With the recent narrative, AI bubble or overvaluation, I rotate my funds into healthcare 40% $NVO ($45) & 30% robotic defense stock $KRKNF ($4). These are my safe haven stocks. Money will start printing in 2026.

This week, there was a significant rally in software (SaaS) stocks

Have SaaS stocks finally bottomed after dropping for over a year?

Based on technical analysis, some stocks like ServiceNow ($NOW) have confirmed a change in trend to a new uptrend

There are two ways to confirm an uptrend.

1) 50MA, 150MA and 200MA crossover with slope change OR

2) The 1-2-3 trend reversal (developed by Victor Sperandeo which I learnt in the 1990s)

For those of you who are not familiar with the 1-2-3 technique, a downtrend to uptrend reversal is confirmed when

1) Price breaks above the downtrend and makes an intermediate high (Point B)

2) Price retraces to point C (Point C cannot go below the lowest low of the downtrend (point A)

3) Price closes back above Point B = Uptrend confirmed

This 1-2-3 reversal pattern has been confirmed on some stocks like $NOW. Technical analysis offers no guarantees but the probability is that prices are more likely to trend higher from here

This is why I ADDED to my existing NOW position on Friday.

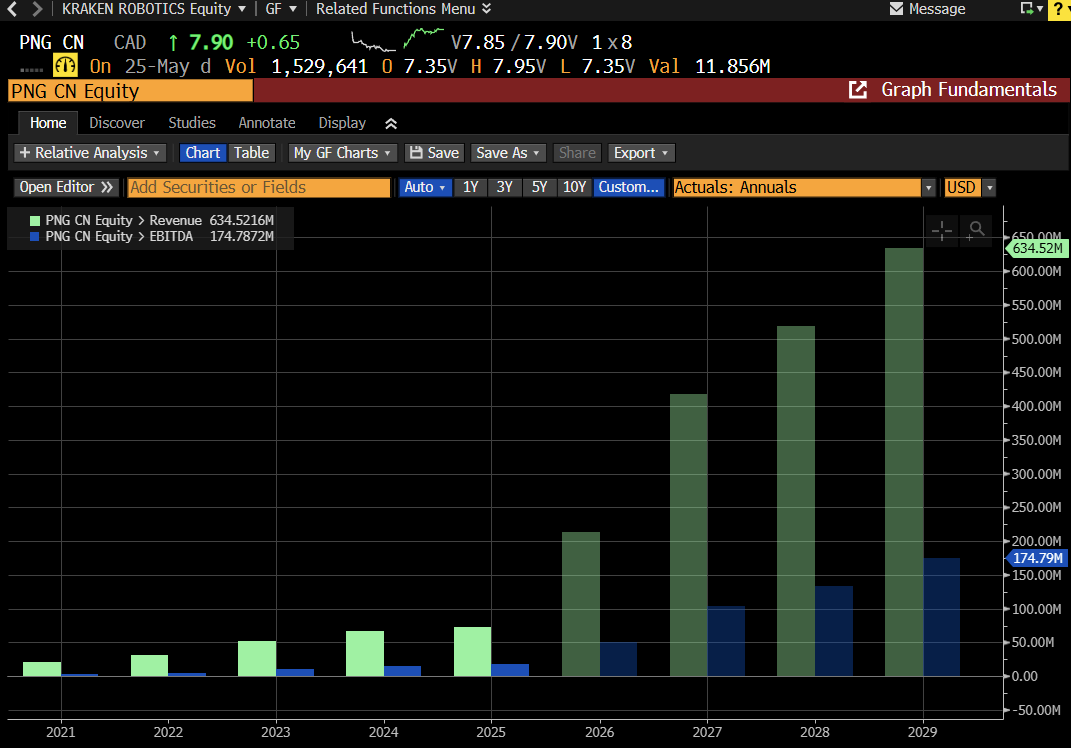

Kraken Robotics ($KRKNF / $PNG.V) just dropped its Q1 earnings report.

This is the subsea drone stock supplying Anduril's maritime products division, that launched out of obscurity into a retail cult following from a junior stock exchange in Canada.

These numbers are just for Kraken Robotics. Not the other profitable underwater intelligence pioneer Covelya they're about to close their acq. of for 2.3x sales.

Revenue: C$21.7M, +35% YoY.

Standalone Kraken business is scaling fast with 50% growth in their product revenue. This is the meat and potatoes of the growth story - with each battery that powers an autonomous submarine drone costs many millions of dollars. 60% revenue growth guided for 2026.

Adjusted EBITDA was positive at C$3.0M, up 7%. The C$3.3M net loss is almost entirely C$2.8M of one-time restructuring and acquisition costs for the Covelya purchase. Strip those out and Kraken posted positive adjusted net income.

Gross margin came in at 56% vs 63%, with the dip from mix. The number swings quarter to quarter on the product and service blend. Services are higher margin and were lighter this quarter (underwater imaging for defense and energy clients), but I care more about product revenue for the bull case with orders over $97M so far this year, more than $KRKNF's entire 2026 revenue.

The order book after all the Strait of Hormuz mine countermeasures narrative is where conviction builds. Kraken product orders in 2026: ~C$97M, up from C$87M last month. Covelya orders in 2026: ~C$165M, up from C$135M last month.

What happened in Iran is generating record breaking demand for $KRKNF's near monopoly position in many of these products.

Guidance reiterated for standalone.

Revenue C$165M to C$175M. Adjusted EBITDA C$40M to C$50M. At the midpoint that is 65%+ revenue growth and 80% EBITDA growth, with implied EBITDA margin above 26%. What other drone adjacent stock is putting up EBITDA margins like this?

Another interesting note?

Asia Pacific revenue more than doubled to C$12.2M, +126% YoY and is now over half of total revenue. That is where the subsea demand signal is loudest.

China sits on an estimated 50,000 to 100,000 naval mines, and a Taiwan contingency is the scenario driving mine countermeasures and seabed-warfare spend across the US, Japan, South Korea and Australia.

The setup is clean.

Covelya closes end of Q2. Next earnings we'll have both on the books and the monster will be clear. Combined guidance follows.

The catalysts: TSX uplisting, Covelya closing, Q2 earnings call in the summer, a U.S. facility, an Anduril US navy deal?

LONG $KRKNF $PNG

$IREN is one of the cleanest AI infrastructure setups on the market.

And retail still has it filed under "Bitcoin miner."

The market is making a generational mispricing. Here's the institutional read:

THE CONTRACTED REVENUE BASE:

→ $3.1B ARR under contract TODAY

→ Targeting $3.7B ARR by end of CY 2026

→ $9.7B Microsoft AI Cloud contract (Nov 2025, NVIDIA GB300 GPUs, 20% prepayment, 5-year term)

→ $1.94B annualized run-rate from Microsoft alone at full ramp

→ $3.4B NVIDIA 5-year contract (May 2026, air-cooled Blackwell at Childress)

→ $700M ARR from NVIDIA contract alone (60MW of capacity)

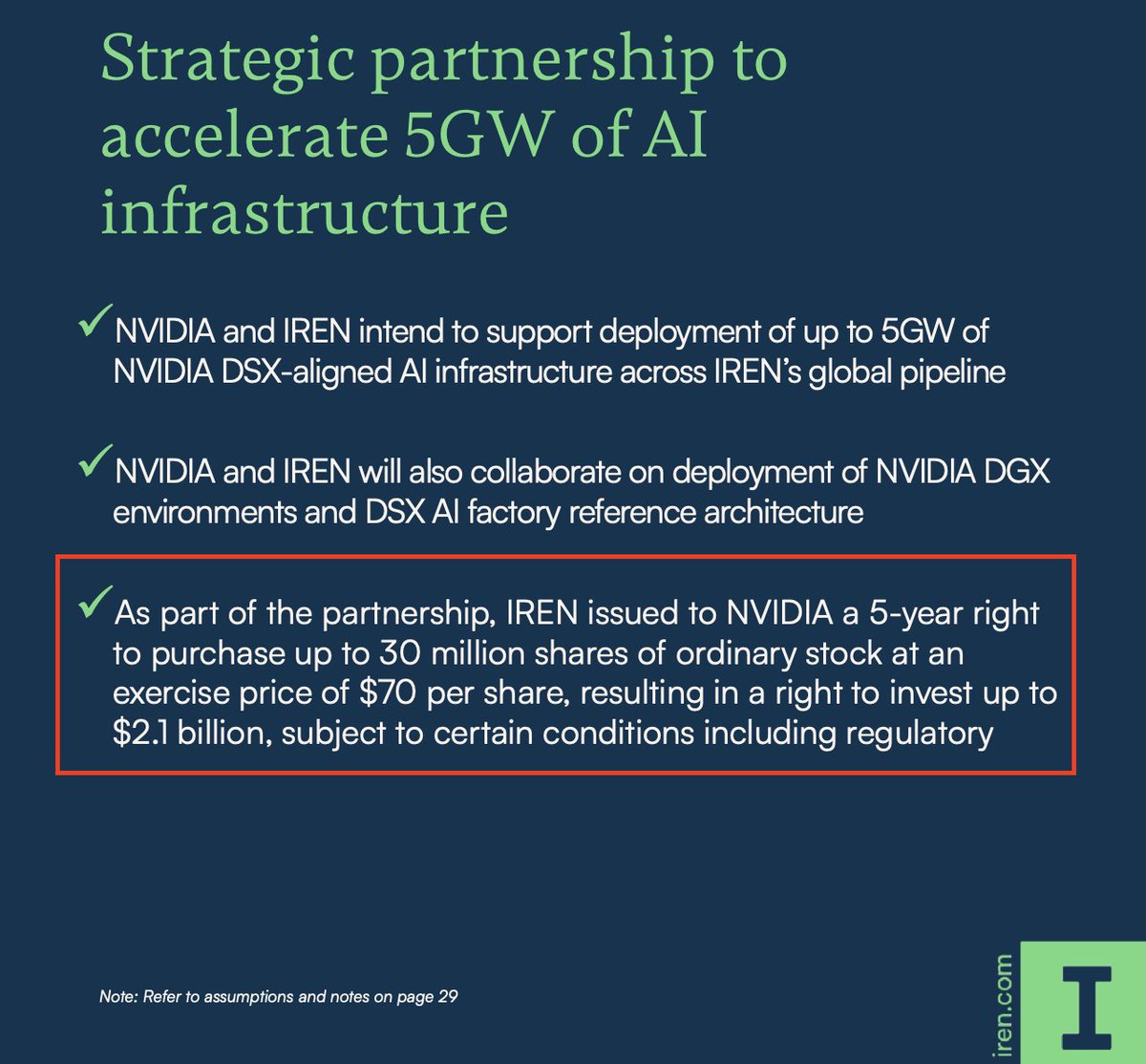

THE $NVDA PARTNERSHIP (the part most underprice):

→ 5GW strategic partnership for DSX-aligned AI factory infrastructure

→ $2.1B equity warrants — NVIDIA has 5-year right to purchase 30M shares at $70 strike

→ Air-cooled Blackwell deployment at Childress

→ IREN is a reference architecture customer for NVIDIA's DSX designs

→ Mirantis acquisition adds 650 engineers for AI cloud delivery

THE ENERGY MOAT NOBODY IS PRICING:

→ 5GW global power portfolio secured (NA + Europe + APAC)

→ Vertically integrated: owns the power AND the data centers

→ British Columbia: 160MW running on 98% direct hydro (near-zero marginal cost)

→ Childress, TX: 750MW grid-secured, 345kV direct grid connection

→ Sweetwater Hub: 2GW total (Sweetwater 1 at 1,400MW energized April 2026)

→ Nostrum acquisition adds 490MW Spanish power + GW+ development pipeline

→ Australia pipeline advancing toward connection agreement

→ Horizon 1-4 liquid-cooled: 200MW critical IT load + 300MW flagship Microsoft deployment

THE BALANCE SHEET (the de-risker):

→ $2.6B convertible senior notes offering (May 2026)

→ Multiple billions secured in funding in past 8 months

→ No going concern, no distress

→ Post-shipment payment structure on NVIDIA GPU orders

→ ATM equity program established as capital management framework

→ $5.8B Dell Technologies GPU purchase agreement tied to Microsoft deployment

THE TRANSITION IS REAL:

→ Q3 FY26 AI Cloud revenue: $33.6M (from $17.3M prior quarter = +94% QoQ)

→ Bitcoin mining hardware being DECOMMISSIONED for GPUs

→ $140.4M impairment last quarter = strategic capital re-allocation

→ 150,000 GPUs deploying through 2026

→ Scaling to 1.21GW capacity in 2027

→ Mirantis acquisition brings enterprise AI cloud operations expertise

→ 2028+ expansion across 5GW underway

THE 2026 EXECUTION PLAN (per Co-CEO Daniel Roberts):

→ 480MW AI cloud capacity delivered

→ 150K GPUs deployed

→ $3.7B ARR by year-end

→ Horizon 1 handoff scheduled Q3 2026

→ Sweetwater 1 substation energized on schedule

→ Construction flywheel running into 2027

THE 2027 EXPANSION:

→ 1.21GW capacity online

→ 730MW under construction across British Columbia and Texas

→ Childress Horizons 5-6

→ Childress air-cooled capacity expansion

→ Sweetwater 1 initial 200MW IT load

→ Repeatable, scalable model accelerating

THE MISPRICING:

The market is pricing IREN as a Bitcoin miner with optionality.

The reality is an AI cloud infrastructure company with:

✓ Two of the world's largest AI customers ($9.7B Microsoft + $3.4B NVIDIA)

✓ One of the largest secured renewable power portfolios globally (5GW)

✓ $NVDA literally holding $2.1B in equity warrants at $70 strike

✓ Vertically integrated power-to-compute stack

✓ Reference architecture customer status with NVIDIA DSX

✓ Multi-billion dollar contracted revenue runway

When NVIDIA's strike price sits above current trading level, the message couldn't be clearer about where this re-rates.

The energy moat is real.✅

The contracts are real.✅

The execution is on schedule.✅

The repricing hasn't happened yet.✅

That's the asymmetric setup.✅

Read the contracts. Read the substations. Read the tape.👀

Consider this...

@nvidia has a 5-year right to purchase 30 million $IREN shares at $70/share

@IREN_Ltd is currently trading at ~$56/share

That means retail investors can buy $IREN today at a $14 discount to the price the world's most valuable company agreed to pay

You can own $IREN cheaper than $NVDA can...