🚨ADDRESS UPDATE!!!🚨

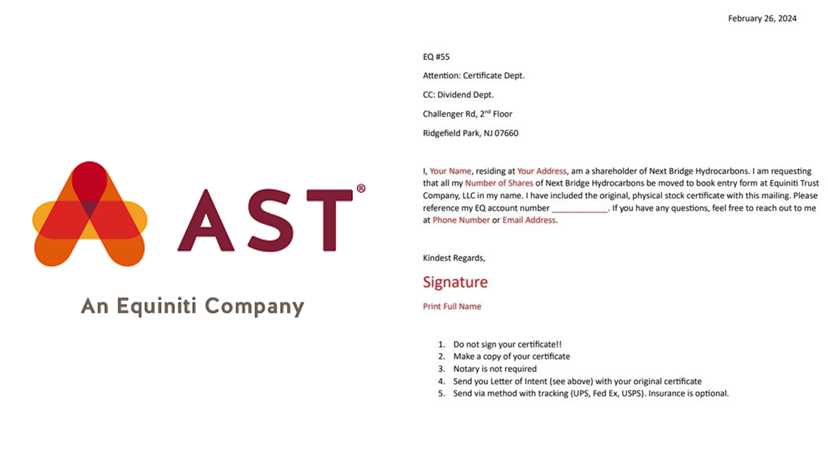

💥AST/EQ PROVIDES INSTRUCTIONS & TEMPLATE FOR REGISTERING CERTIFICATED SHARES IN BOOK ENTRY IN YOUR NAME.If you have requested a transfer of your NEXT BRIDGE HYDROCARBONS (formerly MMTLP) shares to AST/EQ (transfer agent), and your broker has mailed you paper certificates, use the template below to have your certificates registered in book entry in your name. Questions: 800-937-5449.

EQUINITI

Attn: Automated Scanning Team

1110 Centre Point Curve

Mendota Heights, MN 55120

MMTLP MMAT TRCH NBH

💥AST/EQ PROVIDES INSTRUCTIONS & TEMPLATE FOR REGISTERING CERTIFICATED SHARES IN BOOK ENTRY IN YOUR NAME.

If you have requested a transfer of your $MMTLP/#NBH shares to AST/EQ (transfer agent), and your broker has mailed you paper certificates, use the template below to have your certificates registered in book entry in your name. Questions: 800-937-5449.

$MMTLP $MMAT $TRCH #MMTLPArmy #MMTLPFiasco @AST_Financial@equiniti@nbhydrocarbons@Maxfanatic90 Thx for the doc!!!

🚨 NEW SEC FOIA RESPONSE 🚨

FOIA 26-00651-FOIA

This one matters.

This FOIA requested records showing communications/referrals between SEC Corporation Finance and SEC Trading & Markets regarding Next Bridge Hydrocarbons’ S-1 activity.

The response shows something important:

Once FIF entered the discussion, the tone and substance appear to shift.

Before FIF:

SEC / NBH S-1 communications were largely about registration mechanics, eligibility, disclosure, and process.

After FIF steps in:

The discussion turns to operational market-structure concerns:

• shares on loan

• lending broker-dealers unable to recover shares

• customer protections under SEC Rule 15c3-3

• IRA/tax consequences

• transfer-agent capacity

• whether shareholders should be forced out of bank/broker/nominee holding

One FIF point is especially hard to ignore:

“Because of the prior FINRA trading halt, there are shares on loan that lending broker-dealers cannot recover.”

That is not retail speculation.

That is an industry group raising operational concerns to the SEC about the Next Bridge S-1 process.

And FIF’s recommendation?

Do not force participating customers out of bank, broker-dealer, or nominee custody — because preserving that structure would allow for “future reconciliation of outstanding stock loans.”

Read that again.

Future reconciliation of outstanding stock loans.

This FOIA does not prove every theory.

But it does prove the S-1 issue was not just routine paperwork.

It involved broker-held shares, loaned shares, customer protections, transfer mechanics, and reconciliation concerns.

That is exactly why MMTLP shareholders have been asking questions for years.

#MMTLP #MMAT #NextBridge #FOIA #SEC #FINRA

🛎️🛎️🛎️

REMINDER:

FIF sought help from @SECgov executives to interfere in NBH corporate action set to expose their members' short gambit and the truth behind FINRA's U3 halt of MMTLP...

FULL FOIA BREAKDOWN: https://t.co/1jTqZW1YTP

Now, get a peek inside SEC communications with @nbhydrocarbons while they were conspiring with FIF...

👇👇👇

🦋 MMAT | Meta Materials Inc.

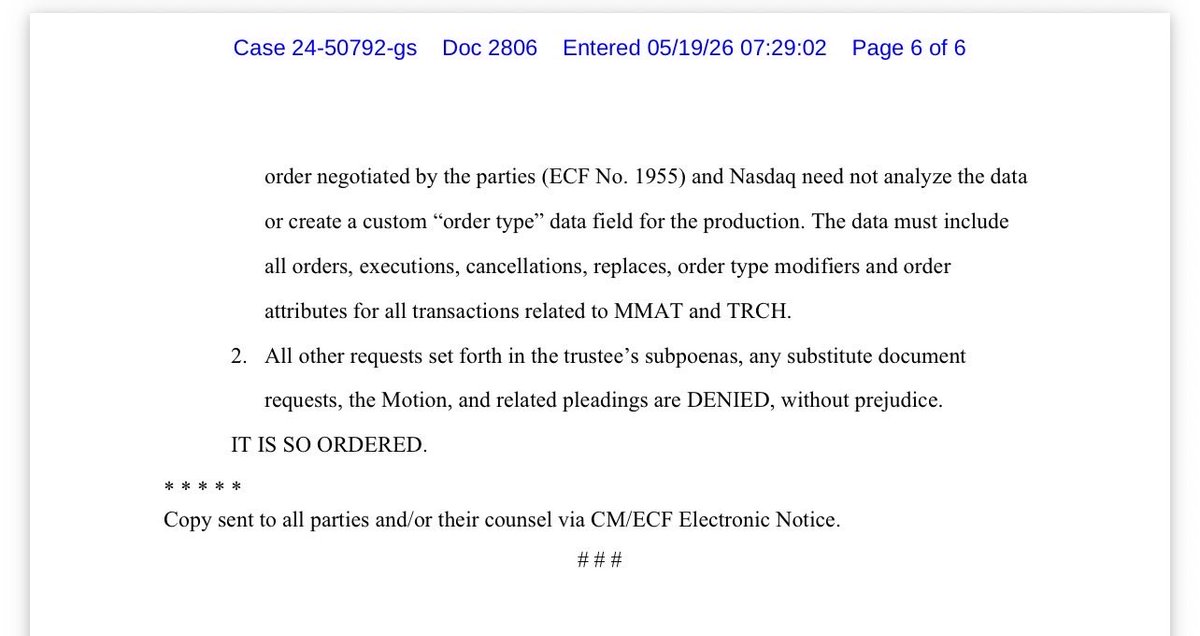

Case No. 24-50792-gs (Chapter 7)

📅 Filed: June 3, 2026

📄 Docket No. 2833 – Ex Parte Application to Set Status Hearing

⚖️ Layman’s Summary

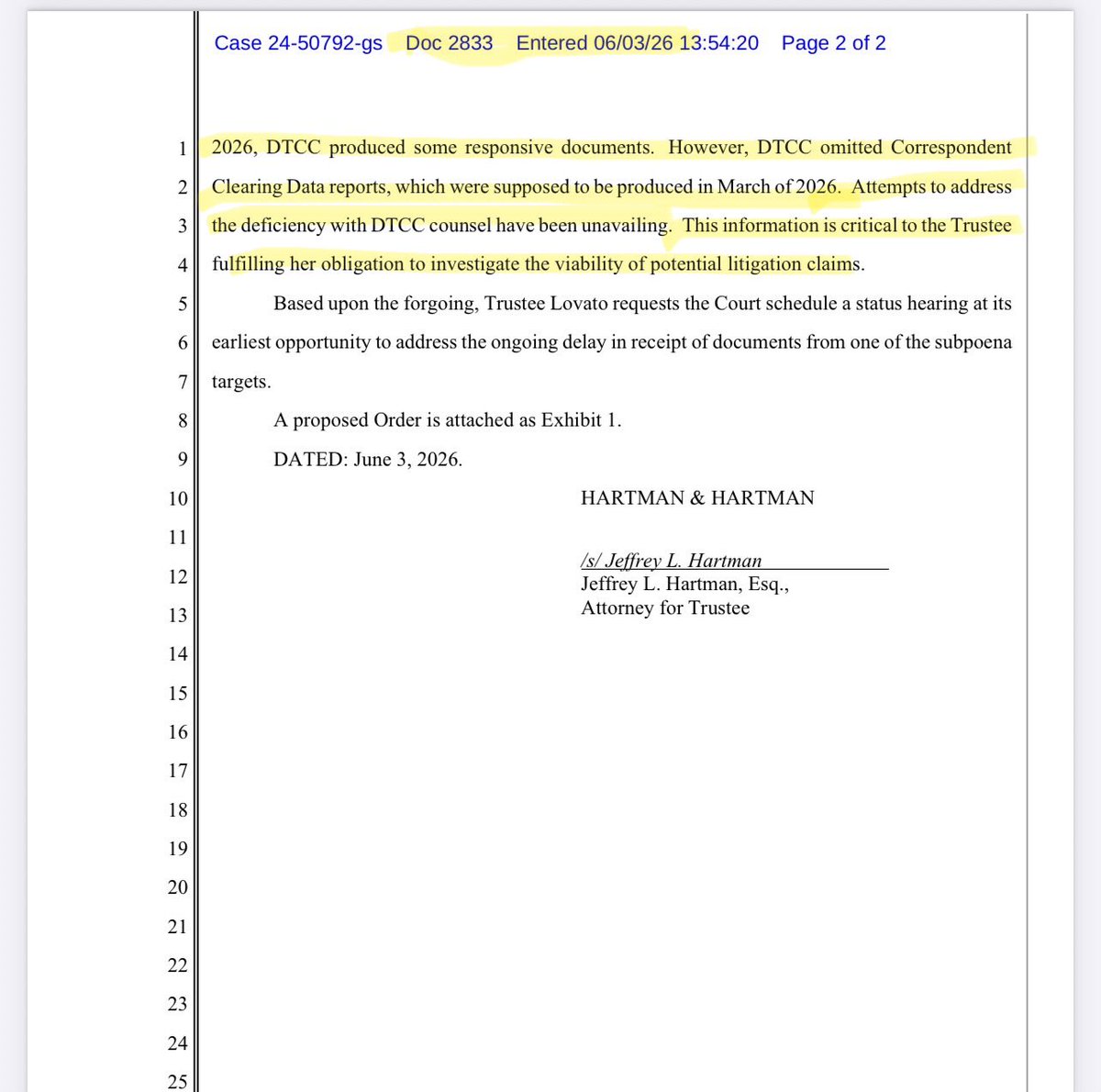

Trustee Christina Lovato is asking Judge Spraker to schedule a status hearing because DTCC has allegedly not provided all of the subpoenaed records the Trustee believes were due months ago.

🔥 Key Quote

“DTCC omitted Correspondent Clearing Data reports, which were supposed to be produced in March of 2026.”

🚨 Why It Matters

The Trustee tells the Court:

“This information is critical to the Trustee fulfilling her obligation to investigate the viability of potential litigation claims.”

In plain English:

👉 The Trustee believes important DTCC data is still missing.

👉 Efforts to resolve the issue privately have failed.

👉 The missing information is important to determining whether litigation claims exist.

👉 The Trustee wants the Court involved to move the process forward.

📌 Bottom Line

This filing suggests the MMAT investigation is still active, the Trustee is still seeking additional DTCC records, and she believes those records are important to evaluating potential legal claims.

⚠️ Not Legal Advice.

🤔 With the Trustee now requesting a status hearing regarding the missing DTCC data, I wonder if Judge Spraker will add the issue to the June 16 hearing that’s already scheduled. Will the DTCC matter be addressed then, or will the Court set a separate hearing date?

That’s not what this is about. Let’s face some real life facts at this moment from a business perspective. Since 2014 this company has attempted to raise $$ to become a real exploration company and every-time they have been shorted to hell and back. This S1 will allow NBH to raise a sufficient amount of capital to fund itself for all the bullshit litigation and to actually pursue real life O&G deals that will make $$$ for stockholders. Anyone that wants to dispute this is welcome to respond. I’ve been here since Greg McCabe got involved and that is all we have tried to do since then. Had we have known that we would have to face this headwind we would have chosen a much easier path. Everyone has choices and they are not always the easiest path. We will win despite these obstacles because losing is not an OPTION ever!!! It just isn’t!!!! Not for me and not for Greg. If he hasn’t proven his tenacity by now then you haven’t been paying attention. He is the guy you want running your retirement plan!! So get on board or get on with your life it isn’t always immediately profitable. I have many investments that have taken many years to develop. You got into this for the same reason you still want it to be. Hang in there!!!

Next Bridge Hydrocarbons Announces SEC Declares Effective its S-1 Registration Statement

Company prices and commences a public offering of 40 million shares

https://t.co/2hO7KuPeJJ

🚨NEXT BRIDGE HYDROCARBONS RELEASES PR ANNOUNCING THE EFFECTIVENESS AND AVAILABILITY OF UP TO 40 MILLIONS SHARES OF NBH COMMON SHARES @ $15/SH.

MMTLP MMAT TRCH NBH

@nbhydrocarbons

https://t.co/df52HGhBtS

💥💥May 27, 2026 marked a

LANDMARK PROCEDURAL VICTORY!

🦋⚖️ $MMAT / TRCH / MMTLP

In re Meta Materials Inc. Chapter 7 Bankruptcy — Case No. 24-50792

On March 6, 2025, the Trustee served nine subpoenas seeking trading and market data from:

📌 Charles Schwab

📌 TD Ameritrade

📌 TradeStation

📌 DTCC

📌 Nasdaq

📌 FINRA

📌 Citadel Securities

📌 Virtu Financial

📌 Anson Funds

⚡ All parties are now complying or moving toward EXPEDITED compliance under individualized protective orders governing sensitive trading data and confidential information.

📆 Upcoming calendar of events shown in the graphic below.

📚 This case is becoming a significant example of a Chapter 7 Trustee strategically leveraging the Bankruptcy Code’s powerful discovery and investigatory tools to pursue potential estate claims and maximize value for creditors.

⚠️ Not Legal Advice

Detailed infographic below and song attached.

https://t.co/HE77dAvkwO

#MMTLP

So Finra reaches out to me about my dispute about Robinhood illegally selling 1500 of my shares in a margin call with no prior notice

She claims to have sent me an email which I never received giving me a deadline for the case

I responded, lets see what happens

will update

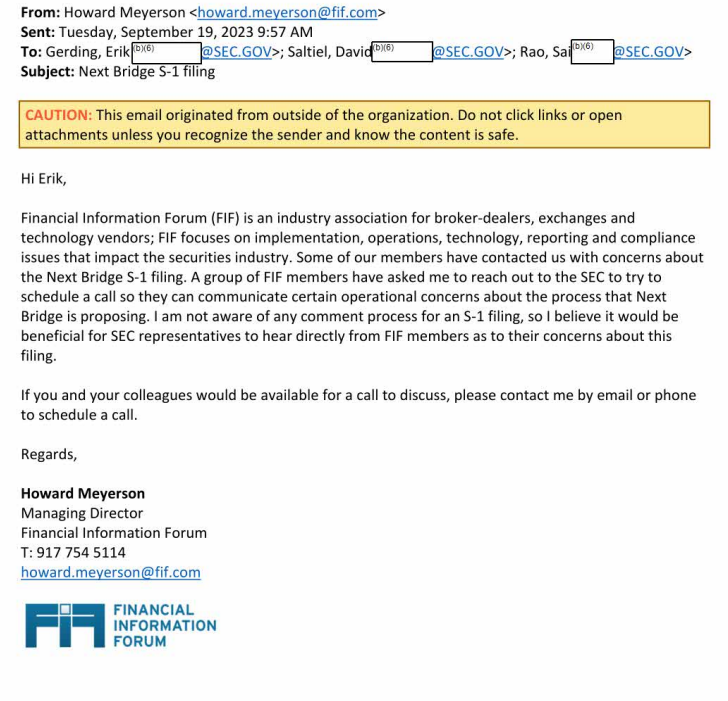

$MMTLP Financial Information Forum (FIF) and Securities and Exchange Commission FOIA.

Pg 1 - Howard Meyerson, FIF Managing Director, emails Erik Gerding, SEC Director of Division of Corporate Finance, David Saltiel, SEC Director of Trading & Markets, and Sai Rao, General Counsel for Division of Trading & Markets.

A lot of people in the $MMTLP community are talking past each other — arguing trading vs. settlement, S-1 delays vs. FOIA, brokers vs. regulators — without stepping back and looking at how all the pieces actually fit together.

Here’s the full picture, without spin.

The problem was never just that trading was halted. The real damage happened because the halt stopped the normal enforcement mechanism of the market. In a functioning market, if someone sells shares they can’t deliver, they’re forced to buy them back at whatever the market price is. That’s how fairness and price discovery are supposed to work.

But in this case, the halt happened before enforcement could occur. Orders — including very high sell orders — were canceled. Shorts were not forced to close. Settlement froze mid-stream.

What makes this worse is what happened next.

FOIA records later show regulators — including @FINRA@SECGov — were explicitly told there were unrecoverable shares caused by the halt, while regulators were also privately engaging broker representatives about settlement mechanics. That’s the turning point.

Up until that moment, delays — including delays in NBH’s S-1 — could reasonably be framed as routine regulatory process. After that knowledge existed, delay stopped being neutral. It preserved a known market failure, protected existing exposure, and left investors trapped with no exit and no timeline.

@nbhydrocarbons has been doing what it’s been asked to do to move the S-1 forward. Yet the prolonged delay has caused real harm — to the company’s future plans, its ability to operate normally, and to investors stuck in limbo. Once regulators know a market is broken, continued delay is no longer just process. It becomes a decision with consequences.

This is where the argument to “just give us the two days back” runs into reality.

In theory, yes — those who couldn’t locate shares should have been forced to pay market price. That rule only works if the market is allowed to function. Once settlement was interrupted and unrecoverable shares were acknowledged, reopening trading later doesn’t guarantee fairness. It risks chaos, uneven outcomes, and more people left unpaid — effectively creating a second failure on top of the first.

That’s why settlement enters the picture.

A real settlement would not be NBH paying investors. It would involve brokers with unresolved exposure, clearing intermediaries, insurers, and independent oversight. The funds would come from institutions that benefited from or participated in the broken settlement chain — not from NBH’s assets or future share issuance.

This is where the proposed ~40M share S-1 offering often gets misunderstood. That offering is about NBH’s future — capital formation and viability going forward. It does not fix past settlement failures, close historic short obligations, or make investors whole. Using new issuance to cover old failures would simply shift liability onto the company and dilute legitimate shareholders.

Yes, settlement protects brokers from unlimited worst-case exposure. That’s true. But once enforcement failed at the moment it mattered, settlement also becomes the only way investors get certainty, equality, and actual payment. Trading no longer guarantees justice — it just creates more risk.

The canceled high-price sell orders still matter. Not because they can execute now, but because they prove lost price discovery and real harm. They show what the market was trying to do before it was stopped. In settlement terms, they become evidence of damages.

Another area where people talk past each other is direct registration vs. broker-held shares. Direct registration at AST does not create the problem, and broker-held positions do not make investors less legitimate. Direct registration removes intermediaries and clarifies ownership; broker custody adds layers and lending complexity — but both represent valid shareholder interests. No resolution should penalize investors for custody choices they didn’t control.

The FOIA matters here because it shows brokers were concerned that forced direct registration would immediately expose unrecoverable shares. That concern isn’t about investor preference — it’s about settlement reality. Regardless of where shares were held, the obligation to deliver never disappeared.

There’s also an earlier issue that can’t be ignored.

Serious concerns have long been raised that MMTLP may have been improperly or fraudulently listed, and that those concerns were flagged while trading was ongoing. Despite this, there was no public investigation announced, no transparent disclosure to investors, and no clear Reg SHO-style reporting that would normally accompany suspected settlement or fraud issues.

That alone doesn’t prove conclusions — but combined with the halt, the later acknowledgment of unrecoverable shares, and the lack of remediation afterward, it raises a critical question: what did regulators know about the listing itself, and why were investors never informed or protected in real time?

This unresolved question further explains why reopening trading is so risky and why resolution outside the market becomes more likely.

So where does this leave FINRA?

FINRA is unlikely to be writing checks or admitting wrongdoing — its regulatory immunity largely protects it from direct monetary liability. But immunity does not mean insulation from scrutiny, explanation, or consequence. The FOIA record undermines any claim that this was purely routine or resolved. It establishes knowledge, post-halt involvement, and continued inaction after awareness.

That places FINRA in a defensive institutional position. Not necessarily criminal by default — but exposed to oversight, discovery, reputational damage, and hard questions about process failure. In situations like this, settlement actually helps FINRA by closing the harm, stopping compounding exposure, and resolving the market failure without reopening a broken system.

If regulators decide settlement is the path forward to limit further exposure, timelines usually compress rather than stretch. Typically, there’s quiet containment and modeling first, then a settlement framework, followed by public disclosure and oversight, then claims and initial payments — often once the process formally begins.

One final point matters more than most people realize: time is no longer neutral. Once a market failure is known, delay doesn’t reduce risk — it compounds it. Records age, inconsistencies grow, and harm continues. Settlement doesn’t require admissions or end oversight; it simply closes the damage while investigations and reforms proceed separately.

That’s why this doesn’t end because pressure fades.

It ends when the cost of doing nothing exceeds the cost of resolution.

Settlement isn’t perfect. It doesn’t recreate what might have happened.

But after the halt, it’s the only option that doesn’t rely on a broken system, doesn’t dump liability on NBH, doesn’t pit shareholders against each other, and doesn’t leave investors waiting forever.

That’s the uncomfortable truth — and the clearest path forward.

The Meta Materials Bankruptcy is a game changer. We don’t know how to fix this is no longer an option and now someone else is deciding for you. You lost your opportunity. The attorneys associated with the case have been involved for a year. They’ve already seen what’s coming in through protective orders. They see the BASELINE harm ($1.3 BILLION). Would they have taken this case on contingency without litigation funding if the preview wasn’t weighted in their favor? The Court case will continue… even if victims die. Our heirs will benefit. In my opinion - they calculated that everyone is as corrupt and greedy as they are… and they were wrong. 9 subpoenas started opening the doors… information is being triangulated. Motions to quash are being denied. Statute of limitations runs in August. Tick tock.

I have not changed my opinion. I would want to start with a share count of ALL shares, IOUs, swaps, synthetics, overseas shares, etc. Drew is making his points, IMO, based on the ability to trade on block chain and force a reconciliation using that methodology. BUT, until someone can prove to me that all shares would ultimately will be accounted for and no BS can happen by using blockchain (see @palikaras long post on that) I am sticking with my opinion. And Drew is entitled to his. What has been proposed recently in the press by exchanges and DTCC does not give me solace that those who wish to usurp the law or play in the gray area will suddenly find Jesus.

MMTLP #FOIAfiasco#FOIAdenials

Just received the latest FOIA data update from our in‑house analyst, Mike - and the numbers are staggering.

During this refresh, the SEC appears to have backfilled more than 5,300 new entries that were not previously present in the database. The total volume jumped by over 6,000 new records, even though April itself only accounts for 652 new FOIA submissions.

Another area of concern, FOIAs Granted in Full or Denied in Part. SEC All: 14.66% MMTLP: 0.766%

Below are the updated charts reflecting the dataset as of 5/19/2026, compared to the prior snapshot from 4/13/2026.

Is the shell game being exposed? @VP@timburchett@Notarighty12@bleedblue18@busybrands

I know that @Maximus711474 actually reads documents.

For those who do not, their dangerous and misleading commentary about the order is another signal of their ignorance and/or desperation to protect their patrons, while running their influencer/faked-shareholders-for-hire little business they are running for professional ambulance chasers.

For the record:

1. The Court did NOT say MMTLP is “irrelevant”. In fact, the order references MMTLP multiple times.

2. The Court DID authorize BROAD production of #MMAT/TRCH trading data, including:

-all orders

-executions

-cancellations

-replaces

-order attributes

-RASH/CORE data

across nearly FOUR YEARS which is extraordinary…

Did you know?

NASDAQ did NOT trade #MMTLP (which traded on the OTC), hence they do NOT have ANY MMTLP data to produce… you weird geniuses you! 🤣

3. The Court explicitly REJECTED Nasdaq’s “undue burden” argument and reaffirmed the Trustee’s broad Rule 2004 investigatory powers regarding potential wrongdoing.😎

4. Saying “everything else was quashed” is simply false. Nasdaq LOST the motion to quash in all MATERIAL respects related to the CORE trading data they control! 🦋

And finally, the Trustee is an independent fiduciary appointed by the Court. If the investigation had no merit, the subpoenas would NOT keep surviving judicial scrutiny.

🧐 speculation and opinions have exactly ZERO evidentiary value in court.

Actual court orders do.

🚨Breaking news: 🦋

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.