Deflation is one of the worst things that can happen to an economy.

You’re seeing it play out in China right now, and it’s a slow bleed that can take years to reverse.

Here’s why deflation is such a problem, in simple terms.

1. Prices fall.

Sounds good, but it’s not.

When prices drop across the board, people wait to spend because they think things will be even cheaper later.

Less spending means less revenue for businesses.

2. Businesses respond by cutting.

Lower revenue leads to layoffs.

Lower wages.

Lower investment.

Lower growth.

3. Debt becomes heavier.

If your income falls but your debt stays the same, that debt gets harder to pay.

Households, companies, and entire governments get squeezed.

4. The whole economy slows down.

People spend less.

Businesses earn less.

Banks lend less.

Everyone pulls back at the same time.

That’s the deflation spiral.

So what exactly is deflation?

It’s the opposite of inflation.

Inflation is when prices rise.

Deflation is when prices fall for a sustained period.

A one-off drop in the price of eggs is not deflation.

A broad, long-term drop in prices across the economy is.

Why China matters here:

China’s consumer prices have been falling.

Its property market is collapsing.

People are saving instead of spending.

Businesses are pausing investment.

Local governments are buried in debt.

This is exactly the type of environment where deflation takes hold and gets harder to escape.

Deflation is dangerous because it changes behavior.

People stop spending.

Businesses stop hiring.

Debt gets heavier.

And the economy drifts downward.

Once that mindset sets in, it becomes extremely difficult to reverse.

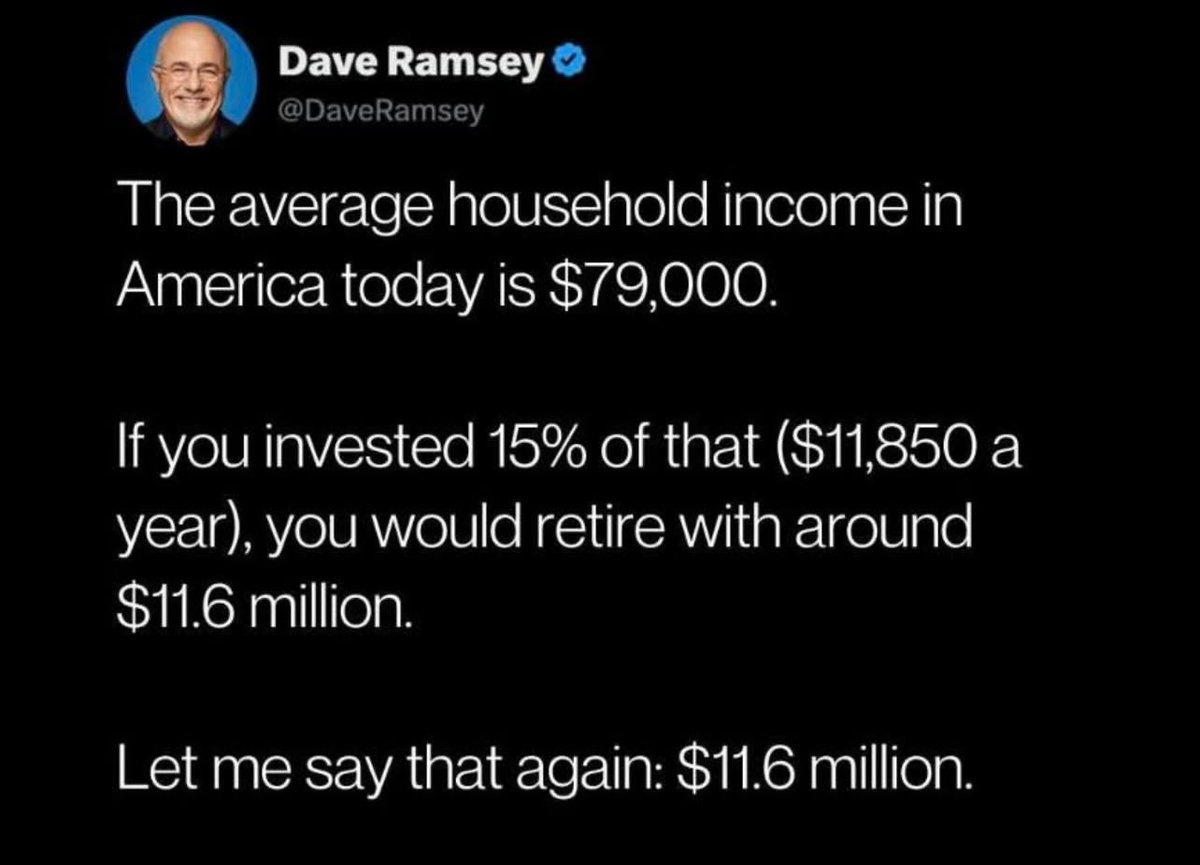

You can end up a multi millionaire by following what Ramsey (and any other finance personality) says:

“Spend less than you make and invest the difference”

Can an average household hit $10 million+ by investing 15% of their income?

No. The numbers are inflated to catch your eye and spark a debate and engagement.

But the principles are correct.

Is investing $987 a month or making $79k at age 20 realistic? Probably not.

Is a 11% return realistic? Also no.

7-8% (especially when you factor in inflation) is a better estimate

The verdict:

Bottom line:

You might get a $2,000 check.

To me, this feels like a response to election results and the number one issue on American’s minds:

affordability

Breaking:

Trump just posted every American will get a $2,000 “tariff dividend” funded by import tariffs.

He added: “not including high income people.”

Here’s how that would actually work (or not).

Running out of money in retirement is a legitimate fear many people feel.

To help you, I put together a free guide:

The 10 Most Expensive Retirement Planning Mistakes (and how to avoid them)

Download it in my profile link.

If you’re 50 or older and afraid of running out of money in retirement…

You’re not alone.

Even people with $1–2 million saved feel it.

Because in this economy, even that might not be enough.

There are 3 numbers that decide if your money lasts or runs out too soon—->

Your Guaranteed Income

Social Security is your safety net…not your plan.

The average couple gets around $4,000–$5,000 a month combined.

For most, that barely covers essentials.

It’s the mistakes that drain your savings before you even get there.

That’s why I put together a free guide:

“The 10 Biggest Retirement Planning Mistakes”

👉Download it in my profile link and avoid the errors that keep most people stuck.

Are you on track for a comfortable retirement?

Most people aren’t…and the numbers prove it.

Median retirement savings in America (Federal Reserve SCF):

•Under 35: $18,880

•35–44: $45,000

•45–54: $115,000

•55–64: $185,000

•65–74: $200,000

Sounds okay… until you apply the 4% rule.

That’s how much you can safely withdraw from your investments each year without running out of money:

•$115,000 → $4,600 per year

•$200,000 → $8,000 per year

That’s barely enough to live on.

For many households, the real goal isn’t $200K.

It’s $1–2 million+, depending on your lifestyle, location, and healthcare needs.

The biggest danger isn’t the number