@overjumped_ I’ve followed this closely and would agree with the potential Endura blunder

Snowy River isn’t the only game, check out the permitting/process on the Bowdens royalty FZR also owns 🤔

$FZR.AX officially filed to dispute the Snowy River buyout clause. Whilst the outcome is uncertain the market price of the royalty is >$40m easily. I’d expect a settlement but interesting times!

https://t.co/DwNvZURuCB

@respeculator@ImmaYieldGuy Can see the Pembroke financials through the Nordic bond they issued, looks grim

Interestingly, from the pricing I can see (could be stale) the bond is still trading at par 🤷♂️

@Kreuzmann13 The offshore assets won’t decline linearly, they should maintain a decent level of production until reserves are done, then drop to 0. Lighting will decline at ~13% until reserves are done.

I’ve spoken to mgmt, the FV of the ARO’s they are confident won’t change from US$8.5M

Whilst I was wrong on timing, buyout proceeds are in 💪

Interestingly, FZR is considering options to challenge to the buyout off the premise that Endura was ‘fully funded’ in late 2025. Could be a major change if the royalty goes live, I’ve got it worth ~$60m at a US$4k oz …

Have progressively built a position in $FZR.AX on the back of an imminent catalyst & potential wind-up of the company.

My first go writing my thoughts on a position, please check it out! Link below.

https://t.co/XYO8nZQ68q

Whilst there is global energy uncertainty a cash backed US based oil producer isn't the worst place to park capital.

Particularly when they're engaging a major shareholder returns strategy, ensuring cash comes back to you!

https://t.co/QsyaYsPYPN

@respeculator Possibly a strong argument for why we need more consolidation in the coal space? Individual companies are (maybe?) less inclined to idle assets given risk to equity vals, but a larger player could do this easily to support prices etc. shame GlenTinto coal spinout didn’t happen

@respeculator This and liquidations/portfolio rundowns, instos stay out because no terminal value and retail get bored if takes >2yrs

Some things are a pretty easy underwrite to a 2x MoM over a few years

Not a sexy 10x, but only need a few of them to get wealthy

@respeculator When https://t.co/K6LsARoBKA buys https://t.co/2iWfQEn4RJ and the merged co. is bought by https://t.co/xD2WxckmlY to feed their industrial businesses? If AEL is cheap enough might make sense given SGH has low cost of capital 🤷♂️

@YellowLabLife As someone in Aus (benefits from franking) with a <$4.6 cost base for WHC and <$42 cost base for HCC this is a dream as, absent any crazy moves up in the coal price akin to 2022/23, would you ever sell the merged co.???

So here’s the issue you get influencers like this guy have a quarter million followers and they claim they don’t know why it is declining… it’s because they don’t understand basic mechanics of price discovery.

They don’t understand that the marginal buyers or the float determines price they think the onchain bitcoin is that is the price discovery

Well, it was once upon a time but now..

Once you can synthetically manufacture the supply, the asset is no longer scarce and once scarcity is gone, price becomes a derivatives game, not a supply-and-demand market.

This is exactly what has happened to Bitcoin.

This is the same structural break that occurred in gold, silver, oil, and eventually equities once they became derivatives-dominated.

The original premise that no longer exists

Bitcoin’s entire valuation logic was built on finite supply (21M) and inability to be rehypothecated.

That died the moment:

•Cash-settled futures

•Perpetual swaps

•Options

•ETFs

•Prime broker lending

•Wrapped BTC

•Total return swaps

were layered on top of the chain.

From that moment forward:

Bitcoin supply became theoretically infinite.

Not on-chain in price discovery.

The metric that explains the collapse

Synthetic Float Ratio (SFR)

Once you can synthetically manufacture the supply, the asset is no longer scarce — and once scarcity is gone, price becomes a derivatives game, not a supply-and-demand market.

That is exactly what has happened to Bitcoin.

This is the same structural break that occurred in gold, silver, oil, and eventually equities once they became derivatives-dominated.

Why Wall Street can now “trade against” Bitcoin

They do exactly what they’ve done in every commodity market:

1.Create unlimited paper BTC

2.Short into rallies

3.Force liquidations

4.Cover lower

5.Repeat

They are not “betting” — they are manufacturing inventory.

The same 1 BTC can now support:

•An ETF unit

•A futures contract

•A perpetual swap

•An options delta

•A broker loan

•A structured note

All at once.

That is six claims on one coin.

That is not a market.

That is a fractional reserve price system.

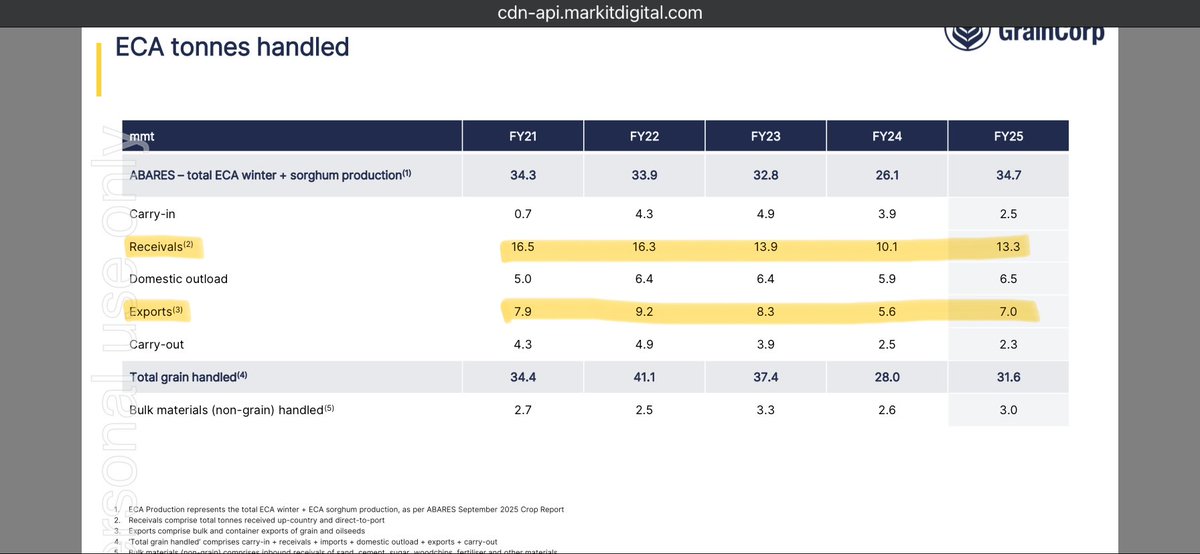

Whether you take mgmt. view of through cycle EBITDA $320m or a more pessimistic $220m $GNC.AX feels cheap at 3.3x EV/EBITDA (using $320m EBITDA) or 4.7x EV/EBITDA (using midpoint of FY26 guide) when compared to historic Val range of 5.1->8x & ~1x P/B

$GNC.AX taking a 📉 as they announce lower than expected FY26 earnings (grain production in 🇦🇺 is strong but pricing is weak so farmers aren’t sending grain through GNC facilities)

Trading near BV ($5.95 at 30 Sep), for irreplaceable 🇦🇺 Ag infra assets

Buy with a 3-4yr hold?

So is the FY26 guide of $200-$240m EBITDA a ‘trough’ pricing in a cyclical industry (see movements in ECA tonnes handled below, Receivals & Exports are key drivers for EBITDA) or a structural change (note that pre FY20 EBITDA through the cycle guide was ~$200m)

@BULLReturns Are you worried about Corp governance with https://t.co/5GaCqyV2TM? They have a pretty horrid track record of screwing small shareholders. Agree ‘spread’ to cash backing is large, but there must be a serious risk that minor shareholders see zero of the cash 🤔

@respeculator Absolutely nuts that https://t.co/RqnHZQ6LzU can muck up that badly, legal action incoming from those who participated in the recent raise?