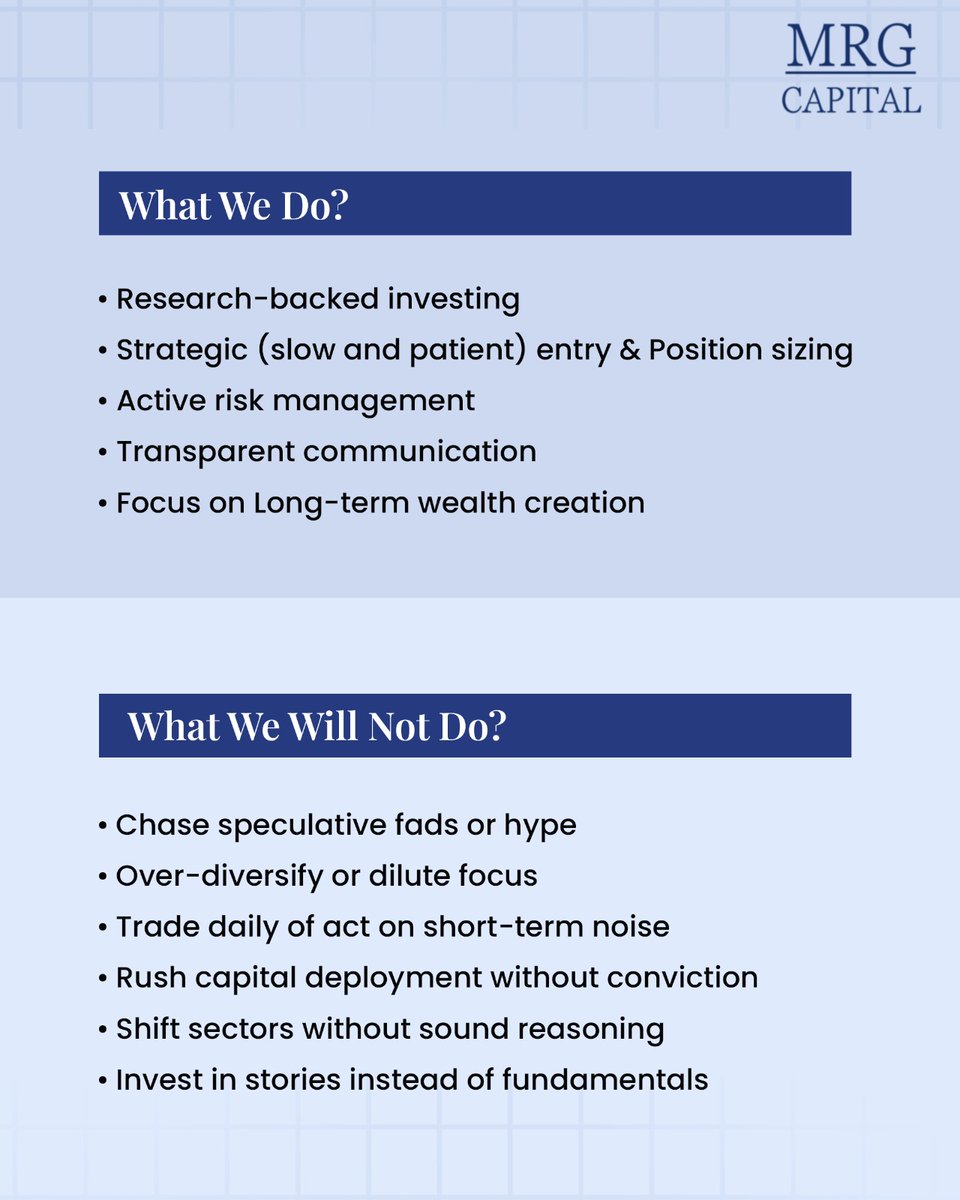

Narratives and Stories fade.

Discipline and Fundamentals endure.

MRG Capital’s PMS strategies, Wealth Maximizer & Wealth Enhancer have been ranked among the Top 10 performing strategies in the Country.

In a period where Indian markets remained range-bound and many active portfolios struggled to generate meaningful alpha, strategies built on valuation discipline, risk filters, and patience stood apart.

Not the result of chasing themes and being greedy

But of adhering to process patiently.

Because markets eventually reward discipline.

The Nifty 50 is down over 10% in six months and most Flexicap funds are in the red.

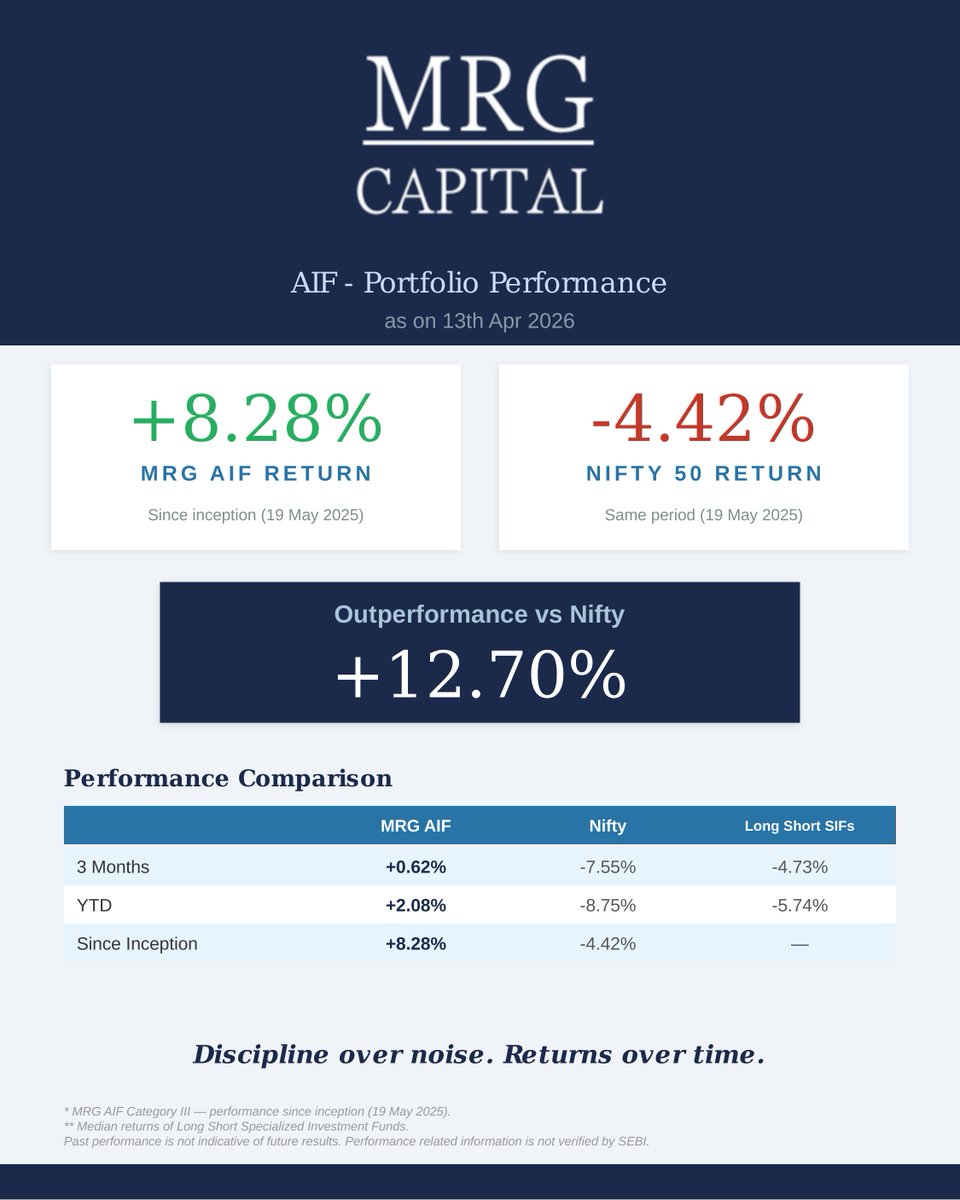

MRG Capital's PMS is up 4.4% on the year and has compounded at 18.4% over three. Our AIF, just past its first anniversary, is up 8.7% since inception, while the Nifty is down 6.3%.

No unnecessary churn. No FOMO. No theme of the month.

Just conviction in what we own and patience for it to compound.

Built to hold. Even when markets refuse to..

The Nifty 50 is down nearly 6% over the last three months and almost 8% year to date. Most Flexicap funds are sitting in the red.

MRG Capital's PMS is roughly flat over three months and up over 10% on the year (YOY).

Our AIF, in its first year, is up close to 8% since inception, with a churn rate of less than 2%.

because....

-We refuse to chase trends

-We refuse to be FOMOed into deploying in a hurry

-And we don't pretend to be disciples of Buffett & Munger while destroying the very values that they have professed over decades.

"Built on process. Measured in outcomes"

Markets bounce. Markets fall. Through both, our process stays constant.

MRG Capital's PMS has outperformed the Nifty 50 by over 10 percentage points on a 3-year CAGR basis. Our AIF, less than a year old, is ahead by ~13 percentage points since inception.

Not because we predicted the cycle - but because we never tried to.

Process and patience compound over time. Chasing momentum and hoping for supernormal returns rarely does.

...Because in the end, markets reward discipline.

When markets fall, portfolios reveal their true character.

The Nifty 50 fell 11.1% over 3 months and most active strategies struggled to contain the damage...

MRG Capital's PMS and AIF stayed the course.

Process and patience pays over time. Chasing themes and greed for supernormal returns almost always destroys capital.

...Because markets eventually reward discipline.

The Illusion of a Floor/Bottom/Support – In case the SIP Shield Cracks

And a call for a tribute to the market legend Siddhartha Bhaiya of Aequitas

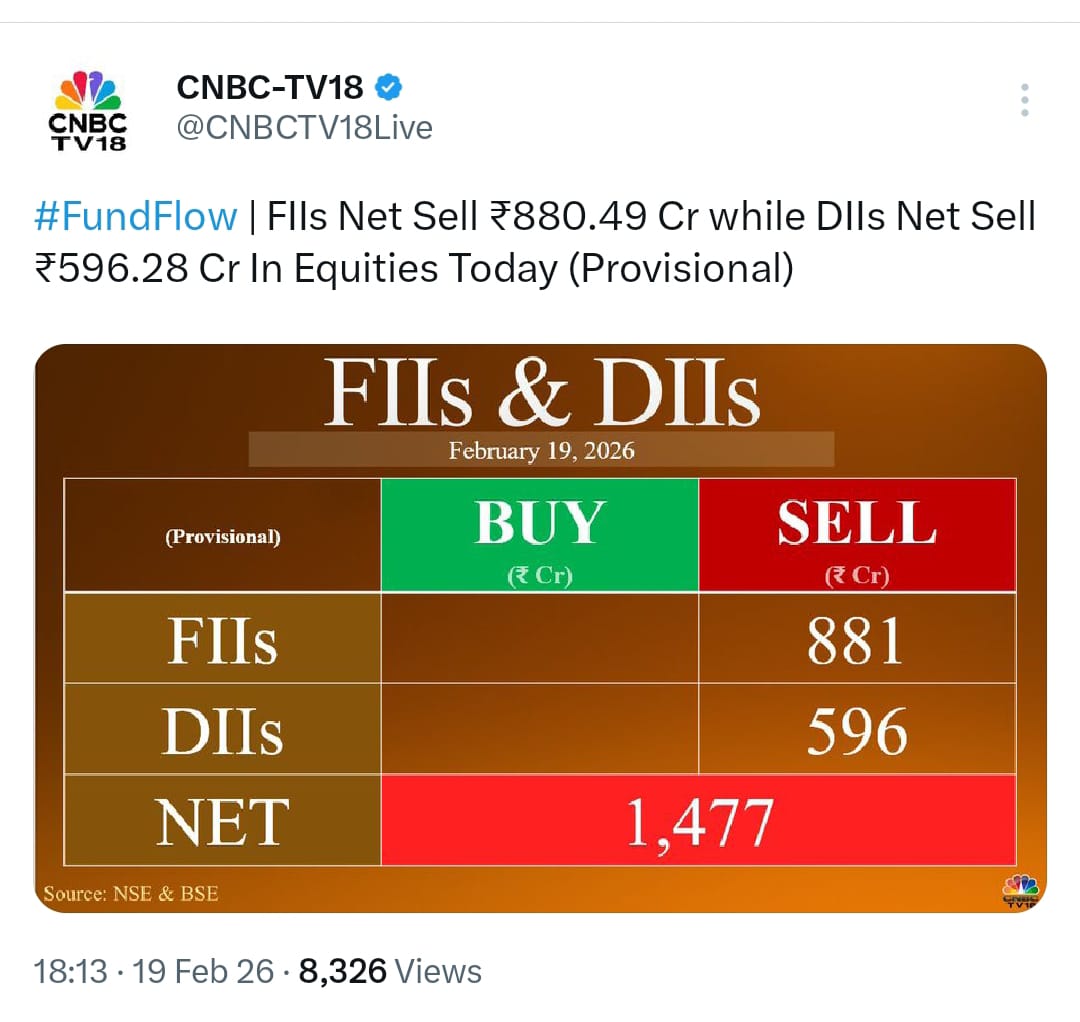

Yesterday's (19th Feb) market action was a sobering reminder of just how fragile India's equity rally has become.

Despite a combined FII and DII net selling of a mere ₹1,477 crore, which is barely 0.0018% of the mutual fund industry's ~₹81 lakh Cr AUM as of Jan 2026 and just about 5.9% of the ~₹30,000 Cr monthly SIP inflows recorded last month, Nifty and Bank Nifty plunged nearly 1.4%. A negligible ripple in the ocean just erased billions in market cap.

Investing in India has transitioned from a financial decision to a "demonstration of patriotism." In reality, the FIIs just need to "NOT SELL", and indices soar. These flows are peanuts in the grand scheme, yet they are swinging the markets wildly.

For 5 years, the middle-class SIP machine has powered Indian Markets to stratospheric heights under the banner of "financialization of savings" But what happens if a global headwind sparks even a modest 5-10% redemption from that ₹81 Lakh Cr AUM?

Where is the counterparty?? Who is the counterparty?? SADLY - THERE IS NONE

Domestic buyers (retail + institutions) have been the nonstop fuel. But in a true exodus, FIIs - who've been net sellers of barely ~2-3% of their total holdings so far over 5 years (cumulative outflows ~₹98K Cr) could flee faster, creating an unfillable vacuum.

No counterparty implies - no floor, no bottom, no support. Slides could accelerate unchecked.

With a counterparty (or lack of it thereof) risk, Indices could easily retrace 30-50% or more. We are trading at a forward P/E of 22x - one of the world's most expensive markets - while peers like China (12x) and Brazil (11x) come across as markets on fire sale.

What's more concerning is that our economy isn't producing cutting-edge, global-problem-solving companies to absorb this capital deluge. Instead, we are creating sub-optimal firms in a hyper-competitive environment (food delivery, resellers, etc.), that are gulping and then burning funds at nosebleed valuations.

Ironically, Swiggy - a recent market darling came out with a QIP barely a little after its IPO.

To put this a bit more succinctly -

"ब्याह की मेहंदी उतरी नहीं और चले बेइज्जत होने"

"The honeymoon isn't over, and the debaucherous scandal has begun."

These "futuristic growth" companies won't see free cashflows or dividends for years, maybe decades. The Ola, Paytm, Swiggy, Zomato, and Nykaa debacles weren't outliers. They were an example of criminal breach of retail investors' trust.

Scale that up, and you have a market built on expensive storytelling rather than fundamentals.

Institutional cheerleaders like Raamdeo Agrawal Ji of Motilal and Nilesh Shah Ji of Kotak bear some definite burden of responsibility here.

They’ve herded retail into this setup, pushing "long-term" narratives while ignoring the structural risk of the exit door.

If redemptions hit, the psychological toll on India’s new investor class (that took birth during the COVID lockdown) will be devastating. It won't just be a financial loss; it will stall the "financialization of savings" story cold.

Trust and Confidence, takes decades to build but only one liquidity vacuum to shatter.

Siddhartha Bhaiya of Aequitas who left us suddenly with an insurmountable emptiness, called out the Indian markets as a bubble of epic proportions. Let's prove him wrong by selling just just 2% of the MarketCap of India as an experiment or risk evaluation/mitigation exercise.

If we succeed in proving him wrong, he will still smile in his abode up there - as markets will stay safe, as will the retail investors ......

Is it time to question the dream before it turns into a nightmare??

As Bob Dylan says - The answer my friend is blowing in the wind......

The Curse of the Fulfilled Wish

And the ‘ass’umed demise of the Indian IT sector

My mother used to tell me often, with a sense of profound wisdom: "बेटा हमेशा सोच समझ कर बोलो क्योंकि कभी-कभी बोलने के समय सरस्वती जुबान पर बैठी होती हैं."

(Be careful what you utter, for sometimes the Goddess of knowledge and truth sits on your tongue and makes it come true).

In the world of investing, we call this the "Beware of what you wish for" syndrome. We often pray for market corrections and make predictions to sound futuristic and visionary – fooled by randomness - obviously. Most of it is done either to gather AUM or attract attention.

And these predictions, sometimes, when they do come true, the world is so broken that we no longer have the courage - or the capital - to click the 'buy' button.

Yesterday, I was keenly listening to a celebrated fund manager on CNBC. He was visibly chuffed, as he discussed the "inevitable downfall" of the Indian IT services industry. More so because he’s been bearish on the IT sector for a while.

His thesis is internally and strongly validated by the rise of AI (Artificial Intelligence), and it (the thesis) recently got strengthened by the rout caused in the AI space by the rise of Anthropic.

Indian IT sector is a $250 billion (in annual sales) behemoth that India has built since 1995. It has created the largest wealth in Indian history for the nation, corporations, and individuals. It is now being touted as a sitting dinosaur waiting for the AI meteor.

People who are enthusiastically writing the obituary of Indian IT may feel empowered by their "first-level thinking" as the idea - that a machine can code, will obviously make the coders and Project Managers dispensable.

But here is where the incontrovertible trust in one’s own intellect becomes dangerous. As investors and fund managers, if we aren't doing second and third-level thinking, we aren't managing wealth; we are just managing egos.

Let's analyse what happens if this "Saraswati" moment does come true and the Indian IT industry, which contributes nearly 8% to 10% of our GDP, actually collapses.

Since the mid-90s, IT hasn't just been a sector; it has been the backbone of India’s middle-class prosperity. Experienced (3-5yrs) IT professionals’ median pay of 10-20 lacs p.a dwarfs the median pay in other sectors like Manufacturing (4-5 lac), Retail (3-4 lac), Agriculture (2-3 lac), Banking (8-12 lac) and Healthcare (6-8 lac).

This industry earns over $200 billion in annual exports, which has catalyzed a ‘Bay Area’ type of prosperity (Minus the infra and the potholes ofcourse!) in the streets of Bengaluru, Hyderabad, Chennai, Gurgaon, and Pune.

These five or six "Tech Republics" are the fiscal lungs of India. These 7-8 cities alone contribute nearly 25-30% of India’s total GST collections.

Bengaluru, Chennai and Hyderabad aren't just cities; they are the primary engines for the Government’s Income Tax pool.

Now, apply second-level thinking. If the "IT dinosaur" dies, who pays the EMIs? The ~5.4 million people directly employed by the IT industry are the primary customers for the Real Estate industry (which is the collateral for our entire banking system). They are the ones fueling the Automobile sector, buying SUVs on leverage. They are the real and frequent users of Zomato and Swiggy. Data suggests that these top 8 cities contribute roughly 60-70% of the Gross Order Value for these platforms.

If the IT professional stops ordering, Zomato isn't a "growth story" anymore; it’s a case study in terminal decline. The "Cab Industry" vanishes. The pubs in Indiranagar and the malls in Gurgaon go silent. The hospitality industry (celebrating its resurgence after nearly a decade of sluggish and indebted performance since the GFC in 2008), The Aviation Sector, and the high-end credit card spends – Nearly everything is a house of cards built on the monthly credit and spending power of an IT professional’s salary.

To be chuffed about the prediction of the downfall of IT because of AI, and a new AI tool is like cheering for the shutdown of a coal mine while living in a town powered by it. You might get rid of the soot, but you’ll also lose the lights, the livelihoods, and the very foundation of the town’s survival.

We must have the maturity to realize that we are all "prime investors" in each other’s survival in an interconnected web. If you are a fund manager betting on "Consumption," you are indirectly betting on the survival of the very IT companies you are currently "shorting" in your mind. True vision demands maturity: second-level thinking weighs immediate impacts, third-level anticipates rebounds or adaptations.

And if the Indian IT industry is really in danger and facing obsolescence, you should be dramatically bearish on the sectors such as - Automobile, Hospitality, Food and Beverage, Real Estate, and the Banks.

After all, as Mom said, God forbid if what you say truly manifests…….well, you know!!

Is it the end of the Road for Silver and Gold?

Conviction is tested only in drawdowns but never in rallies.

And that forms the bedrock of the cliched statement - Buy when there is blood on the street, but the blood better not be yours.

I've been investing in precious metals since 2021. It took me six months of reading, tracking mine production, annual supply degrowth, and rising demand before I built my first real position on the 6th September 2021. Since then, I've followed the data closely every day.

My rule is simple:

Only take positions where your conviction is so strong that you could possibly go all-in. If it's not, you're just gambling, no matter how much you call it - "diversification."

Yesterday, Silver was down about 30% and gold 10% from recent highs. Here's the psychology everyone faces: We all dream of buying assets 30-40% cheaper. But deep down, we want prices to stay high forever. We crave the dip to buy low, and expect prices move up from the day we bought. That's human nature.

Gold and silver have been used as money and a store of value for over 6,000 years. Fiat currencies, on the other hand, are experiments backed by debt. The US moved away from the gold standard in 1933 domestically and 1971 internationally, because infinite debt could not coexist with monetary discipline. And therefore, the petrodollar came into being.

History is very clear on one thing: Every Fiat currency eventually collapses. (Ray Dalio’s take makes it very clear in one of his now very famous videos)

The only uncertainty is timing, whether the Fiat currencies will collapse slowly or suddenly.

And whether we are at the end of the Fiat system today or not - maybe not yet.

But are we moving towards it faster than ever before - Definitely Yes!!

So decisions to buy, hold, or sell precious metals should not be driven by daily price moves, but by your understanding of history, monetary systems, and your own temperament.

Retail investors can't slam prices like this. Over the last 10 years, big banks paid $1.3 billion in fines for spoofing Silver (data is all online).

Yesterday, with China closed and late LME trading, the "Big Boys" likely dumped to spook you out, clearing shorts or loading longs.

Its pertinent to ask a question:

When LME trading was thin and China was shut, who really slammed the price? It wasn’t retail. Price shocks often serve one purpose: scare weak hands, so that large players can exit shorts and quietly build long positions.

This fact is worth noting:

For every ounce of physical Silver available, there are about 400 ounces traded on paper. For Gold, it's around 200 paper ounces per physical one.

Inventories at metal exchanges around the world are depleting fast.

Those recent exchange outages? They're not about power failures or server cooling issues, but it's about the exchanges struggling to meet contractual obligations as paper contract holders are starting to demand physical delivery, and the system can't keep up with that.

Can prices fall more? Sure, they can. Position size is personal, tied to your conviction and biases.

But fast-forward 10 years: Gold at $10K, $15K, or $20K? Silver at $300 or $500? and y0u'll kick yourself for getting shaken out by “The Pros” who do this for a living.

Or keep buying the dip on Nvidia, Google, Amazon, Zomato, Trent, Polycab, all at unsustainable earnings (PE) ratios.

Eventually, your fortune will be the sum total of the choices you make today.

Fun Fact: Respectively, Silver and Gold are still up 270% and 140% in the last 2 years.

Silver Gold Nifty BankNifty Nasdaq DowJones

All three MRG Capital PMS strategies rank among India’s Top 10, as reported by The Economic Times.

Wealth Maximiser

Wealth Enhancer

Wealth Protector

This outcome is not driven by chasing trends or taking excessive risk, but by patient adherence to discipline and to fundamentals of value investing.

Markets reward discipline over time.

The same discipline underpins our AIF platform.

Article link in the thread.

Here’s to New Hopes that inspire,

New Goals that excite,

New Memories that warm the heart,

&

New Beginnings that light the way.

May 2026 be extraordinary for you and everyone in your family ✨

Happy New Year!

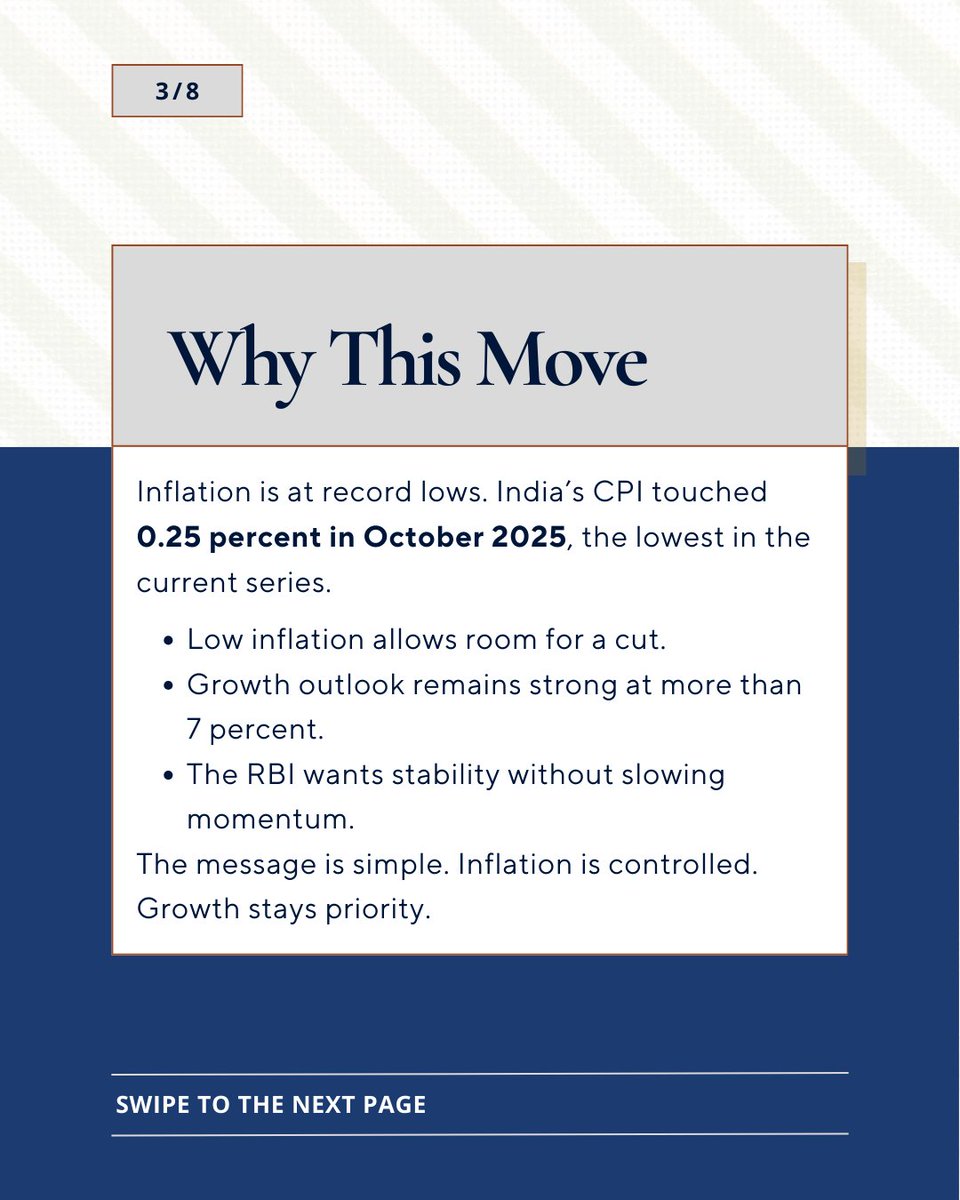

Loan relief or slower savings?

The RBI’s 25 bps rate cut marks a clear shift. See how this move affects your EMI and FD returns. Swipe for the breakdown ➡️

#PersonalFinance#MoneyMatters#InterestRates

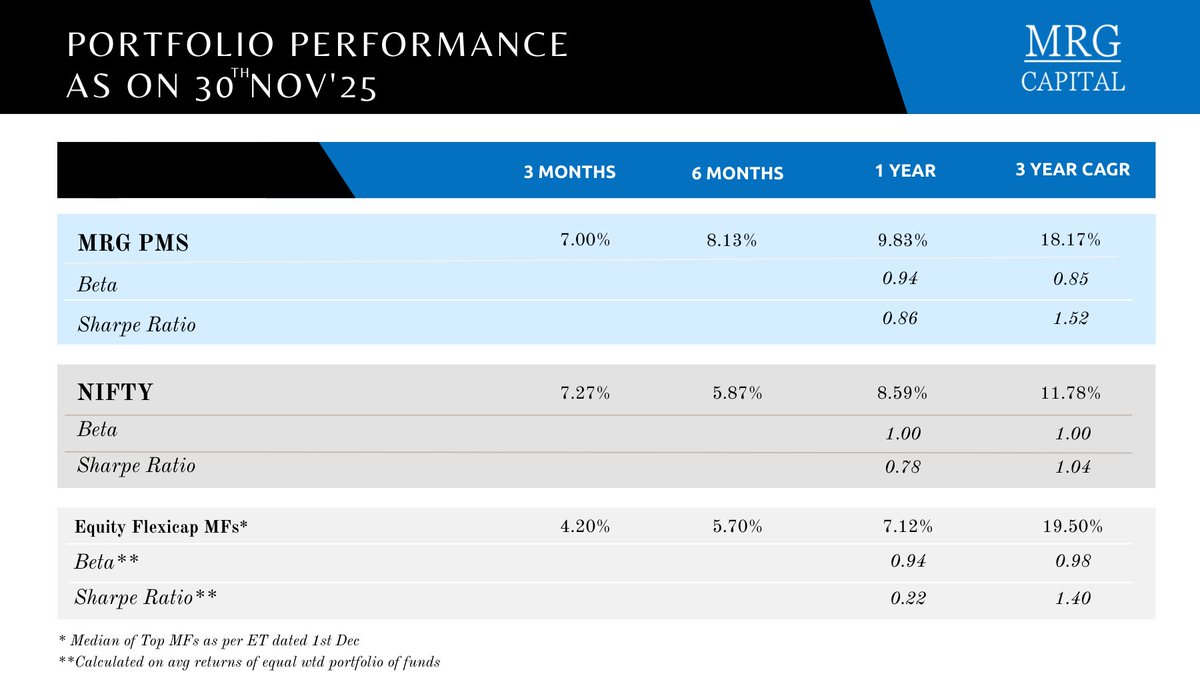

Consistent returns and stable portfolios define your experience with MRG PMS. The latest data shows stronger risk-adjusted return, lower volatility, and steady performance across time frames.

MRG builds this through discipline, balance, and deep research. Your wealth grows through structure, not noise.

USDINR

We’re all looking at the rupee, but the real story lies in global bond markets that are already cracking.

Check out our founder @manurishiguptha’s take to see the full picture.

USDINR

Rupee’s recent fate vs the dollar is memeable - especially when you revisit the chest-thumping tweets from 14 - 15 years ago by people who are now conveniently missing.

But honestly, that’s the least of the worries.

The real 9 - richter quake (already in progress) is in the Japanese bond yields.

Deep under the global financial ocean, the tremors from that quake haven’t even begun to hit the surface.

Fretting about the INR right now is like obsessing over a scratch on your car while you’re overspeeding on a freeway with a cracked axle, overheating tyres, and brake pads already burning.

Interesting times.