Stronger Data for Stronger Decisions @ Lumos

Empowering Financial Institutions to discover actionable insights through data

Specializing in Small Business data

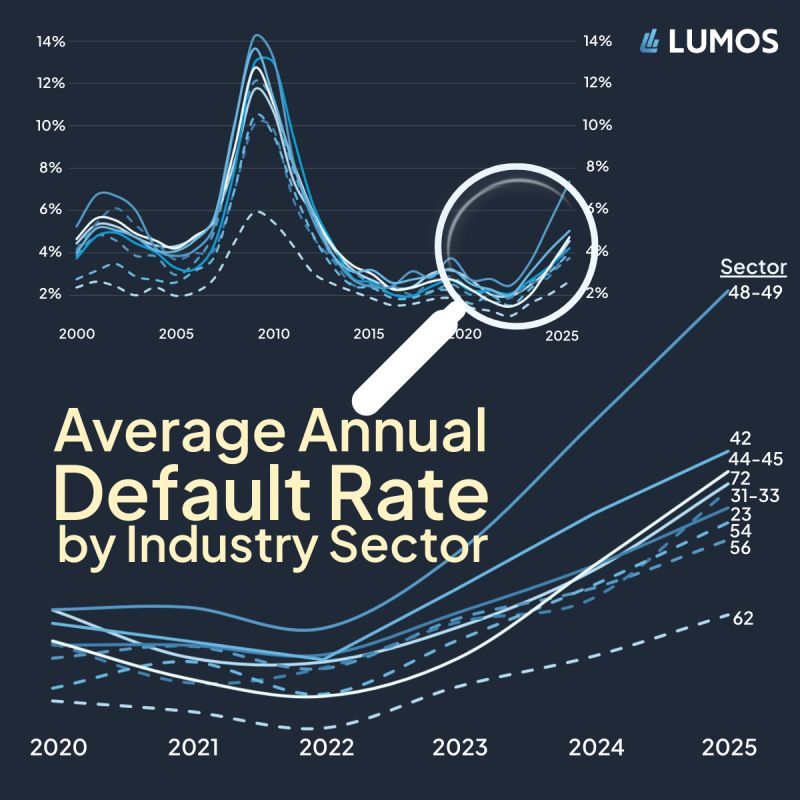

23 Construction

31-33 Manufacturing

42 Wholesale Trade

44-45 Retail Trade

48-49 Transportation & Warehousing

54 Professional, Scientific, & Technical Services

56 Administrative & Support, Waste Mgmt, Remediation Services

62 Health Care & Social Assistance

72 Accommodation & Food

These are among the most active sectors for SBA lending. For 2025, Healthcare/Social Assistance (62) and Transportation/Warehousing (48-49) establish the low and high default curves. The middle 7 sectors span 3.75%-5% default rate for 2025.

List of NAICS sectors in the comments.

It takes raw Call Report/UBPR data and turns it into fun visuals.

⚡ Fast navigation

🤼 Custom peer groups

🫰 Zero cost

Stop scrolling through endless tables and start seeing the data.

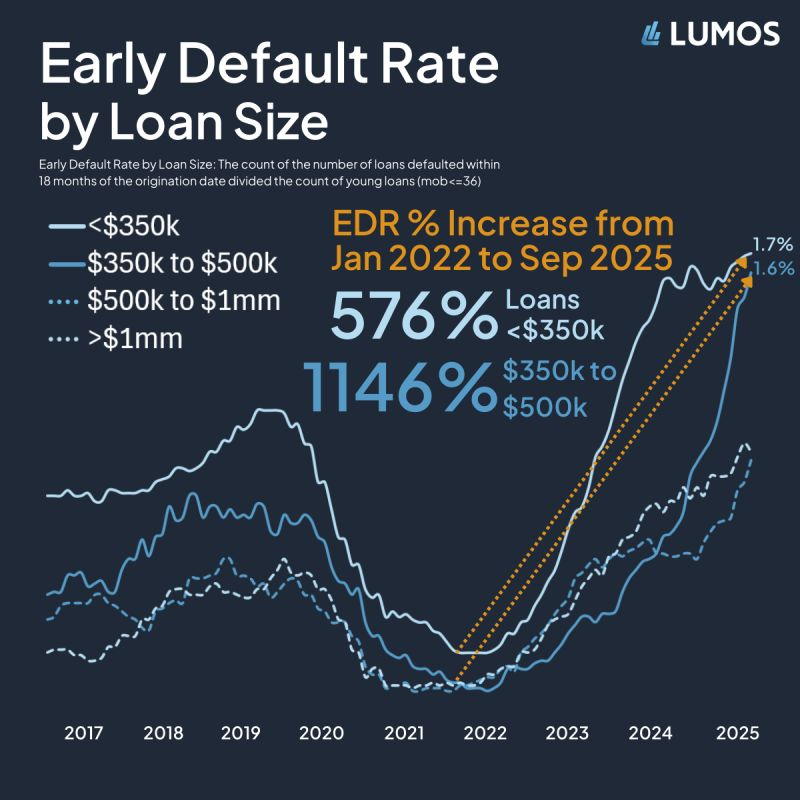

The early default rate for loans <$350k has flattened out recently. It will be interesting to see how that trend plays out in the coming year.

The rate for loans in the $350k–$500k range does not show a plateau yet and has nearly converged with the <$350k group.

Early default rates for small business loans have increased steadily since reaching lows in January 2022 of 0.25% and 0.13% for loan amounts <$350k and $350k–$500k, respectively.

We're looking at SBA 7(a) trends here.

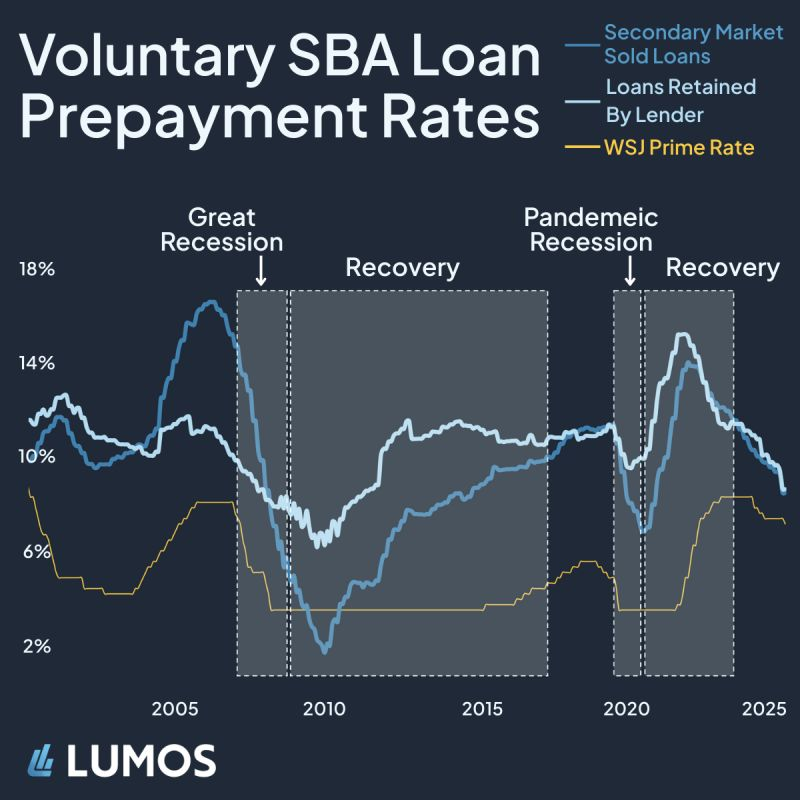

Voluntary prepayment rates for small business loans in the SBA program are continued to trend downward in 2025.

Loans originated in 2020 had the highest prepayment rate in 2025 at approximately 21%. Makes sense, peak prepayment is typically in Year 5-6 of the life cycle.

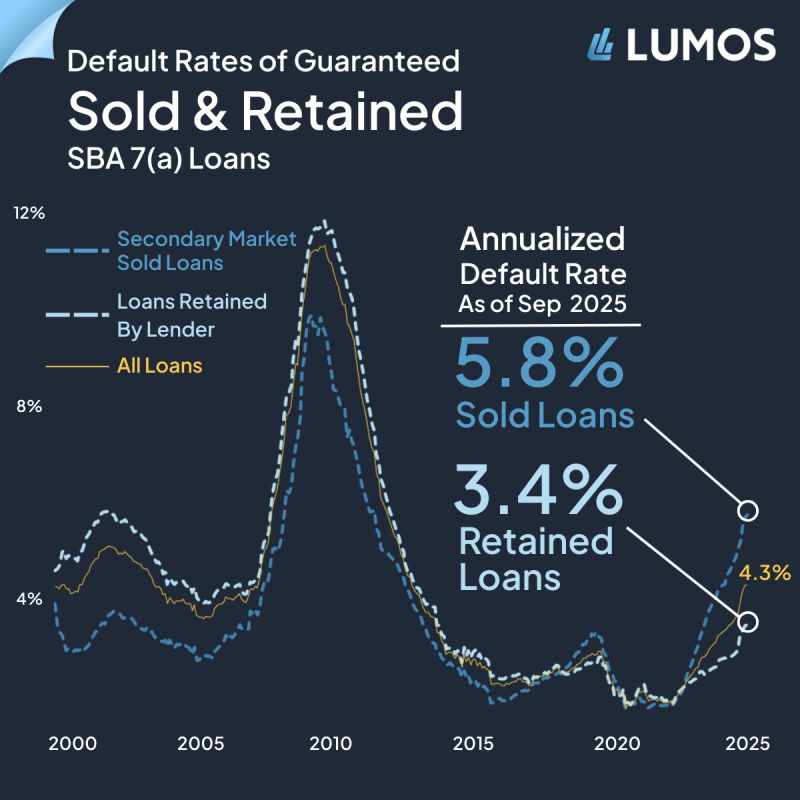

You’re looking at a 5.8% default rate for sold loans vs. 3.4% for retained ones.

So, does the lender’s ability to more easily modify terms on the unsold loans account for a 240-basis point spread? That's at least part of the explanation.

Since 2023, annualized monthly default rates for loans sold into the secondary market have been significantly higher than those retained on lender balance sheets. This flips the script on the last 25 years (with a nod to 2019 for being the other flip).

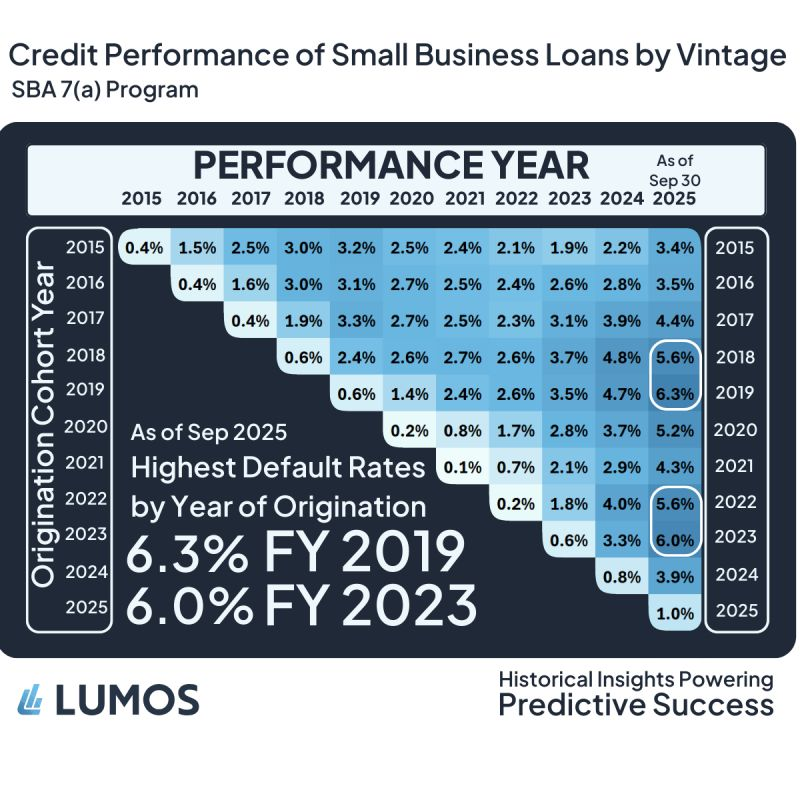

Small business loans usually hit their default peak around year three or four.

Right now, the FY 2024 and 2025 originations are looking a little too ambitious at 3.9% and 1.0% for Year 2 and Year 1 performance, respectively. Those are ones to watch.

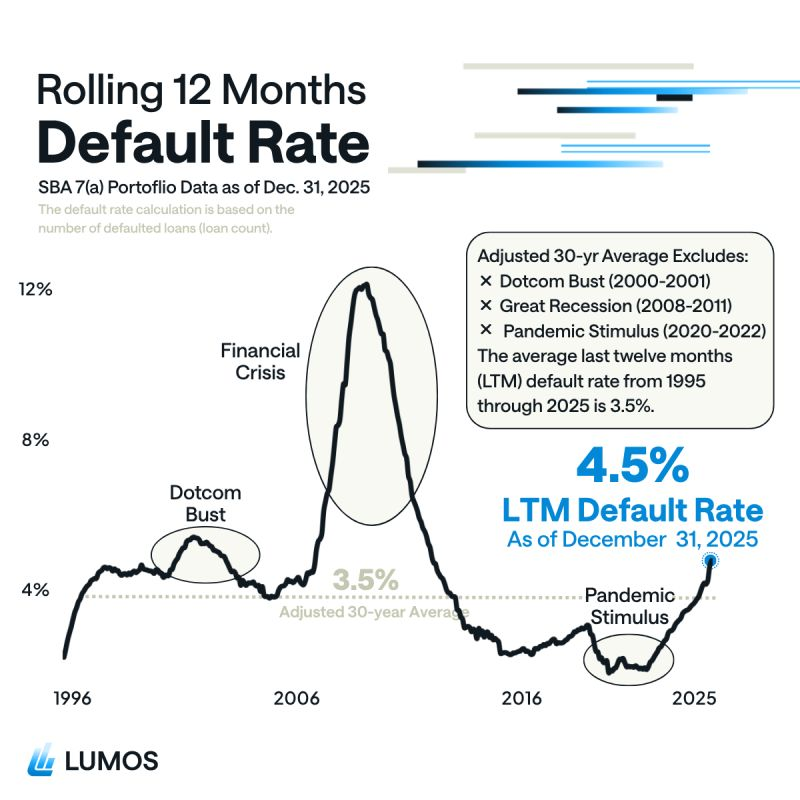

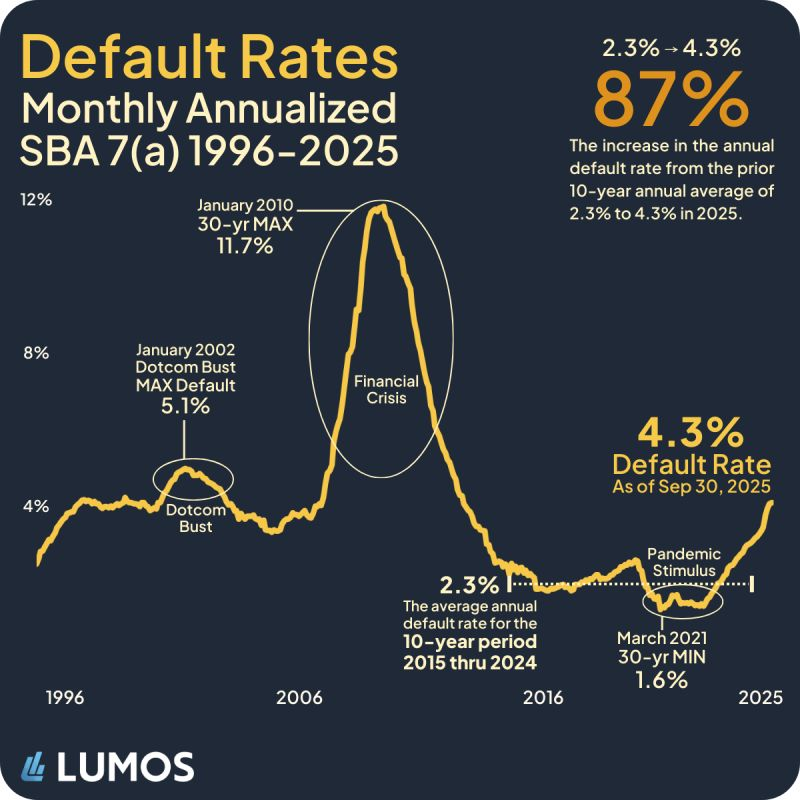

We are currently sitting at a 4.3% default rate, an 87% increase over the 10-year average from 2015-2024.

Stimulus put business-as-usual loan defaults on pause, but the bill is coming due for some of those credits and the numbers are giving dotcom bust flashbacks.

For a decade, we experienced a 2%–2.5% annual default rates in SBA supported small business lending.

Now, our short-term memory is clinging to the drunk-on-stimi lows (sub-2%) adding extra sting to the 2025 face slap.

(Please note this is the annualized not cumulative rate.)

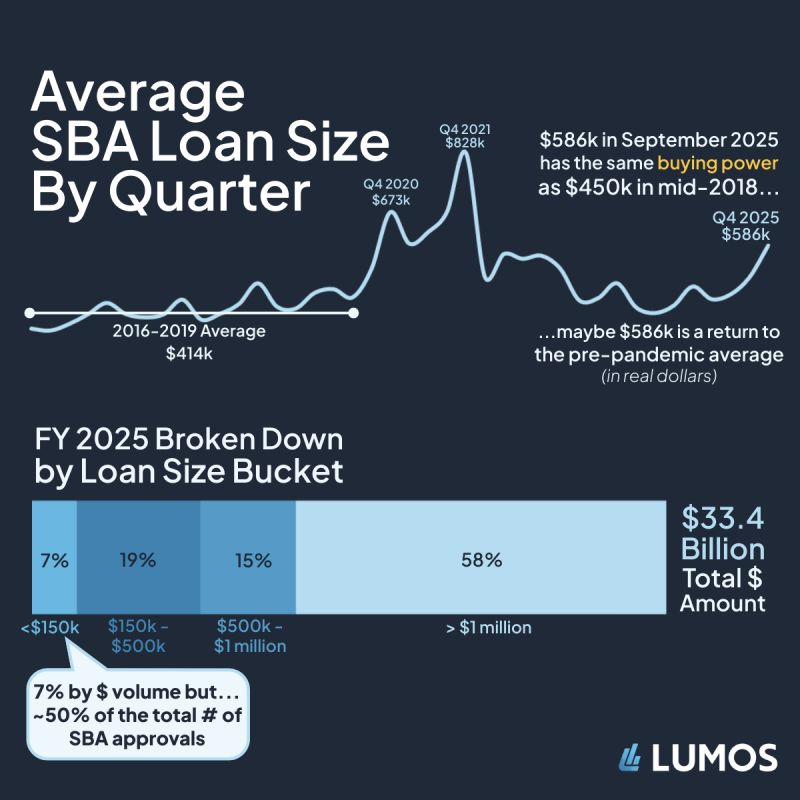

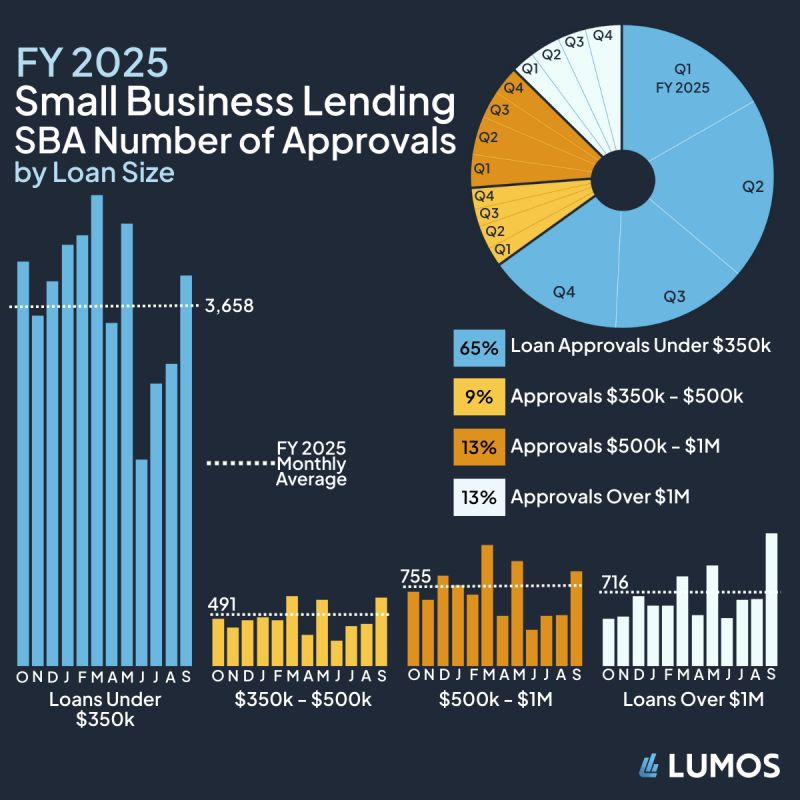

$586 Thousand doesn’t go as far as it used to 🎈

Amazingly, we are back to the old normal. Q4’s average loan size has roughly the same purchasing power of the average loan size of the SBA 7(a) program in the 5 years preceding the pandemic stimulus roller coaster.

Interestingly, approvals for loans greater than $1 million were a fiscal year high in September (by count). With fiscal Q4 being a record quarter by loan amount, looks like loan approvals greater than $1 million drove that.

Approvals rebounded significantly since the June ‘25 drop-off for SBA supported loans.

This was a strong climb out of June’s minimum, especially for loans below the $500k mark. For the year, approvals less than $500k comprised 74% of the total (by loan count).

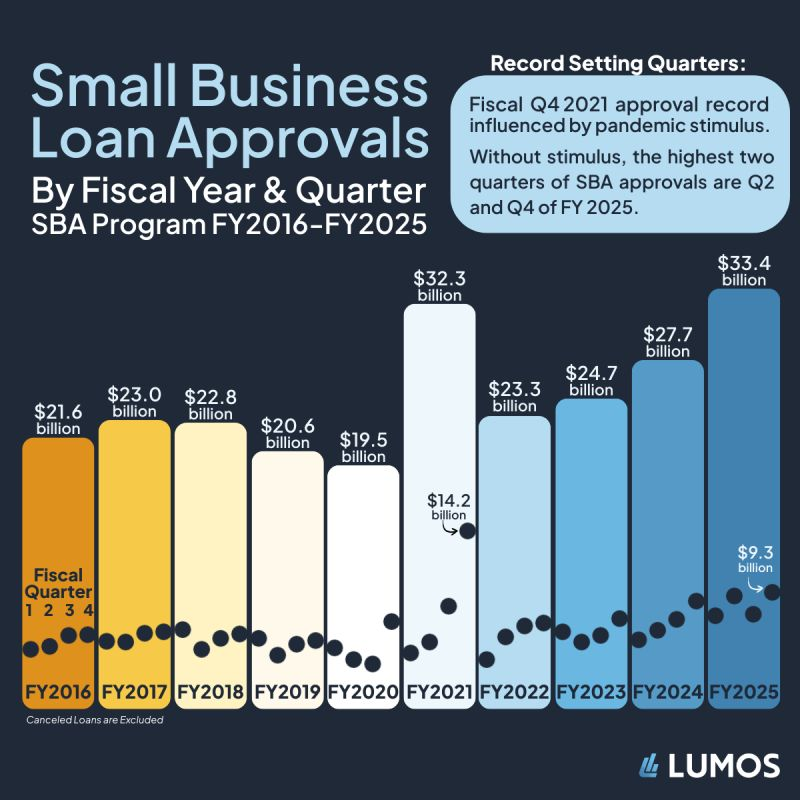

2025’s momentum also produced a record quarterly amount, with $9.3 billion approved in Q4 (July–Sept) alone…again setting aside the stimulus-influenced Q4 of FY 2021.

Note: Canceled loans are removed from their corresponding original approval quarter.

$33.4 billion in SBA loan approvals in fiscal year 2025. Excluding the pandemic-influenced spikes of 2021, this is the highest performing year.

👀 Be on the lookout for multiple posts wrapping up 2025 throughout the coming weeks.

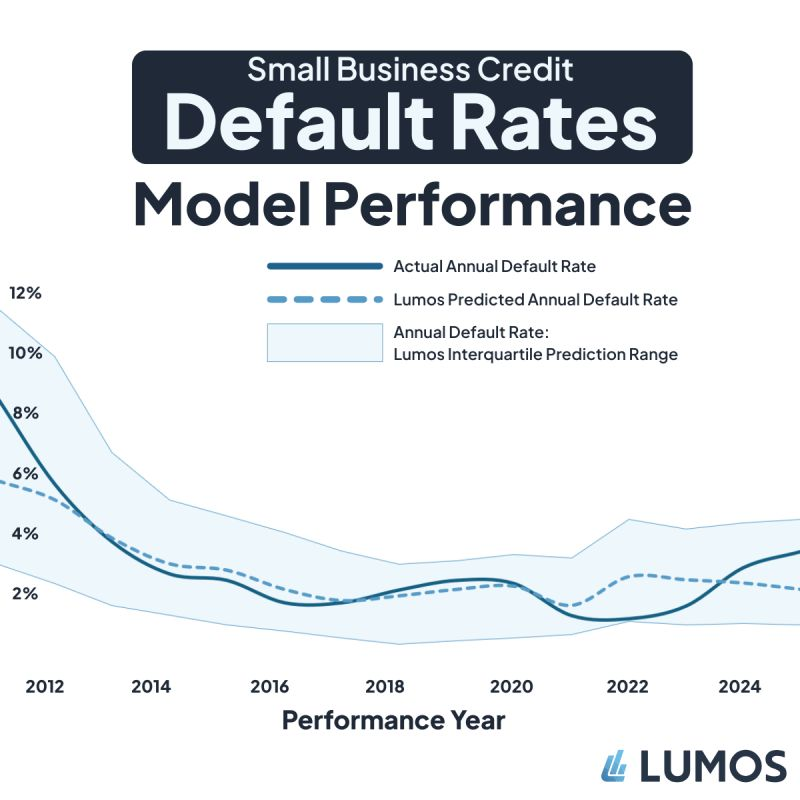

🔵The model's IQR narrowed before the pandemic & widened in 2021, mirroring the rise in economic uncertainty

🔵It overpredicted defaults from 2021-2023 due to small business stimulus

🔵It underpredicted defaults in 2024 and 2025 as delayed defaults from 2021-2023 materialized

Actual defaults consistently fall within our model's interquartile range (IQR), showing the predictions are not only accurate but robust. The model has successfully adapted to changing economic conditions and periods of high macroeconomic uncertainty.