Is Islamic banking Islamic?

In my column I examine if Islamic banking in Pak is just based on interest rates or is it close to Islamic ideals. https://t.co/2TjpM0k2UG

“There are three decisions in life: a good decision, a bad decision and no decision.”

We celebrate good calls and we learn from bad ones.

But standing still is the real danger.

Will Greenwood on decision-making on and off the rugby pitch.

پاکستان میں ڈگری ویریفکیشن پر نظرِ ثانی کی ضرورت ہیں بطور گریجویٹس ہم یہ توقع رکھتے ہیں کہ ہماری یونیورسٹیاں کی ڈگری ہماری محنت اور کامیابی کی پہچان ہو۔ لیکن حقیقت یہ ہے کہ ڈگری ویریفکیشن کا عمل ایک طویل، مہنگا اور مشکل سلسلہ بن چکا ہے جو طلبہ کو ذہنی اور مالی طور پر متاثر کرتا ہے۔

سب سے پہلے یونیورسٹی ڈگری جاری کرتی ہے جس پر کنٹرولر امتحانات اور وائس چانسلر کے دستخط ہوتے ہیں۔ اس کے باوجود وہی ڈگری دوبارہ ویریفکیشن کے لیے یونیورسٹی بھیجی جاتی ہے، پھر ہائر ایجوکیشن کمیشن (HEC) کو تصدیق کے لیے بھیج دی جاتی ہے، اور آخر میں وزارتِ خارجہ (MOFA) سے اٹیستیشن کروائی جاتی ہے تاکہ HEC کی مہر کی بھی تصدیق ہو سکے۔

ہر مرحلے پر اضافی فیس، تاخیر اور غیر ضروری مشکلات طلبہ کا انتظار کر رہی ہوتی ہیں۔ یہاں ایک سنجیدہ سوال پیدا ہوتا ہے: جب ڈگری پہلے ہی تسلیم شدہ ادارے جاری کرتے ہیں تو طلبہ کو بار بار اس کی اصلیت ثابت کرنے کے لیے ادائیگی کیوں کرنی پڑتی ہے؟

پاکستان کو ایک ون ونڈو اور سادہ ویریفکیشن سسٹم کی ضرورت ہے جو تکرار کو ختم کرے، وقت اور پیسہ بچائے اور نظام پر اعتماد بحال کرے۔ ڈگری ویریفکیشن کو آسان بنا کر ہم نہ صرف گریجویٹس کو بااختیار بنا سکتے ہیں بلکہ اپنے تعلیمی نظام کی ساکھ کو بھی بہتر بنا سکتے ہیں۔

اگر آپ واقعی نظام میں تبدیلی چاہتے ہیں تو اس پوسٹ کو repost کریں اور ہماری آواز کو مضبوط بنائیں۔

In 1983, Steve Jobs predicted the next 50 years of technology.

His predictions:

• iPhone

• Internet

• Softwares

• App stores

• Artificial Intelligence

10 futuristic predictions from this talk that came true:

1. Every major revolution starts ugly

They predicted the Great Depression. Then the 2008 crash. Then 2020's inflation surge.

A group of economists spent 150 years warning about the same pattern.

Nobody in power listened.

And every time, they were proven right.

This is the story of the Austrian School. 🧵

There is a common misperception that high remittances are good for GDP, and growth - *not necessarily*

A simple scenario:

Y = C + I + X - M is the accounting equation linking GDP (Y) to consumption (C), investment (I), exports (X) and imports (M)

One scenario is that 10B dollars of remittance inflow raises consumption by the same amount, and are used to finance additional imports by the same amount

The economy has higher consumption, but same output. Remittances have ZERO effect on GDP in this example

More generally …

MLCF’s acquisition of PIOC (future earnings outlook):

The deal is being done at an attractive price, below the cost of building a new cement plant, which means MLCF is buying capacity cheaply. With both plants located close to each other, costs can be reduced through shared logistics and better efficiency. PIOC mainly sells locally, while MLCF can use its stronger network to improve volumes and exports. Over time, this merger should improve margins, cash flows, and market share, supporting strong upside in the stock.

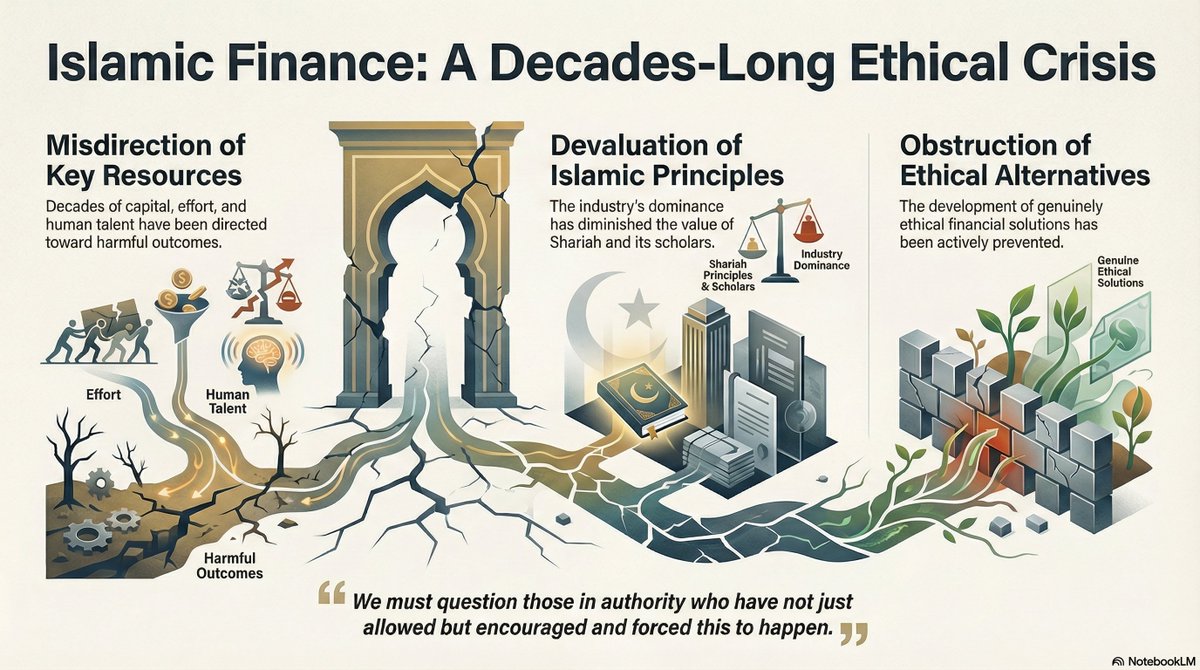

Part 4/4 Islamic banking is not a compromise with Riba. It IS Riba — industrialised, licensed, and Shariah-approved

Series - Why Islamic banks Lend instead of invest - The Economics They Don't Want You to See. - From an Insider who built this machine

BEGINNING

In the previous parts we have observed the following:

Islamic banks are subject to stringent regulatory requirements, such as Basel 3, which requires banks manage the risks that they enter into by taking certain measures. A key measure is that the bank must allocate sufficient regulatory capital to meet the risk of adverse events, such as their customers (borrowers) failing to repay loans, and other assets of theirs falling in value (or being illiquid such that they cannot effectively be utilised in emergency scenarios)

The consequences of these regulations mean that lending is far more efficient than actually buying an asset or making an investment. The latter two attract much higher risk weightings, meaning they are less efficient for the Islamic bank.

With the addition of credit creation, this inefficiency is now longer just impractical, it is downright impossible. Credit creation can be utilised for lending and not for investing or buying assets. As such, the Islamic banks can deliver 30x more loans than a single investment of the same size, and when it comes to residential property, it can make over 40x more profit with the same capital outlay (cash and regulatory capital) than buying a property outright,

Islamic banks obtain a banking license that permits them to lend whilst putting the deposits at risk. It is this activity that requires a banking license (as defined by the Bank of England) and the following activities do NOT require a banking license:

- The taking of deposits

- The provision of loans (look at the proliferation of nob bank credit providers in the market).

- The buying of assets, such as property, commodity, Palm Oil, or milk cartons

- The holding, and selling of such assets

- Investments into any financial assets

So, if an entity goes through the process of obtaining a (Islamic) banking license, then it will be intending to lend money whilst putting deposits at risk.

And the process of obtaining a banking license is not something you wake up and decide. It is a long onerous and expensive process.

For example, in the UK, Revolut obtained its banking license in 2024, and it took their application 3 years to be accepted, and at the time they had 9 million customers in the UK and group revenue of over £2bn.

As noted in FinTech Weekly:

“A full UK banking licence would grant Revolut access to the domestic lending market, enabling it to deploy customer deposits for loans and other credit products. Such a move could introduce new competition to established high-street banks, particularly in digital consumer finance.

However, without the licence, Revolut’s capacity to operate as a traditional bank remains limited. The company continues to function as a hybrid platform that combines payments, foreign exchange, and investment services under its existing permissions.”

So, we have an Islamic bank, that has undertaken the serious, lengthy and expensive process of obtaining a banking license, the primary benefit of which is it can now lend money.

There is also another benefit of a banking license, which is that it can engage in credit creation, a right that is given to private banks and to no other entity on the planet. (This is, in fact a monstrous right that they have, and is the source of much of the financial slavery we experience today).

Islamic banks also have this right to effect lending via credit creation. And that is WHY they obtained a banking license in the first place.

The result is that for an Islamic bank to buy a real asset, instead of lending, it must accept making 1/40th of the profit it can make via lending. This decision is suicide.

If they did not have a banking license, and instead actually purchased property, and made investments, such as is the activity of a huge portion of the global investment market, then they would not be subject to such comparisons, They would utilise real capital, make real investments and be forced to deliver efficiencies to ensure their investments are profitable. All of these are good things, and especially so in Islamic Finance.

So, we must conclude, that the fact that Islamic banks have decided to obtain a banking license means they have already worked all of this out and decided that lending is the way to go.

Now, of course, lending money and making profit on it is Riba. So they cannot do that.

But they must utilse credit creation to benefit from this 40x profit leverage, so what do they do? What they do is very simple.

They utlise simple Shariah contracts such as buying and selling to instead replicate this lending, This provides the required façade to enable some scholars to provide Shariah approval and thus the activity of the bank is now Shariah compliant.

My position is that the robust and intellectually honest application of Shariah to these trading activities of an Islamic bank would result in this Shariah compliance being removed.

So, we now have a clear presentation of the battlefield:

- An Islamic bank has a banking license and thus must lend to benfit from this 40x profit leverage

- An Islamic bank cannot be seen to be lending money as this results in Riba

- Islamic banks thus engage in buying and selling to replicate the effect of lending (thus gaining access to this 40x profit leverage) whilst demonstrating that their activities are simply buying and selling and thus Shariah compliant

If the above was true, we would see certain outcomes be clear:

- When an Islamic bank is engaging in trading, the outcome would be the same as a loan

- Any sales activities that result in the bank taking risks on the underlying assets must then be tweaked such that any asset risk is removed For example:

- The bank will buy and then immediately sell an asset

- The bank takes no risk on the delivery or performance of this asset

- The bank will only buy the asset once the immediate sale of it is contractually certain

- When the bank buys assest (cash out) it will pay immediately and when it sells an asset (cash in) it will sell it on deferred repayments to replicate the required loan

- The sale to the customer (to effect the loan repayments) will be a function of the loan size, the repayment time, and the market interest rates (just like a regular loan)

In market practice we see every one of these outcomes, all the time, every time.

And this is all deemed as Shariah compliant because basic rules of sale contracts are followed. But the rules around combinations of sales contracts are ignored. It si this combination that results in the loan and Riba, not an isolated sales transaction in itself.

So the Islamic banks now apply themselves to present these sales transactions as standalone, isolated sales transactions, and not structued as a combination of 2, 3, or 4 circular sales transactions.

When we play games with Shariah, I have seen that something happens. It forces us to encounter anomalies and plain impossibilities. Because our Shariah is never intended to be used to justify lending and Riba, and when we force this, the reality then forces outcomes that are plain impossible. It is these outcomes that everyone must lie about, or plain hide from scholars. For example:

- When the banks conduct a Tawarruq transaction, which is a sequence of sales transactions, we end up having to claim that a commodity broker, with £5mn is buying and selling commodity worth £1bn in a single transaction

- We have a commodity / Tawarruq exchange in Malaysia that is selling $25tn of commodity a year, when only $2bn max of that commodity exists, and the Shariah requirement is that the commodity must be delivered to the buyer if requested

- We have billions of dollars of Islamic loans being effected by the buying and selling of commodities that nobody every wants, like platinum, timber, copper, palm oil and milk cartons

- Whenever an Islamic bank sells something it is replicating the repayment of a loan with interest, so that sales prices is deferred, repaid in the future, and benchmarked to interest rates, just like a loan demands

- When an Islamic bank sells something, it has to buy it first, but it will have cast iron guarantees, BEFORE it buys the item, that it will be onsold immediately to the customer

- The Sukuk market, which comprises 25% of the global $4tn Islamic finance industry, is built on the apparent investment into assets, but all risk of asset ownership is systematically removed, piece by piece, so what is left is a bond which is Riba (I have written a whole book about this and made a 2 hour video about a single Sukuk issuance showing all this complex trickery works in practice)

- A Malaysian professor from INCIEF analysed 900 Sukuk issuances over 15 years and found precisely ZERO retain asset risk and performance, and all deliver bond performance, which is Riba

- We have a multi trillion business built on organised commodity sales to deliver Riba and supported, in a 250 page policy document, by a simple statement that sales transactions are permitted in Shariah, and quoting one verse from the Quran

- We have Islamic banks whose balance sheets are comprised between 95-99% (assets and liabilities) of interest rate instruments, not sales and investments

This is utter madness.

This is diabolical

We have systemically chosen Riba as our foundation (Islamic banking) and we have consistently, and relentlessly, delivered Riba via the guise of Shariah compliance, and we have built an army of scholars who fight to approve it and preserve it.

We are wholly lost.

We are wholly to blame.

In this part 4/4, I was meant to also address solutions, but our descent into madness prevents that. I will write a part 5/4 that looks at solutions and what the way forward must look like.

I have played a big role in building this monster, this abomination, and this is part of my public penance, my tawbah, and my duty to expose what I know. I have blame here, and do not seek to avoid it. I face it full on and ask for forgiveness.

My only aim is to lighten my scales on the Day and be a servant of Allah swt.

May Allah swt forgive us

Part 5/4 to follow - the way forward out of this diabolical mess

Why (Islamic) Banks Lend Instead of Invest: The Economics They Don’t Want You to See

Part 3/4 , see the 1min video here and the full post below 👇

See how lending for Islamic banks is 42x more profitable than investing and helping the real economy

For 40 years we have been told Islamic banking is “ethical, asset-backed, and different.”

I’ve spent 25 years inside the system.

The truth is far worse — and far simpler.

Islamic banks don’t invest in assets. They manufacture debt.

I’ve broken the entire hidden architecture into a 4-part series.

Part 1 drops tomorrow.

Here’s the core problem in laid out in four images:

Why (Islamic) Banks Lend Instead of Invest: The Economics They Don’t Want You to See

PART 1/4

My criticism of banking, and, by extension, Islamic banking is well documented. A common response to this is along the lines of the following:

- It might be not perfect, but these are steps in the right direction

- Islamic banking is a young industry, and we need more time to develop

- Islamic banks are just trying to be commercial in a competitive industry

- Let’s support all the work that has been done, and let’s continue to build on it and support improvements

Any my response to these points has, unwaveringly, been as follows:

- Banks (including Islamic banks) are built on debt - debt is their DNA, they cannot change

- Banks must lend or they will die

- Of all the models we could have chosen to build on, the selection of a banking platform is immensely damaging to Muslims, and could only have been a decision encouraged by the enemies of Muslims

- Waiting for a bank to move from debt and lending, to real investment, real profit sharing, and beneficial direction of capital, is like waiting for the sun to rise in the west

For those familiar with my stance, you will notice that I have watered down the wording of my positions, so that I do not exclude those who might be supportive of Islamic banks. I would say that the supporting of Islamic banks can only be a position based on ignorance, or the will to harm Muslims, but I will not say that here. Yet.

In the early days of my Islamic finance career, before Blackberries were the newest thing, when we still sent faxes to execute deals, I was not aware of many of the structural imperatives that decided for banks what they must do. What I did see, were the consequences of these imperatives.

I observed deals being executed that started off as regular sales transactions, or what appeared to be investments in real assets, but then were combined, or structured in such a manner (often by myself) such that the end result bore no resemblance to what was initially presented.

I created products on Murabaha, Musharakah, Wakala, Mudarabah – and all of them, invariably – were tweaked,amended, deconstructed - and turned into debt.

This structuring process was at the heart of my role as Global Head of Islamic Structuring at JP Morgan, and my roles in setting up the Islamic banking teams at UBS and Credit Agricole investment banks. It was something I actually enjoyed, and it was very challenging.

My main aim was to make money for my bank, and if I failed in that, I would have been fired. And quickly. In order to make these large amounts of profit, I had to understand what the markets wanted, and my clients were all Islamic banks. I had to gain an expert knowledge of what they wanted, what tools we had available to us, and how to use those tools to deliver what was required. The conventional banks I worked for never presumed to have a position on what is good or bad in Islamic finance. Their stance was:

- We are here to make money

- We need to do what our clients want

- We don’t care if Islamic finance / banking is good, bad, ethical or downright Satanic

- Tell us your rules, your requirements, what you want, and we will deliver it or Safdar will lose his job

What I did notice was that, if I wanted to keep my job, I had to deliver debt to the Islamic market. And, virtually, all the time.

There were exceptions. We created some funds, which were fun, and actually invested in real things and made profit for investors. But in terms of size, these funds probably totally $500mn and the debt I delivered was at least $20bn, and more. And I was not even the debt specialist in my teams, and they did more.

I also delivered many solutions that were needed because of the size and complexity of the debt that was created, We found that Islamic banks, once they started to accumulated debt instruments and liabilities on their balance sheets, had a need to manage this interest rate risk. So I personally constructed the first Profit Rate Swaps in the sector, which have some of the most involved and complex characteristics of any products I developed.

We also delivered currency and treasury risk management solutions to Islamic banks. These were lots of fun too, to develop.

But all of these were needs of the market that arose because of their entrenchment in debt. Manage interest rate risk because they were giving so many loans of differing tenors and risk profiles to clients. Manage currency risk because they were busy in giving loans in different currencies.

Before I get lost in the nostalgia of the “good” old days, let’s bring this back to the topic at hand.

While I was structuring all these weird and wonderful products, I noticed that everything led back, in an indirect and roundabout sort of fashion, to debt.

And, clearly, I noticed the structuring elements that converted the purchase of commodity, or the apparent investment into property, or oil fields, that converted these transactions into debt products. I noticed this because I was the one who did it.

I knew Islamic banks liked debt, and had debt everywhere in their business, but did not understand how deep this need was, and why it arose. Perhaps I thought it was because they just saw it as easier to manage and everyone wants loans, so it’s an easy way to make money.

It took me some years to delve deeper into this, and to gain some understanding of the underlying conditions that resulted in these actions. And the more I discovered, the more depressed I became.

In this paper, I want to provide a mechanical, practical and realistic example of why Islamic banks love debt. And why it is insanity to expect Islamic banks to somehow develop, or improve, and move away from debt.

As I sit here at a café while writing this, watching the world pass by, I think it is more likely that the whole street is lifted into the air, and turned over, and deposited back upside down onto the ground, than seeing Islamic banks move away from debt.

PART 2/4 tomorrow, the details of the beast inside that force Islamic banks to embrace debt and Riba

Stay tuned