@proof_of_thermo Damn, I guess NVDA is also going back down -90%, first to $30 to fill that big gap from May 2023, and then to $20 to fill the gap from Feb 2023. Gonna load the boat then.

$GANX Gain Therapeutics able to return functions with Parkinson's drug GT-02287

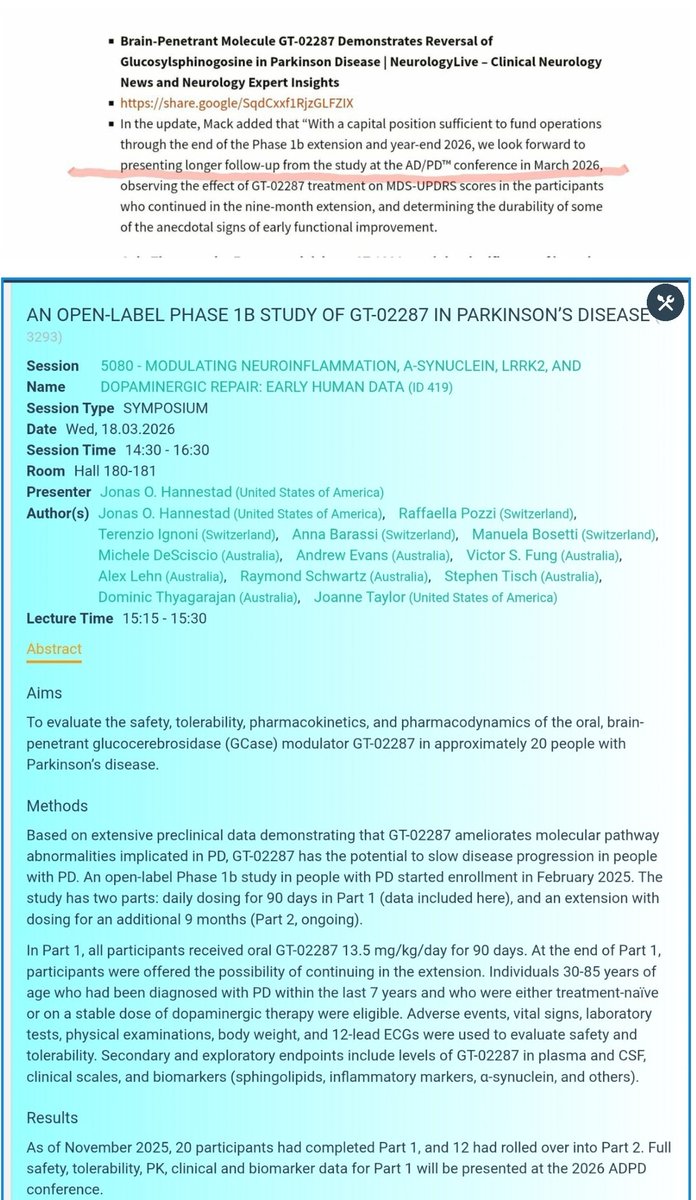

Most common benefits reported by study participants include meaningful improvements in specific functional areas such as smell and taste, sleep, and balance or gait

https://t.co/HrMBfI4hYJ

$IREN Development White Paper

This is the first time IREN CEO Daniel Roberts has published a continuous long-form statement comprehensively explaining IREN’s development direction and positioning. I would call it IREN’s “Development White Paper,” or even a “Strategic Manifesto” for a global AI infrastructure platform.

As an investor in $IREN, the following points deserve particular attention, in no specific order of importance:

First, IREN positions itself foremost as an organizer of infrastructure for the AI industrial era, deliberately downplaying the GPU itself, with the ultimate goal of transforming from an ��asset company” into a “platform company.”

This redefines IREN from being merely an “owner of compute” into an organizer of infrastructure. Compared with the past identity of a bare-metal supplier, this represents a leap upward by several levels. For the conductor of a perfect symphony, every component matters. Once a company truly possesses orchestration capability, enterprise-grade support systems, deployment toolchains, and the ability to integrate into customer workflows, the role it plays fundamentally changes. It is no longer simply an “infrastructure provider”; it begins evolving into a “platform organization.”

And once a company enters the platform paradigm, its valuation framework changes as well. The value logic of platform companies is fundamentally different from that of traditional asset-heavy companies. Asset companies depend on a linear relationship between input and output, while platform companies rely on network effects, ecosystem stickiness, deep integration into customer workflows, and the compounding effects generated by cross-layer capabilities.

This is how IREN defines its own future positioning, and these are also the key elements associated with the highest valuation frameworks.

Second, “compute does not merely satisfy demand — it creates demand.”

IREN’s management has explained to investors with remarkable clarity what kind of future they are building and what its value proposition truly is. This is a super self-reinforcing compounding model in which the more infrastructure is built, the more demand is created. This compounding effect comes not only from demand generated within the industry itself, but also from entirely new forms of external demand. At the same time, these forces reinforce one another. This may represent a growth phenomenon unlike anything seen before in human industrial history.

In the past, growth on this scale required an entire interconnected industrial ecosystem working collectively. Today, a single company can potentially achieve it — but only if it possesses extraordinary foresight and vision, beginning operations eight years in advance in order to have any chance of controlling such a phenomenon. Once this self-reinforcing compounding growth model takes shape, it can evolve into an incomparable giant enterprise. It cannot be replicated, imitated, or reproduced, nor can there be a second company like IREN, because the scarce physical infrastructure required no longer has alternative options available, and the time window necessary to build it has already closed.

Up to this point, no industry has existed where its own growth simultaneously lays the foundation for its next stage of growth. This can no longer simply be called a spiral upward cycle. It is an interactive feedback-driven compounding system, almost resembling a chain reaction in the atomic world.

Third, by drawing lessons from the growth process of Amazon Web Services, IREN aims to build a full-stack cloud platform for the AI era.

Amazon first built an irreplicable heavy-asset system consisting of global warehousing, logistics, servers, electricity, networking, and operational infrastructure. Only afterward did it abstract “the cloud” from those underlying assets. The true winners of future AI Cloud will not be “the smartest people at the software layer,” but rather “those who first control global physical AI infrastructure.”

Fourth, the essence of the partnership with NVIDIA is to turn DSX into the future standard for AI factories.

IREN is one of the global physical deployment platforms for DSX. I have already provided an extremely detailed argument for this point in the pinned article on my personal account.

Fifth, the window for becoming an AI platform company is rapidly closing.

“The future software opportunity will always exist,” but “the window for deploying hundreds of thousands or even millions of GPUs will close.” The AI infrastructure industry is not a slow-growth industry. It is an industry in which the winners will be rapidly determined over the next few years.

The reason is very simple. Power resources are finite. Substations are finite. Grid connection timelines are finite. GPU allocation capacity is also finite. Meanwhile, customer migration costs will continue rising, and operational track records will gradually form trust barriers. Together, these factors constitute the early stages of a classic platform network effect.

Once that network effect truly forms, latecomers will not merely face “difficulty catching up” — they will become fundamentally incapable of catching up. Resources will already be locked up, customers bound into ecosystems, operational records solidified, and supply chains occupied. The industry structure itself will crystallize within a short period of time. The essence of the window period lies in the moment when resources, time, and trust converge to determine who can become a core node of the global compute platform.

This is a generational opportunity, not a cyclical industry where participants can afford to wait patiently. Whoever can truly deploy hundreds of thousands or millions of GPUs over the next few years will hold the structural advantages of the entire industry for the next ten or twenty years. This is the underlying logic explaining why light-asset models will ultimately reinforce the compounding advantages of vertically integrated heavy-asset models. Time will prove that the overwhelming majority of value creation will ultimately flow toward vertically integrated models, because they deliver the lowest costs and the highest efficiency.

In the future, light-asset models may survive only as complementary or redundant participants. Even if companies recognize this issue today, it is already too late to transform. It is no longer realistically possible, because all scarce resources have already been occupied.

This fundamentally redefines what true full-stack ownership really means. This window period is a one-time event.

Sixth, IREN intends to satisfy the needs of all users through a global AI platform.

This white paper emphasizes IREN’s international expansion strategy and, for the first time, informs the public that IREN’s potential power application pipeline is several times larger than 5GW. More importantly, IREN aims to serve every type of customer with compute demand — completely covering all use cases. Whether users prioritize latency, data sovereignty, green energy, compliance with local regulations, or simply whether compute exists anywhere available, IREN intends to satisfy all of those requirements. At present, this is a uniquely global positioning.

Seventh, this is why brand-building is now being emphasized so heavily.

As an international AI sovereign platform, IREN hopes to establish a kind of first-principles brand presence. When people go shopping, the first thing they think of is Walmart or Costco. When buying soft drinks, they think only of The Coca-Cola Company and ignore alternatives. When visiting a theme park, they choose The Walt Disney Company. When taking a cruise, they look only at Costa Cruises. In the future, when customers need compute, IREN wants to become the first choice.

Eighth, IREN is transforming from a cyclical industry participant into a “national-level infrastructure narrative.”

European data sovereignty, Asia-Pacific AI shortages, global regional deployment, power grids, compliance, physical infrastructure, AI factories, and enterprise-grade reliability — together, these elements indicate that IREN is evolving toward becoming “the next-generation global AI infrastructure layer.”

A national-level infrastructure platform is fundamentally a different valuation species from a traditional data center company. The value of the former comes from strategic positioning, resource scarcity, irreplaceability, and long-duration stability across cycles. The latter relies far more heavily on asset returns and supply-demand cycles. What IREN is attempting to unlock is precisely this higher valuation ceiling.

Finally, IREN’s execution phase to become a global compute platform is happening within roughly the next 30 months.

If the window period is lost, it will never return. And if execution during this phase fails, the outcome will be significantly diminished. As a result, IREN’s management clearly understands what must take top priority in order to secure this position, and they are steadily implementing it step by step. Most importantly, the critical foundational deployments have already been completed.

The previous perception that IREN struggled to communicate effectively with the market existed largely because building such a system required more execution focus and a certain degree of confidentiality. Now that the system has reached the stage where its core foundational elements are largely in place, IREN will begin appearing before customers, industry participants, and investors in an entirely new form.

To support this transformation, IREN even acquired a professional advertising and communications coordination company, preparing to present itself with a completely new image in both brand development and investor relations.

Daniel Roberts’ unprecedented series of long-form statements today is the declaration of this new era.

Gain's 1b data is showing that over 50% of Parkinson's patients have a toxic lipid that is elevated and which is known to cause multiple downstream issues, including aggregation of the infamous a-synuclein. GluSph is the same lipid that is central to Gaucher's disease, which shares key similarities to GBA1 Parkinson's. In Gaucher's, but reducing GluSph, they've effectively been able to stop progression of the disease. But those Gaucher's treatments do not cross the blood-brain barrier. GT-02287 does.

GT-02287 successfully reduced this toxic lipid (GluSph) by an average of 81% in 100% of those patents who had elevated levels. And what they've found, unsurprisingly, is that by reducing this toxic lipid, these same patients experienced improved motor function as per UPDRS assessments. Improved, not just "slowed progression". Patients also reported improvements in areas like sense of smell.

IMO, the Gain team is underselling what they've accomplished. GT-02287 is showing disease modification, which would be a first in Parkinson's disease.

$GANX Gain Therapeutics on NPR this week and presenting Phase 1b Parkinsons data at GBA1 Conference on Friday.

BioTech Nation ... with Dr. Moira Gunn | A Different Way to Treat Parkinson's...Dr. Jonas Hannestad & Dr. Joanne Taylor, Gain Therapeutics

https://t.co/sOtj19Yhrv

$GANX remains my biggest position. I don't know when a deal happens, but I am very confident that it will happen. The science is my conviction here. I had hoped that a deal would have been done already, but as the extension study continues to show durability, while at the same time the science community converges on the importance of Gcase in the lysosome, ER, and mitochondria, the inevitability of a deal becomes more of a certainty in my mind. Hopefully it is pre-phase 2, but if it is post-phase 2, the value of the drug goes from ~$1-2 billion to multiples of that.

@genaue1263 Many options that don't result in dilution. Not saying dilution isn't a possibility, but we don't know what discussions are taking place behind the scenes and which companies are watching the extension study closely for further evidence of durability.

$GANX Gain Therapeutics. Recent scientific article validates Gain's approach that increasing GCase can slow, stop and maybe reverse trajectory of Parkinson’s.

https://t.co/skvEDXOq7w

“The data from our Phase 1b study furthers our hypothesis that GT-02287 is among the first disease-modifying therapies promising to shift the treatment paradigm in PD from symptom relief to halting or slowing symptom progression, targeting the causative biology (or pathophysiology) of PD to enable a more durable and predictable treatment effect for those living with PD.”

From today's press release. There are no therapies for Parkinson's that are disease-modifying, and companies are very careful about using "disease-modifying" in their press-releases, especially in the context of the above statement by the CEO. The data fully justifies this statement IMO, and if anything, they are still being conservative with their wording.

@MWB741 $GANX Gain Therapeutics

Great article. Here is a bunch of recent research.

Gain Therapeutics(GANX): KOL Reports : GT-02287 Shows Signs of Disease Modification

https://t.co/jko65tS302

This was a small, short-duration study-- only 90 days-- and it was not powered for statistical endpoints. The subgroup wasn't random. GluSph was pre-specified and the main focus since it (1) reflects target engagement and (2) is known to drive a-syn aggregation, lysosomal and mitochondrial dysfunction, and ER stress. That they were able to show statistical significance in only 90 days in this (large) sub-goup is pretty amazing.

In yesterday's Oppenheimer event, the CEO also mentioned that they'll be revealing another biomarker reduction that correlates with this same group, DOPA decarboxylase, which would mean some level of normalization of the dopaminergic circuitry. More strong evidence of disease-modification.

$GANX Update on Gain Therapeutics

First, a short summary on what Gain Therapeutics is trying to do in aiming for “disease-modification”… most Parkinson’s treatments help manage symptoms like tremor or stiffness, but they do not slow the disease itself. A disease-modifying therapy is different. It aims to slow, stop, or even partially reverse the underlying disease process, not just mask symptoms.

Today, there are no approved disease-modifying treatments for Parkinson’s disease.

Gain Therapeutics ($GANX) believes its drug candidate GT-02287 is showing early signs of disease modification — which, if confirmed in larger studies, would represent a major breakthrough not only for Parkinson’s, but potentially for related diseases such as Lewy body dementia, Gaucher disease, and possibly Alzheimer’s disease.

February Corporate Update:

Gain released an updated corporate deck recently (link in comments), and there are two Phase 1b findings that greatly change the risk profile going into Phase 2:

GluSph reduction (upstream biological signal) About one-third (maybe more) of patients entered the Phase 1b with elevated CSF glucosylsphingosine (GluSph), a toxic lipid linked to dysfunction in Parkinson’s (and Gaucher’s disease). In this subgroup, 100% of patients saw GluSph reduced toward normal, with an average ~81% reduction after 90 days on GT-02287.

Statistically significant functional improvement That same GluSph-elevated subgroup also showed a statistically significant improvement in combined MDS-UPDRS Parts II + III, with a mean improvement of 6.17 points (p < 0.05). This was actual improvement, not just “less worsening,” and it occurred over ~90 days — which is unusual for programs aiming at disease modification in PD.

The “statistical significance” means that within that GluSph-elevated subgroup, the probability that the observed UPDRS clinical improvements occurred by chance alone is less than 5% (p < 0.05). In other words, If GT-02287 had no real effect in that GluSph-elevated group, the probability of observing an improvement this large (or larger) purely by chance is less than 5%.

This reduction in GluSph and link to clinical improvements has never been seen before in Parkinson’s patients. If 30% is representative of the number of Parkinson’s patients who have elevated levels of GluSph, this is a giant number. Importantly, it also does not mean (1) that patients who do not have elevated levels will not develop elevated levels in the future, and (2) that GT-02287 would not be beneficial to individuals who do not have elevated GluSph levels. This (very large) sub-population simply looks like low-hanging fruit.

For phase 2, this matters because:

• It links mechanism to biomarkers to function in humans, not just animals

• It identifies a defined responder population, which allows for clear phase 2 planning and setting it up for success

• It reduces reliance on noisy, purely clinical endpoints by anchoring outcomes to GluSph

• It lowers the chance of a “clean safety but messy efficacy” Phase 2 readout

This is what big pharma teams look for when assessing whether early PD signals are real or just statistical noise. The company is explicitly framing this as “translation” from animal models to clinical success in humans. Upstream correction of cellular dysfunction with a strong correlation to functional benefits.

CEO Gene Mack succinctly summarized what they are seeing with GT-02287 in a BioSpace interview a few weeks back:

“Rather than simply trying to boost enzyme activity in the lysosome, GT-02287 stabilizes GCase folding and trafficking throughout the cell, restoring function across multiple compartments, including those critical to mitochondrial health. That matters because Parkinson’s can be seen as a disease of cellular stress, impaired waste clearance, and energy failure.”

16 out of 19 of the patients who completed the initial 90 days elected to continue into the extension study, despite the further testing and lumber puncture. If they weren’t experiencing benefits, it is unlikely they’d choose to continue. Data from the extension will show whether improvements continue over time. They should already have the 180 day blood and UPDRS data, and judging from the CEO’s statement above, the data continues to support disease-modification.

Despite the recent surge, the share price is considerably lower than it was in mid-December pre-data release. Most people will look at this and assume that something must have been wrong. But the market gets misprices companies all the time, especially in small biotechs. To me, this is a great opportunity to buy what might turn out to be the first and most important disease-modifying drug in neurodegenerative disease history.

@LouBasenese@PhilipEtienne@RealAvidTrader@BiotechStockRsr@odibro@yaireinhorn@thebiotechforum@BiopharmIQ@BPharmCatalyst@SupNovaTrading@StocksPursuit@Microcapreturns@dixielee1969@fundmyfund @makedatbread88

@SheffStation@bwsm12702@TopStockAlerts1