This week’s Market Note with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers:

• Fed Outlook: CPI surprised to the upside, but markets still price a 95% chance of a cut at Wednesday’s FOMC. SEP projections and language will guide the path ahead.

• Inflation: Headline and Core CPI hit their fastest pace since January. Shelter cooled, but food and tariff-driven goods inflation picked up.

• PPI: Deflationary at -0.12% MoM, driven by margin compression—raising the risk of future pass-through pricing.

• Business & Consumers: NFIB optimism hit its best since January, while Michigan Sentiment slid as long-term inflation expectations rose.

• Housing: Mortgage rates dipped to ~6.5%, lifting applications to their highest since 2022. A “five handle” could unlock more buyer demand.

Watch the full episode and hear how these trends shape the macro outlook in the latest Weekly Market Commentary: https://t.co/Pshg0N8hsX

Main Management is pleased to share that the Net Expense Ratio of the Main BuyWrite ETF (BUYW) has been reduced to 0.99%, effective immediately.

“Lowering BUYW’s Net Expense Ratio to 0.99% encompasses our mission: Put clients first, deliver exceptional service, and manage what we can control, with the goal of allowing investors to keep more of their potential returns.” - Darol Ryan, Managing Partner at Main Management

We invite you to read the latest press release for full details: https://t.co/JCbp1vSlbc

This week’s Market Note with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers:

• Jobs: Payrolls rose just 22K, with June revised negative (the first decline since 2020). JOLTS, ADP, and job cut data all confirm a softer labor market.

• Participation & Unemployment: Prime-age participation hit a post-2024 high, while U3 and U6 unemployment climbed to their highest since 2021.

• Fed Outlook: Weak jobs data boosts odds of a September cut—90% for 25bps, 10% for 50bps—pending CPI/PPI this week.

• Productivity & Costs: Q2 productivity surged to 3.3% (best since 2023), while unit labor costs eased.

Watch the full recap and hear how these trends shape the macro outlook here: https://t.co/S5UDR8R6SY

This week’s Market Note with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers:

- GDP revised up to 3.3%

- Corporate profits rebound, margins steady

- Durable goods & capex show strongest gains in years

- Consumers spend more than inflation, energy costs decade-low share

- Housing prices soften, hinting at affordability

Watch the full recap and hear how these trends shape the macro outlook: https://t.co/qZxKV7buVT

This week’s Market Note with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers:

- Markets Move Higher: Broad strength across equities, led by small caps and healthcare. Tech and communication services cooled after leading much of the year.

- Fed Policy Shift: Powell’s Jackson Hole speech interpreted as dovish, with markets now leaning toward a 25 bps rate cut in September.

- Housing Strain: Existing home sales up, but high prices and rates keep the market tight. Inventories at highest since 2016; permits slowing sharply (lowest since mid-2020).

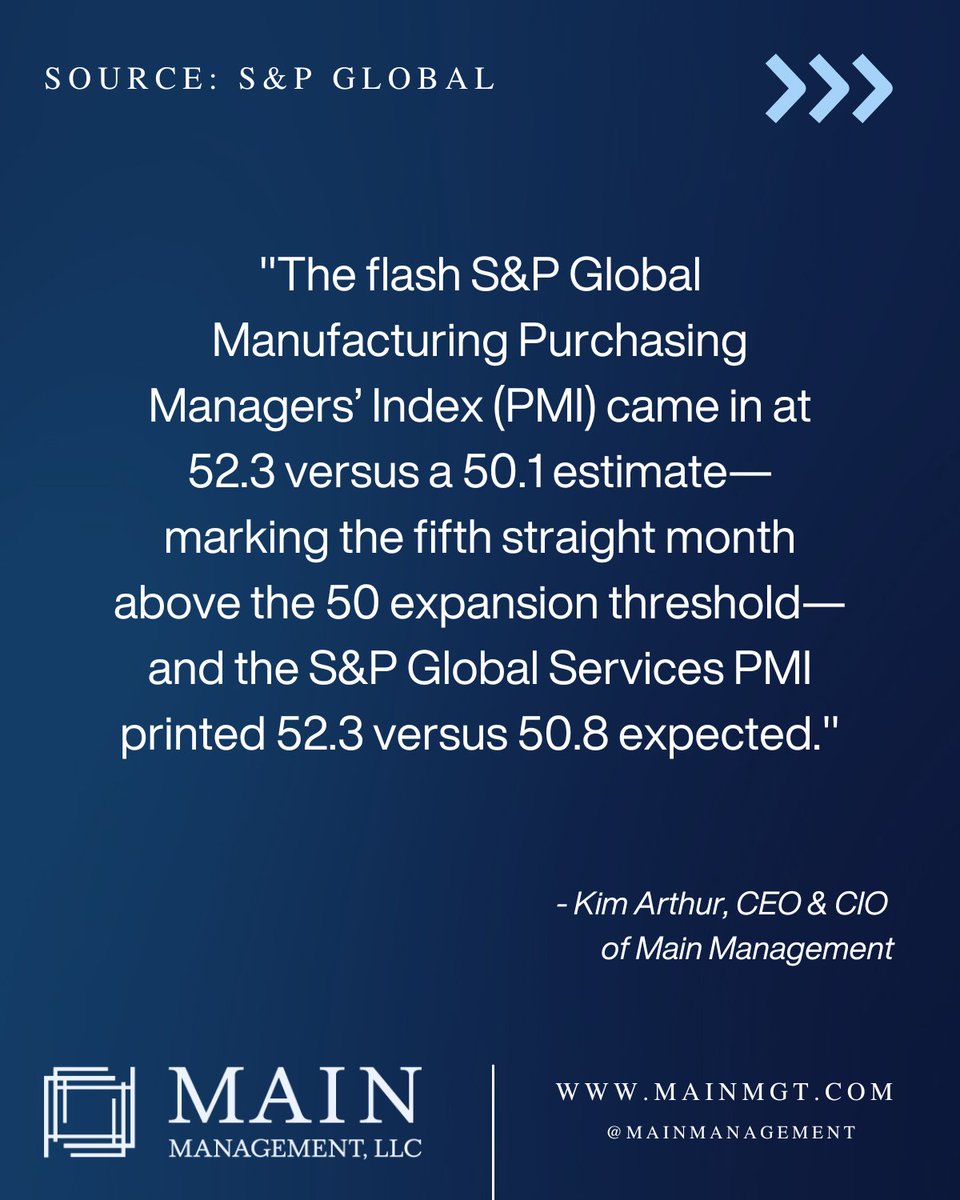

- Global Manufacturing Revival: U.S. PMI hits highest since 2022 (53.3), India strongest since 2009. Europe improving but still near contraction. Services more mixed, though U.S. remains solidly in expansion.

Watch the full recap and hear how these trends shape the macro outlook: https://t.co/mb11X3iW6a

This week’s Market Note with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers:

• Markets mostly green: Europe leads (+27% YTD); small caps and healthcare show strength, signaling broader rotation

• Inflation pressures: CPI in line (+0.2% headline, +0.3% core MoM); tariffs lift durable goods; PPI +0.9% MoM, biggest since March 2022

• Fed at a crossroads: Weak payrolls suggest easing, but hot inflation pressures tightening; September FOMC likely contentious

• Consumer resilience: Retail sales +0.5% MoM, June revised higher; autos and furniture rebound despite tariff uncertainty

• Industrial production mixed: Output soft, but AI-driven high-tech demand boosts semiconductors to strongest growth since 2021

Watch the full recap and hear how these trends shape the macro outlook: https://t.co/oOP37IZB3d

This week’s Market Note with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers:

- Markets climb: S&P +2.5%, led by Consumer Discretionary & InfoTech. Healthcare and Energy slip into negative YTD.

- Trade gap narrows: Deficit at $60.2B, lowest since Sept. 2023. Imports (-3.7%) and exports (-0.5%) ease post-tariff surge, with U.S. businesses absorbing most costs via margin compression.

- Productivity rebounds: Q2 +2.4% QoQ, best output growth since Q3 2023. Manufacturing logs 5 straight quarterly gains.

- Debt rises, delinquencies tick up: Household debt hits $18.4T (+$185B QoQ). Severe delinquency rates edging higher but remain below long-term medians.

- Mixed manufacturing & credit: Factory orders fall on transport volatility; ex-transports +0.4%. Consumer credit growth accelerates, driven by non-revolving loans.

Watch the full recap and hear how these trends shape the macro outlook: https://t.co/DIKzAap2YE

This week’s Market Note with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers:

- Business Survey Data: NFIB expectations and capex plans tick higher despite headline slippage.

- Bitcoin: Quietly making record highs.

- Copper: Futures jump on talk of tariff risks, flagging cost pressure.

- S&P 500: Dividend yield near a 150-year low as dynamics have shifted.

- Inventories: Durable-goods stockpiles post their steepest drop since 2020.

Watch the full recap and hear how these trends shape the macro outlook: https://t.co/vHMRBsDmws

“Trust, transparency, and true partnership.”

In this candid conversation between Kim and @RustyVanneman , Main Management’s new Advisory Board Chairman Rusty Vanneman, CMT, CFA, BFA™ shares why joining Main Management was an easy decision — and what sets the firm apart after decades of due diligence across the industry...

This is a must-watch and/or listen episode: https://t.co/mp8X8J5WNy

This week’s Market Note conversation with Alex Varner (Head of Research) and James Maxwell (VP of Research) covers a full slate of developments across geopolitics, Fed policy, and key macroeconomic data...

Click here to watch the full episode for in-depth insights on what’s driving markets and where things may be headed next: https://t.co/9e3tQJ2EnG

Highlights include:

- Israel–Iran tensions escalate, pushing oil and energy prices higher

- FOMC holds rates steady; projections still call for two cuts in 2025 despite weaker GDP and rising inflation expectations

- Retail sales, industrial production, and housing all show soft data as high interest rates and prices weigh on demand

- The U.S. deficit remains in focus, with spending outpacing revenue despite tax inflows

Looking ahead, the team previews key data to watch — including the final Q1 GDP release and the all-important Core PCE and consumer spending figures due Friday. Be sure to check back weekly for regular updates from the team at Main Management.

This week’s Main Management Weekly Market Note with Alex Varner & James Maxwell dives into the latest CPI release, where inflation cooled more than expected as tariffs didn’t spark the price jump many feared.

We break down why core inflation is at its lowest since March 2021, how tariff impacts are shaping up to be more contractionary than inflationary, and what it means for the Fed’s next move.

Watch the full update for expert insights on inflation trends, policy risks, and the path forward for markets: https://t.co/Ba0JUeMZ8j

This content is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. All views expressed reflect current analysis as of the date of recording and may change without notice.

This week’s Main Management Weekly Market Note covers everything from inflation trends to surprising consumer strength and a look ahead at key economic data. Plus, we announce our new Chairman of the Advisory Board - @RustyVanneman !

Watch the full update for expert insights on market dynamics and what’s next: https://t.co/eOjyuoOn1p

Main Management is excited to announce Rusty Vanneman as our new Chairman of the Advisory Board. Rusty is a widely respected investment executive with over 35 years of experience in the financial industry. A long-time friend of the firm and a yearly speaker at our Top Advisor Conference, Rusty epitomizes our core values of “Client First, Exceptional Service.” We are thrilled to have him help advise on our next chapter of growth in the coming years.

Access Rusty's full bio via the link below:

https://t.co/9pUXOLW8PE

📈 Watch the full episode: https://t.co/TljdhoMNVR

In this week’s episode, the Main Management Research Team — Alex Varner and Alex Dippery — covers a data-heavy week filled with meaningful inflation and sentiment updates:

✅ Encouraging inflation readings, as April CPI came in cooler than expected (+0.2% MoM), with core PPI down -0.4% MoM — the biggest drop since April 2020

✅ Small business optimism (NFIB) dropped below pre-election levels as tariff uncertainty weighs on confidence, CapEx plans, and pricing intentions

✅ University of Michigan consumer sentiment dropped to its second-lowest reading ever; inflation expectations surged to 7.3% (1-year) and 4.6% (5-year), with divergence by party beginning to narrow.

With inflation readings softening and economic sentiment deteriorating further, the Fed may gain more room to cut — but ongoing tariff impacts and consumer expectations remain key risks to watch.

📝 Read the full Weekly Market Note: https://t.co/KMVORtAVHV

📌 This content is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. All views expressed reflect current analysis as of the date of recording and may change without notice.

🔔 Subscribe for more Weekly Market Commentary and research insights!

📈 Watch the full episode: https://t.co/fKTC5U3Sec

In this week’s episode, the Main Management Research Team — James Maxwell and Alex Dippery — covers key developments in markets, inflation, and policy, including:

✅ Q1 productivity posted a negative reading, but the 20-quarter trend remains solidly positive — underpinned by rising AI adoption

✅ Trade balance confirmed Q1 import surge driven by tariff front-running; pharmaceuticals stood out with a major increase

✅ Major tariff de-escalation announced: U.S. drops effective rate on China from 145% to 30%, China reciprocates — signaling renewed cooperation

✅ FOMC stays on hold; Powell reiterates data dependence and inflation vigilance, even as labor market risks increase

✅ Inflation expectations remain elevated in the short term, but 3- and 5-year expectations are holding steady — a key focus for the Fed

With tariffs easing and disinflation trends holding (for now), all eyes are on upcoming CPI data and Fed commentary to gauge the path forward for rates and growth.

📝 Read the full Weekly Market Note: https://t.co/iwQtDylvew

📌 This content is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. All views expressed reflect current analysis as of the date of recording and may change without notice.

🔔 Subscribe for weekly market commentary and research insights!