📌 Stock Under Watch: SEDEMAC MECHATRONICS

Business Model:

SEDEMAC makes small electronic devices called ECUs that act like a "brain" for two/three-wheelers and backup generators — telling the motor or engine how to run properly. They build the tech in-house and don't rely on sensors most competitors need.

🧠 Why it's interesting:

A new emissions rule (OBD2B) is pushing more vehicles to adopt this technology — and India has barely scratched the surface, with less than half the two/three-wheeler market covered so far

Their "sensorless" technology is rare — no one else seems to have cracked it yet, giving them a real head start

They're expanding into new areas — electric vehicle parts, commercial vehicles, and even power tools — all using the same core technology they've already built

📊 Key positives:

Revenue crossed ₹1,058 Cr in FY26, up 61% from last year — first time ever above ₹1,000 Cr

Profitability is climbing fast — margins went from 12.8% to 21% in just 3 years

Returns on capital are strong at 40%, and they're growing without taking on debt from shareholders (funded by their own cash + some borrowing)

3 out of the top 4 two-wheeler brands in India already use their technology

Building bigger factories now, ahead of expected demand

⚠️ Risks:

They depend heavily on a few big customers — and a recent correction showed this risk is actually a bit worse than first reported

Management doesn't share much detail on numbers (no volumes, margins, or future targets) even when investors ask

Their whole business rests on one core technology — if a competitor cracks it, their edge could shrink

Part of their business (generators) depends on US weather patterns like hurricane season

Rising chip/component costs could squeeze profits a little next year

🎯 My view:

Watching for long-term potential — strong technology edge and efficient growth, but keeping an eye on how transparent they are with numbers going forward.

Not a recommendation. Do your own research.

58 HIGH-QUALITY SME STOCKS TO STUDY, TRACK & RESEARCH 🔥🔥🔥

▪ Indo SMC

▪ Susan Electricals

▪ Prizor Viztech

▪ Blue Water Logistics

▪ Maxvolt Energy Industries

▪ Sunita Tools

▪ Sunlite Recycling Industries

▪ Shree Refrigerations

▪ Airfloa Rail Technology

▪ Grand Continent Hotels

▪ Alpex Solar

▪ TechD Cybersecurity

▪ V-Marc India

▪ Afcom Holdings

▪ ABS Marine Services

▪ CFF Fluid Control

▪ Anondita Medicare

▪ GSM Foils

▪ Apsis Aerocom

▪ Cosmic CRF

▪ OBSC Perfection

▪ Aimtron Electronics

▪ Zelio E-Mobility

▪ Concord Control Systems

▪ JD Cables

▪ Z-Tech (India)

▪ KP Green Engineering

▪ Oriana Power

▪ Hemant Surgical Industries

▪ FlySBS Aviation

▪ Fabtech Technologies Cleanrooms

▪ Sugs Lloyd

▪ Baheti Recycling Industries

▪ Neetu Yoshi

▪ Connplex Cinemas

▪ Purple United Sales

▪ OSEL Devices

▪ Yash Highvoltage

▪ Adisoft Technologies

▪ Msafe Equipments

▪ Monolithisch India

▪ Sacheerome

▪ KRM Ayurveda

▪ PNGS Gargi

▪ Goel Construction

▪ Namo eWaste Management

▪ Yash Optics & Lens

▪ Vivid Electromech

▪ Bondada Engineering

▪ Danish Power

▪ Saakshi Medtech & Panels

▪ Beezaasan Explotech

▪ Jainik Power Cables

▪ Divine Power Energy

▪ Teamtech Formwork Solutions

▪ Safe Enterprises Retail Fixtures

▪ Highness Microelectronics

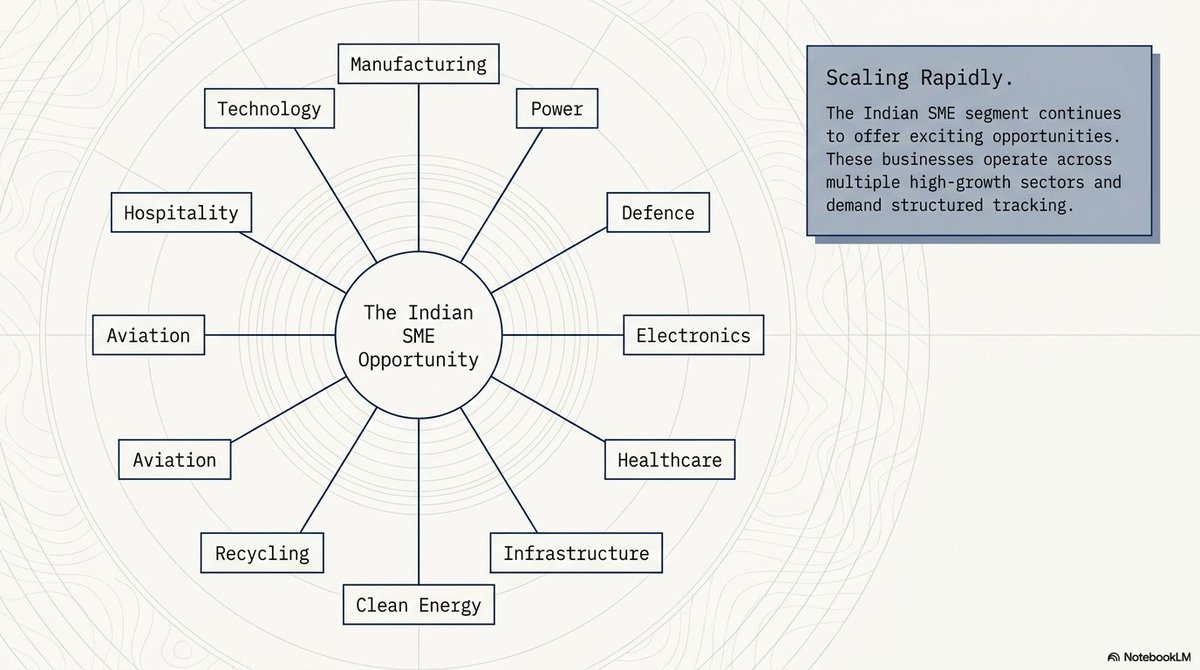

India's SME segment continues to offer exciting opportunities across manufacturing, power, defence, electronics, healthcare, infrastructure, clean energy, recycling, aviation, hospitality, and technology.

SMEs are often young, fast-growing businesses that are still in the early stages of their growth journey. If a company has a scalable business model, strong management, and executes well, it can grow much faster than mature businesses over the long term.

That is why some of India's biggest wealth creators were once small companies. Studying SMEs regularly helps you identify emerging businesses early, understand new industries, improve your research skills, and build a high-quality watchlist before they become widely discovered. Continuous tracking and research are the key to finding tomorrow's leaders.

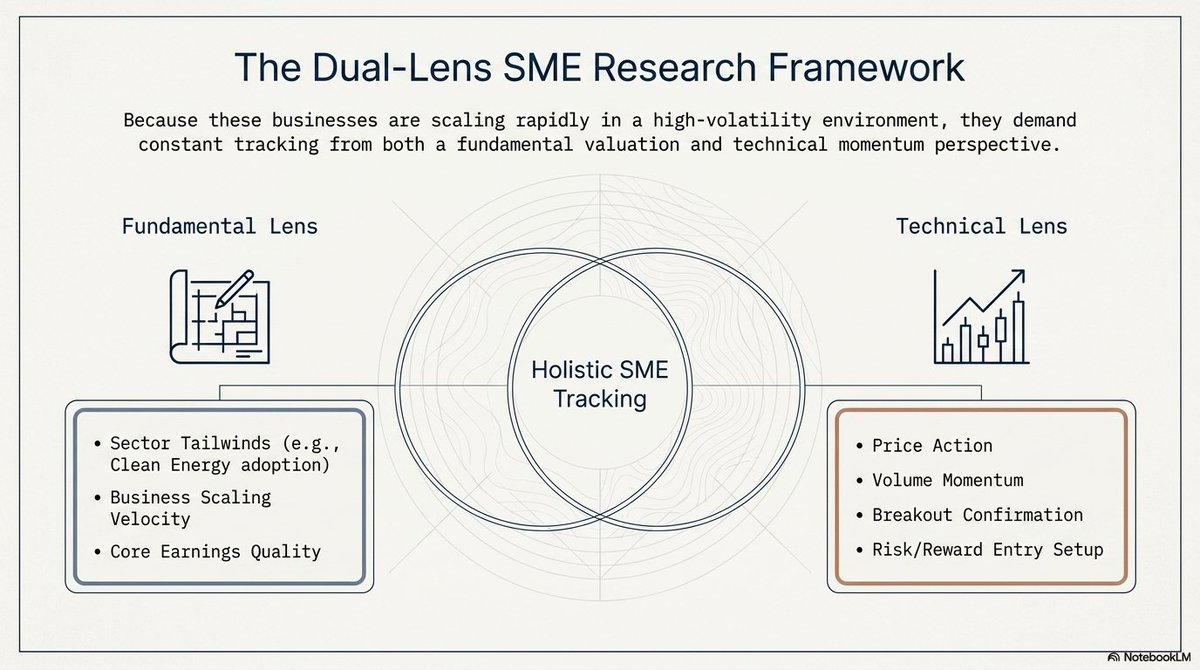

Many SME businesses are scaling rapidly and are worth tracking from both a fundamental and technical perspective.

DISCLAIMER

The above list is shared solely for educational, learning, research, and tracking purposes. It is not a buy, sell, or hold recommendation. Please conduct your own research before making any investment decisions.

V2 Retail,

Another man from whom you can pick up a lot learning. You can chnage your life 360 degree only if you want.

The Man Behind Vishal Mega Mart | Ram Chandra Agarwal's Success Story https://t.co/q8xFYZyLzz via @YouTube

📌 Stock Under Watch: RateGain Travel Technologies

Business Model:

RateGain is an AI-powered travel technology company that provides SaaS solutions to hotels, airlines, and online travel agencies (OTAs). It helps customers optimize pricing, increase direct bookings, run AI-driven marketing campaigns, and manage bookings across multiple platforms. Around 60–67% of its revenue comes from recurring SaaS subscriptions.

🧠 Why it’s interesting:

• Customer base expanded from ~3,000 to 13,000+ after the Sojern acquisition, creating a massive cross-selling opportunity.

• FY26 revenue growth of ~69% YoY, driven by acquisition synergies and platform expansion.

• Transitioning from a traditional travel SaaS company into an AI + Data platform, strengthening its long-term competitive moat.

📊 Key positives:

• Revenue / profit trend: FY26 revenue expected to grow ~69% YoY, with 60–67% recurring subscription revenue.

• Strong balance sheet / business quality: LTV/CAC of ~12–13x, revenue per employee up 70%+, and the top 10 customers contribute only 20–24% of revenue, indicating good diversification.

• Industry growth potential: Benefiting from AI adoption, digital transformation in travel, dynamic pricing, and increasing demand for direct hotel bookings.

⚠️ Risks:

• Growth is currently acquisition-led, so organic growth needs to improve.

• Net Revenue Retention (NRR) has declined from ~120% to ~100%, indicating slower expansion from existing customers.

• Short-term margin pressure due to acquisition costs, amortization, and integration risk. Employee attrition has also increased to ~14–15%.

🎯 My view:

Watching for long-term potential. If management successfully integrates Sojern, improves organic growth, and stabilizes margins, RateGain could become a leading AI-driven travel technology platform.

Not a recommendation.

Do Your own research

📌 Stock Under Watch: Jeena Sikho Lifecare

🏥 Business Model:

Jeena Sikho runs 119 Ayurveda centers and hospitals, where doctors prescribe its own medicines—creating a vertically integrated healthcare ecosystem.

🧠 Why It’s Interesting:

• 📈 EBITDA margin expanded from 30% to 44%, driven by operating leverage

• 💊 Medicine business enjoys ~88–89% gross margins and is the key profit driver

• 🏥 Network expanded from 111 to 119 centers, supporting volume growth

• 🌿 Rising adoption of Ayurveda and chronic disease management creates a structural tailwind

📊 Key Positives:

• 🚀 EBITDA grew 148%, indicating strong operating leverage

• 📈 OPD, IPD and medicine volumes continue to rise

• 💰 High-margin medicine sales are increasing as a share of revenue

• 🔄 Asset-light product business offers better scalability than hospitals

⚠️ Risks:

• ⚖️ Model depends heavily on doctors prescribing in-house products

• 📉 EBITDA margin declined from 45% to 36% QoQ due to one-offs

• 💸 Finance costs are rising as the company expands

• 🏛️ Potential regulatory and ethical scrutiny

🎯 My View:

⚡ Jeena Sikho isn't a hospital company—it's a high-margin healthcare product business disguised as a hospital chain.

Not a recommendation. Do your own research.

📌 Stock Under Watch: Sansera Engineering

⚙️ Business Model:

Sansera manufactures precision-engineered components for automotive, aerospace, defence, and industrial applications. Its products are critical components used in engines, transmissions, EVs, aircraft, and defence systems.

🧠 Why It’s Interesting:

• 🚗 Supplies to global OEMs like BMW, Stellantis, Daimler, Yamaha & Royal Enfield

• ✈️ Expanding into high-margin aerospace & defence segments

• 🌍 Export revenue contributes ~35%+ of total revenue

• 📈 Beneficiary of premium motorcycles, EVs, aerospace & defence growth

📊 Key Positives:

• 💰 FY25 Revenue: ~₹3,450 Cr+

• 📈 EBITDA Margin: ~18% (among the best in the auto ancillary space)

• 🌎 Strong presence across India, Europe & North America

• 🏭 Precision engineering creates high entry barriers

• 🚀 Non-auto business targeted to contribute 20%+ of revenue over time

⚠️ Risks:

• 🚗 Auto sector slowdown can impact demand

• ⚙️ Customer concentration with major OEMs

• 🌍 Global recession may affect export demand

• 💸 Raw material cost fluctuations

🎯My View:

⚡Sansera isn't just an auto ancillary company—it's a precision engineering play benefiting from aerospace, defence, EVs, and premiumization trends.

Not a recommendation. Do your own research.

📌 Stock Under Watch: HFCL

📡 Business Model:

HFCL manufactures optical fibre cables (OFC), telecom equipment, and defence communication systems used in 5G networks, BharatNet, railways, and defence infrastructure.

🧠 Why It’s Interesting:

• 📶 India's fibreization is still <40% vs 80%+ in developed markets

• 📦 Order book of ~₹9,900 Cr provides strong revenue visibility

• 🛡️ Defence orders crossed ₹1,000 Cr+, a higher-margin segment

• 🌍 Export revenue contribution has increased significantly in recent years

📊 Key Positives:

• 🚀 OFC capacity of ~33 million fibre km annually

• 📈 Beneficiary of ₹1.4 lakh Cr+ BharatNet rollout

• 🌎 Expanding exports across 40+ countries

• 🏭 Backward integrated fibre manufacturing improves competitiveness

• 💰 Net debt-to-equity remains comfortable

⚠️ Risks:

• 📉 Telecom capex slowdown can impact growth

• 🏛️ Delays in government projects

• ⚔️ Intense competition in fibre and telecom equipment

• 💸 Working capital-intensive business

🎯 My View:

⚡HFCL's future isn't in cables—it's in defence, exports, and high-margin technology products.

Not a recommendation. Do your own research.

Most investors are looking at what this company was.

Very few are looking at what it could become.

• Strong revenue growth 📈

• Expanding margins 💰

• Industry tailwinds at its back 🌊

• Capacity expansion underway 🏭

• Multiple growth drivers kicking in 🚀

The opportunity isn't in today's numbers.

It's in what the business could look like 3–5 years from now.

The chart also supports the fundamental turnaround.

Most investors are looking at what this company was.

Very few are looking at what it could become.

• Strong revenue growth 📈

• Expanding margins 💰

• Industry tailwinds at its back 🌊

• Capacity expansion underway 🏭

• Multiple growth drivers kicking in 🚀

The opportunity isn't in today's numbers.

It's in what the business could look like 3–5 years from now.

The chart also supports the fundamental turnaround.

📌 Stock Under Watch: Quality Power ⚡

🔧 Business Model:

Quality Power builds critical power transmission equipment and grid stabilization solutions like Reactors, FACTS, STATCOM & HVDC systems that help electricity grids run efficiently and reliably.

🧠 Why It’s Interesting:

• 🌍 Beneficiary of global grid modernization & energy transition

• 📦 Strong order book of ₹1,406 Cr providing revenue visibility

• ⚡ Increasing focus on high-margin FACTS, STATCOM & HVDC solutions

• 🇪🇺 European subsidiary (Endoks) opens access to premium markets

📊 Key Positives:

• 📈 Moving from products → high-value grid technology solutions

• 💰 Endoks operates at >25% EBITDA margins

• 🚀 Strong demand from renewables, grid expansion & electrification

• 🌎 Global footprint reduces dependence on a single geography

• 🔥 High entry barriers: certifications, technology & utility relationships

⚠️ Risks:

• 🏗️ Project-based business can lead to revenue volatility

• 🌍 Global capex slowdown can impact order inflows

• ⚔️ Competition from giants like Siemens, Hitachi Energy & GE

• 🔄 Aggressive expansion and acquisitions increase execution risk

🎯 My View:

This is no longer just a transformer/reactor company.

Quality Power is gradually becoming a grid technology player.

If management successfully scales FACTS, HVDC and energy transition solutions, the business could see both earnings growth and valuation re-rating.

Not a recommendation. Do your own research.

📌 Stock Under Watch: SOLAR INDUSTRIES 🚀

🏭 India's largest explosives player, transforming into a defense manufacturer.

🧠 Why it's interesting:

• 🌍 Export revenue jumped from ~₹800 Cr → ₹3,800+ Cr (4.7x growth)

• 🚀 Management guiding for ~30% export growth

• 🛡️ Entering high-margin defense products like 155mm artillery shells & Bhargavastra counter-drone systems

• 🌏 Expanding globally across Thailand, Indonesia & Australia

📊 Key Positives:

• Export growth inflection visible 📈

• Strong entry barriers: licensing, technology & govt relationships 🔒

• Defense can become the next profit engine 💰

⚠️ Risks:

• Defense execution delays ⏳

• Mining business remains cyclical ⛏️

• Valuation already pricing in optimism 📉

🎯 My View:

A company transitioning from a commodity explosives business to a high-margin defense platform.

Track: Defense orders, export growth & margin expansion.

⚠️ Not a recommendation. Do your own research.

#StockMarket #Investing #Defense #SolarIndustries

📌 Stock Under Watch: TD Power Systems (TDPS) ⚡

🏭 What it does:

Manufactures AC generators & motors used in power plants, industrial facilities, gas engines, and data centers across the globe.

🧠 Why I'm tracking it:

🚀 Riding the AI & Data Center Power Demand Boom

🌍 75–80% of order inflows now come from exports

📈 Order inflow running at ₹550–600 Cr per quarter

🏗️ 3rd manufacturing plant operational, supporting growth without major capex till FY28

📊 Key Positives:

✅ Massive order book provides strong revenue visibility

✅ Moving into large generators (up to 200 MW) — a higher-margin opportunity

✅ Benefiting from a global power infrastructure upcycle

✅ Operating leverage kicking in as capacity utilization remains high

✅ Strong positioning in fast-growing gas engine generator segment

⚠️ Risks:

❌ Working capital-heavy business (cash flow lags earnings)

❌ Customer concentration through OEM relationships

❌ Execution risk in scaling large generator business

❌ Competition from global giants like Siemens & Mitsubishi

🎯 My View:

This isn't just a generator company anymore.

⚡ AI needs data centers.

⚡ Data centers need power.

⚡ Power plants need generators.

TD Power sits right in the middle of that value chain.

A company quietly benefiting from one of the biggest infrastructure themes of the decade. 👀

⚠️ Not a recommendation. Do your own research.

📌 Stock Under Watch: Shadowfax (Emerging Logistics Play)

Business Model:

Shadowfax is a tech-enabled logistics platform powering e-commerce and quick commerce deliveries across India — handling everything from parcel shipping to same-day delivery and reverse logistics.

🧠 Why it’s interesting:

• Riding the massive tailwind of e-commerce + quick commerce growth

• Rapid market share gains (aggressive scaling vs incumbents)

• Clear shift from loss-making → profitable scale (operating leverage kicking in)

📊 Key positives:

• Revenue growth ~70%+ YoY with order volumes doubling

• Profit inflection: PAT scaled sharply as margins improved from ~1% → ~4–5%

• Strong network expansion (pan-India reach + rising delivery partner base)

• Increasing contribution from higher-margin segments (hyperlocal, value-added services)

⚠️ Risks:

• Thin margins — small cost shocks can impact profitability

• Hyper-growth may normalize as competition reacts

• High dependence on e-commerce ecosystem demand

🎯 My view:

This is a classic scale game turning profitable.

If execution sustains, it can become a core logistics backbone of India’s digital economy.

Watching closely for long-term potential — especially margin trajectory and market share sustainability.

Not a recommendation. Do your own research.

📈 Been in the markets for 2 years now, and one thing I've learned:

🚀 A great company in a bad industry can struggle, but even an average company in a sector with strong tailwinds can create wealth. 💰

📊 That's why understanding industry trends is just as important as analyzing the company itself. 🎯

📌 Stock Under Watch: MTAR Technologies

Business Model:

MTAR manufactures high-precision components used inside nuclear reactors, fuel cells, aerospace, and defence systems.

👉 Not end products — but critical parts that cannot fail

🧠 Why it’s interesting:

• Order book: ~₹2,580 Cr vs ₹876 Cr revenue → strong visibility

• Clean energy dominates (~70% revenue / ₹615 Cr) → riding fuel-cell growth

• Capacity expansion: 8,000 → 30,000 units (~4x) → strong demand visibility

• Nuclear orders: ₹500+ Cr → segment turning meaningful

📊 Key positives:

• Revenue: ₹876 Cr (FY26)

• EBITDA margin: 19.5% → target ~24%

• Operating cash flow: ₹197 Cr → improving cash conversion

• ROCE: ~17.2%

• Working capital days: 267 → 172 (major improvement)

⚠️ Risks:

• Customer concentration: 70% from clean energy segment

• Aggressive growth target: ₹876 Cr → ~₹1,600 Cr (execution critical)

• High dependence on fuel-cell demand cycle

• Execution risk in scaling capacity rapidly

🎯 My view:

This is a high-growth engineering + clean energy story but the real outcome depends on whether the company can execute aggressive growth without hurting margins or cash flows

Not a recommendation. Do your own research.

🚨 This “unknown” engineering company is sitting on a ₹2,580 Cr order book… and targeting ~80% growth

Stock may seem overvalued.

But the numbers are hard to ignore 👇

⚡ Order book: ₹2,580 Cr vs ₹876 Cr revenue

⚡ Growth guidance: 80% YoY

⚡ EBITDA margin: 19.5% → targeting ~24%

⚡ Clean energy contributes 70% of revenue

⚡ Capacity expansion: 8,000 → 30,000 units (~4x)

And here’s what makes it interesting:

⚡ ₹500+ Cr nuclear orders already in hand

⚡ Aerospace moving from prototype → volume production

⚡ Working capital days improved: **267 → 172

And the real story?

👉 This is not just engineering — it’s a clean energy + nuclear manufacturing play scaling fast

If execution holds, this kind of setup can change how the market values the business.

Will discuss this today.

🚨 **This “boring” industrial stock is sitting on a ₹1,940 Cr opportunity

It doesn’t look exciting.

No hype. No buzz.

But the numbers tell a very different story 👇

⚡ Order book: ₹1,228 Cr → ₹1,940 Cr (+58%)

⚡ Revenue growth: +38% YoY

⚡ EBITDA growth: +53% YoY

⚡ A hidden segment delivering >20% margins

⚡ Quietly entering global energy supply chains

And here’s the part most people miss:

👉 The business is shifting from a

heavy capex phase → cash generation phase

That’s where valuation re-ratings usually begin.

Will Discuss This Today

🚨 **This “boring” industrial stock is sitting on a ₹1,940 Cr opportunity

It doesn’t look exciting.

No hype. No buzz.

But the numbers tell a very different story 👇

⚡ Order book: ₹1,228 Cr → ₹1,940 Cr (+58%)

⚡ Revenue growth: +38% YoY

⚡ EBITDA growth: +53% YoY

⚡ A hidden segment delivering >20% margins

⚡ Quietly entering global energy supply chains

And here’s the part most people miss:

👉 The business is shifting from a

heavy capex phase → cash generation phase

That’s where valuation re-ratings usually begin.

Will Discuss This Today