Belated summary of 2025: +28,56%

1/x

Reflections on my mistakes and biggest holdings going into 2026.

Not too bad, not too good. When you are mostly focused on Nordic small caps, it is simply not good enough, taking the many great opportunities throughout the year

@AntonRosen2160@Havrebollen00 Enig i, at det er en lidt svag reaktion fra markedet. Dog er en større del af det som kom ind her i Q1, "lånt" fra fremtidige kvartaler.

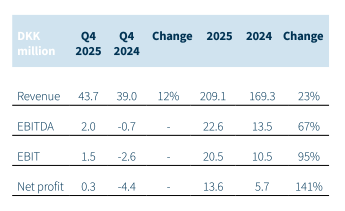

Hove: Rapporterade Q4 idag och 2025 växte starkt men uppvärderingen har varit försiktig (+25% sen i september).

EV/EBIT på 6x 2026e med modesta 10% tillväxt. Delar ut 25 öre nu som jag inte hade förväntat mig, ca 4,5% direktavkastning på det. >>

Belated summary of 2025: +28,56%

1/x

Reflections on my mistakes and biggest holdings going into 2026.

Not too bad, not too good. When you are mostly focused on Nordic small caps, it is simply not good enough, taking the many great opportunities throughout the year

28/x

and keeping to the promises made in 2023. They are gaining market share, having strong cost control, no M&A talk, and negative cost gearing coming to an end in Q2 2026 (adding 30-40m EBIT yearly). CEO Göran has also made a "symbolic" purchase after the Q3 report.

@spelbolagstorsk Very important market, but they already have operations in Orlando under “Hove Americas”, which is an American office, which isn't only a sales office.

@Ktharenlol It may also be that HelloFresh genuinely underperformed more than I anticipated in the Nordics, making it easier for Cheffelo to gain market share. Nevertheless, I was wrong, and I paid the price for that mistake. Congrats on the return though!🙌

@Ktharenlol At the time, at 37 SEK, neither the growth nor the margin outlook appeared strong enough to argue for a higher multiple, with EPS growth being the main driver of the expected return. These figures would only appear in a bull scenario;