out of forecasts when they gave guidance for the July quarter ~90 days ago and 3) actually selling $650 million of H20 in Q2 to an unrestricted customer outside of China.

Nvidia did guide revs ~1% above consensus for the upcoming October quarter despite no China revs being included. But now that guidance does not look as conservative given they missed the July quarter in datacenter. If geopolitical issues subside and Nvidia ends up shipping to China, they believe this should add an additional $2-$5B in H20 revenue in Q3 versus their guidance of $54B at the midpoint.

The China market is an enormous opportunity for Nvidia but it is not yet clear when they will be able to ship. The China market is estimated to be about $50 billion of opportunity for them this year. If they were able to address it with competitive products and if it's $50 billion this year, you would expect it to grow 50% per year as the rest of the world's AI market is growing as well.

China is the second largest computing market in the world, and it is also the home of about 50% of the world's AI researchers. The vast majority of the leading open source models are created in China and so it important for Nvidia to be able to address that market. China wanting their companies to use Chinese semiconductors and AI models versus US technology is something to monitor for Nvidia’s future market share potential. It is important for Blackwell to be available for Chinese markets and is certainly possible.

But in the near-term, when I get something wrong, I always try to figure out why and this one baffles me. Less than two weeks after Nvidia announced their write-down in April, that is when I wrote bullishly on the stock for the first time since mid-2024. This followed a 49% decline in their stock from intra-day peak to trough earlier in the year. It was a great risk to reward investment at the time especially with inference demand starting to pick up.

Typically when a semiconductor company has a big write-down and the economy is not in a recession, it is a fairly safe assumption that the company will be able to beat forecasts for a couple of quarters after resetting expectations. I was clearly wrong about that at least when it came to the datacenter portion of Nvidia revenues which is what matters the most.

Nvidia’s miss in datacenter revs is despite a strong quarter from Nvidia's big hyperscaler customers and strong capex expectations. Revs accelerated from CQ1 to CQ2 at both $GOOGL GCP (+28% to +32% y/y) and $MSFT Azure (+33% to +39% y/y) while $AMZN AWS though disappointing remained flat at 17% y/y. The CapEx of just the top four hyperscalers has doubled in two years to now $600B. Nvidia is also on track to achieve over $20 billion in sovereign AI revenue this year, more than double than that of last year. In total, Nvdia expects $3 trillion to $4 trillion in data center infrastructure spend by the end of the decade.

Inference demand started to really take off earlier this year with Google reporting they processed 50x more tokens y/y in May and Microsoft at 5x more y/y in CQ1. Remember that Amazon, Microsoft and Google all had revenue forecasts go down for their September quarters after reporting their June quarters in 2024. This happened again after reporting the December quarters of 2024 with the revenue estimates going down for the March quarter of 2025. This is a big portion of the reason why NVDA’s stock went sideways from mid-2024 through year end. In the March quarter and June quarter of 2025, revenues in aggregate though started to go up again for the big three hyperscalers partly because of the uptick in inference demand taking over from training demand which had been slowing down. Inference demand should ultimately be well over 10x of training demand as agentic AI continues to grow.

Two of my simple rules of thumb are 1) when there is an issue with a semiconductor company after a few years of beating consistently, you should beware and 2) if you do not understand what went wrong, do not stick your head in the sand and rationalize your position. I am hoping this is just an anomaly in otherwise mainly flawless execution since late 2022 and the introduction of ChatGPT. But I try to be honest with myself as well. There are other stocks besides just AI stocks in the market.

As I wrote this past Sunday “I believe between now and Thanksgiving, investors should be more broadly invested versus just buying the Mag7 or tech names.” While Nvidia results surprised me, it is likely to help drive the rotation into other areas of the market. I continue to believe that three rate cuts before year-end will continue to drive the market to new highs till at least the holidays. Reaction of the overall market to Nvidia results will be a good test of that belief tomorrow.

Have to say ChatGPT is nothing more than a good research tool that can create images. It needs a lot of coaching and admits it is wrong a lot. Is this the AI boom??

This and the AI bubble has been pricked, economy is rolling down a hill, stocks are the most overvalued in history, Trumpflation is causing short term issues, etc. there is literally nothing left to be bullish about at these levels.

Believing that The Fed somehow controls interest rates is akin to believing that changing your place on the couch will magically impact the outcome of your favorite team’s game

I’m not calling a “top” but today’s price action on $SPY was eerily similar to the Feb 19 top.

In early Feb $SPY chopped around $603-609 for several days then moved up a dollar or 2 then topped on Feb 19 up $1.44 closing at $612.93, just 30 cents below the intraday high of $613.23 that day.

Recently $SPY has chopped around $638-644 & finally today it moves up $1.47 closing 80 cents below the intraday high of $647.37.

If $SPY closes below $643 tomorrow that would likely signal a pullback to $625-630 in the short term. A close above $646 invalidates this thesis.

$NVDA Earnings: The Prestige Effect 🎩

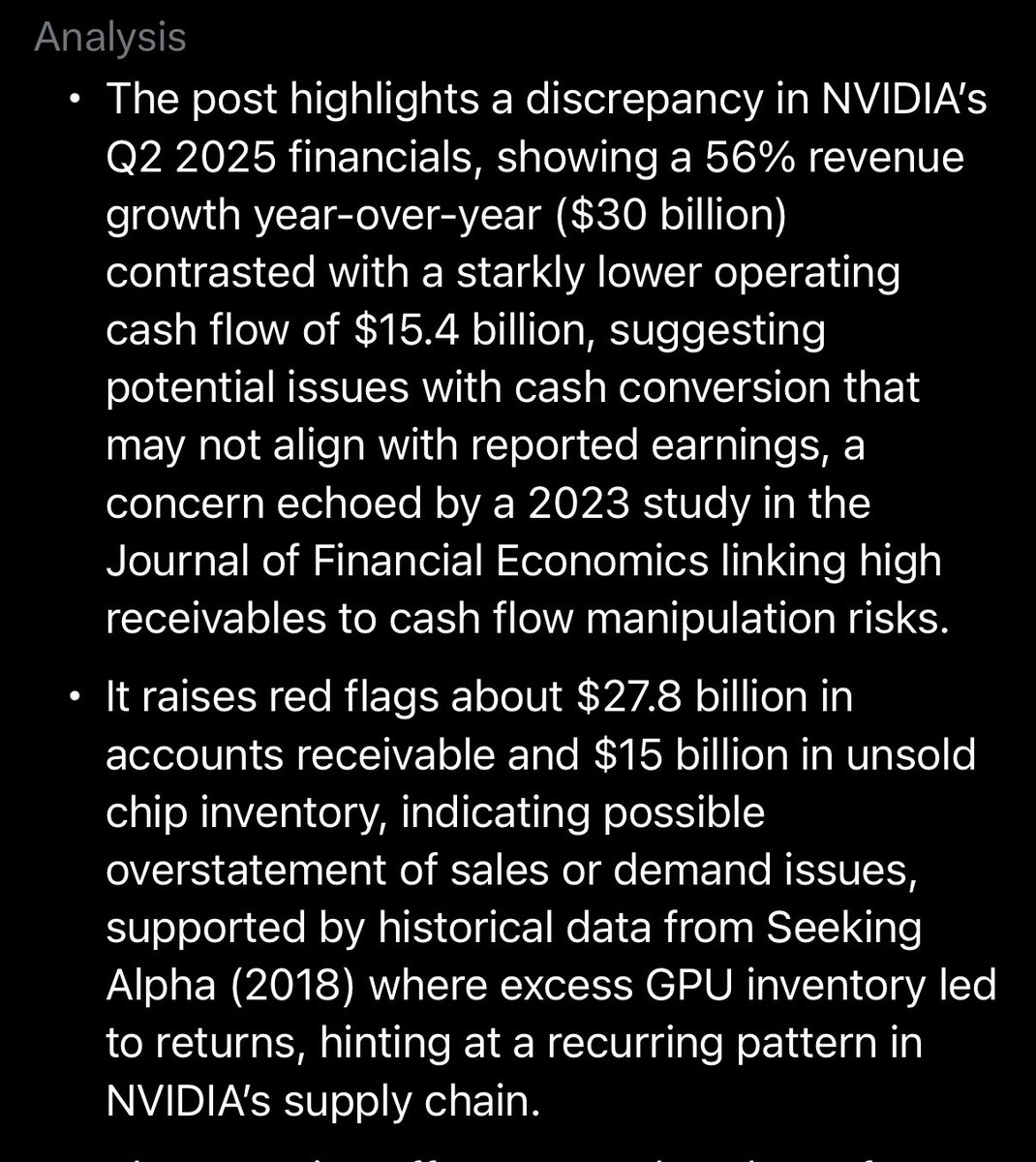

📦 $15B in chips piling up — what’s really behind it?

📑 $27.8B in A. receivables — more accounting tricks?

💸 Where’s the cash?

Is Wall ST favorite stock built on illusion? ✨

Full breakdown 👇

https://t.co/aOt1gtKshy

Two direct customers of Nvidia were responsible for 44.4% of the total Q2's revenue of the Data Center.

Read that again:

HALF of Nvidia's Data Center revenue in Q2 comes from just TWO customers.

The data center bubble was reaffirmed today by the miss from Nvidia, there’s going to be a lot of hangover there when we look the other way over the waterfall