Return expectations of many first-time investors who entered after COVID were shaped by an extraordinary bull market. They saw stocks surge, SIPs perform well, and even moved money from FDs to equities expecting 20–25% annual returns.

But markets move in cycles. Just as there can be 2 great years, there can also be 2 difficult years.

New investors are understandably worried today. Seasoned investors know volatility is part of the journey. Staying invested through cycles has historically been the key to generating 12–15% long-term returns.

A Middle Class Tax Paying Citizen visits a local Honda Showroom to Buy a 110 CC Honda Activa Standard Model. Their First Vehicle.

He has already paid proper Income Tax and only then gets Salary.

He gets a quotation of ₹97456 + extra for Accessories.

He asks for Breakup.

He sees that the Basic Price of the Vehicle is only ₹66337.

GST (18%) comes to ₹11940 (9% to State & 9% to Central)

Then Road Tax + Registration + Smart Card etc comes to ₹13279.

Insurance is ₹5000 + ₹900 GST.

So basically he pays ₹66337 to Honda & ₹26089 in the form of GST & Road Tax & other charges.

For accessories, he has to pay additionally ₹4000 to ₹5000 which also includes GST.

He closes his eyes and imagines the Road on which they will be riding in the Monsoon which will come now. He imagines riding on the roads filled with water logging. He knows that the roads are not upto the mark. He wishes his Road Tax was fully utilized on High Quality Pothole Free Roads.

He feels bad for paying Road Tax for Roads which have potholes in the city. He knows that his Health will go down. But he has no choice. He cannot take a Car because he would be stuck for hours in a jam.

He feels that he has paid Income Tax, but has to pay 18% GST for a basic 2 wheeler. He has to pay 18% GST on Vehicle Insurance. On Accessories.

Then he looks at his family. He sees the joy on their faces as they purchase their first vehicle. He takes his phone out.

He makes the payment using Digital India UPI & takes the vehicle home !!! His family is happy. He goes to work next day.

Story of Middle Class.

#FI

The Indian public agrees on almost every common issue privately.

Everyone knows

- traffic is bad

- pollution is bad

- corruption is bad

- Life is getting expensive.

But the moment these issues become political, people get divided into parties and ideologies instead of standing together as citizens.

And once that happens, the common issue slowly disappears behind political fights.

PART 1: The Journey So Far

1 USD = ₹60

Elect us. We will bring it down to ₹40.

₹70 :-Working on it. These things take time.

₹80 :- We need to undo 60 years of damage first.

₹90:- Weak rupee is actually good for exports.

₹95:- Why does it even matter? Economy is still growing.

PART 2: Future Course of Action

₹100:- Don’t compare with the dollar. Compare with weaker countries.

₹105:- Every global currency is suffering. This is normal.

₹110:- India is becoming a superpower. Stop negativity.

₹120:- Rupee is not falling, it is finding its real value.

₹130:- Please use UPI. Don’t think in dollars.

₹150:- New education policy will remove colonial mindset about USD.

Indian governance today:

If something improves : Masterstroke leadership.

If something fails : 60 years of damage.

If citizens complain : Anti-national mindset.

If media questions : Foreign-funded agenda.

If data looks bad : Western propaganda.

If youth leave the country : They were never patriotic anyway.

And if nothing works : Change the topic to nationalism before people ask real questions.

When it comes to operating margins:-

Nvidia=65%

Apple=32%

MICROSOFT=46%

Micron=68%

Meta=40%+

Price to sales fails as a metric when margins of the businesses one is assessing are high.

Better metric to use is EV/Cash flow, Ev/FCF/

& Forward PE estimates which will help one to know PEG ratio that these businesses have.

Let us do one for example:-

Nvidia's PE=32 times

Nvidia's 1 Year Forward Growth estimates in EPS=100%

Effectively NVIDIA trades at a forward PE of 22 times for CY2027.

PEG=PE/GROWTH rates= 0.32. For 1 unit of growth theoretically, an investor is paying 0.32 times. Peter Lynch in his book has mentioned that he liked businesses which had a PEG of less than 1 times.

P/S is a vanity metric in a nutshell when it comes to valuing high margin businesses. Always check the

1. Longevity of growth

2. Margins if they are peaking out or not

3. The market expectations via reverse DCF

4. Peg ratio

Bubble or not- that is one's individual opinion :)

“𝘖𝘯𝘤𝘦 𝘺𝘰𝘶 𝘤𝘢𝘳𝘳𝘺 𝘺𝘰𝘶𝘳 𝘰𝘸𝘯 𝘸𝘢𝘵𝘦𝘳, 𝘺𝘰𝘶 𝘸𝘪𝘭𝘭 𝘭𝘦𝘢𝘳𝘯 𝘵𝘩𝘦 𝘷𝘢𝘭𝘶𝘦 𝘰𝘧 𝘦𝘷𝘦𝘳𝘺 𝘥𝘳𝘰𝘱.”

— 𝘈𝘧𝘳𝘪𝘤𝘢𝘯 𝘗𝘳𝘰𝘷𝘦𝘳𝘣

“Once you earn from your own analysis, tips will never feel the same again.”

— Dalal Street

Real estate in India has become so expensive that the older generation might be the last one to own a house.

If your parents already own a house or land, you still have a chance. But if you’re starting from zero, buying property today is impossible unless you have black money.

For most people in the next generation, living on rent will become normal.

Earlier, renting was seen as a temporary thing or even looked down upon. Now it’s slowly becoming the only realistic option for many people.

Dubai: 36°C

Riyadh: 38°C

Doha: 37°C

Meanwhile in India:

Delhi: 45°C

Nagpur: 46°C

Jaipur: 44°C

Desert cities are now cooler than many Indian cities.

This is not just climate change.

It is also years of poor urban planning, endless concrete expansion, disappearing trees, and zero focus on livable cities.

And still 18% GST on ACs.

I remain confounded & stupefied at the vocal cries of my fellow financial veterans, who are all writing open missives to the FM, asking for abolition of LTCG.

Why did we not hear them say the same thing when these taxes were actually imposed and then increased?

Then everybody was busy giving 15/ 10 too those union budgets.

( And if my memory serves me right, I did shed actual sad tears on television interviews when these taxes were imposed. You may find them online on YouTube).

The government wants the public to get awed by a "record breaking" $95 billion "gross FDI" in India last year.

Ofcourse they didn't tell you the "net FDI", which happens to be in single digits.

Forget that !

Even if you consider the gross FDI, let's get a perspective of where we stand wrt the world.

Just one US company (Nvidia) is investing $150 billion every year in a tiny nation like Taiwan.

This is 1.8 times what the entire world together invests in one of the fastest growing economy like India.

And this perspective matters.

The world is moving ahead at break neck speed. And the world is losing confidence in India.

If the government is not accepting the harsh realities, they is no way they are going to work towards fixing them.

An open, heartfelt appeal to the Hon’ble Finance Minister @nsitharaman from those who back India’s growth story with their risk, patience, and capital:

Every single day, millions of ordinary Indians, alongside global fund managers, make a profound choice. They look past global conflicts, fractured supply chains, and rising macroeconomic headwinds. They bypass the traditional, passive safety of gold and real estate. Instead, they put their hard-earned savings into the ultimate act of faith: the Indian equity market.

Investing in Indian enterprises isn't just about chasing a ticker symbol; it is an act of nation-building. It is the patient capital that builds our highways, funds our tech startups, erects our manufacturing units, and creates millions of jobs for our youth.

Yet, today, our fiscal policy treats this courageous capital with a flat, rigid hand.

When a blanket 12.5% Long-Term Capital Gains (LTCG) tax is levied without the shield of indexation, it ignores a harsh economic reality: inflation and rupee depreciation eat away at nominal gains. An investor holding a stock for a decade is taxed at the exact same rate as someone who held it for just 366 days. By erasing the time factor, we are essentially taxing phantom profits and treating long-term partners like short-term travelers.

Look across the world at how our peers treat those who commit their capital over horizons of time:

The United States structurally rewards time, dropping tax rates down significantly even to 0% for certain brackets to incentivize people to stay invested.

Singapore and Hong Kong charge 0% on long-term capital gains, understanding that frictionless capital is the lifeblood of an economic superpower.

In a deeply volatile geopolitical era, where global capital is fiercely contested and a depreciating rupee pressures dollar-denominated yields, India cannot afford to penalize its biggest believers. If we tax away real returns, we risk pushing global capital to friendlier shores, and worse, driving domestic savings back into dead, unproductive physical assets.

The solution isn't just a simple tax cut it is a structure that honors time.

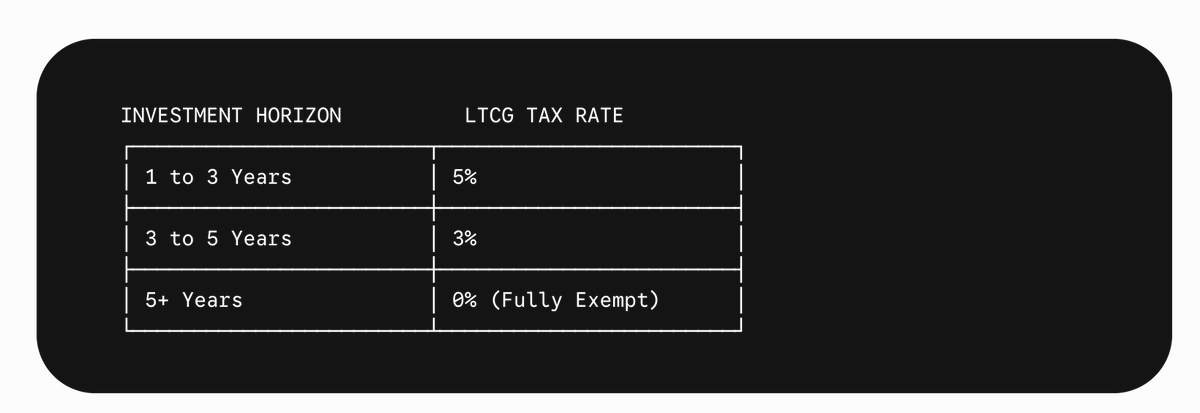

We propose a bold, competitive Tiered LTCG Taxation System that separates the speculators from the builders and positions India as a premier global destination for capital:

Held for 1 to 3 Years: 5% (Instantly boosting global competitiveness and liquidity).

Held for 3 to 5 Years: 3% (Providing deep relief as corporate capex cycles mature).

Held for 5+ Years: 0% (A complete exemption for true, generational partners of India’s growth).

By introducing this tiered structure, the Government will not be giving a "concession" to the wealthy. You will be building a behavioral firewall. You will be radically lowering the cost of capital for every Indian corporate champion trying to build a global empire, and you will be giving the retail investor the middle-class citizen putting ₹2,000 a month into a SIP a clear, predictable path to true financial independence.

Wealth creation is not a vice to be taxed; it is a virtue to be nurtured.

Let’s not view our capital markets merely as a revenue stream to fund the next fiscal quarter. Let’s view them as the roaring engine of a $10 Trillion Viksit Bharat.

Honorable Finance Minister, trust the investors who trust India over the long haul. Reward the time they commit to our nation, and watch us build an economic fortress that no global storm can shake. 🇮🇳

#LTCG #TaxPolicy #ViksitBharat #IndianEconomy #BudgetSpirit #LongTermInvesting

Dear FM Madam @nsitharaman ji,

I have said it before. And I'll say it again. Loud & Clear. I hope you read this. My audience will repost this until it reaches the Ministry.

LTCG of 12.5% on Equities is one of the Lowest in the World.

But there are a few issues:

1. LTCG was ZERO from 2004 to 2018. STT was introduced to offset the Loss in Revenue. It incentivised long term Investors to Hold on Patiently and enjoy Long Term Returns. I believe that Step was something Golden and rewards Long Term Thinking. FM Madam should reconsider this. Keep STT. Abolish LTCG. Consider Long Term Investors as a Partner in Growth of India.

2. STT is already taken for every transaction. This is a tax. Again putting Capital Gain, especially on Long Term Gains is not Ok. This is my Opinion. STT is borne by the investor irrespective of Profit or Loss.

3. We are not against Paying Taxes. In fact, we all Pay Income Tax, Capital Gains Tax, GST, Excise, VAT, Tax on Dividends and what not. The problem is the Freebies which are Distributed during the Elections. This is not at all ok. We don't want a single rupee of our Capital Gains to be used for Freebies. Please.

I humbly request the FM Madam to Abolish LTCG on Equities. Make the Long Term Period 24 months instead of 12 months. You will see Patient Capital 👍 We need Patient Capital to Drive Markets. Incentivise Long Term Investing Mindset.

For Indian Investors like me, the Pain is lesser. We will continue to Create Wealth. But what about our FII brothers & sisters. They also deserve to get minimum returns in Dollar Terms.

I feel for the FIIs who have suffered due to declining Rupee and they still have to pay LTCG on Rupee Terms. Something the FM Madam and team should revisit.

I think that it is a good time to implement this. FII no longer control our markets. Domestic Funds are consistent and plenty. If FIIs leave, let them Leave with Head Held High. That is our Responsibility.

India Structually is Brilliant. Let's make it Tax Friendly as well.

Patient Capital will Flow More & Stay, if these Steps are Taken.

A Proud Indian Investor,

#FI

Respected @nsitharaman ji and @FinMinIndia ,

Suggestion 1 of 3 for strengthening India's capital markets:

Long-term capital gains tax on listed equities should be abolished.

A long-term shareholder is not a speculator but a provider of patient risk capital. By investing in and holding businesses, investors help companies expand, create jobs, innovate and contribute to India's economic growth.

India requires enormous amounts of long-term capital to build world class enterprises, infrastructure and global champions. Tax policy should encourage households to move savings from passive assets, including imported stores of value such as gold, into productive businesses that create jobs, generate tax revenues and build national wealth.

The appreciation in a company's value is not created in isolation. During its growth journey, the government already collects corporate tax, GST, income tax from employees, customs duties, stamp duties and numerous other levies. Long-term capital gains are often the final outcome of economic activity that has already generated substantial tax revenues.

Most importantly, tax policy should clearly distinguish between investment and speculation. A long term shareholder is a partner in wealth creation, not merely a participant in market transactions. Tax policy should reward long-term ownership of productive businesses and distinguish it from short-term speculation.

India needs more patient capital, more entrepreneurship and more long term investing. Abolishing long-term capital gains tax on listed equities would be a powerful step in that direction.

Respectfully submitted.

should protect wealth, not reduce returns.

Basic rule:

✅ Term insurance for protection

✅ Health insurance for emergencies

✅ Investments separately for wealth creation

Mixing insurance + investment often creates confusion and poor returns.

#Insurance#FinancialPlanning

Many people buy insurance.

Very few understand it. ⚠️

Raj bought:

❌ Traditional LIC plans

❌ Random ULIPs

❌ Multiple small policies

Total premium:

₹1.2 lakh/year

Actual life cover?

Only ₹18 lakh.

One medical emergency or income loss could destroy savings.

Insurance