@shaguncrypto Valuable investment wisdom:

-Don't put more than 2 - 3% of your total capital into any single idea - no matter how compelling it seems to be at the time or how much of a genius that you think you are.

-Don't speculate if it keeps you up at night

-Don't gamble with retirement $

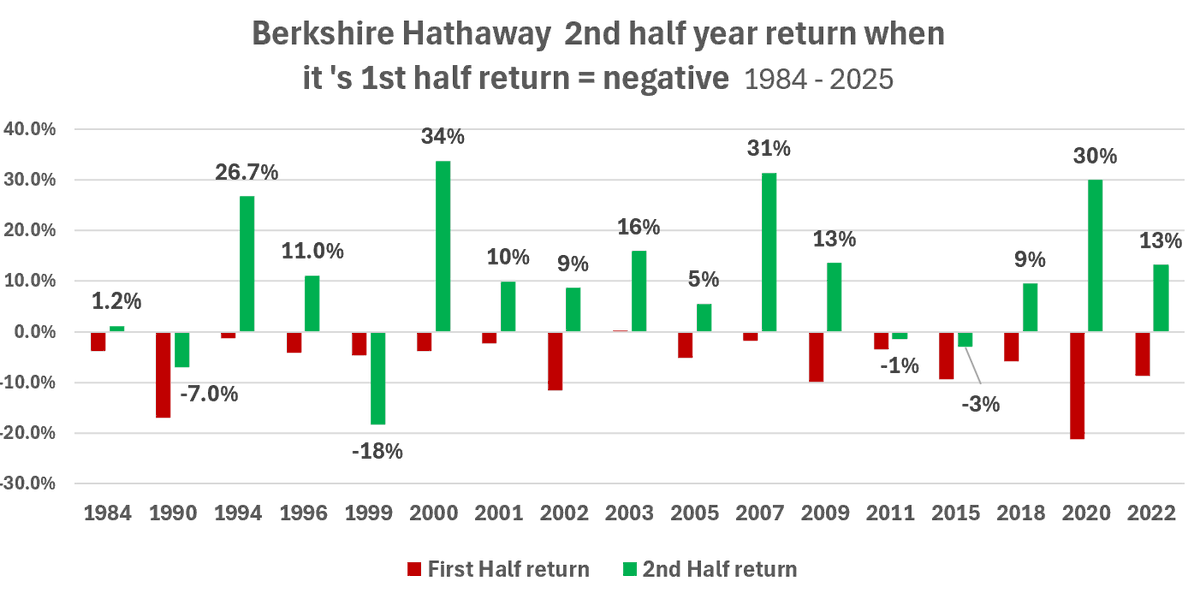

@GuyTalksFinance Since 1980, when BRK has produced a negative return in the 1st half of a year ( -2%,YTD ), the 2nd half typically returned a positive return

@JTheretohelp1 7/ So in light of the high odds of a positive market return coming up in the next 12 months and a Treasury yield spread that has been normal since Dec 2024, it's doubtful that a market top is in the cards

@JTheretohelp1 6/ FRED interest rate data even indicates a yield spread inversion as late as Feb 1930 - with the other variables aligned in July 1931 - leading to a 12 month loss of -66%.

@JTheretohelp1 5/

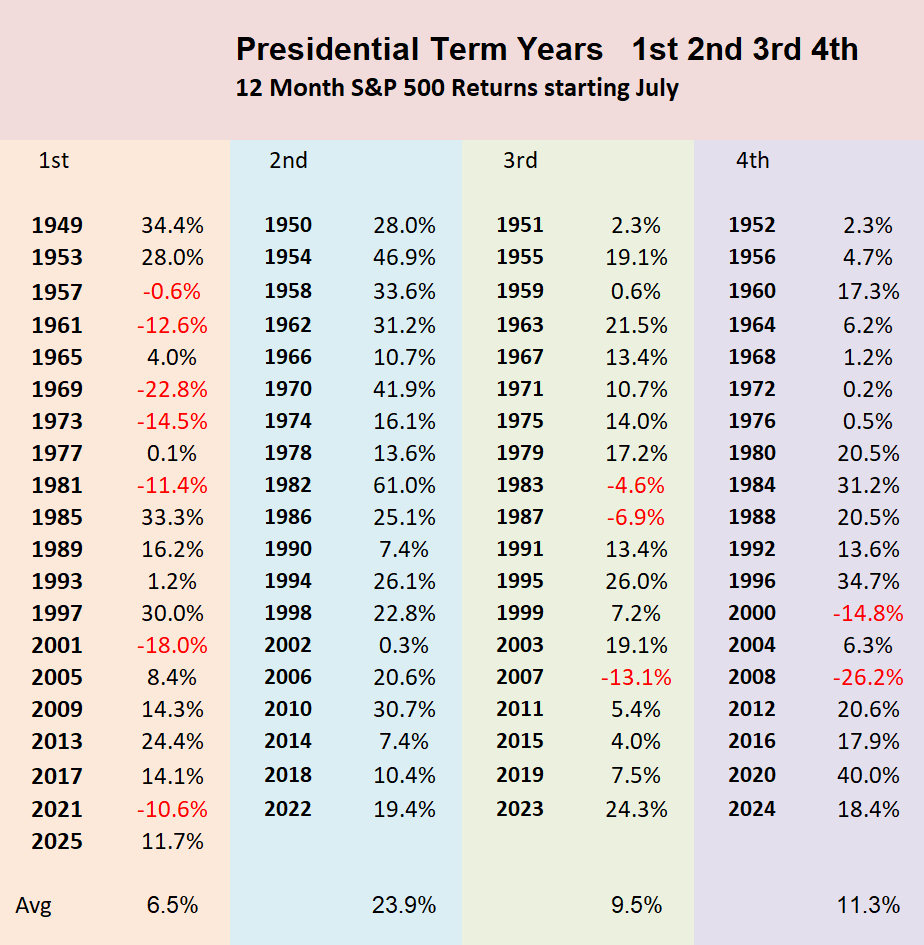

2nd or Mid term years are exempt from the process as their July - June returns ( and even forward 24 month returns ) have been predominately positive

@JTheretohelp1 4/

d) the 3 month T bill yield being higher than the 10 year Treasury note yield (yield spread inversion) within 24 month proximity to variables a, b, & c

Signaling record :

@JTheretohelp1 3/

b) the YTD S&P500 return being negative into June 30th / July 31

c) variables a & b falling within "Presidential term years" 1, 3, or 4

@JTheretohelp1 2/ Since 1950, periods of stock market risk have been identified by the alignment of 4 empirically defined variables :

a) the S&P 500 price residing below its 10 period moving average (monthly basis) value on "June 30th"or "July 31"

@awealthofcs 9/ An investor can own the small and large value stocks through low expense ETFs such as through Vanguard, Avantis, Dimensional, etc. ( with the portfolio being held most optimally in tax advantaged accounts )

Read "Stock Market Investing “Cheat Sheet”" at stockmarketmap .com

@awealthofcs 8/ Even elite money managers or hedge funds would be hard pressed to beat the S&P500 by 80%+ over 30 years - and few have endured the business for that long. Therefore, the average investor need not be a genius active portfolio manager in order to produce "genius" like returns.

@awealthofcs 7/ even rolling 20 year periods

( And it would be far easier to justify allocating to international stocks if they could demonstrate even a single 20‑year stretch of clear outperformance ! )

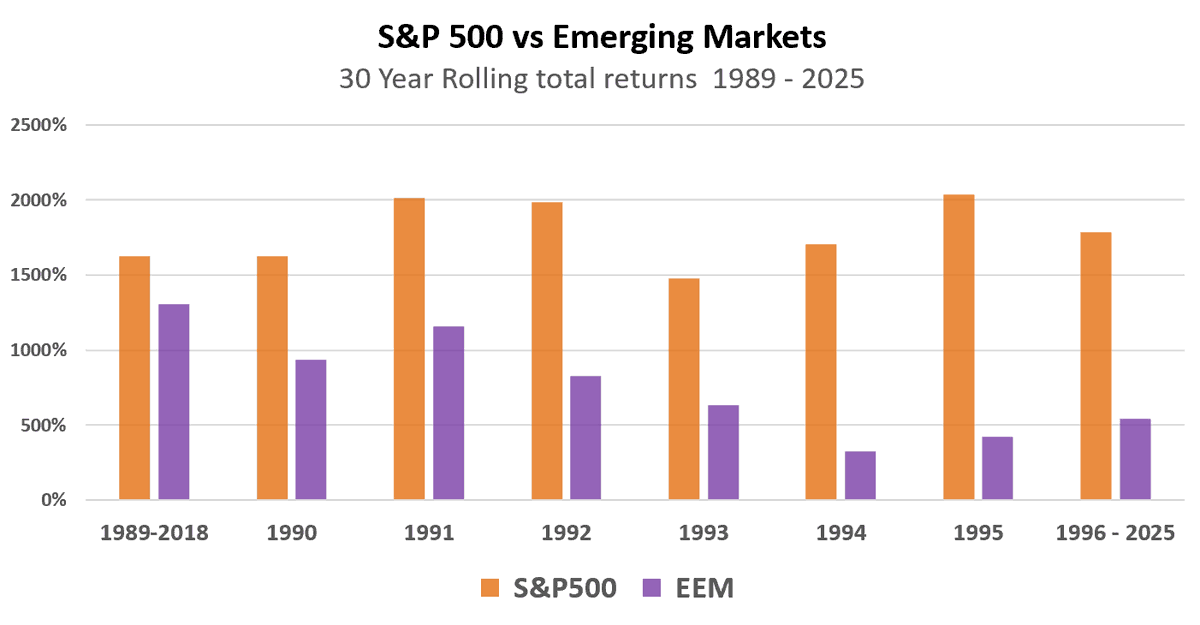

@awealthofcs 6/ Since 1980, US stocks ( S&P500 and Total US Market Index ) have handily beaten MSCI World ex US Index and emerging markets over 17 & 8 rolling 30 year periods respectively

@awealthofcs 5/ And over very short periods, other asset classes may produce periods of outperformance - such as international or emerging market stocks. Yet it has paid to not be pulled in.

@awealthofcs 4/ Then the "size, value, and quality" returns factors are added for diversification and negative covariance against the QQQs volatility ( such as during the 2000-02 & 2022 declines ).

@awealthofcs 3/ - 30+ years being a typical accumulation stage investment horizon.

This portfolio exploits the "capitalization weighting" structure of the Nasdaq100/QQQ - the same Darwinian stock selection approach that has made the S&P 500 index so so "unbeatable" over the last 60 years

@awealthofcs 2/ Since 1986, a portfolio of small & large "value" stocks and the Nasdaq100/QQQ has produced 80%+ more return, on average, versus the S&P500 and 4X the returns of the Total World Market Index, with equivalent risk, over eleven rolling 30 yr periods