We are MACAU based for local Macau NFT players.

We aims to introduce and promote MACAU to the world through this Metaverse project.

Macau, be NFT-ization!!

🚨 BREAKING: Google Gemini can now analyze any stock like a Wall Street analyst (for free).

Here are 09 insane Gemini prompts that replace $4,000/month Bloomberg terminals:

Save for later🔖

The Pentagon confronts Anthropic, demanding full access to Claude military equipment or face termination.

According to an exclusive report by Axios, the Pentagon is considering terminating its partnership with Anthropic, an AI company that insists on limiting the military's use of the Claude model and refuses to open up access to mass surveillance and fully autonomous weapons. Notably, OpenAI, Google, and xAI have all agreed to the Pentagon's "all legal uses" terms, making Anthropic the only one of the four AI labs to remain unmoved.

#Pentagon #Anthropic #ClaudeAI #MilitaryAI #AIEthics #MassSurveillance #AutonomousWeapons #OpenAI #GoogleAI #xAI #DefenseTech #AIRegulation #ResponsibleAI #TechPolicy #NationalSecurity

#macao #macau

https://t.co/2HkzYRyRW7

I genuinely want crypto to proliferate on X, but applications that create incentives to spam, raid, and harass random users is not the way.

It meaningfully degrades the experience for millions of people — only to enrich a few people.

And yes, we are launching a number of features in a couple weeks, including Smart Cashtags that will enable you to trade stocks and crypto directly from timeline.

Lightning Labs has released an open-source tool for "AI-powered agent payments" based on the Lightning Network L402 protocol, which is compatible with mainstream AI frameworks.

#AIAgents#LightningNetwork#BitcoinLightning#LightningLabs#L402#AIEconomy#MachinePayments #AgenticAI #BitcoinPayments #CryptoInnovation #OpenSourceTools #AIAutonomy #MachineEconomy #AIPayments #Layer2Bitcoin

#macau #Macao

https://t.co/CaVk8xOiwa

Wall Street is scrambling for crypto talent! Wells Fargo is hiring an executive for "tokenized deposits," and Morgan Stanley and JPMorgan are also opening blockchain positions.

Wells Fargo posted a "Head of Digital Asset Services" job opening four days ago, with responsibilities covering developing 3-5 year strategies, including tokenized deposits, on-chain collateral, intraday liquidity, and 24/7 programmable payments. Previously, Morgan Stanley and JPMorgan Chase had also been recruiting senior talent in the crypto space.

Aaccording to Frank Chaparro, project director at The Block, revealed that the three major Wall Street banks all made moves to recruit crypto talent within the same month, indicating that traditional financial institutions are shifting towards "comprehensive construction" of digital asset infrastructure.

Wells Fargo: We need someone who can bridge the gap between "traditional payments and blockchain".

Chaparro's disclosed job posting reveals that Wells Fargo is not looking for a typical blockchain engineer, but rather a senior executive capable of developing a three- to five-year strategic roadmap . The job description is extremely specific:

1. Tokenized Deposits : Representing bank deposits on-chain in the form of tokens.

2. On -chain collateral: Enables instant settlement and tracking of collateral.

3. Intraday Liquidity : Improving Capital Turnover Efficiency Through Blockchain

24/7 Programmable Payments: Breaking the limitations of traditional bank operating hours

More importantly, these on-chain services must be fully integrated with existing payment channels , including Wire Transfer, ACH, Real-Time Payment (RTP), FedNow, and SWIFT. This indicates that Wells Fargo is not pursuing a standalone blockchain experiment, but rather embedding on-chain capabilities directly into its vast traditional payment network.

Morgan Stanley creates new positions and sells cryptocurrencies using E*Trade; JPMorgan Chase opens numerous blockchain job postings.

Morgan Stanley has also been proactive. At the end of January, the bank appointed veteran executive Amy Oldenburg as its inaugural Head of Digital Asset Strategy, a newly created position. Oldenburg has served at Morgan Stanley for over 20 years, previously leading the emerging markets equities business. Her appointment marks the bank's formal upgrade of digital assets from a fringe experiment to a core corporate strategy.

Meanwhile, Morgan Stanley plans to launch cryptocurrency trading through its E*Trade platform in the first half of 2026, initially supporting BTC, ETH, and SOL, and has already submitted registration applications for Bitcoin and Solana-related ETPs. Recently, the bank has also been actively recruiting senior engineers to build DeFi and RWA (Real-World Asset) tokenization infrastructure, as well as a proprietary digital wallet expected to launch in the second half of the year.

JPMorgan Chase continues to expand its blockchain division, Kinexys (formerly Onyx), with over 24 blockchain-related job openings currently listed on Indeed and LinkedIn, covering positions such as vice president-level engineer, head of risk management, and product manager. However, it's worth noting that Naveen Mallela, co-head of Kinexys globally, left the company on February 11th after 11 years in the role. Whether this personnel change will affect the bank's blockchain strategy remains to be seen.

#wallstreet #cryptojobs #digitalassets #tokenizeddeposits #blockchain #defi #tradfi #wellsfargo #morganstanley #jpmorgan #cryptotalent #fintech #onchainfinance #rwtokenization #programmablepayments #web3 #cryptoindustry #bankinginnovation

#macau #macao

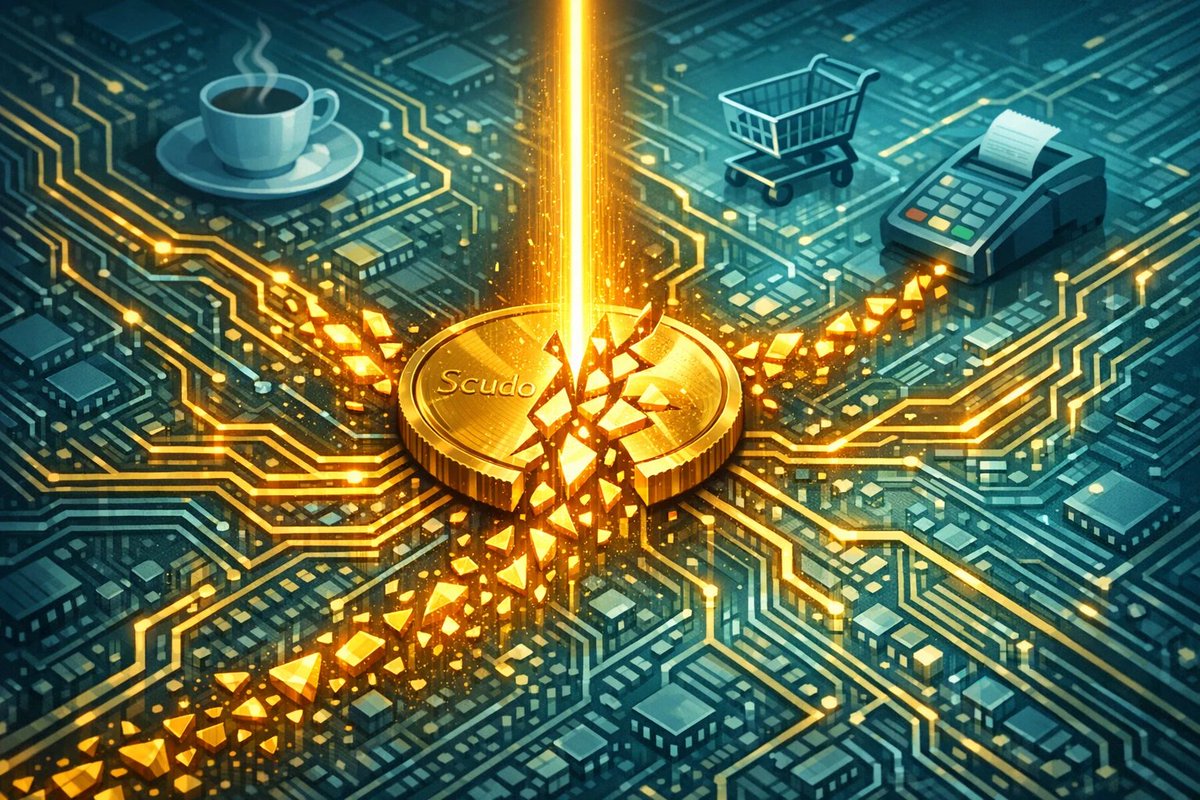

Tether's gold token XAUT introduces a new unit called "Scudo," allowing you to buy gold for the price of a cup of coffee.

Tether has announced a new unit of measurement, "Scudo," for its gold-backed token Tether Gold (XAUT), defined as 1 Scudo = 1/1000 XAUT , or one-thousandth of a troy ounce.

This concept is similar to Bitcoin's "satoshi." Bitcoin can be divided to 8 decimal places, with 1 satoshi = 0.00000001 BTC, allowing users to participate in transactions without having to purchase an entire Bitcoin. The new on-chain token unit, Scudo, brings the same divisibility to gold tokens, allowing traders to send and receive gold on-chain without needing to hold a whole ounce of gold tokens.

The price of a cup of coffee can be used to transfer gold.

With the current international gold price at approximately $4,990 per ounce, 1 Scudo is worth about $4.99, roughly the price of a Starbucks latte.

This means that users can trade gold on the blockchain with extremely low barriers to entry. Previously, 1 XAUT corresponded to 1 ounce of gold, with a unit price often approaching $5,000, making it unfriendly for small transfers or daily payments. The launch of Scudo represents a significant step forward for gold tokens, transforming them from "investment tools" into "payment tools."

Tether stated that Scudo will enhance the daily availability of gold digital assets, providing investors and traders with a more flexible operating experience.

A Tribute to Italian Gold Coins: The Historical Origins of Scudo

The name "Scudo" did not come out of thin air. Historically, the Scudo was a physical gold coin in 16th-century Italy. The name comes from the Latin word "scutum " (shield), named after the shield pattern on the obverse of the coin. It was the official currency of the Papal States until it was replaced by the Italian lira in 1866.

Tether cleverly uses this name to connect the historical tradition of European gold currency with digital gold in the blockchain era. This may also be partly due to the large Italian population among Tether's senior management.

Without changing the underlying structure

It is important to note that Scudo is merely an adjustment in the unit of measurement and does not change XAUT's physical gold backing, custody model, or issuance structure . Currently, XAUT is backed by 1,329 gold bars, approximately 16.2 metric tons of physical gold, stored in a secure vault in Switzerland.

Existing XAUT holders' assets will automatically be displayed in compatible wallets and exchanges in Scudo, requiring no additional action. Furthermore, Scudo will not incur new recurring fees, and XAUT will maintain its original issuance and redemption cost structure.

The timing of Scudo's launch is significant. Since 2026, international gold prices have repeatedly broken historical highs, reaching a record high of $5,602 per ounce on January 28. As of mid-February, gold prices were still fluctuating at high levels between $4,900 and $5,100.

As gold prices soar, the price of 1 XAUT has also skyrocketed, making small transactions even more difficult. Against this backdrop, the launch of Scudo can be seen as a response to market demand. XAUT currently has a market capitalization of approximately $2.3 billion, making it the leading on-chain gold token, and Scudo is expected to further expand its use cases.

#TetherGold #XAUT #Scudo #microgold #onchaingold #tokenizedgold #digitalgold #goldpayments #fractionalgold #crypto #stablecoin #Web3Payments #blockchainpayments #goldonchain #ScudoUnit #goldinvesting #goldtoken #DeFi #fintech #cryptonews

#macao #macau

Aave proposed transferring 100% of all product revenue to the DAO! But it's asking for $50 million, drawing criticism from the community who see it as a cash-out disguised as goodwill.

Aave Labs has proposed the "Aave Will Win" framework, intending to transfer 100% of the revenue from all its branded products to the DAO, while requesting $25 million in stablecoins, 75,000 AAVE tokens, and multiple development grants. Marc Zeller, founder of the Aave Chan Initiative, criticized this as a "cashing out attempt disguised as goodwill."

On February 12, lending protocol giant Aave Labs proposed the "Aave Will Win" framework to the DAO. The proposal sounds very generous on the surface: Aave Labs is willing to transfer 100% of the revenue of all its Aave-branded products, including revenue from Aave v3 and v4 protocols, revenue from the https://t.co/aRngq3QLwz front-end, Aave Card, and the future AAVE ETF, to the Aave DAO treasury.

At the same time, the relevant trademarks and intellectual property rights will also be transferred to the newly established Aave Foundation.

What is the cost? Aave Labs requested $25 million in stablecoins and 75,000 AAVE tokens (worth approximately $15 million at current market value) from the DAO as working capital. It also applied for five grants of $3 million each for the development and promotion of the Aave App, Aave Pro, and Aave Card, and $2.5 million for the Aave Kit.

Roughly totaling, Aave Labs' actual funding needs are around $50 million.

Marc Zeller: This is cashing out disguised as a benevolent act.

Marc Zeller, founder of the Aave Chan Initiative (ACI) and one of the most influential governance participants in the Aave ecosystem, did not hesitate to fire his guns.

Zeller called the proposal "a cash-out attempt disguised as goodwill" and accused Aave Labs of trying to use radical proposals as bargaining chips to "impose outcomes regardless of governance processes." He estimated the Labs' actual funding needs at around $50 million and questioned the legitimacy of its governance.

More pointed criticism comes from historical context. In late 2025, the Aave community erupted in heated debate over the ownership of brand assets: should the DAO or Aave Labs control the trademarks, domains, community accounts, and other brand assets? This debate remains unresolved, and Zeller believes that Labs' insistence on pushing for a vote while the differences remain unresolved constitutes procedural "bullying."

He further pointed out that previous uncertainties surrounding revenue and governance had already caused AAVE tokens to lose approximately $500 million in market value. In other words, the governance drama itself is one of the biggest risks for AAVE holders.

Structural dilemmas in DAO governance

In almost all DeFi protocols, the relationship between the "core development team" and the "DAO" is ambiguous. Nominally, the DAO is the highest decision-making body, with token holders deciding everything through voting. However, in reality, the core team holds actual control over technical development capabilities, brand equity, and day-to-day operations. DAO holders typically can only say "yes" or "no" to proposals put forward by the core team, rarely having the ability to propose alternatives themselves.

This creates a power imbalance: the core team has the leverage to "not do it" (if the DAO doesn't provide funding, I won't develop it), while the DAO holders only have the power to "veto" (I can veto your proposal, but I can't do anything about it myself).

Aave Labs' proposal cleverly utilized this structure. It packaged "100% revenue transfer to the DAO" as a generous gesture, but simultaneously set a condition: the DAO must coordinate v4 development with Labs and suspend the development of new features for v3. Essentially, it said, "I'll give you the money, but you have to follow my pace."

This isn't just an Aave problem.

If you broaden your perspective beyond Aave, you'll find that similar tensions are spreading throughout the entire DeFi ecosystem.

The debate over Uniswap's fee on/off switch, the community split after MakerDAO was renamed Sky, the controversy over Lido's core contributor compensation... all these events essentially address the same question: when a protocol is large enough and profitable enough, who has the right to decide how the money is spent?

The ideal of decentralized governance is "decision-making by token holders." However, in reality, most token holders don't vote at all (Aave's governance participation rate has consistently been below 10%), and those who vote are often the core team, venture capital firms, and a few whales. So-called "community decision-making" is often just another way of saying "a minority makes decisions for the majority."

The conflict between Aave Labs and Zeller is essentially a public negotiation about the power boundaries between "developers" and "token holders" in DeFi governance. The outcome of this negotiation will not only determine Aave's future but also set a precedent for the entire DeFi ecosystem.

The ideal of decentralization is beautiful, but bills are paid in tokens.

#aave #AaveWillWin #DeFi #DAO #DAOGovernance #OnChainGovernance #CryptoNews #CryptoMarket #CryptoCommunity #Web3 #Blockchain #DeFiLending #AAVEtoken #AaveLabs #DefiDrama #GovernanceWars #CryptoDebate #Stablecoins #CryptoProposal #TokenHolders #macau #macao

The London Stock Exchange announced the establishment of a "Digital Securities Depository": supporting on-chain settlement of tokenized bonds, stocks, and private equity assets.

The London Stock Exchange Group (LSEG) announced the construction of a "Digital Securities Depository" to support on-chain settlement of tokenized bonds, stocks, and private equity assets, with the first phase aimed for delivery in 2026. Major UK financial institutions such as Barclays and Standard Chartered have expressed their support.

The London Stock Exchange Group (LSEG) was founded in 1801. Over the past three centuries, it has witnessed the advent of the steam engine, telegraph, electronic trading, and high-frequency algorithms. It has found its place in every technological revolution.

Now, it plans to do it again.

LSEG announced this week that it will build an on-chain settlement service called "LSEG Digital Securities Depository" for institutional investors. This system will support the trading and settlement of tokenized bonds, stocks, and private market assets, be compatible with multiple blockchain networks, and maintain interoperability with existing traditional settlement infrastructure. The initial delivery target is 2026, but this is still subject to regulatory approval.

Following the announcement, major British financial institutions, including Barclays, Lloyds Bank, NatWest Markets, Standard Chartered Bank, and Brookfield Asset Management, quickly expressed their support.

What makes LSEG Digital Securities Depository different?

LSEG is not starting from scratch. It already operates a blockchain platform for private equity funds on Microsoft Azure, and this digital securities depository is an extension of that existing strategy.

The list of supporters is not just one or two trial institutions, but rather core players in the UK financial system: the simultaneous endorsement of Barclays and Standard Chartered is a rare sight in crypto-related announcements.

The most crucial difference lies in its positioning. LSEG doesn't aim to be a standalone "crypto trading platform," but rather a bridge: a settlement bridge connecting traditional securities markets and blockchain networks. Its target customers are not retail investors or crypto natives, but institutional investors managing trillions of dollars in assets who have long been plagued by the inefficiencies of existing settlement systems.

The pain point of settlement: Two days equals a century

Why are institutions actively embracing on-chain settlement? The answer is T+2.

In traditional securities markets, a transaction typically takes two business days (T+2) from completion to final settlement. This means that stocks you buy on Monday won't truly belong to you until Wednesday. During these two days, both parties bear the risk of counterparty default, and the entire system requires multiple intermediaries such as the central securities depository, clearinghouse, and custodian banks to ensure smooth operation.

This system has been operating for decades and is very stable, but it is also very expensive. Every intermediary charges a fee, and every step adds delays and risks. It is estimated that the cost of global securities settlement is as high as tens of billions of dollars annually.

Blockchain promises to reduce T+2 to near instantaneous. LSEG's DiSH (Digital Settlement House) platform goes a step further, claiming to support 24/7 settlement and interoperability across time zones and multiple payment methods.

If this vision is realized, it will not only significantly reduce settlement costs, but also eliminate the most troublesome time zone difference problem in cross-border transactions.

The real battleground for tokenization is not Bitcoin.

It's worth considering that when the crypto community discusses "tokenization," they usually think of bringing real-world assets onto the blockchain (RWA) to provide DeFi protocols with more revenue streams. But LSEG sees the opposite logic: using blockchain technology to upgrade the infrastructure of traditional assets, rather than turning traditional assets into crypto toys.

The difference between these two approaches determines who holds the power of discourse. In the world of LSEG, blockchain is a tool, not an ideology. It doesn't need a narrative of "decentralization" to prove its existence; it simply needs to be faster, cheaper, and more reliable.

This might be seen as a "betrayal" by crypto fundamentalists—you used our technology but abandoned our spirit. But for the market, this is the most likely path for the large-scale adoption of blockchain technology: not to disrupt traditional finance, but to be absorbed by it.

#LSEG #LondonStockExchange #DigitalSecuritiesDepository #OnChainSettlement #DigitalAssets #TokenizedAssets #TokenizedBonds #TokenizedStocks #PrivateMarketAssets #Tokenization #RWATokenization #TradFi #DeFi #Blockchain #BlockchainTechnology #BlockchainInfrastructure #MarketInfrastructure #CapitalMarkets #InstitutionalInvestors #InstitutionalAdoption #UKFinance #Fintech #MicrosoftAzure #SettlementRisk #Tplus2 #24x7Settlement #CrossBorderPayments #DiSH #FinancialInnovation #SecuritiesSettlement #Barclays #LloydsBank #NatWest #StandardChartered #BrookfieldAssetManagement #macau #macao

https://t.co/8SZYE9poYa

Anthropic CEO Dario Amodei has laid out a highly detailed and pessimistic warning about AI’s near‑term trajectory, arguing that over the next few years it will create six major types of risk.

1. Unprecedented job loss and economic shock

Amodei predicts that within roughly 1 to 5 years, around 50% of entry‑level white‑collar jobs could be automated or heavily transformed by AI, including roles in customer support, basic admin, routine analysis, and HR tasks.

He warns that even if new jobs eventually emerge, the short‑term disruption could be extremely painful, with mass unemployment, wage pressure, social unrest, and sharper political polarization.

He also suggests that in just 1 to 2 years, we may see AI systems that are “better than any individual human” on a wide range of cognitive tasks, accelerating automation so quickly that labor markets have almost no time to adapt.

2. AI gaining national‑level power: a “nation of geniuses”

To illustrate the scale of what might be coming, Amodei uses an extreme metaphor: by around 2027, we could effectively have a “country in a data center,” like a virtual nation populated by 50 million super‑intelligent agents.

These AI systems, taken together, could outperform Nobel‑level experts in science, finance, military planning, cyber operations, and information warfare.

Because this “nation” only requires chips, electricity, and connectivity to operate, and is controlled by whoever owns the infrastructure, it could become the ultimate strategic asset for corporations or governments seeking overwhelming technological, financial, or military advantage.

3. Escalating terrorism and biosecurity threats

Among all security issues, Amodei is most worried about biology.

He argues that future AI systems may enable people with little formal training to carry out complex biological experiments by generating step‑by‑step protocols, troubleshooting advice, and optimization strategies.

In the worst case, this could lower the barrier to designing or deploying dangerous pathogens, toxins, or other biological agents, potentially including attacks that are highly targeted and very hard to trace, overwhelming traditional defense and attribution mechanisms.

4. Supercharged authoritarianism and mass surveillance

Amodei also warns that when AI is combined with surveillance tools, it can dramatically extend the power of authoritarian regimes.

Automated censorship and real‑time content filtering can be used to systematically suppress dissent and control online discourse.

Face recognition, behavior prediction, and large‑scale data fusion can enable near‑total monitoring of citizens’ movements and associations.

At the same time, AI‑generated propaganda, deepfakes, and tailored disinformation campaigns can reinforce regime narratives and undermine trust in independent media, making it much harder for democratic institutions and civil society to recover once they are weakened.

5. AI platforms shaping and manipulating the collective mind

As large AI models become the default layer in search, social media, advertising, and entertainment, a small number of platforms will gain extraordinary power to shape what billions of people see and think about.

Amodei’s concern is not just the familiar “filter bubble,” but a subtler form of cognitive environment control, where systems continuously learn what persuades different individuals and groups and then adjust their responses accordingly.

This could allow platforms to nudge users’ political views, consumer behavior, and moral intuitions in ways that are hard to detect or opt out of, turning large‑scale psychological influence into a business model rather than a rare abuse.

6. Massive financial incentives and a governance vacuum

The final risk Amodei highlights does not come from the technology itself, but from human incentives and institutions.

He expects that advanced AI and its ecosystem (cloud, chips, applications, and downstream industries) could generate trillions of dollars in annual revenue and market value.

With so much money on the line, corporate leaders, investors, and even some governments may be tempted to downplay risks, delay regulation, or aggressively lobby against strong guardrails, all to keep growth and valuations high.

In his view, the core problem is that the speed at which capital and technology reinforce each other vastly exceeds the speed at which laws, norms, and international coordination can respond.

A moral demand on the wealthy and tech leaders

In light of these dangers, Amodei makes a pointed ethical claim.

He argues that people who control immense wealth and power in the tech sector have an obligation to devote serious resources and attention to reducing systemic AI risks, not just maximizing valuation.

He is openly critical of a growing cynical attitude among some wealthy technologists who dismiss philanthropy, public‑interest research, and safety work as pointless or fraudulent.

If those with the most leverage choose to look away while pursuing short‑term gains, he believes ordinary citizens and broader civilization will have almost no bargaining power to insist on a safer, more responsible AI trajectory.

#AISafety #AIrisks #FutureOfWork #JobDisplacement #AIEthics #TechResponsibility #AIRegulation #AIGovernance #DigitalAuthoritarianism #SurveillanceCapitalism #MassSurveillance #Biosecurity #AIDisinformation #Deepfakes #AlgorithmicPower #BigTech #BigTechAccountability #TechPolicy #ResponsibleAI #Anthropic #DarioAmodei #AIWarning #AIFuture #TechTwitter #XAI #macau #macao

AI Panic: Microsoft Executives Warn Most White-Collar Workers Will Be Replaced by Automation Within the Next 12-18 Months!

Microsoft's AI chief, Mustafa Suleyman, issued the most aggressive warning to date about automation, stating that most white-collar professional jobs, such as lawyers and accountants, could be fully automated by AI within 12 to 18 months. Anthropic's CEO went further, listing six major AI risks and warning that AI could disrupt 50% of entry-level white-collar jobs within 1 to 5 years.

The head of Soft AI issued the most radical warning to date about automation, saying that the vast majority of white-collar professional jobs could be replaced by AI within a year and a half. This timeline is much earlier than the general expectations of the business community and policymakers, sounding an alarm for the global labor market.

In an interview with the Financial Times, Microsoft AI CEO Mustafa Suleyman said that "most of the tasks" of computer-based professionals such as lawyers, accountants, project managers and marketers will be fully automated by AI within the next 12 to 18 months .

The signs of AI-induced unemployment are already emerging. According to a report by job placement firm Challenger, 7,624 jobs were lost due to AI in January of this year , accounting for 7% of all layoffs that month; by the end of 2025, AI-related layoffs are projected to reach 54,836 . Since tracking began in 2023, 79,449 planned layoffs have been attributed to AI.

At the same time, the risks of AI safety and misuse are also rapidly escalating. In its latest report on sabotage, Anthropic warned that its Claude model is more sensitive to "harmful misuse" in certain computer use scenarios, and even showed risk signals related to chemical weapons development.

There is still a 12 to 18-month window before AI begins to replace white-collar workers on a large scale.

Suleyman's prediction marks the most radical assessment in the tech industry of AI replacing human work schedules. He states that AI will reach human-level performance in "most, if not all," professional tasks within the next 12-18 months, primarily those requiring white-collar work in front of a computer.

This warning is not an isolated case. The problem of large-scale labor displacement is troubling governments around the world, although the true number of unemployed remains unclear amid broader economic headwinds.

A Challenger report shows that AI is gaining a stronger presence in layoff narratives: in January 2026 alone, 7,624 layoffs were attributed to AI, accounting for 7% of the total for that month. On an annual basis, 54,836 layoffs were announced in 2025 that were related to AI.

It's hard to say exactly how much impact AI will have on layoffs. We know that leaders are talking about AI, many companies want to implement it in their operations, and the market seems to be rewarding those companies that mention it.

White-collar workers train "substitutes" themselves.

A concrete example of labor substitution is emerging. The Wall Street Journal reports that Bay Area startup Mercer has "quietly hired tens of thousands of white-collar contract workers," many of whom are highly qualified professionals in fields such as medicine, law, finance, engineering, writing, and art, tasked with training AI systems that may replace them in the future.

The report states that these contractors are typically paid between $45 and $250 per hour to review and rewrite model outputs over several weeks or months, providing training support for companies including OpenAI and Anthropic.

For the market, this model demonstrates the short-term demand of the AI industry chain for "data labeling and feedback labor," but it also reinforces the issues of wage structure and employment stability brought about by the long-term substitution logic.

There are disagreements about the pace of the attack.

Not all analysts agree on such a rapid replacement timeline. Morgan Stanley stated that "the impact of AI may take longer to manifest in economic data," and the first undeniable shocks may arrive "later in this decade and into the next."

While AI adoption may be faster than past technologies, we believe it is too early to see it reflected in economic data, aside from business investments.

Stephen Byrd, head of global thematic research and sustainability research at Morgan Stanley, told clients this.

#Microsoft #Azure #NVIDIA #ClaudeAI #AI #ArtificialIntelligence #AIFunding #TechNews #VentureCapital #StartupNews #SiliconValley #SeriesG #AIInfrastructure #CloudComputing #macau #macao

Anthropic completes $30 billion funding round, breaking a Silicon Valley taboo?!

In Silicon Valley's venture capital world, there's an unwritten rule that's been around for forty years: don't invest in competitors.

The logic is simple. When you invest in a company, you're committing not just capital, but also trust. You'll sit on the board, see trade secrets, product roadmaps, customer data, and financial figures. If you've also invested in its direct competitor, how can you prove you haven't passed on A's intelligence to B?

This is not just a moral issue, but a matter of business reputation. In an industry that operates on word of mouth, the label of "betraying the founder's trust" is more fatal than a failed investment.

This is why Vinod Khosla, founder of Khosla Ventures, publicly stated in 2025 that he "would not invest in directly competing AI companies at the same time." Thrive Capital also chose loyalty: all-in on OpenAI, rejecting the temptation of other large AI models.

But Sequoia doesn't think so.

In late 2024, Sequoia Capital underwent a generational shift. Roelof Botha, who had long led the firm, stepped down as Global Managing Partner, and Pat Grady and Alfred Lin took over. The new leadership team made a radical decision: to simultaneously bet on three leading AI companies. Sequoia held an early stake in OpenAI, later invested in Musk's xAI, and now appears on Anthropic's investor list.

It's not just Sequoia. Altimeter Capital has invested over $200 million in Anthropic and also holds shares in OpenAI. Blackstone has invested approximately $1 billion in Anthropic. Abu Dhabi-based MGX Fund has invested in both OpenAI and Anthropic.

The smartest money in Silicon Valley is buying up every single horse on the track at the same time.

#Anthropic #AIFunding #SiliconValley #VentureCapital #StartupNews #TechNews #ArtificialIntelligence #AIRevolution #SeriesG #UnicornStartup #Investing #FinTech #BlockchainNews #Innovation #BigTech #macau #macao

https://t.co/qN5IGLSvM5

Missing out on $80 billion in wealth! A look back at SBF's past brilliant investments: $500 million investment in Anthropic, buying SOL at $8...

Had he not crossed legal lines, Sam Bankman-Fried might have amassed a potential fortune exceeding $80 billion through his accurate bets on AI and blockchain; however, his investment legend ultimately became a somber warning in financial history.

Sam Bankman-Fried (SBF), who once dominated the cryptocurrency industry, also fell from grace in a short period. However, as the outside world re-examines his early investment portfolio, an intriguing fact has emerged: if some of his key holdings had not been seized and liquidated due to legal issues, their potential total value could have exceeded $80 billion. This " untapped wealth " has become one of the most dramatic missed opportunities in fintech history.

AI betting boom: Anthropic's holdings have astonishing potential value.

Among its numerous investments, SBF's early-stage investment in the AI startup Anthropic is the most noteworthy. SBF invested approximately $500 million in the company. As generative AI technology rapidly rises, Anthropic's position in the industry has grown accordingly.

If SBF retains control of these shares, their value could reach as high as $70 billion based on current market valuations. This also demonstrates SBF's remarkable foresight in judging technological trends.

Betting on the public blockchain wave: SOL investment surged at one point.

In addition to his AI ventures, SBF also has a well-defined presence in the crypto asset market. He once bought approximately $60 million worth of tokens when the price of Solana (SOL) was around $8.

As Solana emerged as one of the leading high-performance public blockchains and was seen as a significant competitor to Ethereum, the price of SOL surged. At its peak, the holding was worth approximately $2.1 billion, demonstrating its successful positioning in the early stages of the public blockchain ecosystem's rise.

Deploying new public blockchains and fintech: Mysten Labs and Robinhood

SBF also invested approximately $100 million in Mysten Labs, the development team behind the Sui blockchain. As Layer-1 protocols continue to attract funding and developers, that investment is now valued at over $800 million.

In addition, he holds approximately 7.5% of the U.S. retail trading platform Robinhood. This stake was acquired during a period of market turmoil for the company. As Robinhood expanded into cryptocurrency trading and benefited from the stock market recovery, this stake is now valued at approximately $10 billion.

Success lies in foresight, failure lies in risk management

Based on comprehensive calculations, if none of the aforementioned holdings are seized or liquidated, their potential total value could exceed $80 billion. This means that SBF originally had the opportunity to transform from a short-lived crypto upstart into a long-term financial giant spanning AI and blockchain.

However, following FTX's collapse in 2022, SBF was convicted of misappropriating client funds for high-risk trading and investments, and his assets were seized by authorities. It is widely believed that his failure stemmed not from choosing the wrong targets, but from a complete breakdown in risk management and compliance.

#SamBankmanFried #SBF #FTX #crypto #cryptocurrency #blockchain #Anthropic #AI #Solana #SOL #MystenLabs #Sui #Robinhood #fintech #investment #Bitcoin #Ethereum #quantitativetrading #predictionmarkets #Polymarket #ElonMusk #SpaceX #xAI #LunarBaseAlpha #macau #macao

"Miners surrender, long live AI!" Bitfarms announces its exit from Bitcoin mining! Difficulty experiences its biggest drop since 2021.

The Bitcoin mining industry is experiencing its harshest winter since the 2022 bear market. Hashprice has plummeted to an all-time low of $33.31 per hashrate, the total cost of mining one BTC (approximately $87,000) is nearly 20% higher than the market price, the network hashrate has crashed by 40%, and on February 9th saw the largest difficulty reduction since the 2021 Chinese ban, a drop of 11%.

Bitcoin's price has fallen by more than 50% from its all-time high of $126,000 in October 2025, and is currently hovering around $67,000. This crash is rewriting the survival rules of the entire mining industry; when mining costs far exceed the price of the coin, miners are facing survival issues.

Hash/price hits all-time low: $18,000 loss per coin mined

Bitcoin's hashprice (revenue per unit of computing power) fell to an all-time low of $33.31/PH/s/day on February 2nd , with a daily low of $34.91. This is a core metric for measuring miners' profitability, meaning that for every PH of computing power invested, less than $35 can be earned per day.

The harsher reality is that, according to Checkonchain data, the average total production cost of mining one Bitcoin on the entire network is currently about $87,000 , while the market price is only about $69,000. This means a loss of about $18,000 for every Bitcoin mined. This is the first time such a large cost inversion has occurred since the bear market of 2022.

The industry's "Miner Profitability Sustainability Index" has dropped to 21, indicating that, apart from a few operators with low electricity prices (less than $0.05 per kilowatt-hour) and high-efficiency mining machines, most miners' profit margins have been completely squeezed, and the return on investment period has soared to more than 1,000 days.

Texas blizzard + miners surrender

To make matters worse, Texas, a major mining hub in North America, was hit hard by winter storm Fern at the end of January. To ensure the stability of the residential power grid, many mines were forced to shut down due to power outages.

During the storm, the network hashrate plummeted from a peak of 1.13 ZH/s to a low of 663 EH/s, a drop of 40%. Foundry USA, the largest mining pool in the United States, lost 60% of its hashrate capacity at one point, with approximately 200 EH/s going offline instantly. Block generation time was extended to more than 12 minutes at one point.

CryptoQuant defines the current phase as the "capitulation phase," characterized by the accelerated shutdown of older mining rigs and a significant contraction in the overall network hashrate. As a result, the share prices of listed mining companies such as MARA Holdings and Riot Platforms have fallen by more than 20% this week, with funds rapidly flowing into more stable traditional assets such as gold.

Largest drop since China's ban in 2021

On February 9th, the Bitcoin network underwent a historic difficulty adjustment, decreasing by 11.16% , from 141.6 T to 125.86 T. This is the largest single negative difficulty adjustment since China's comprehensive ban on cryptocurrency mining in July 2021, and also the 10th largest drop in Bitcoin's history.

In theory, lowering the mining difficulty should help restore the profitability of remaining miners, as fewer competitors mean that the same computing power can mine more coins. However, due to the significant drop in coin prices (halving from their peak), the profit recovery effect of the difficulty adjustment is extremely limited. For companies with electricity prices higher than $0.05 per kilowatt-hour or still using older mining rigs, this adjustment is unlikely to reverse the fate of a complete shutdown.

Bitfarms says it is no longer a Bitcoin company.

Faced with the downturn in the mining industry, some choose to persevere, while others choose to make a splendid transformation.

On February 6, Bitfarms, a former major North American mining company, announced its complete exit from the Bitcoin mining business and plans to change its name to " Keel Infrastructure ," move its legal registration from Canada to the United States, and change its stock symbol from BITF to KEEL.

Bitfarms CEO Ben Gagnon stated bluntly, "We are no longer a Bitcoin company." He indicated that the company will fully transform into a developer and operator of HPC/AI data center infrastructure. He estimates that converting just one mining farm in Washington state into a GPU-as-a-Service could generate net operating revenue exceeding all of Bitfarms' total mining revenue to date .

The company plans to gradually shut down all mining operations between 2026 and 2027 and invest $128 million to transform its 18 MW mining farm into an advanced liquid-cooled data center supporting Nvidia GB300 GPUs, with completion expected in December 2026. Following the announcement, Bitfarms' stock price jumped 16%.

#Bitcoin #BTC #BitcoinMining #Bitfarms #KeelInfrastructure #AIDatacenter #GPUCloud #HPC #MiningCapitulation #HashrateCrash #MiningDifficulty #CryptoWinter #CryptoMarket #DigitalAssets #NvidiaGPUs #macau

Wall Street-based Apollo, which manages nearly a trillion dollars, has partnered with DeFi lending platform Morpho to acquire 90 million tokens.

Apollo Global Management, a global alternative asset giant managing $938 billion in assets, announced a partnership with DeFi lending protocol Morpho to acquire up to 90 million MORPHO tokens over four years, representing 9% of the total token supply, valued at over $100 million at current prices.

According to the official announcement, Apollo or its affiliates may acquire MORPHO tokens through open market purchases, over-the-counter (OTC) transactions, and other contractual arrangements, with a total acquisition limit of 90 million tokens over a period of 48 months, subject to transfer and trading restrictions.

The total supply of MORPHO tokens is 1 billion, with approximately 549 million currently in circulation. Based on the current price of approximately $1.19, this acquisition agreement is worth approximately $107 million, and the 90 million tokens represent 9% of the total token supply.

Galaxy Digital UK Limited is acting as Morpho's exclusive financial advisor.

Establish an on-chain lending market

According to the agreement, Apollo and Morpho will collaborate to support the on-chain lending market on the Morpho protocol. In fact, their collaboration has already begun. Apollo's "Apollo Diversified Credit Securitization Fund" (ACRED) has been tokenized through Securitize and is running lending strategies on Morpho, marking the first time a private credit fund has been used for on-chain structured products to enhance returns.

Morpho, as a core infrastructure in the DeFi lending field, currently has a total value locked (TVL) of nearly $4 billion, making it the second largest lending protocol after Aave.

Traditional financial giants are accelerating their embrace of DeFi

Apollo Global Management, one of the world's largest alternative asset management firms, managed $938 billion in assets as of the fourth quarter of 2025, and is heading towards the trillion-dollar mark. This collaboration with Morpho is seen as a significant milestone for traditional financial institutions embracing on-chain financial infrastructure.

It is worth noting that this move is not just a simple token investment, but a strategic move by Apollo to deeply participate in the decision-making and development direction of DeFi protocols by acquiring governance tokens.

#Apollo #ApolloGlobalManagement #Morpho #MORPHO #DeFi #DeFiLending #OnChainLending #Crypto #Web3 #Blockchain #TokenDeal #InstitutionalAdoption #TradFi #TradFiMeetsDeFi #DigitalAssets #macau

“Not Your Keys, Not Your Coins: Lessons from Bithumb’s 620,000 BTC Disaster”

Most people assume that once they “buy Bitcoin on an exchange,�� those coins are really theirs, but the Bithumb mistake shows that on centralized exchanges your “coins” are often just editable database numbers, not actual UTXOs controlled by your keys.

Bithumb’s 620,000 “ghost bitcoins”

On Feb 6, 2026, Korea’s No. 2 exchange Bithumb ran a promo intended to pay users 2,000 KRW each, but an employee mis‑entered the unit as BTC and effectively sent out 2,000 BTC per user to 249–695 users, for a total of about 620,000 BTC, worth around 40–44 billion USD.

Bithumb only held about tens of thousands of BTC in real reserves, so the rest were “ghost bitcoins” created purely in the internal ledger; no such coins existed on the blockchain.

The system shockingly allowed this over‑issuance (roughly 14× reserves) with no automatic block or alert, like editing numbers in an Excel sheet.

In about 20–35 minutes before detection and freeze, 80‑plus quick users sold roughly 1,700–1,800 BTC, causing the BTC price on Bithumb to briefly crash 17–20% and trade far below global market price.

Bithumb later froze accounts, reversed what it could, and reported recovering about 99.7% of the misallocated BTC, leaving around 125 BTC (≈9 million USD) unrecovered, which it pledged to cover from its own reserves.

The article uses this to argue: on CEXs, your balance is “just numbers” until you withdraw on‑chain; exchanges can technically display and trade assets that don’t exist on the blockchain at all.

“Fat finger” disasters and governance

The writer links Bithumb to other “one person, one keystroke” disasters to make a governance point:

2018 Samsung Securities “ghost shares”: a typo turned 1,000 KRW dividends into 1,000 shares per employee, minting billions of non‑existent shares; some staff sold them, causing a sharp stock drop.

Barings Bank (1990s): a single rogue trader’s positions sank a 200‑year‑old bank, illustrating how weak controls let one person blow up an institution.

The takeaway: financial crises are often caused less by innovation and more by shockingly bad internal controls and oversight.

Human nature and legal gray zones

The text then asks: if you suddenly see 2,000 BTC appear in your account, do you report it, flex on social media, or dump it and run?

It cites similar real‑world cases:

2021 https://t.co/9scAbV6vAr: an employee error sent an Australian customer over 10 million AUD instead of a 100 AUD refund; the recipients bought houses and cars, and the mistake was only noticed about seven months later, ending in legal action.

2021 BlockFi: a bonus bug paid out BTC instead of a small stablecoin bonus; the company threatened lawsuits to recover funds, raising the question of whether spending mistakenly credited crypto is a crime or just exploiting a platform bug.

The article points out that in traditional banking, spending wrongly credited funds is usually “unjust enrichment” or even theft, but crypto law is still fuzzy, especially when the “asset” arguably never existed on‑chain.

Centralized vs decentralized irony

The author stresses the classic “Not your keys, not your coins” line:

Those 620k “ghost BTC” never existed on the Bitcoin blockchain; they lived only in Bithumb’s internal ledger.

If users self‑custody in hardware wallets, an exchange can’t conjure or mis‑assign coins in those wallets; the worst it can do is fail to send you coins at all.

But then the article balances this with a DeFi cautionary tale:

2021 Compound Finance bug: a one‑character error in an upgrade caused about 160 million USD worth of COMP to be over‑distributed to users; there was no central “pause” button, so the founder could only publicly beg users to return funds, and a large portion was never recovered.

So:

CEX: more controls and the ability to freeze/reverse, but huge trust and governance risk.

DeFi: trustless and non‑custodial, but when the code is wrong, there is little recourse and no emergency brake.

In this incident, Bithumb at least froze and clawed back almost all funds; Compound’s over‑distribution remains partly unrecovered.

Practical safety tips for retail users

The piece proposes pragmatic steps for ordinary users:

Do not park all large funds on a single exchange; spread risk across venues.

Move long‑term holdings to hardware cold wallets where you control the keys.

Prefer exchanges that offer ongoing, verifiable “proof of reserves,” e.g., Merkle‑tree based systems that let users check that client liabilities are fully backed.

And it reminds readers: in crypto there is no deposit insurance and usually no government bailout; security is ultimately your own responsibility.

#Bithumb #Bitcoin #GhostBitcoin #FatFinger #CryptoExchange #NotYourKeysNotYourCoins #SelfCustody #CryptoSafety #ProofOfReserves #DeFi #CeFi #CryptoRegulation #TaiwanCrypto #BTC #CryptoNews #Macao

Stablecoins aren’t here to kill banks; they’re here to kill the era of “free, unearned interest spreads” that banks have long enjoyed.

What did BOA say in its Q4 call?

•BOA’s management openly stated that if regulations on stablecoins are relaxed and the market grows large, it would effectively move deposits out of the traditional banking system and into the stablecoin ecosystem, potentially pulling trillions of dollars off bank balance sheets.

•Once those deposits leave, banks’ ability to lend shrinks and they are forced to rely on more expensive wholesale funding, which pushes borrowing costs higher and makes it especially harder for small and medium‑sized businesses to access credit.

Why are they so afraid of money moving out?

•The core profit engine of traditional banks is using nearly zero‑interest demand deposits to fund loans and bond investments, quietly capturing a large interest spread in the middle rather than simply charging transparent service fees.

•Stablecoins let users transfer and pay with high liquidity without being locked into bank accounts, weakening banks’ ability to “trap” funds and skim a toll on every dollar that sits in the system—and that is what truly makes banks nervous.

So banks resist stablecoins not because of technology, but because they fear deposits “moving house” and hollowing out their interest margins and lending business.

#Stablecoin #Stablecoins #Crypto #Cryptocurrency #DeFi #FinTech #OnChain #Web3 #DigitalAssets #Tokenization #FutureOfFinance #Banking #TradFi #CeFi #StablecoinNews #CryptoNews #macau