Mizuho is defending $SOFI against the Muddy Waters short report:

• The $312M JPM transaction looks like a true sale (not hidden debt)

• The 3.9% discount rate looks reasonable for a ~4-year loan duration

• SOFI’s filings clearly distinguish true sales from secured borrowings

• Fitch data & company disclosures align more closely with management’s figures

• The charge-off rate appears closer to 4.4% (not 6.1% alleged in the short report)

A great conversation with @AnthonyNoto, @FunOfInvesting, and @Futurenvesting on where SoFi has been and what's ahead.

Watch the full conversation and let us know what you think! 💭

📣 SoFi delivers another record-breaking quarter! In Q4 we delivered a record $1 billion in adjusted net revenue and had the biggest increase in new members and new products in SoFi history. This is durable growth, powered by our one-stop shop.

Full results here: https://t.co/3k9lYlj7Nr

$SOFI 🚨BREAKING NEWS🚨

JP MORGAN CHASE has increased ownership by an additional +39% 📈

Total Shares: 65,000,000👀

Total Value: 1.7 Billion 💰

They have surpppased BLACKROCK in total shares

citadel is about to get fucked up in china. incase you were wondering this is how america could fix the market along with removing rule 203b fill before locate the bernie madeoff exemption.

BREAKING 🚨 UNDER GARY GENSLER’S LEADERSHIP, THE SEC HAS BEEN CAUGHT COLLUDING WITH WALL STREET

FOIA records reveal a broker trade group pushed the SEC to deny an S-1 due to unaccounted-for shares, known as naked shorts ⬇️ $MMTLP

.👇Yes, sir. If this is enacted—and that’s a big if, though part of me hopes it is—we would likely see a significant contraction in industry credit card lending. Credit card issuers simply won’t be able to sustain profitability at a 10% rate cap.

Consumers, however, will still need access to credit. That creates a large void—one that @SoFi personal loans are well positioned to fill. I’ve long believed many consumers are disadvantaged by high-reward credit cards (they know who they are), only to end up carrying tens of thousands of dollars in balances at 20–30% APRs. In many cases, those balances are effectively interest-only and can persist indefinitely.

By contrast, a SoFi personal loan at 9–13% offers a lower rate with a fully amortizing structure that actually pays the balance down. If credit card lending contracts, SoFi can step in to offer borrowers a more transparent, lower-cost alternative to revolving debt. We could also expand to a larger target market & appropriate rates with still great returns.

This dynamic would also materially simplify marketing. Today, credit cards win the acquisition battle because consumers don’t realize they’re signing up for high-interest, long-duration debt—until they’re already deep in it. Only then do many borrowers find @SoFi as a solution to an existing problem. If credit card lending contracts, SoFi personal loans become the solution before the problem exists, not after. SoFi marketing shifts from debt consolidation to smart upfront financing.

Bottom line: less credit card lending could translate directly into more personal loan demand for SoFi. Giddy up!!

Also if this scenario plays out, underwriting discipline and borrower education become even more important—SoFi’s advantage isn’t just price, it’s helping customers exit debt, not revolve in it. GYMR!!

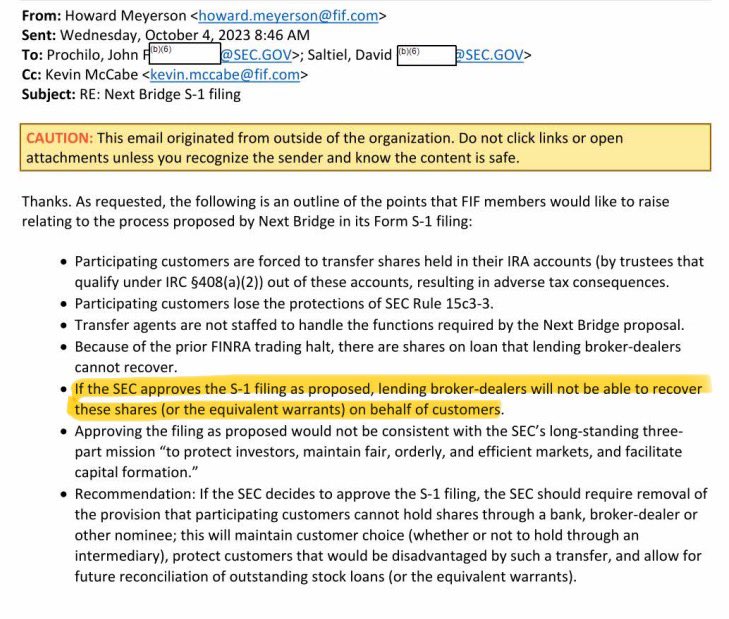

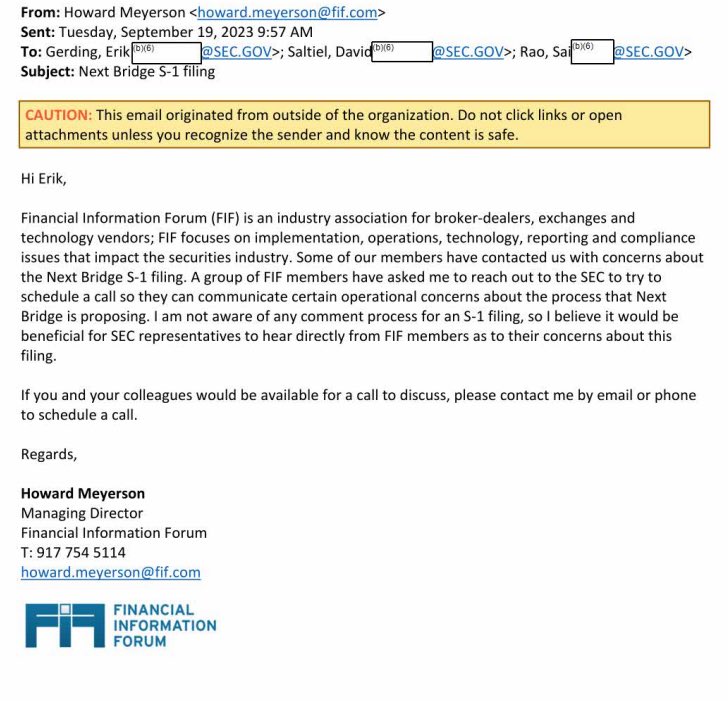

BREAKING🚨 SEC EXPOSED IN COUNTERFEIT SHARE (NAKED SHORTING) COVER-UP

- Internal emails reveal private coordination between FINRA, the SEC, and the broker-dealer lobby (FIF) regarding $MMTLP, showing concerns over unrecoverable loaned shares (COUNTERFEIT SHARES).

➡️ Regulators and broker-dealers were aware the share count didn’t add up.

➡️ Their own communications show the priority wasn’t investor protection.. It was containment and damage control to protect brokers.

The concern wasn’t shareholders, but the reality that loaned short shares could not be recovered after the trading halt.

Approving the S-1 as proposed would have locked in significant losses for lending brokers.

That’s why an independent, audited aggregate share count has never been released…

And why shareholders still aren’t being told how severe the imbalance really is.

More than two years later, the SEC still has not approved the company’s S-1 filing.

SEC & FINRA are in on it, and not doing a single thing to protect retail investors 🚨

🔂 Repost to spread the word about the corruption carried out by our OWN regulators 🚨🚨

$GME $AMC $MMTLP $OPEN $BYND $GNS $QNTM

JUST IN🚨 Letters Sent to Over 50 Publicly Listed Companies Urging Investigations Into Potential Short & Naked Shorting Manipulation

Retail United Advocacy Group is calling on CEOs of companies such as $GME $AMC $MSTR to initiate investigations

REPOST 👍 IF YOU SUPPORT THIS

Uh-oh ROBINHOOD IS IN TROUBLE 🚨🚨

All RETAIL investors should repost the below post to show HOW CORRUPT THESE BROKERS ARE⬇️⬇️⬇️

$GME $AMC $BYND $BBBYQ $MMTLP $GNS $MSTR $OPEN $QNTM

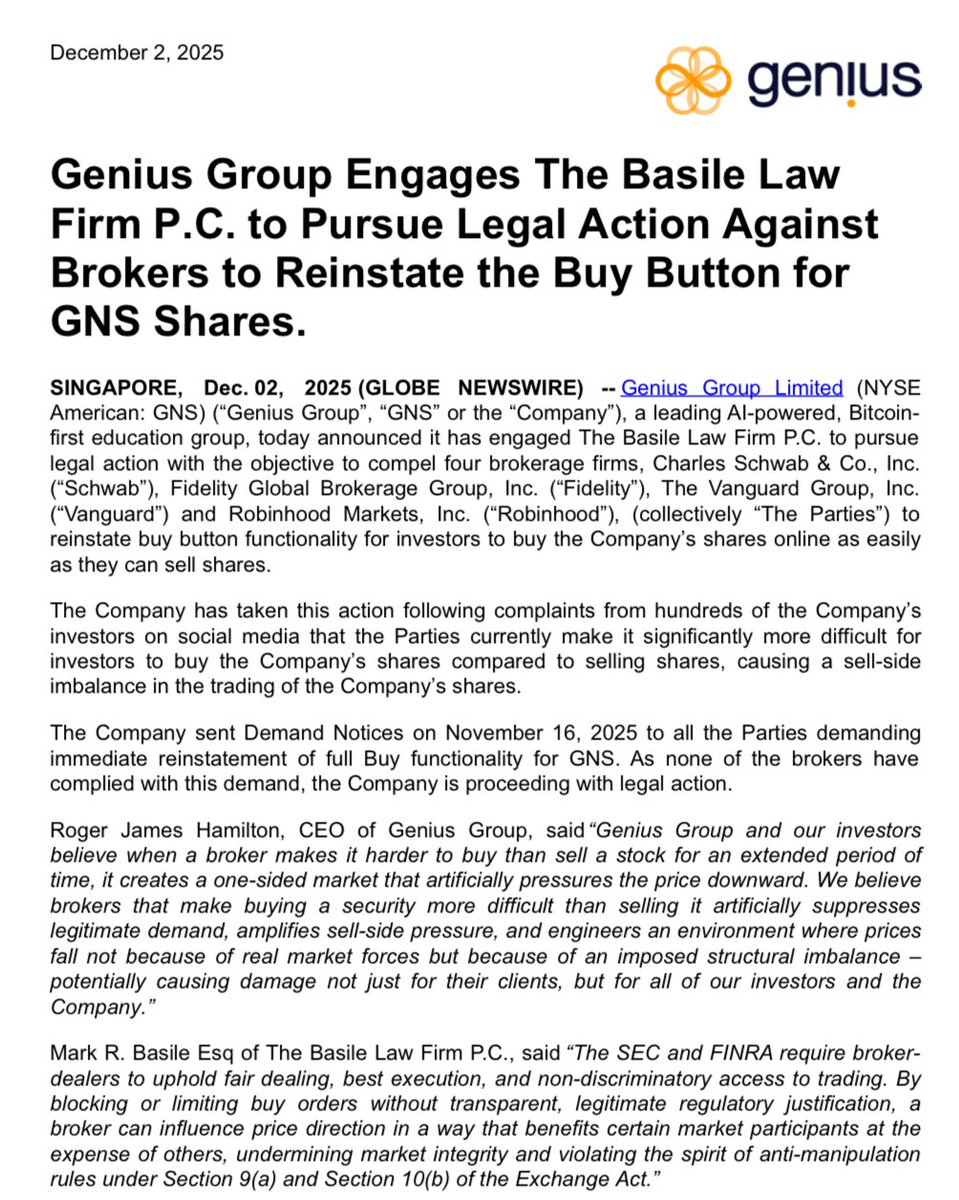

BREAKING🚨 PUBLIC COMPANY TO TAKE LEGAL ACTION AGAINST ROBINHOOD, FIDELITY, AND MORE BROKERS

- Genius Group Announced Today It Is Pursuing Legal Action Against Brokers for Removing the Buy Button $GNS

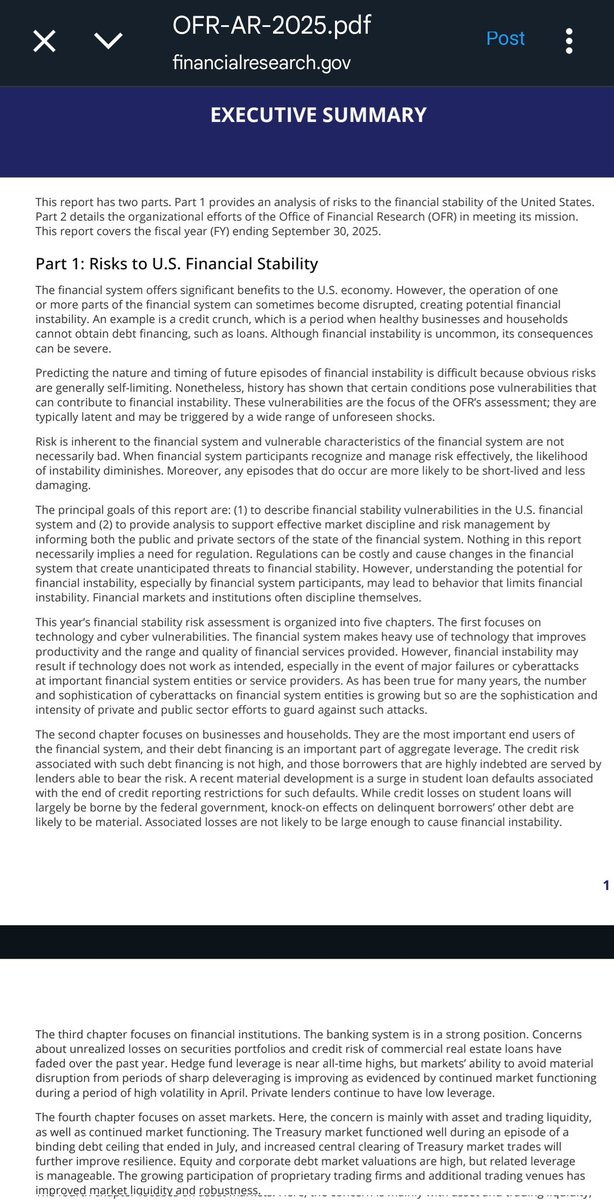

BREAKING 🚨 US OFFICE OF FINANCIAL RESEARCH SHOCKED TO LEARN OFF-EXCHANGE REPO MARKETS (DARKPOOL REPO LOANS) EXCEEDS $5 TRILLION 😱

That's over 100% MORE than expected...

The report states this could cascade into domino bankruptcies and systemic crisis.

Lehman Bros on mega steroids💥

Repo = basically short-term loans backed by bonds that can amplify systemic shocks and liquidity issues... Margin Calls ☎️ & domino bankruptcies worldwide

The total REPO market now exceeds over $12 TRILLION

Thr shadow banks $5 trillion is now 40% of the ENTIRE $12 trillion US repo market per the Federal Reserve = remember that's more than double their prior estimates

In 2008, the repo market's lack of transparency fueled uncertainty, as regulators and financial institutions underestimated risks in shadow banking sectors like mortgage backed securities

Most people fail to realize that the MBS crisis in 08 was actually due to the repo markets, EXACTLY LIKE TODAY 🌋

Janet Yellen warned us about this way back in 2021 = anyone following me on YT or Twitter for awhile has seen me sharing the video of Ole Yeller 🐶 testifying in front of Congress, stating that this is the number 1 risk to the entire global financial system...

Now we're finding out the repo market is DOUBLE what Yellen and regulators thought at the time

#2 risk, according to Yellen, is overleveraged hedge funds.

Surprise, surprise, folks

This opacity of off exchange trading could obfuscate (hide) these building pressures, allowing market stress to cascade undetected, much like how hidden subprime loan exposures (repo market derivatives) snowballed in 2008.

Recent events echo this, such as the October 2025 repo rate spikeS where banks borrowed over $15 billion from the Fed's Standing Repo Facility (SRF) in two days, signaling private market strains amid depleted reserves (down to $2.8 trillion from QT)

- Hedge funds $1.3 trillion in short Treasury positions via basis trades could unwind under rising rates, forcing Treasury fire sales and pressuring prices, akin to 2008's collateral crisis

- Global spillovers remain a HUGE threat, with non-U.S. banks relying on dollar repo funding (European and Japanese banks = 30% of liabilities) potentially transmitting stress via currency swaps

Can you say Japanese Yen Carry Trade?

Fuck... I'm tired of writing. This took about 55 minutes to write up. You get the idea.

Repost, bookmark, and follow for more if you learned something to show appreciation for my efforts.

🚫This darkpool off-exchange BS has to stop = So we've spent the last 4 years creating a stock and crypto brokerage firm and app to combat this by routing to LIT MARKETS 💡

🔥 Follow @LitXchangeApp = you can even become a Founder in the company. Link in bio. 🔥

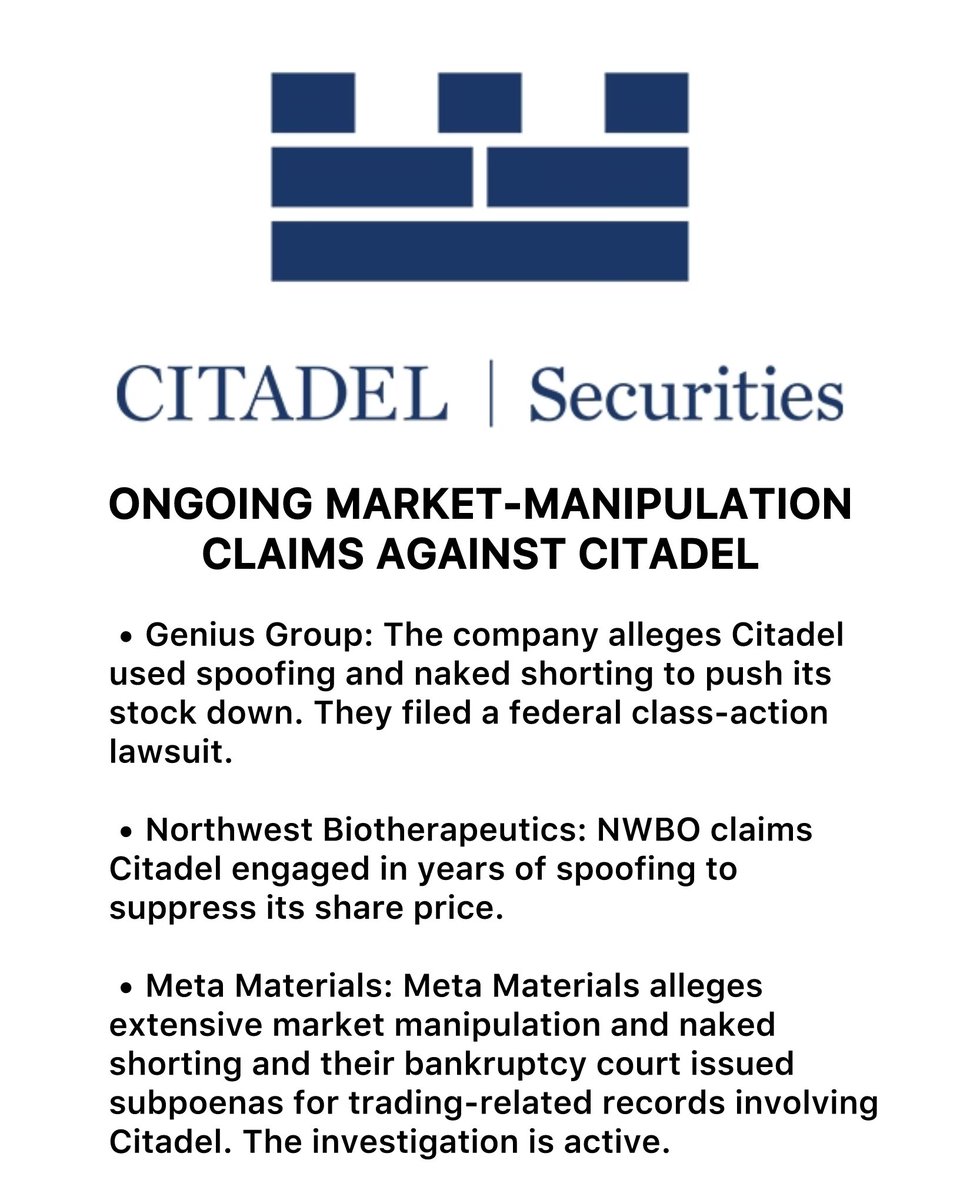

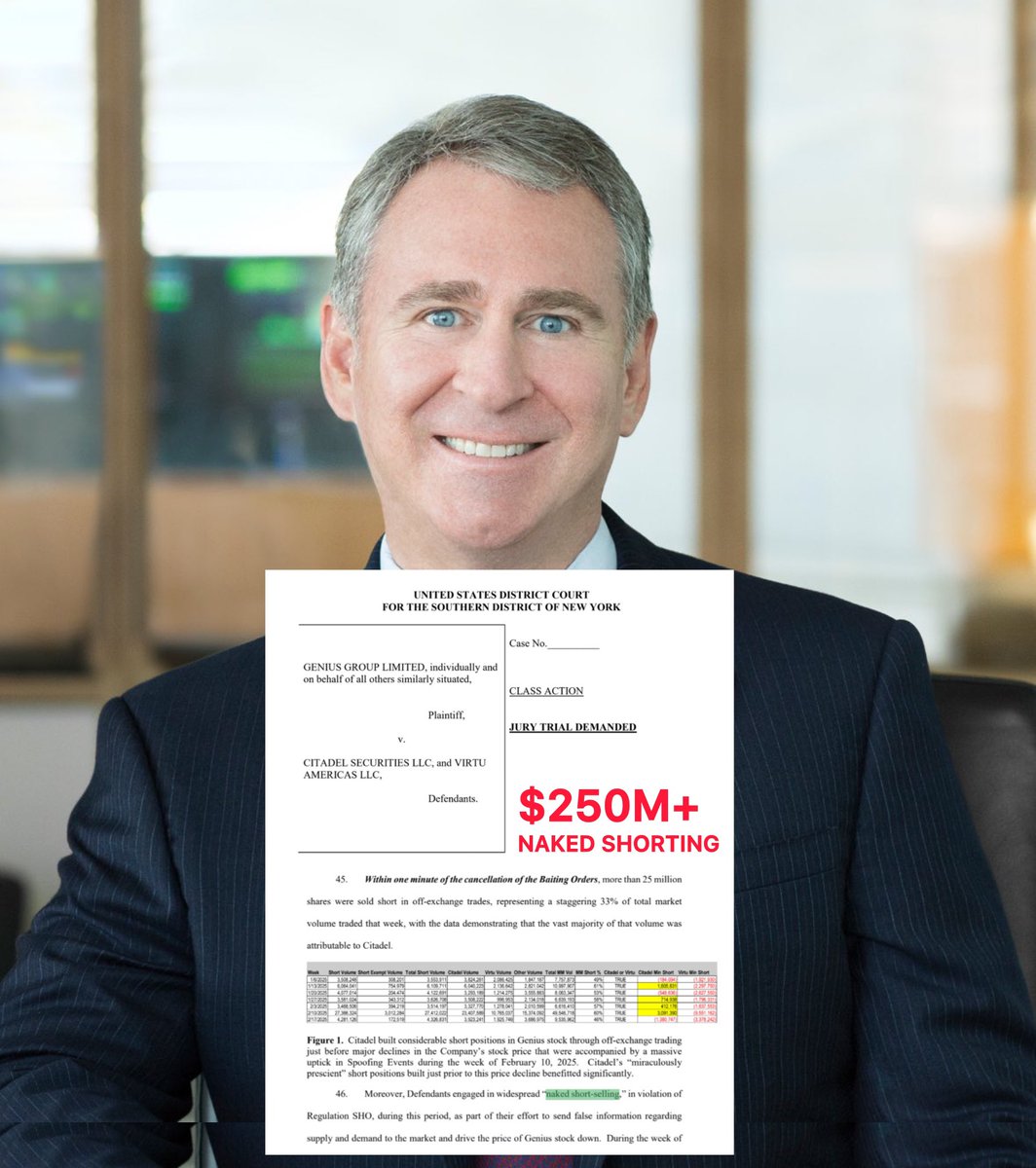

Citadel Market Manipulation 🚨🚨

- Citadel is being sued by a cancer company for spoofing $NWBO

- Citadel is being sued by an education company for Naked Shorting $GNS

- Citadel received a subpoena for manipulation from nano-tech company $MMAT

REPOST to spread the word��