As a qualitybro myself, who has sinned in overpaying for good companies, current valuations are not 'major depressions' or 'generational lows'. They're just very normal, healthy levels where returns purely from yield and growth in same actually starts making sense for once.

@KarstResearch@anonymouskeepit Whats the math here? Casualty still not softening, but property is. Lets say prop rates down 15%. Exposure has been heavily constrained due to incredible hard market, so you make up mby +50pc of that on exposure, historical elasticity

So half of biz is -6pc, rest is still fine?

Today we are diving into a fairly niche topic --- remigration of E&S policies back into the admitted market, and the effect this would have on wholesale brokers ($RYAN $BRO $AJG - also relevant for investors in carriers $KNSL $RLI $MKL $WRB $CINF)

Read part 5 on su bstk below

For example, the MSFT and Google numbers you indicate... none of those cost anywhere close to that price... so probably quite high penetration in lower-salary workers where 300/mo is double-digit percentage of salary?

Second would be pricing. Electricity and air travel is also ubiquitous. Doesn't mean its not sold at marginal cost and razor-thin margins. Not hard to imagine open source models, local inference and competition to keep DC utilization high means all value accrues to buyers of AI, not providers.

@SouthernValue95 But that spend of 300/mo wouldn't that be in like 2040? CRM is obviously a high pay / FTE employer compares to the average white collar in those 900. So 300/mo compared to full monthly salary is small... but move down to an Italian accountant or a government bureaucrat...

Thanks! In my mind a bit of a false dichotomy. Brokers are not pure cyclicals (i.e. soft market bottom always being best place to buy). Brokers will still grow EPS in a soft market, maybe just 'only MSD' thru inorganic. So at this valuation, it's expectations vs reality, not if we have throughed fully. Remember, its only the difference in organic EPS growing msd in a moderare market or declining LSD in a soft market. It's not like carriers where profitability can be materially impaired.

Secondly, casualty is still firm, so its a question of P&C hardening. Generally, inflation and increases in exposure unit demand is helpful here. Hormuz and data centers both help here.

Third, its a question of reinsurance. 2025 was a super clean accident year. Softer reinsurance pricing flows directly into retail. I think reinsurance will continue to soften until major cat risk hits.

Lastly, we have been in a very hard market. As prices moderate, people will re-add more coverage again. So brokers only suffer partially... its total written premiums that actually have to decline, not just pricing.

So at 13x foward earnings, I would say all of this is more than priced in. For a cyclical where EPS can decline double-digits in a soft market this would be less interesting, but again... soft/hard is just the difference in growing fast or slow, not whether they grow at all.

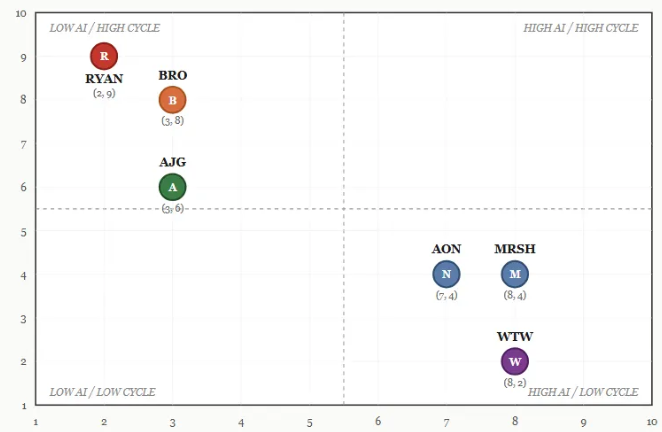

New post today in insurance brokers: "Which horse to pick" - combines our takes on Cycle + AI risk with an overlay of management quality, M&A capabilities and broader business quality (excuse the AI-assisted graph). $AJG $RYAN $BRO $AON $MRSH $WTW - link in bio & below.

@aerockrose Do binary search for 3 rounds, then always assume he would think adversarially and go to margins of probabiliyy space (i.e. no 57/58).

If you still havent hit by last free guess, stop playing. He never stipulated you have to finish the game.

We published part 3 of our insurance broker writeup on the stack today. Cycle risk in focus, for both admitted + E&S. $AJG $BRO $RYAN $WTW $AON $MRSH

We go through recent pricing data on renewals, E&S market dynamics, casualty vs property and how the earnings outlook is hit.

Today we released our 2nd of four articles on insurance brokers ($AJG $BRO $WTW $AON $MRSH $RYAN) -- focused on AI-risk.

Steel-man is that brokers live on information asymmetry and LLMs collapse this - but we have 4-6 reasons to believe this won't be so.

@ToffCap $RELX --> Cheap and growth inflection ahead on relevance of data assets + increase in digital fraud.

$AJG --> Will grow EPS +50% next 3-4 years, and trades 15x NTM P/E.

$CDW --> Bombed out after todays okay earnings. Peak depression on mediocre results.

$CDW - open Q - "ugh, why do I own this shit? Christine is continually unable to manage costs" - down 20% - "fuck, can't sell it this cheaply"

Huge overreaction, but pretty natural since no natural ownership... no growth for compounderbros, not cheap enough for value-guys.