$ONDS is down 40% from its January high.. which is why I'm a buyer.

Nothing has changed fundamentally. In fact, it's gotten better:

- FY26 revenue guidance: $170-$180M (up from $49M in FY25)

- Backlog grew 180% to $65M

- Q4 revenue crushed estimates by 51%

- Analyst price targets at $19-$25.

The weekly chart still shows higher lows since March 2025. Ascending trendline intact. This pullback is a gift.

40% pullbacks in an uptrend are where positions are built, not sold

$USAR is building the first fully domestic rare earth mine-to-magnet supply chain in the U.S. Now down 58% from its highs, it's looking like an attractive dip buy👀

→ Stillwater magnet facility coming online H1 2026

→ Round Top deposit in Texas has the richest known source of gallium & beryllium in the U.S.

→ Dept. of Commerce took an equity stake

→ Trump's $12B Project Vault minerals stockpile directly benefits USA Rare Earth

→ G7 meeting to reduce rare earth dependence from China

→ Acquired Less Common Metals, expanding supply chain globally

→ Long-term target of $2.6B revenue, $1.2B EBITDA by 2030

→ Stock up 50% YTD after securing government collaboration agreement

China controls 90%+ of rare earth magnet production. The US government wants to reduce that number, and USAR is one of the companies they're backing to fix it. However, there are risks:

⚠️ Pre-revenue ($0 in sales, net loss of $156M last quarter)

⚠️ < 50 employees building a $3.9B market cap company

⚠️ Stillwater still needs to prove it can operate at scale profitably

⚠️ Round Top won't be self-sourcing until 2028

⚠️ Earnings Feb 25 could be volatile

Falling wedge on the daily chart, volume shelf support at $17, and sitting on previous resistance.

If America wants true rare earth independence, USAR has to deliver. Are you buying the dip?

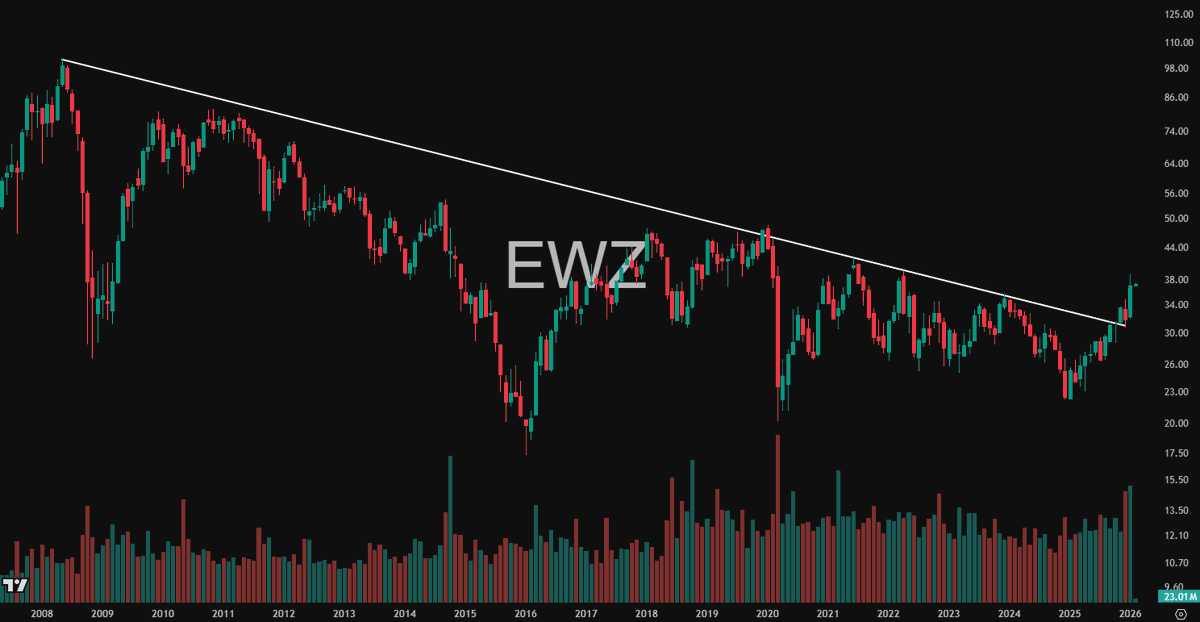

Is Brazil breaking out? 👀

An 18 year downtrend was just broken on the $EWZ iShares Brazil ETF.

Shoutout to @Geiger_Capital for the call, the chart looks beautiful.

$CIFR pulling back to support after a 750%+ run from $1.86.

Bitcoin miner → AI data center pivot:

- $8.5B in AWS + Google contracts

- $870M projected revenue

- Morgan Stanley PT: $38

Earnings Feb 24. Are we heading back to all time highs?

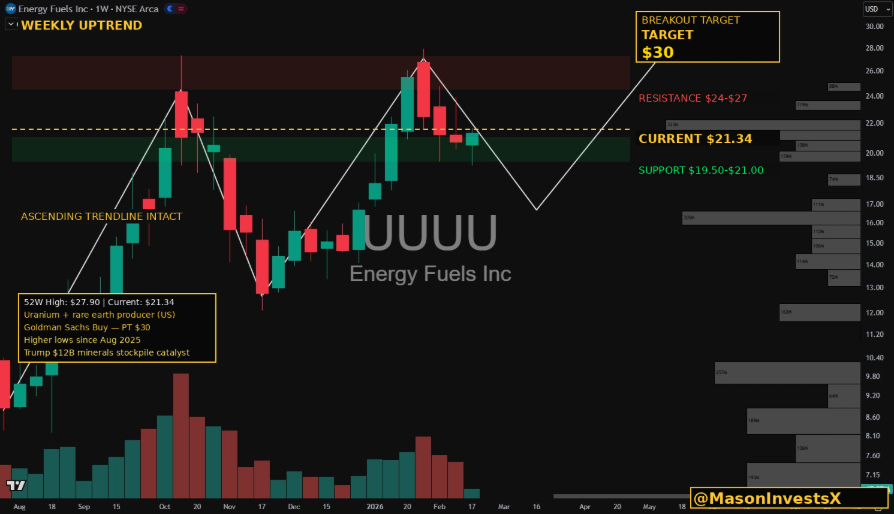

$UUUU is the only US company producing both uranium AND rare earths. Goldman initiated with a Buy and a $30 price target. The bull case is hard to ignore:

✔️ Leading US uranium producer with 1M+ lbs. produced in 2025, beat guidance by 11%

✔️ Rare earth expansion at White Mesa

✔️GM, DOE, and the Trump admin's $12B minerals stockpile all point the same direction

✔️ Revenue up 104% YoY → $298M working capital, fully funded

China controls 90%+ of rare earth refining. The U.S. government has decided that changes, and Energy Fuels is the vehicle. But there are risks:

⚠️ Stock is up over 500% from its 52W low of $3.20, good news may be priced in

⚠️ Still unprofitable on a GAAP basis (P/E: -42x)

⚠️ Rare earth expansion won't be fully ramped up until 2029

If the US is serious about critical mineral independence, UUUU is the most direct play. But size accordingly, this is a bet on execution over the next 3 years.

Earnings Feb 27 is the next catalyst. Which comes first, drop to $16 or straight to $30?

$LAC is sitting on the largest lithium deposit in North America. The U.S. government took an equity stake. Few are paying attention.

Here's what's happening at Thacker Pass:

→ Largest measured lithium resource in North America

→ $2.26B DoE loan secured

→ GM owns 38% of the project ($625M invested)

→ US DOE took a 5% equity stake (first time ever for a lithium m

→ 40,000 tonnes/year of battery-grade lithium carbonate at full capacity

→ Enough to supply batteries for ~1 million EVs per year

China controls 70% of global lithium refining. The US government decided that's a national security problem and put its money directly into this project.

This is a pre-revenue, construction-stage play. High risk, but the backing speaks for itself: DOE, GM, Orion, Bechtel.

When the US government invests, take notice.

$ONDS is down 40% from its January high.. which is why I'm a buyer.

Nothing has changed fundamentally. In fact, it's gotten better:

- FY26 revenue guidance: $170-$180M (up from $49M in FY25)

- Backlog grew 180% to $65M

- Q4 revenue crushed estimates by 51%

- Analyst price targets at $19-$25.

The weekly chart still shows higher lows since March 2025. Ascending trendline intact. This pullback is a gift.

40% pullbacks in an uptrend are where positions are built, not sold

$CMCL is a gold miner trading at 10x earnings while gold sits near all-time highs.

Gold is above $5,000/oz for the first time in history.

JP Morgan targets $6,300 by year-end. Deutsche Bank says $6,000. Central banks are buying at record pace.

Caledonia Mining is down 23% sitting in an obvious weekly uptrend.

→ P/E ratio: 10.9x (most gold miners trade 15-25x)

→ Dividend yield: 2%

→ FY25 production: 76,213 oz (met guidance)

→ Blanket Mine cash flowing, fully operational

→ Bilboes gold project funded. $150M convertible notes closed, gold hedged at $3,500/oz floor

→ Director recently bought shares at $29.78.

Cash flow, a dividend, and a massive growth project about to come online. The Bilboes project alone could transform this company, funded at a gold hedge floor of $3,500 while spot is $5,000+.

Gold is in a structural bull market. Is this the cheapest way to play it?

$ENPH Weekly downtrend broken✅

Strong Q4 earnings reaction sent Enphase Energy over its lower high of $40. Low volume retest last week with a big volume shelf support level below.

Do we see $60 in the next few months?