1. Codex many times 'breaks' and can't continue a conversation. An error pops up... many times I ask it on another conversation to fix the other conversation and does it

2. Several times the transcription doesn't work and it gets lost.

3. Updates aren't smooth. The app doesn't restart cleanly after the update, and the download/update process isn't clear

4. Some times it just freezes when it goes through various processes and it might shut down immediately rather than waiting

The repricing to the upside on such news could be brutal.

Might be tough in the short term, but medium term (and for as long only all the 'good' people have access to them) then that's very bullish.

Don't forget that all software bugs, and It's actually worse for banks

The truth is that AI is short term bearish for crypto. For many protocols too...

But the question is: what happens if the crypto companies get access to Mythos?

What if all the major protocols have them because crypto is strategically important to the US?

@zerohedge Of course it is bruv ... the us is holding hostage everyone with AGI.

Try say no to them. They use Mythos and it's the equivalent of getting nuked.

A new phase of the AI trade is starting to matter for markets.

The first phase was easy to see: semiconductors, data centers, model labs, power demand, and the companies selling the picks and shovels of AI. The next phase is less obvious, but potentially just as important: what happens when frontier AI starts changing the economics of software itself?

If advanced models can find vulnerabilities at scale, then software security debt becomes a market variable. Code quality, patch speed, observability, testing discipline, incident response, and access to defensive AI tools all start to matter more for valuation.

That creates a dispersion trade.

The winners are the companies that can use AI to harden their systems faster than attackers can exploit them. The losers are the companies and protocols that discover their codebases were carrying unpriced security debt.

This matters for software, because stronger AI can raise the cost of building, securing, operating, and proving software. It also matters for crypto, because the same vulnerability-discovery shock is more reflexive there: a bug in enterprise software can become a cost; a bug in DeFi can become an immediate asset drain.

So the market implication is not a broad anti-software or anti-crypto call. It is a quality and resilience trade: own the systems that can prove durability, and be careful with the systems that cannot.

The Software Setup

IGV is now the clean software ETF reference for this theme.

The data is interesting because software is not where the obvious crowding is. IGV is trading around 94, with about $14.4B in AUM. Relative to SPY, IGV is still low: around the 20th percentile on the local 10-year history and around the 25th percentile over the last year, but the path has turned up over the past month.

That is exactly the kind of setup I want for a rotation trade: not dead, not euphoric, and not already the most crowded sleeve.

The contrast with semiconductors matters. BoFA's latest crowded-trade data still has long global semiconductors as the obvious consensus trade, and tech/QQQ relative strength is already near extreme levels. So the trade is not "buy tech." It is more specific:

Own software that can benefit from the AI-security reset, while avoiding the most crowded AI hardware chase.

The Flow Context

The IGV data is now more complete than just a latest quote.

There is a 10-year local price and IGV/SPY relative-strength history. There is also an exact current iShares snapshot for NAV, shares outstanding, and AUM. On top of that, ETF Central / Trackinsight shows IGV with about $14.37B in AUM as of May 20, with roughly +$871M of 1-month flows and +$6.53B of YTD flows.

The longer flow picture is also not dead: ETF Central shows positive 1Y, 3Y, and 5Y flows. At the same time, performance is still negative YTD and negative over one year, which fits the "washed out but starting to recover" idea.

There is one important caveat: exact iShares daily historical AUM is not available from the current parser. We do have a historical shares-outstanding file from 2010 to 2023 and an AUM proxy built from those shares and IGV market price, but that proxy is not the same as exact issuer NAV/AUM history. For trading context, the combination is enough: current exact AUM, flow-horizon summary, and long relative-strength history.

Why Mythos Changes The Software Moat

Mythos-style models change the cost curve.

If frontier systems can find and exploit vulnerabilities at scale, then closed source, complexity, and old audit cycles stop being enough. The moat shifts toward operational speed: code visibility, automated testing, CI/CD, observability, incident response, security telemetry, and proof that vulnerabilities can be fixed before attackers can monetize them.

This makes software more expensive to build and maintain.

AI compute is not free. GPU rent is not free. More AI-generated code means more systems to review, integrate, secure, monitor, and own. Developer demand can rise because AI increases how much software can be attempted, while humans still need to manage architecture, workflows, security, deployment, and accountability.

That favors incumbents with distribution, cash flow, model access, security teams, and deep workflow lock-in.

It hurts thin SaaS, weak codebases, small vendors with poor telemetry, and software companies whose value depends on the old assumption that attackers and auditors are human-limited.

How I Would Express It

The broad version is long IGV as a software rebound vehicle.

The sharper expression is long hardened software and security infrastructure versus weak software-security debt.

The companies I would want are the ones with one or more of these traits:

Early access to frontier defensive models.

Control of cloud, identity, endpoint, developer, or security telemetry.

Deep enterprise workflow lock-in.

Ability to ship patches quickly without breaking production.

Ability to prove resilience to boards, regulators, insurers, and customers.

The companies I would avoid are the ones with old codebases, low test coverage, slow patch cycles, thin UI moats, and no realistic ability to absorb continuous security remediation.

This is why Mythos can be bullish for the right software names. It is bearish insecure software, but bullish economically hardened software.

Crypto Is The Same Story, But Faster

Crypto has the same security-debt problem, but the consequences are more immediate.

In normal enterprise software, a vulnerability can mean data theft, downtime, ransomware, procurement delays, or liability. In DeFi, a vulnerability can become instant money leaving the protocol.

That makes weak crypto more exposed than weak software.

The vulnerable zones are obvious: DeFi forks, bridges, oracles, restaking layers, upgrade keys, multisigs, wallets, custody, signing infrastructure, and anything with high TVL but weak security budgets.

The first-order Mythos reaction can therefore be bearish for crypto beta. If stronger models expose bugs before protocols have access to comparable defensive tools, long-tail DeFi and bridge-heavy ecosystems can sell off hard.

But Crypto Also Has A Bullish Second Step

The second-order crypto thesis is more interesting.

If major protocols eventually get access to frontier defensive agents, the market can start rewarding security credibility. Continuous AI red-teaming, formal verification, live monitoring, bridge/oracle hardening, emergency controls, and better key management become part of the valuation story.

That creates two scenarios:

No access or late access: weak DeFi and long-tail crypto sell off, BTC outperforms, and capital hides in safer base-layer exposure or stables.

Access and hardening: security-serious protocols rerate, BTC remains the quality anchor, and selected ETH/SOL/DeFi names recover after they prove resilience.

This is why I would not be blindly bearish crypto. I would just be selective.

Current Crypto Read

The current crypto setup is not a perfect buy signal.

Fear/greed is depressed, which is usually interesting. But the rest of the positioning is not washed out enough. ETH clients are still meaningfully long, broad crypto clients are still long, and BTC/ETH options are not showing a clean panic-volatility reset.

So the cleaner stance is cautious exposure, not zero exposure.

BTC is the better relative hold during AI-cyber stress because the base layer is simpler, public, transparent, heavily reviewed, and socially easier to trust than opaque systems. Long-tail DeFi and bridge-heavy beta should be treated with more suspicion until there is evidence of real hardening.

The strongest crypto trades are therefore relative:

Long BTC or high-quality base-layer exposure versus fragile DeFi and under-secured long-tail beta during AI-security panic windows.

Then rotate selectively into protocols that can prove security spend, continuous testing, strong governance, bridge/oracle discipline, and clean positioning.

Bottom Line

Mythos is not bearish software. It is bearish insecure software.

Mythos is not bearish crypto. It is bearish fragile, composable, under-secured crypto.

The software trade is long the companies that can turn AI into a security moat: hardened platforms, security infrastructure, and deeply embedded enterprise systems. IGV works as the broad software rebound vehicle because software is still low versus SPY while semiconductors are already crowded.

The crypto trade is quality first. BTC should hold up better than fragile long-tail beta during AI-cyber scares. DeFi and high-beta ecosystems become interesting only after the market sees real evidence of hardening.

The big idea is simple:

AI does not destroy software. It reprices trust.

Own the systems that can prove resilience. Avoid the systems that cannot.

Markets are giving a strange but useful message right now: the best opportunities are not necessarily in chasing the trades that already look obvious.

The equity trend still looks alive, but the leadership is crowded. Oil has a bullish narrative around it, but price action has not been convincing enough. Inflation fear is still prominent, which makes duration more interesting if that fear starts to fade. Crypto has enough fear to stay on the radar, but not enough positioning reset to make it the cleanest long.

So the view is more selective than simply "buy risk."

I would rather be bearish oil on failed strength, bullish broadening equities, long duration, short AUD/CHF, cautious on crypto, and selective with commodity shorts. The common thread is simple: fade the crowded narratives, and look for the places where skepticism is still feeding the trend.

Bearish Oil

The oil narrative has become too comfortable.

Barron's is talking about a major energy supply shock and stocks to play it. The Economist recently framed oil prices as not yet high enough. Barron's has also been leaning into airline pressure, which indirectly reinforces the same high-fuel-cost story.

That is usually the setup I want to fade, especially if price refuses to confirm it. If oil cannot move higher while the media story is this bullish, that is weakness.

The positioning is not perfectly one-way, so I would not blindly short every dip. Brent small specs are crowded long, but client positioning is mixed across Brent and WTI. The cleaner idea is to sell failed strength in oil and energy, not to force the trade if crude starts breaking higher with confirmation.

If oil rolls over, it also supports the deflationary trade: duration, consumers, airlines, and parts of the equity-broadening story.

Equities Higher, Rally Broadens

The equity setup is still constructive because people are not euphoric.

AAII bulls are still low, bears are still relatively high, and this is happening while the market is in an uptrend. That is important. In a bull trend, persistent caution is fuel. For the trend to become fragile, the surveys would need to flip into real bullish excess. We are not there.

Client positioning also supports upside risk. Retail/broker clients are still short the S&P, Nasdaq, Russell, and mildly short the Dow. That does not guarantee an immediate squeeze, but it means the broad equity tape is not loaded with obvious late longs.

COT also helps the broadening view. Dow and midcap positioning look supportive, while small speculators are not at the kind of extreme long levels that have marked prior equity peaks. That matters because the better trade is not "buy the most crowded index." It is long breadth: Dow, Russell, midcaps, equal-weight, and lagging cyclicals.

Duration And Deflation

The market is still very worried about inflation and yields. That makes the opposite trade attractive if the data stop validating the fear.

BoFA's latest tail-risk work still shows inflation as the dominant fear. TLT relative to equities remains deeply washed out. Cash levels are high. If oil weakens and inflation fear fades, duration can rally, yields can fall, and that would give more oxygen to the equity-broadening trade.

This is why long duration fits the same story as bullish breadth. Lower yields would not just help bonds; they would also help lagging equity areas that have been held back by the rate narrative.

Short AUD/CHF

AUD/CHF remains one of the cleaner FX expressions.

The Australian dollar is crowded from a COT perspective: commercials are extremely low and large specs are extremely high. The Swiss franc is the opposite: positioning is more supportive, and clients are still short CHF.

The macro logic also fits. If oil and commodities weaken, and if the market moves toward a deflationary/rates-down trade, commodity FX should struggle more than CHF.

So the trade is not just "short AUD." It is short commodity-risk currency versus a currency that positioning already supports.

Tech And Semis: Do Not Chase

Semis are the obvious crowding problem.

BoFA has long global semiconductors as the dominant crowded trade again. XLK and QQQ relative strength are also near extreme levels. Levered upside ETF flows have come back strongly.

That does not mean semis must immediately crash. Strong crowded trades can keep working longer than people expect. But it does mean I would rather not make semis or mega-cap tech the main long here.

The cleaner equity read is breadth and catch-up, not fresh chasing of the most loved AI hardware trade.

Crypto: Cautious, Not Zero

Crypto has fear, but it is not a clean despair setup.

Fear/greed is depressed and has been below 50 for nearly two weeks, which normally creates potential opportunity. But the positioning layer is not washed out. ETH clients are still meaningfully long, broad crypto clients are still long, and BTC/ETH options are not showing the kind of panic-volatility reset I would prefer.

So I would keep some exposure, but I would not make crypto the highest-conviction long here.

The AI-security angle makes the split even sharper. Stronger models can find smart-contract, bridge, wallet, custody, oracle, and key-management weaknesses. That is bad for fragile DeFi, unaudited forks, bridge-heavy ecosystems, and long-tail beta.

BTC is the cleaner relative hold during AI-cyber scare windows because the base layer is simpler, more transparent, and more battle-tested. Higher-beta crypto becomes more attractive only after positioning resets or after protocols can prove real AI-assisted hardening.

Commodity Shorts

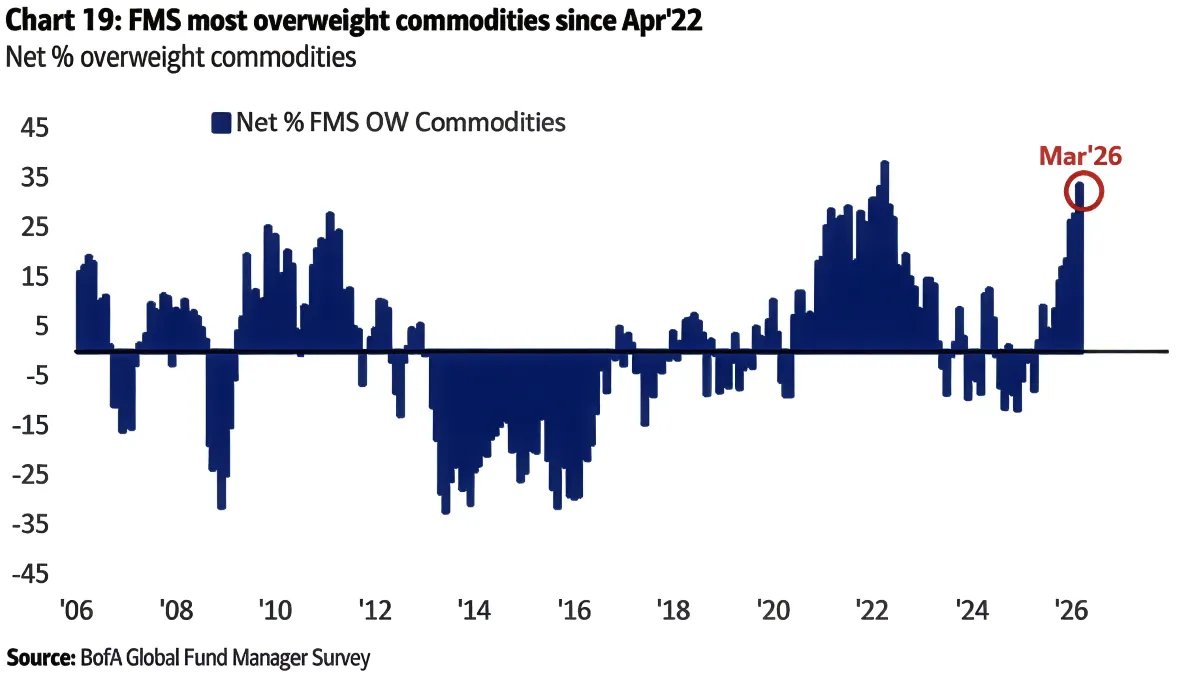

Commodity shorts make sense, but they need selectivity.

Copper is the cleanest candidate because positioning is crowded and client sentiment is long. Oil is the cleanest narrative fade. Platinum and palladium can work, but they are less clean. Silver is trickier because client longs are high, but COT is not as bearish. Gold is not a clean short to me after the earlier crowding reset.

So I would separate commodities instead of treating them as one trade. Oil and copper are the better short candidates. Silver and gold need more confirmation.

Bottom Line

My preferred ranking:

Bearish oil / energy on failed strength.

Long broadening equities.

Long duration.

Short AUD/CHF.

Avoid chasing semis and mega-cap AI hardware.

Keep crypto exposure smaller and prefer BTC over fragile long-tail beta.

Use selective commodity shorts, with copper cleaner than silver.

The big risk to this view is simple: surveys flip euphoric, clients stop being short equities, yields break higher again, oil confirms an upside breakout, or crypto positioning fully resets while AI-security risk gets absorbed faster than expected.

Until then, the setup still looks like a wall-of-worry equity market with crowded inflation/oil/semi narratives, and the better trades are in the fades and the broadening.

My current base case:

This looks more like a deflationary broadening trade than a simple "risk-on everything" trade.

The market still seems too worried about inflation and higher yields. BoFA inflation expectations are at 66%, around the 92nd percentile of the local 24-month history, while bonds are deeply under-owned. One BoFA chart topline shows investors net 44% underweight bonds, the biggest underweight since June 2022.

COT supports the same idea. Commercials are heavily positioned for Treasuries:

2Y Treasury: commercials 94.6 vs large specs 5.4

U.S. Treasury Bond: commercials 92.0 vs large specs 7.4

10Y Treasury: commercials 82.4 vs large specs 26.6

So if inflation and yield fears stop worsening, duration looks like one of the cleanest setups.

For equities, I am still bullish, but not through chasing the most obvious winners.

The broad equity COT picture is not bearish. Average commercial positioning across the current U.S. equity-index set is supportive, large specs are not crowded long, and small-spec breadth is only around the 38th percentile. That is not the kind of small-spec euphoria I would normally associate with a major top.

The survey layer also supports the bull case. AAII bulls are only 31.7, near the 9th percentile, while bears are 43.6, near the 80th percentile. NAAIM is elevated but not extreme. If the uptrend persists while surveys remain this cautious, that is usually wall-of-worry fuel, not a top signal.

So my equity view is:

Broadening over chasing.

I prefer Dow, Russell, midcaps, and other laggards over the already-obvious AI/semiconductor winners.

The reason is simple: BoFA shows the crowded trade is now long global semiconductors at 73%, with crowded-trade share around the 98th percentile. That does not mean semis must crash, but it does make the short-term risk/reward worse. The rally can continue while leadership broadens away from semis.

The cleanest FX expression still looks like short AUD/CHF.

AUD positioning is extremely stretched: commercials 1.0, large specs 99.7, small specs 91.3. CHF is closer to the opposite profile, with commercials high and clients heavily short CHF across crosses. That makes AUD/CHF a clean expression of over-owned cyclicality versus under-owned defensiveness.

Crypto is different. I do not think this is a clean buy yet.

Crypto Fear & Greed is low, around 29, and has been below 50 for almost two weeks. That can eventually become useful. But the rest of the stack is not there yet:

BTC COT: commercials 1.0 vs large specs 97.1

ETH COT: commercials 4.6 vs large specs 96.2

ETH clients are crowded long

Social sentiment is not washed out

So keeping some strategic crypto exposure can make sense, but aggressive new exposure does not look as clean as duration, equity broadening, or AUD/CHF. There is also a short-term narrative risk around AI, Mythos-style stories, and broader pressure on crypto credibility. That may eventually make crypto stronger, but it can create instability first.

On commodities, I am selectively bearish, but the evidence is uneven.

Copper is the cleanest short candidate: commercials 2.2 vs large specs 99.0. That fits the idea that cyclicals may be too optimistic if the deflationary/yield-down trade starts working.

Silver is more tactical. The client layer shows XAGUSD clients net long across three sources, so I would be cautious chasing silver here.

Oil is more complicated. My instinct is bearish if oil keeps failing to rally despite geopolitical and supply narratives. That kind of failure would be important. But the sentiment evidence is mixed: clients are already short WTI/Brent, and the Barron's energy cover was actually a contrarian support signal for energy. So oil needs price confirmation. It is not as clean as duration, AUD/CHF, or copper.

Platinum and palladium may fit the same commodity-short idea, but I would want more direct positioning evidence before ranking them highly.

Bottom line:

Long duration.

Long broadening equities.

Short AUD/CHF.

Avoid chasing semiconductors and AI leadership.

Avoid aggressive new crypto longs.

Look for selective commodity shorts, especially copper and maybe silver.

The strongest evidence is in duration, equity breadth, and AUD/CHF.

The most uncertain part is oil: bearish if price confirms failure, but not yet the cleanest sentiment-backed trade.

I think that it will get messy at some point, but this 10% correction just really flushed out the bulls and the bears that pilled in... are now getting squeezed.

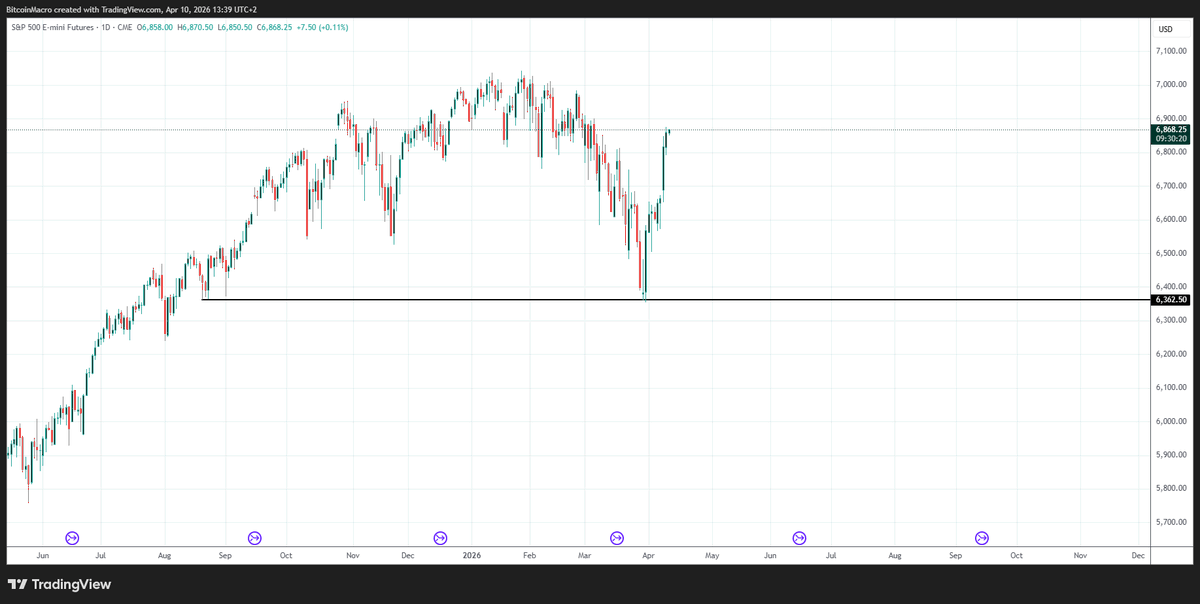

Based on all the data I am seeing right now, a 20% increase by the EoY for stocks is on the table.

The upside in risk assets doesn't seem to be over. The SPX will probably face resistance around 7200-7300, but it looks like the AI bull isn't stopping here.

Doesn't even feel that this is about money printing or deficits, but a real tech boom.

For US stocks, any company with access to Mythos or the top US AI models could accelerate to the upside.

If these models get released at some point, if top crypto devs don't have access to them (i.e. BTC, ETH, etc)... then crypto is in huge trouble.

It's clear that the market got too bearish and now rising. At least that's the case for stocks.

It's clear there is no ceasefire and that there will be a blockade either way, but maybe where we are going oil doesn't matter.

I see too many issues ahead, but positioning and sentiment clearly indicated that that the bottom is in the short-medium term.

Might not be a long term bottom, neither for stocks nor crypto, but for now the potential upside remains.

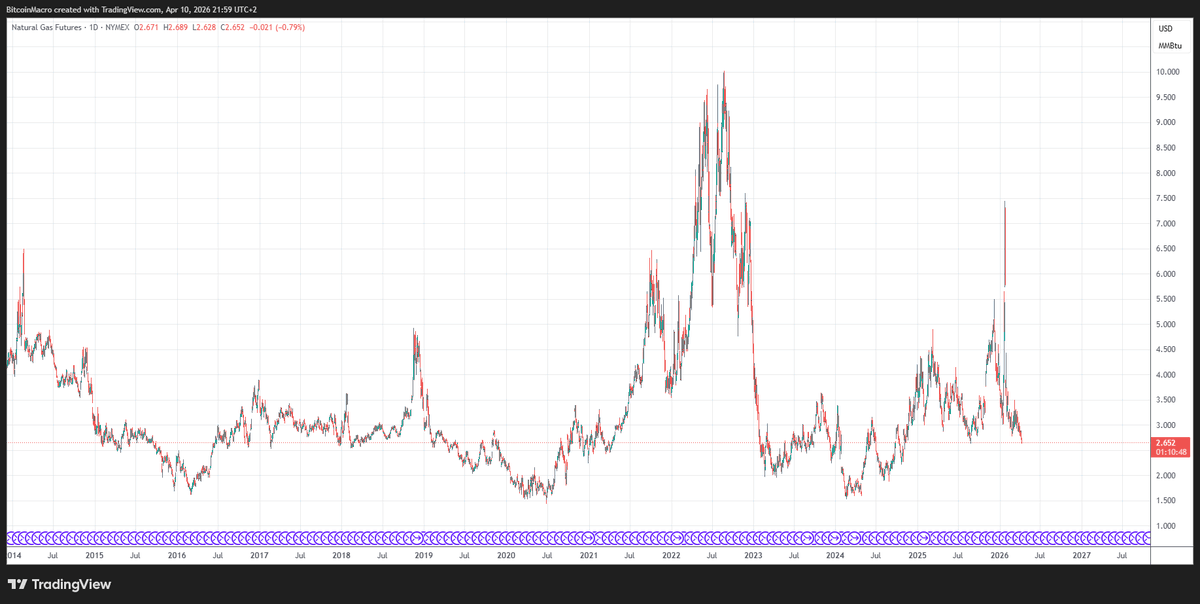

Oil is looking quite weak here. Other commodities like Natural Gas too.

Seems like positioning in commodities going into the war was already heavily long (at least that was the situation in March before oil had hit 120$).

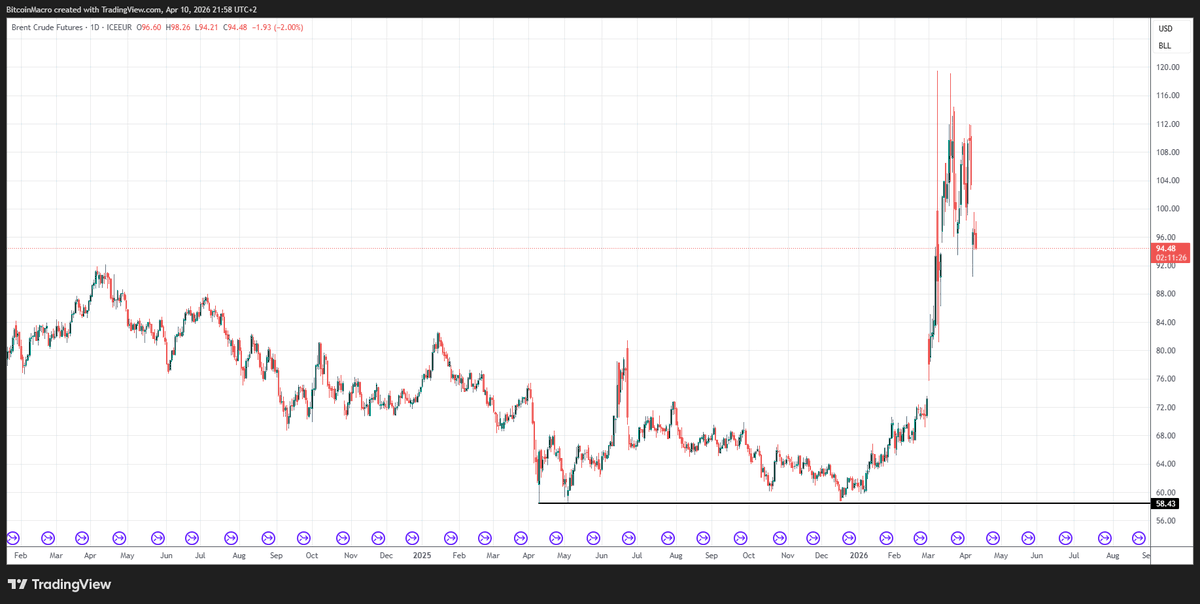

Brent is trading below Crude which is definitely signaling something. I think we are potentially in a heavy demand destruction phase both due to high rates, high oil prices, and AI disruption.

Oil has a double top higher, hence it could hit that level in the near future... but Brent also has a triple bottom lower. Wouldn't be surprised if we saw a complete collapse first before oil runs higher again.

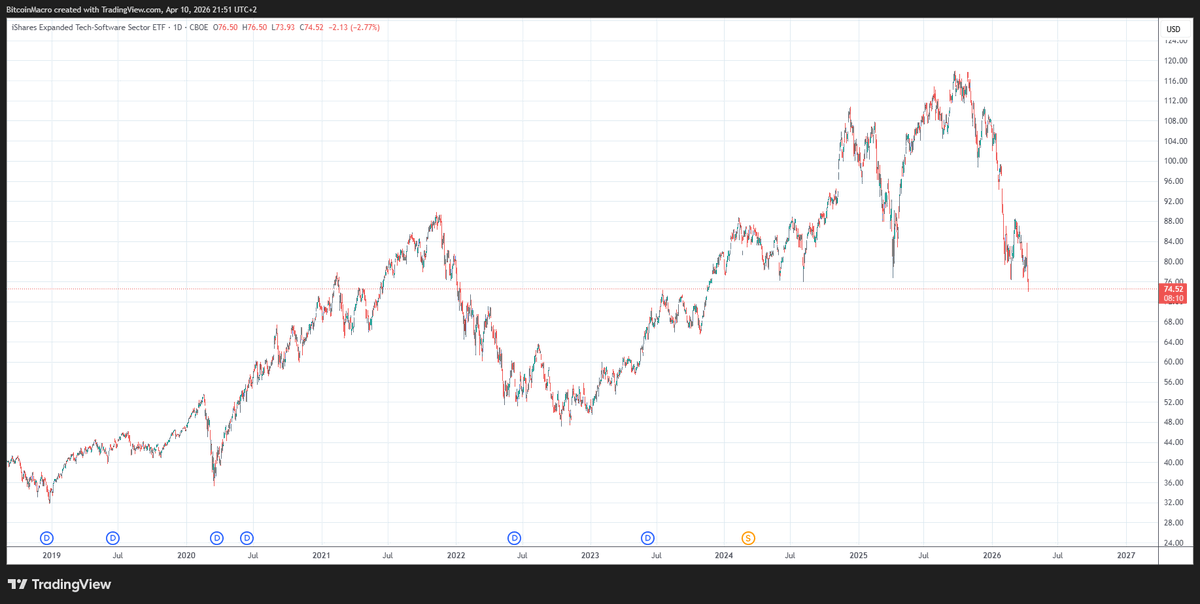

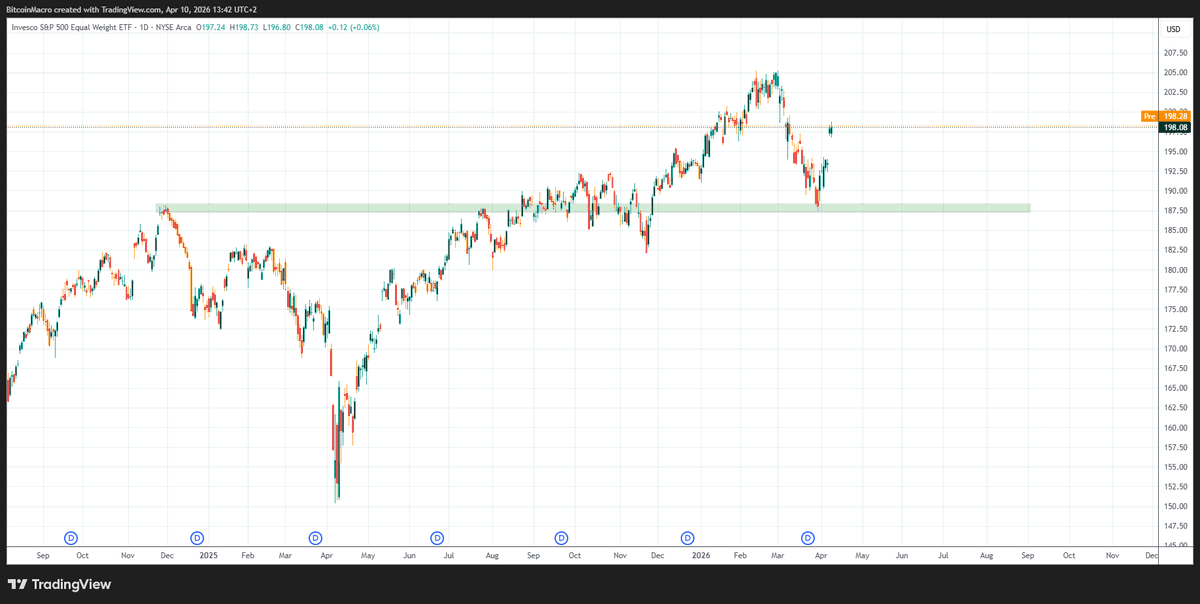

$IGV seems to have fully broken down. Probably due to #Claude#Mythos, which I think is totally real.

We are very close (and probably already there) to AGI. If not now, within a few months we will be. Getting 100% to SWE Bench Pro = AGI/ASI to me.

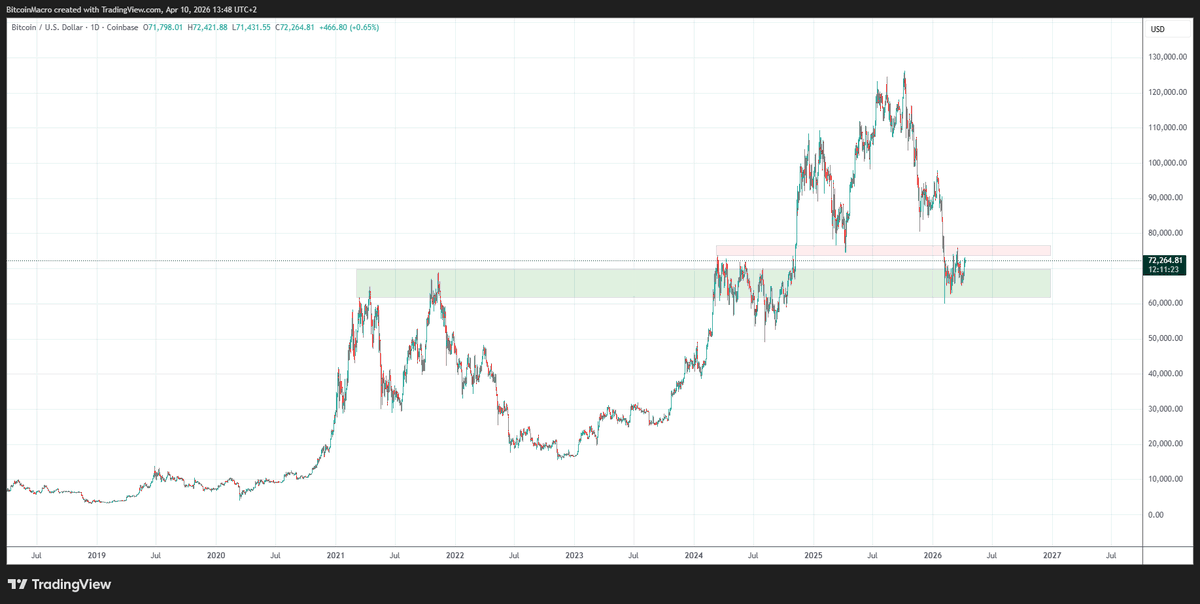

This has huge implications for everything, and markets will be affected too. #Bitcoin hasn't followed to the downside yet, but it definitely could...

It looks like it is Sep 2022... and haven't seen the final legs yet.

Will Anthropic help fix all the bugs? Will that be enough?

Right now it's very hard to see any significant decline for risk assets.

Even crypto seems primed for a strong rebound. Like the above indices retested their key breakout levels, one could say BTC did the same in the 60-75k area.

Although Crypto might be vulnerable due to AI (short term) and energy prices could go higher due to the war, markets have rebounded sharply after getting substantially oversold.

The S&P 500 swept several key lows and filled major gaps. Then rallied hard, erasing the war losses.

Sentiment got significantly bearish, while positioning seems to be pretty neutral (or was actually slightly bearish going into the war).

Extreme bearishness on the dollar has also subsided substantially.

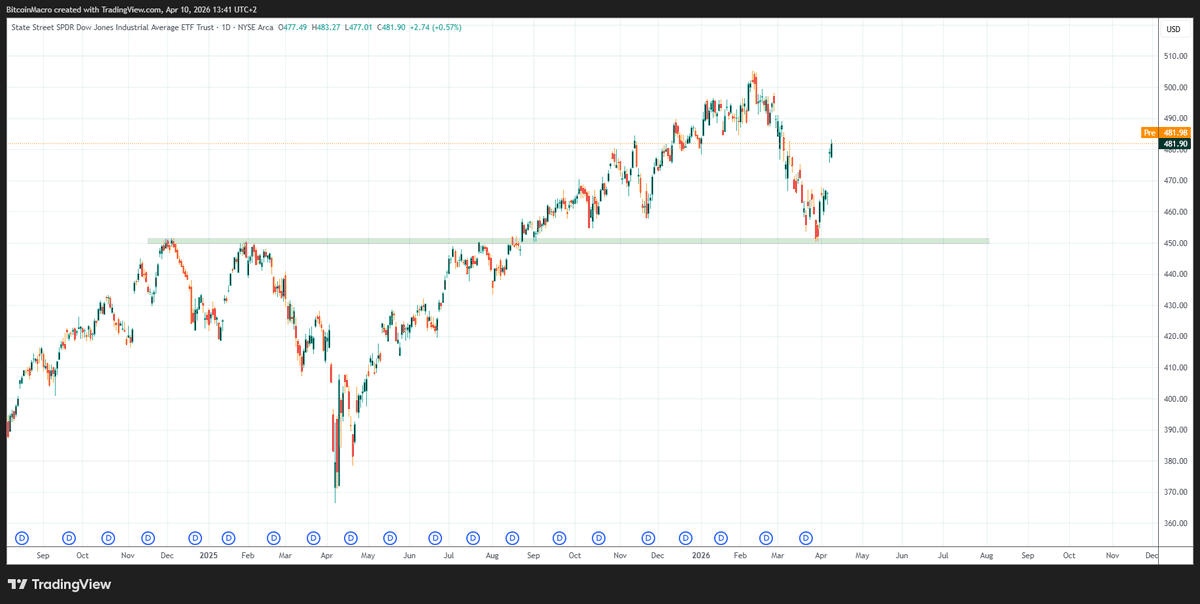

$RSP and $DIA retested key breakout levels and bounced perfectly.