@dampedspring Agree. But just one counter argument is that the ~107M shares they are placing at 380 yen per share would not have had the same demand (~$255M) if it werent for the warrants.

This is desperate capital raising. They obviously did not learn from the large raise they did last year.

Why do you think bitcoin performs poorly in the next few years? what changed all of a sudden from say October of last year? Sure, we went the 4 year cycle way (again, unlike many had predicted) - but long term, the story is still intact.

Dont project short term sentiment way into the future - we all did this for Metaplanet in June last year (this was on the bullish side). Now, you are doing this for bitcoin, BTCTCs - just because last few months have been really bad.

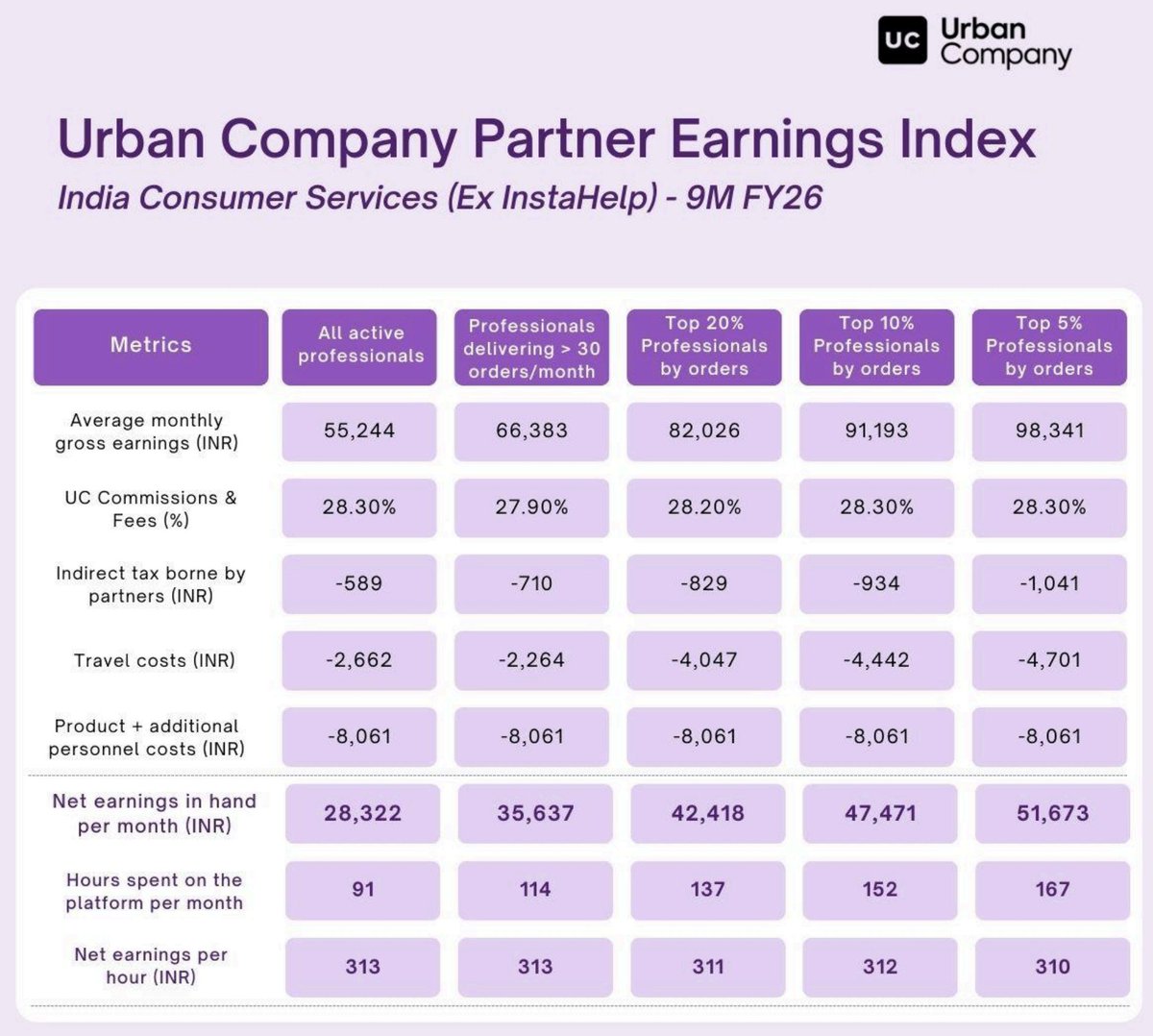

One more reason why UC could create long term sustainable returns.

In fact, the average monthly in hand is brought down by the fact that bottom earners do not work full time. They spend 3 to 4 hours per day as a side gig. The top 20% earners work full time and is comparable to IT entry level.

Top earners on Urban Company are making ~60% higher than typical entry level IT salaries

Urban Company Partner Earnings Update

Average monthly net in hand earnings for all active partners: ₹28,322 (vs ₹26,489 YoY)

Top 20% partners: ₹42,418 per month

Top 10% partners: ₹47,471 per month

Top 5% partners: ₹51,673 per month

I think you should avoid this stock primarily because of poor corporate governance. Clearly SGFin is not a focus for APL Apollo promoters and the current management lacks direction.

The guidance was massively reduced from an EOP loan book of 6000 Cr in FY27 to 7500 Cr in FY30. Like in just one quarter? When asked to the management why this was done - they cited the RBI issue and management change.

RBI issue? like that was like 2 years back and the 6000 Cr guidance was given post that issue was cleared. And management change - what is with this management that the reduction was this drastic?

When poked further, Anubhav (chief strategy officer) admitted the lowered guidance was not because of the RBI issue but because of management change.

And the worst thing is that they plan to grow the loan book linearly. Then someone asked why linearly - he couldnt answer that well. Then he started saying the loan book might even reach 6000 Cr by FY27 and we might be at 10,000 Cr by FY30.

And the new CEO was silent all the time.

Also - they said PAT would grow at 30%. I dont see this happening. Sure operating leverage will play out - but as debt grows - the interest payment will go up - so 30% PAT growth on 20% loan book growth is tough.

Also one more thing - the new warrant money might be directed towards new ventures - which are very unrelated to current supply chain financing business - AIF, insurance broking. They have no moat or experience here. And then Anubhav said they will take approval from the board.

There is clearly no direction. 20% AUM growth with such a small base, underpenetrated market, and great anchors is just unjustifiable.

I think you should avoid this stock primarily because of poor corporate governance. Clearly SGFin is not a focus for APL Apollo promoters and the current management lacks direction.

The guidance was massively reduced from an EOP loan book of 6000 Cr in FY27 to 7500 Cr in FY30. Like in just one quarter? When asked to the management why this was done - they cited the RBI issue and management change.

RBI issue? like that was like 2 years back and the 6000 Cr guidance was given post that issue was cleared. And management change - what is with this management that the reduction was this drastic?

When poked further, Anubhav (chief strategy officer) admitted the lowered guidance was not because of the RBI issue but because of management change.

And the worst thing is that they plan to grow the loan book linearly. Then someone asked why linearly - he couldnt answer that well. Then he started saying the loan book might even reach 6000 Cr by FY27 and we might be at 10,000 Cr by FY30.

And the new CEO was silent all the time.

Also - they said PAT would grow at 30%. I dont see this happening. Sure operating leverage will play out - but as debt grows - the interest payment will go up - so 30% PAT growth on 20% loan book growth is tough.

Also one more thing - the new warrant money might be directed towards new ventures - which are very unrelated to current supply chain financing business - AIF, insurance broking. They have no moat or experience here. And then Anubhav said they will take approval from the board.

There is clearly no direction. 20% AUM growth with such a small base, underpenetrated market, and great anchors is just unjustifiable.

Electronics components manufacturing scheme outlay was just increased to 40,000 Cr. This will benefit Kaynes. Read my deep dive on Kaynes - this covers the services, recent issues causing negative sentiment, future growth and valuation.

#BudgetSession2026#Budget2026#Budget

Published a deep dive on Urban Company (NSE: URBANCO). Lot of similarities here with Dentalkart.

1. Both are trying to organize a highly unorganized and fragmented market

2. Both have very low penetration (low single digits) of online services

3. Full stack

4. Market leaders

5. Great management teams

At the peak of the bitcoin treasury bubble - when everyone was saying that its *only* the bitcoin per share that matters for BTCTCs - we got to learn that this was not true.

In this treasury bear market, only $MSTR and Metaplanet (to a lesser extent) have been able to buy bitcoin at a meaningful scale.

$MSTR's moat with its scale, preferreds, and a great team proved quite solid - evident after today's buy.

Navigating the market in 2026 - year with midterm elections $SPY $QQQ #Bitcoin

Three important charts/images here to talk about. Midterm years are very volatile, and if things play out as they have historically, this gives us an incredible opportunity to buy the dip in Q2 and Q3 of 2026.

Chart 1

If you see, lows are formed in late Q3. This is right before the elections - as market slowly gets rid of uncertainty as to how the elections would play out. There will be volatility - see the avg/median dips - but also factor in the fact that lot of these years have had:

- Recessions (1974, 1982, 1990)

- High inflation/stagflation (1974, 1978, 1990, 2022)

- Nasty bear market (2002, 2010)

- FED tightening w/o high inflation/recession (2018)

These ingredients are missing this year:

- Recession risks are low as AI productivity/spend and OBBB help GDP growth

- Inflation, though above 2% target, is more manageable and below 3%

- No bear market, we are in decent momentum

- FED has stopped QT, we are in a rate cutting cycle

So, it is quite likely, unless something crazy happens, that we will see a peak to trough on S&P500 of single digits or at max mid single digits. This could likely fall around late Q3 (as it has historically).

Chart 2

This chart just echoes what the above one says. See the pattern usually formed - consolidation in Q1 (may even have an upswing if earnings beat across the board), and then somewhere in Q2 we start to correct, to a bottom at the end of Q3.

Q2 and Q3 could be good opportunities to buy the dip.

Then its quite bullish in Q4. Q4 has been positive ~80% of the times.

Chart 3

This one guides for 2027 returns. It is quite extraordinary that there has been no down year after a midterm year.

@samvardhansingh what do you think are the reasons?

1. lack of awareness?

2. averse to change - like just why try something new when you know the local guy can do it?

3. is urban company more expensive?

4. service quality?

Anything else? Looking to invest, trying to understand it better.