April Trading Data

1. Kalshi weekly volume: $3.91B for the week of April 26 (+27.8% WoW), an ATH. Prior week $3.06B; Masters week $3.5B.

2. Polymarket same week: $1.96B (+4% WoW). Kalshi's lead widened to ~$2B, the largest recent gap.

3. Kalshi sports: $3.0B/week, 76.7% of total. Drivers: NFL Draft (Apr 23-25), NBA Playoffs, NCAA tournament.

4. YTD through April 20: Kalshi $37.5B, Polymarket $29.2B.

For #RWA, this changes everything. NYSE listing tokenized securities means on-chain assets get:

→ Regulated primary markets

→ Institutional-grade liquidity

→ T+1 finality with existing CUSIP infrastructure

Invesco running a tokenized Treasury fund on-chain means:

→ $2.2T in AUM now has a live on-chain product

→ Proof that compliance + on-chain structure can coexist at scale

SEC removed crypto entirely from its 2026 exam priority list.

Three variables are converging simultaneously: Regulatory clarity × Institutional capital × TradFi going on-chain.

The infrastructure layer that wins in this cycle, 3–5 year build window.

→ On-chain securities issuance platforms

→ Institutional-grade custody

→ Prime Brokerage on-chain

→ RWA base-layer protocols

Future Innovation Capabilities of RWA

1. 24/7 Trading: Shareholders can trade on-chain stocks 24/7 on supported venues, no longer restricted by traditional trading hours of the NYSE or Nasdaq.

2. DeFi Collateral & Synthesis: Transfer agents can still track the "beneficial owner" when equity is deposited into lending pools or collateral positions, ensuring dividends and corporate actions are correctly distributed to the ultimate address.

3. Capital Efficiency: Shareholders can obtain liquidity without selling their stocks (via collateralized lending or derivative hedging). This allows for cross-asset class hedging and leverage within a single account, reducing position risk caused by settlement delays.

As regulators like the SEC clarify the different legal attributes of issuer-led tokenization vs. custodian-backed tokens, and as traditional exchanges (e.g., Nasdaq) advance licenses for tokenized securities trading, we can expect a hybrid market structure to emerge within the next 3–5 years. This structure will feature "on-chain shareholder registers + compliance whitelists + multi-venue price discovery." Transfer agents and settlement layers capable of bridging mainboards, compliant CeFi, and compliant DeFi are likely to become the new systemic infrastructure-level players.

As of Feb. 11, Paradigm’s Prediction Markets Volume Distribution chart shows total all-markets volume at $580.1 million. Sports-related topics — including baseball, NCAA, and NBA — led with $292.4 million, followed by uncategorized topics at $174.5 million, crypto at $33 million, and politics at $49.9 million. Overall, sports-related predictions accounted for over 50% of total trading volume.

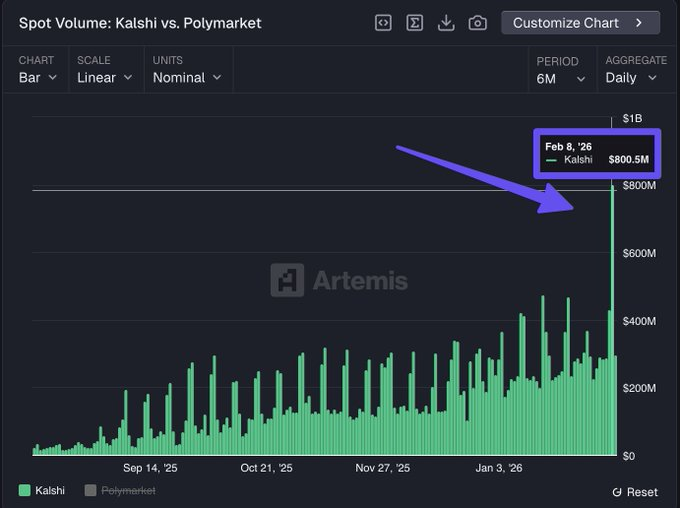

According to data from Artemis, Open interest across platforms including Polymarket, Kalshi, Limitless, and Opinion surpassed $1.1 billion for the first time on Feb. 7, setting a new ATH.

n terms of spot volume, platforms also hit a record $1.4 billion. On Super Bowl Sunday, Feb. 8 alone, Kalshi generated $800 million in volume, while Polymarket recorded approximately $311 million.

Opportunity Analysis

1. Infrastructure gap in tokenized silver: There is a notable absence of compliance-grade, institutionally recognized silver tokens comparable to PAXG for gold within major DeFi ecosystems (Ethereum/Solana/Monad). This represents a substantial infrastructure opportunity.

2. Full release of asset liquidity: On-chain gold can be deposited into lending protocols (e.g., Aave) and used as collateral to borrow USDT for other investments. This enables investors to enjoy gold’s price appreciation while retaining liquidity-something impossible with physical gold.

3. Shift in trust mechanism: Blockchain-based RWAs (real-world assets) offer on-chain transparency and instant redemption, gradually replacing reliance on traditional over-the-counter gold trading. For users in regions with underdeveloped financial infrastructure, tokenized gold becomes the only practical asset for accessing real-time, global gold exposure.

Smart contract failures are rarely “black swans”. They are repeatable patterns: privilege abuse, oracle manipulation, reentrancy, bad accounting, unsafe upgrades, and MEV blind spots.

Security is a system: threat model → audits → monitoring → incident playbook.

Retention isn’t a metric. It’s the only proof your product is real.

If users don’t come back without incentives, you don’t have PMF - you have paid activity.

Track cohorts. Reduce time-to-value. Fix onboarding friction. Ship the one feature that makes the second use inevitable.

Durability > hype.

#web3 #startups #product #growth