One thing that cannot be overlooked is AmpliTech Group $AMPG and their defense customers.

Those include Boeing $BA, Lockheed Martin $LMT, Northrop Grumman $NOC and the U.S. Air Force.

$AMPG's low-noise amplifiers (LNAs) are crucial for secure defense communications, radar stations, and electronic warfare, and AmpliTech has the best LNAs of the industry.

Having defense customers of the likes of $LMT, $NOC, $BA and the U.S. Air Force shows military-grade validation at the highest level. Getting into defense is extremely hard and takes years of qualifications, alongside the important requirement that it is manufactured in the United States. AmpliTech has passed those requirements.

I recently bought SK hynix, here is why:

SK hynix is a South Korean memory powerhouse. Despite the massive rally it's already had, it is still trading at merely 4.78x FY2027 earnings.

Customer demand for HBM for the coming year far exceeds supply capacity. They literally cannot make enough. DRAM, NAND, and HBM are completely sold out, it's impossible to satisfy all customer orders.

Hyperscalers (likely Microsoft $MSFT, Google $GOOG and Amazon $AMZN) are reportedly offering to fund SK hynix's capacity expansion just to secure future HBM supply. That is how insane the memory shortage is.

Add to that the AI inference and agents shift, newer CPUs/TPUs/GPUs demanding more memory and SK hynix locking in long-term agreements with customers, and we are looking at a structural change in the memory industry. $MU and $SNDK are amongst the winners, but so is SK hynix.

SK hynix is planning to list on the US stock exchange with an ADR (most likely in the second half of 2026), which could be an extra catalyst for the stock.

The surge in memory prices continues

Q2 2026 memory contract pricing has been far above JP Morgan's expectations of a +40-50% increase q/q, with DRAM prices increasing +58-63% q/q and NAND prices +70-75% q/q.

One comment from JP Morgan that I found very interesting: "This is higher than our expectation of +40-50% q/q increase and we sense a stronger environment mainly due to rising CPU memory demand and tighter LPDDR5X supply."

In other words, more CPU demand is driving more demand for memory as well. And with the transition towards AI inference and agents, that demand will only significantly rise over time. Most look at $AMD, $ARM and $INTC to play the CPU boom.

But in my opinion, memory is the better way to play the CPU boom. The valuations are still compressed and the markets are yet to re-rate memory stocks to higher multiples, while it's more than obvious by now that memory demand is not going anywhere.

There is no end to the memory supercycle in sight. $MU and $SNDK are at the forefront to massively profit from it.

The U.S. is attempting to broker a temporary ceasefire deal between Ukraine and Russia in exchange for sanctions relief for Moscow, the Kyiv Independent has learned, trying to revive stalled talks as Washington looks for a foreign policy breakthrough. https://t.co/1ESvpCjtmM

A review of Automatic Identification System (AIS) data from https://t.co/Y4QTdcQsH7 over the past 24 hours indicates 0 commercial vessel transits through the Strait of Hormuz, one of the world’s most strategically vital maritime chokepoints. Prior to the launch of Operation Epic Fury on February 28th, the average number of vessels transiting the Strait was 130.

SEC: The agency proposed letting public companies file semiannual reports instead of quarterly 10-Qs. If adopted, companies could choose one 10-S and one annual report each year rather than three quarterly filings, with semiannual reports due 40 or 45 days after the half-year.

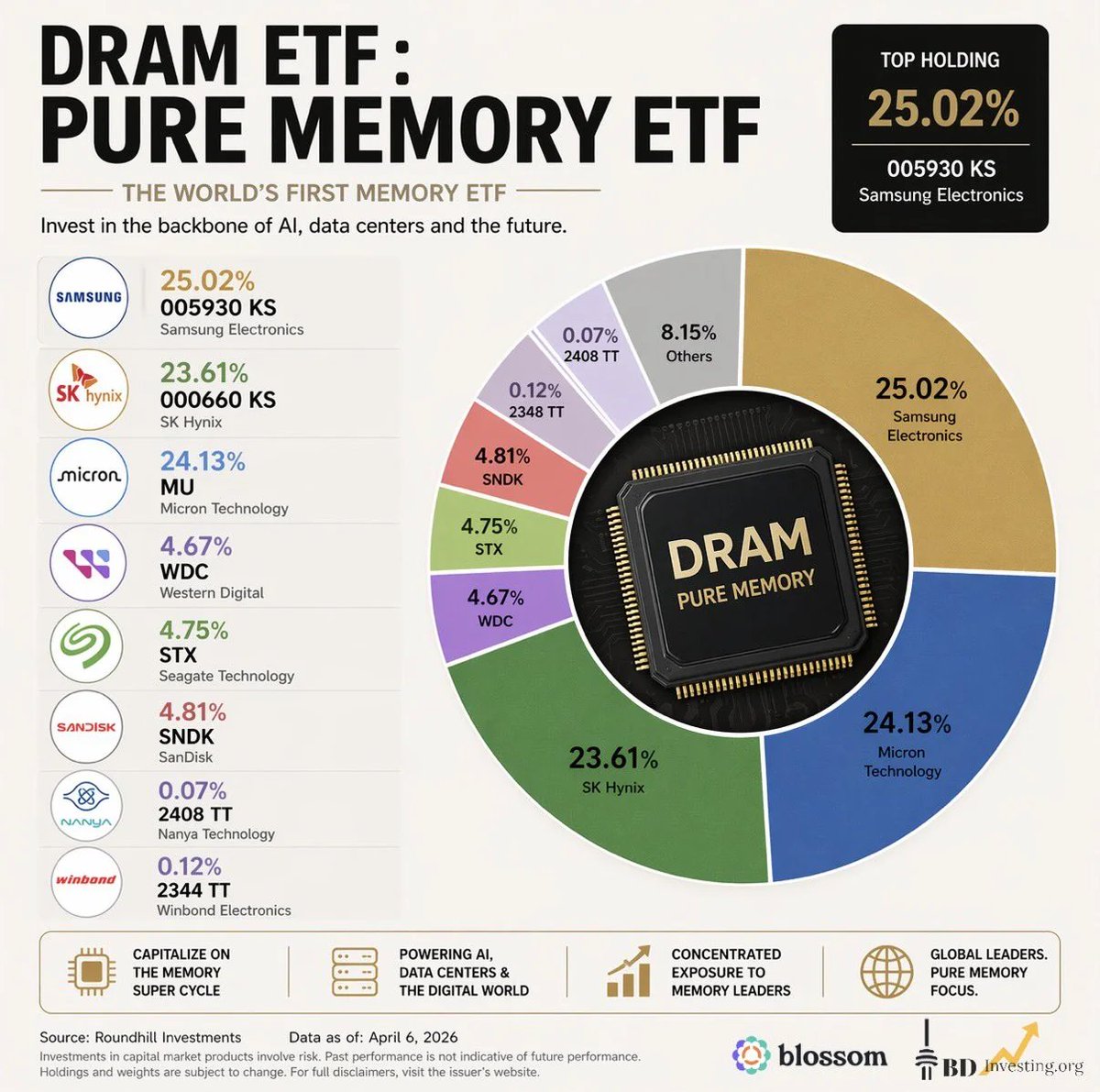

Is $DRAM ETF a good pick?

The ETF $DRAM has been formed recently and has already made quite a name. Diving deeper into it however, there are two things that make me stick to individual stocks rather than buying $DRAM:

1. $SNDK has a weighting of only 4.81% in the ETF, in my eyes $SNDK deserves a bigger weighting. I presume this weighting is mostly based on market cap though.

2. $STX and $WDC are both HDD stocks and poised to profit from the AI boom. However, both stocks have already gone a structural repricing to higher multiples, in the range of 25-28x FY2027 earnings. These stocks are definitely not bad, but the real risk/reward asymmetry is in $SNDK, $MU, SK Hynix and Samsung, which are yet to undergo a structural repricing to higher multiples.

Overall, $DRAM is a solid ETF and a good pick, but I would opt to pick individual stocks if you want to properly optimize your risk/reward ratio. From my point of view, the risk/reward ratio of memory stocks is much better than HDD stocks.

Not financial advice.

Why I believe memory is structurally underpriced

As you may have noticed already, I am quite bullish on memory, in particular on Micron $MU and SanDisk $SNDK. While they have surged to extreme highs lately, their valuation (as well as Samsung and SK Hynix) is still very compelling.

$MU is trading at 5.12x FY2027 earnings, while $SNDK is trading at 8.85x FY2027 earnings. Samsung is trading at 5.41x FY2027 earnings. SK Hynix is trading at 3.72x FY2027 earnings. These valuations are very low compared to the rest of the semiconductor industry. Why is that the case?

Historically, memory has been very cyclical, with periods of a boom followed by periods of a bust. In the boom period, consumer demand is high and memory prices increase, leading to strong profits. But at some point, the trend reverses and consumer demand decreases. Sharp declines in earnings follow and we face a bust period. Usually, PE ratios are low near the peak when the market expects a massive drop in earnings in the period after.

Earnings and cash flows from memory stocks have always been rather volatile, with periods of high performance and also periods of weak earnings. With volatile performance and unstable cash flows, investors perceive the risk of these stocks to be higher and therefore the valuation becomes more compressed. This is why memory stocks have always had a relatively low valuation multiple compared to the rest of the semiconductor industry.

Moving forward, I expect this to change. With AI demand dominating the consumer market, and demand remaining higher than supply for the time being, memory prices will remain high for much longer and may rise further. Furthermore, $MU, $SNDK, Samsung and SK Hynix are already working on LTAs with customers, which mitigates the downside risk and ensures these companies will have high sales for the coming years.

As the bust scenario is being increasingly ruled out due to AI demand, the cyclical nature of the consumer market will be of much less significance for memory stocks from now on. Cash flows and earnings will become much less volatile (to the downside). Therefore, the perceived risk on these stocks should decrease and we should see a re-rating to higher valuations.

If $MU were to double overnight, it would still be valued at only ~10x FY2027 earnings. The potential is still massive and over time, I expect the market to reprice memory stocks to higher valuation multiples.

$MU $SNDK $EWY

⚡️ Iran's foreign minister visits Russia to meet Putin, consult on US ceasefire talks.

The Kremlin has confirmed that Russian President Vladimir Putin would meet the Iranian foreign minister during his visit.

https://t.co/vu1IWmiCxb