THE MOST RELIABLE $BTC BOTTOM SIGNAL JUST FIRED. AGAIN.

When the % of supply in profit crosses the % of supply in loss, half the network is underwater.

Every prior cross marked the cycle bottom zone:

2015, 2019, 2020, 2022.

And now in 2026.

We're closing in on the Bitcoin bottom.

Usually it takes another 1-3 months after the cross before the final low prints.

This is the most rigorous Bitcoin paper

I've read. I've been studying —

and testing — it for 20 days.

https://t.co/mCfJQpJTbE

Dr. Santostasi and Dr. Perrenod gave us the ruler —

and the imagination to see the oscillator.

Together: the most falsifiable framework

in crypto economics.

The Power Law isn't just a model —

it's the most precise ruler we have

for measuring where Bitcoin stands.

Most models describe the past.

The Power Law keeps passing tests

it was never designed for.

"Isn't β=5.69 just curve-fitting?"

Fair question.

So I ran a test the paper didn't.

━━━━━━━━━━━━━━━━━━━━━━

Materials & Methods

━━━━━━━━━━━━━━━━━━━━━━

Data: Daily closing price and non-zero balance

address count (BitcoinMagazinePro,

2010-08-17 to 2026-06-04, n=5,771).

Model: log₁₀P(t) = log₁₀A + β·log₁₀(t)

where t = days since Genesis Block (2009-01-03).

Out-of-sample design:

The power law was fitted exclusively on data

up to the freeze date, with zero observations

from the test period used in estimation.

Two freeze points were tested:

① Freeze at 2016-07-08 (2nd halving)

Training: n=2,153 | Test: n=3,617 (10 years)

② Freeze at 2020-05-10 (3rd halving)

Training: n=3,555 | Test: n=2,215 (6 years)

Residuals computed as:

ε = log₁₀(P_observed / P_predicted)

normalized by in-sample σ.

Mean residual and area integrals

(trapezoidal rule) applied to test period only.

The out-of-sample test was my idea.

Computation and analysis executed with

Claude Opus 4.8 (Anthropic).

━━━━━━━━━━━━━━━━━━━━━━

Froze the power law using data up to 2016 only (β=5.717).

Then measured the following 10 years it had never seen.

Result: mean residual −0.05σ. Effectively zero.

Frozen at 2020 instead → next 6 years, −0.13σ.

Same story.

The line drawn in 2016 ran straight through the next decade.

That's not fitting. That's forecasting.

The Power Law: powerful because it can be broken —

and hasn't been.

Knowing where we are won't tell us when things will happen — but it tells us exactly what to do now.

Buy Bitcoin Now.

@Giovann35084111@moneyordebt@ScientificBTC@saylor@natbrunell

#Bitcoin #PowerLaw

I love the cadence of this chart

Bitcoin % of Supply in Profit/Loss

As I said previously, you start looking for major market cycle bottoms *after* they cross, not before.

They just crossed.

Such a great chart for keeping people on the right side of the market in midterm years

DON’T OVERTHINK IT.

Just wait until October 6.

Then buy $BTC.

Bitcoin has always moved in a 4-year cycle.

And every cycle, people say the same:

“This time is different.”

It isn’t.

You don't have to believe me today.

Bookmark this now and thank me later.

"The 4-Year Cycle is dead."

Most traders fail because they overcomplicate things.

Simple rules survive longer:

Respect capital.

Protect profits.

Cut losers fast.

Don’t get emotionally attached to positions.

Stay flexible.

Change your mind when structure changes.

Narratives feel good.

Price pays better.

If your entire plan depends on

"This time is different"...

Be careful.

🩸 WARNING: $BTC JUST BROKE THE MOST IMPORTANT LINE IN ITS HISTORY.

14 years of support. Gone.

That trendline survived Mt. Gox. 2018. COVID. FTX.

It just failed.

🚨 YOUR BOT WILL PRINT IF YOU CHANGE TIMEFRAME

It'ss not broken.

Just running at the wrong time.

This is the most common reason why solid strategies bleed.

Thanks to one fix, my bot is printing ~$4k daily.

Public wallet: <https://t.co/UoAjMxAPUI>

Here is exactly what to do about it:

Polymarket is a global platform but the traders on it are not evenly distributed across time zones.

When US markets are open, you have fast reactive traders, institutional flows and bots with serious infrastructure all competing simultaneously.

Inefficiencies close in seconds.

Order books are deep.

Competition for fills is brutal.

When Asia dominates, the participant profile shifts completely.

Slower reaction times.

Thinner books.

Different emotional patterns around entries and exits.

The same signal that gets front-run in 200ms during US hours might sit open for 3-4 seconds during Asian session.

That difference completely changes whether your strategy is profitable.

Weekdays vs weekends is an even bigger split.

Monday through Friday you get structured flow from people trading with purpose.

Weekends shift toward slower less disciplined participants who overreact to momentum and recover from moves more gradually.

A mean reversion strategy that breaks even on weekdays often prints cleanly on weekends.

A momentum strategy that works during US hours might collapse completely during low-volume overnight windows.

Here is what to actually do with this:

Pull your bot's historical results and split them by day of week and by UTC hour.

Do this before you change a single line of logic.

Most developers are surprised to find their strategy has a clear profitable window and a clear losing window hiding inside their overall flat performance.

Gate your bot to run only during windows where the data shows positive results.

Do not let it trade continuously just because it can.

That single change turns more break-even bots profitable than any signal improvement ever will.

Hope this will help you too.

Spent weeks perfecting my signal logic last month.

Win rate looked great in testing.

Deployed live.

Started bleeding immediately.

Took me three days to figure out the strategy was never the problem.

The data feeding it was broken the whole time.

This is the lesson that costs every bot builder real money at least once.

Here is exactly why data quality destroys strategy quality every single time:

Your bot makes decisions based on what it sees.

If what it sees is wrong, the decision is wrong regardless of how good the logic behind it is.

Raw websocket feeds from Polymarket are full of problems that most developers never account for.

Stale ticks that arrive late from cached snapshots.

Duplicate messages showing the same price twice.

Gaps from brief disconnects that your bot never noticed happened.

First tick from any new connection that almost always reflects old order book state not current.

Jitter that causes ticks to arrive out of sequence making your bot think price moved when it did not.

Your strategy sees all of this as real market data.

It makes entries based on prices that no longer exist.

It hedges against moves that already happened 400ms ago.

It holds through reversals it would have avoided if the data was clean.

The backtest looked perfect because backtests use clean historical data.

Live trading uses whatever garbage your websocket connection delivers in real time.

That gap between clean backtest data and dirty live data is where most strategies die.

The fix is not complicated but it requires treating data infrastructure as the first priority not an afterthought:

> Validate every tick before it reaches your strategy

> Reject anything that does not pass quality checks

> Run multiple parallel connections and take only the fastest clean tick

Warm up connections before windows open and skip any window where the feed quality fails your minimum threshold.

Fix the inputs first, then look at your logic.

This is the first step you MUST do if you're into bots building.

Also leaving a full guide with most common mistakes attached below.

This will help you a lot.

Remember when we dropped the full Polymarket order book archive? 30M+ rows per hourly dump, raw parquet files, everyone loved it

The problem: you had to download 500MB-1GB parquet files, write your own parser, reconstruct the book yourself from tick deltas

That's over. You can now query historical order books directly from the API. 4 lines of Python. 🧵

🚨 FOR US POLYMARKET BOT OWNERS

(this info will save you THOUSANDS)

If you are running a Polymarket bot from the US, read this:

Cause you are fighting with one hand tied behind your back.

Most people building bots have no idea this structural disadvantage even exists.

Here is exactly what changed and why it matters:

Polymarket now allows KYC-verified colocation for market makers.

It means that professional trading firms can place their infrastructure physically close to Polymarket's matching engine with full authorization.

(mostly Asian and China-based operations)

These setups are running sub-10ms round trip times to the CLOB.

US-based bots sitting on domestic servers are looking at 80-120ms minimum just from geographic latency.

That gap is not closeable with better code.

It is a physical distance problem.

In FIFO queue systems like Polymarket's CLOB so milliseconds determine everything.

First order placed gets filled.

Second place gets nothing.

A bot 100ms slower than a colocated Asian market maker is not competing.

It is consistently arriving after the fill is already gone.

The competitive reality post-KYC colocation is that the most profitable edges in short-window crypto markets are now dominated by foreign professional setups.

With infrastructure advantages that US-based developers simply cannot match from home...

Ireland and Dublin VPS setups are currently the closest viable option for non-Asian developers.

Properly tuned servers there can reach 16-17ms P50 round trip to CLOB.

Not perfect.

But dramatically better than US domestic.

The practical advice is blunt.

If your 5-minute BTC bot was profitable before V2 and is now bleeding, geographic latency combined with increased professional competition is likely the reason.

Look at this guy: [https://t.co/suqyZxusTD]

He made $727k in one month and disappeared right after the update.

Migrate your infrastructure to Ireland or consider pivoting to market types where speed is less critical.

The game changed.

The setups that win reflect that reality.

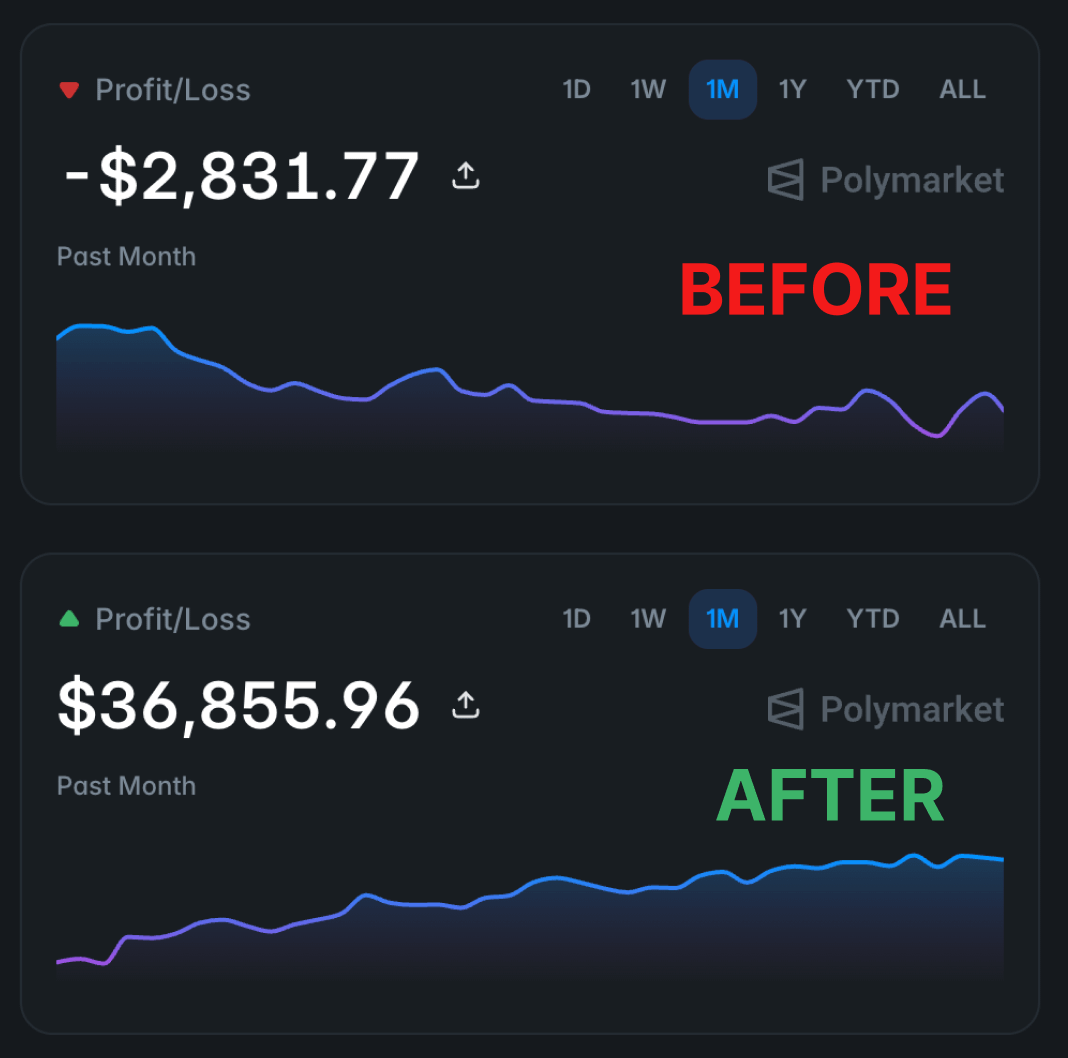

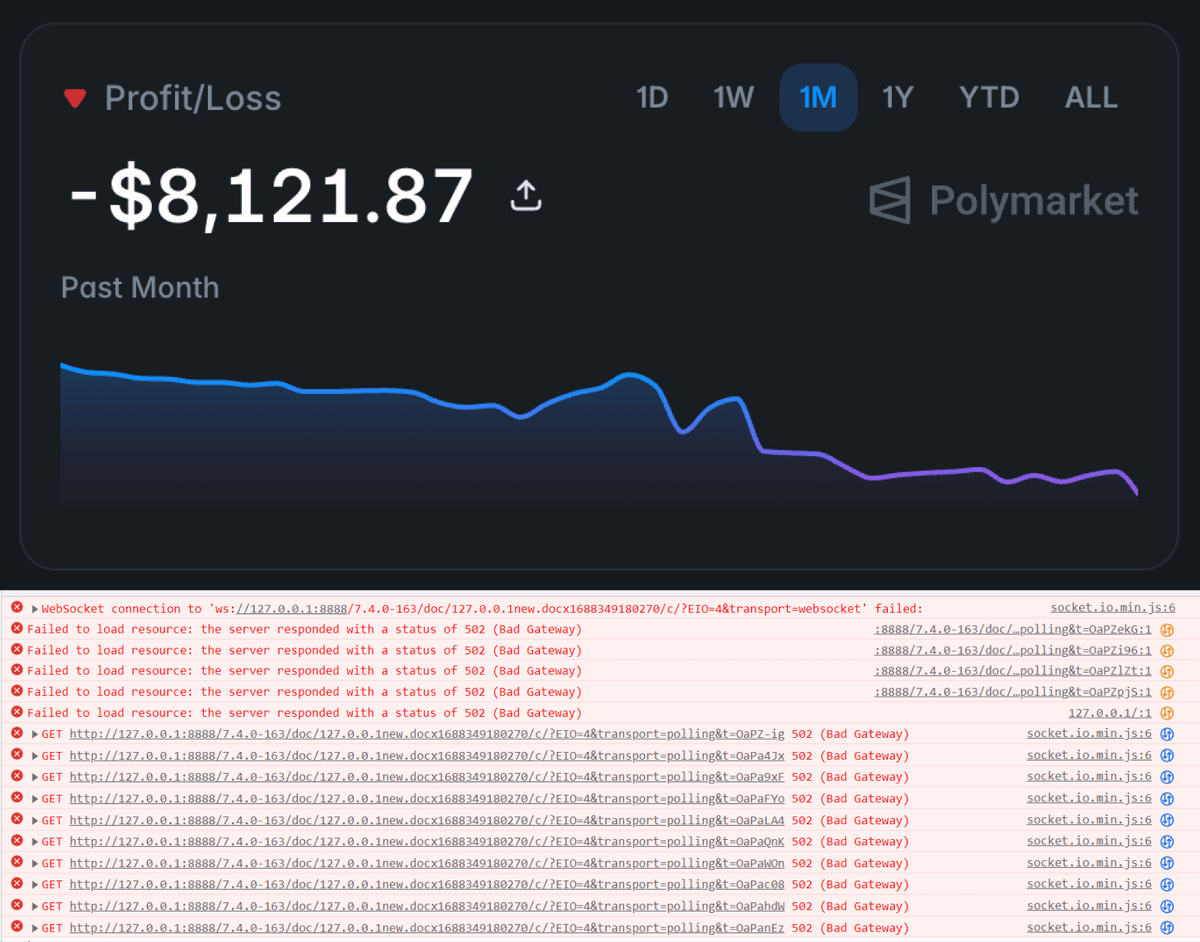

Your bot is losing because of dirty data.

Not bad strategy.

Most developers spend weeks perfecting signal logic and never touch their websocket setup.

That is the single most expensive mistake in Polymarket bot building.

Here is exactly what is happening and how to fix it completely:

Raw Polymarket websockets are full of stale snapshots, missed ticks, jitter and brief disconnects.

Your bot is reacting to prices that do not exist in the real order book.

That is not a strategy problem.

That is an infrastructure problem.

Here is the full fix system layer by layer:

Start every connection 15 seconds before the window opens.

In the final 5 seconds before trading begins - require at least 3 ticks per token with no single price jump above 5 cents.

If your connection fails that test - skip the entire window completely.

Trading on a bad connection is worse than not trading at all.

Never run one websocket.

Run 100 to 300 parallel connections per feed.

Every 4 seconds kill the slowest 10% and respawn them.

Your bot always takes the first deduplicated tick from whichever socket wins the race.

More connections means higher probability of getting clean data before competitors.

Compare every incoming tick against the last known price from your warmup period.

Any tick with a delta above 15 cents gets rejected immediately and logged.

Stale data entering your decision logic is how a working strategy becomes a bleeding one.

Drop the very first tick from every new connection without exception.

It is almost always Polymarket's cached orderbook snapshot from before the window opened.

Acting on it puts you in trades based on prices that are already gone.

Spread your connection startups evenly across one full second.

Never launch all sockets simultaneously.

Staggered startup gives each connection a better shot at receiving genuinely different market data.

Track timing variance per connection using a jitter EMA.

Cull the most erratic connections first.

Give new sockets 8 seconds to stabilize before including them in the cull cycle.

The result of running all six layers together is dramatically cleaner data than 99% of competing bots ever see.

My best bot was also losing before.

Now it's sitting at $100k PnL.

Public wallet: <https://t.co/UoAjMxAPUI>

Clean data alone has turned losing strategies into profitable ones without changing a single line of trading logic.

This guy has $100k PnL on his public bot.

And just dropped the ENTIRE blueprint on how to build it.

I read every word.

Here is what actually matters combined with my own bot analysis:

His bot focuses on BTC 15-minute markets entering at average 46 cents before windows open.

Pre-positioning.

Not reacting.

Already in before the crowd arrives.

The strategy is inventory routing :

Buy both sides cheap, manage the hedge, clean up through split/merge/redeem flow after every trade.

$100,000 came entirely from carrying positions correctly to settlement.

Not fast entries or complex signals.

Just clean execution repeated thousands of times.

Now here is what his guide adds that most people skip completely:

Websockets are the foundation and most bots are running dirty data.

He runs 100-300 parallel websocket connections simultaneously and kills the slowest 10% every 4 seconds.

Starts connections 15 seconds before each window.

Rejects any tick with a jump bigger than 5 cents.

Then drops the first tick from every new connection because it is almost always a stale cached snapshot.

Clean data alone can turn a losing bot profitable without touching the strategy itself.

Backtesting is where 99 out of 100 ideas die and should die.

AI backtests are fiction for anything beyond the simplest strategies because they ignore latency, fill rates, slippage and adverse selection.

Record your own tick data.

Simulate real fills.

Only deploy when live results match backtest within 3%.

Entry price beats win rate every time.

70% win rate entering at 85 cents loses money.

55% win rate entering at 40 cents prints.

His public bot: https://t.co/NMsjydTaI7

Build it right or don't build it at all.

Full guide attached.

🇩🇪 LEUTE, ICH BIN SCHOCKIERT!

Ich habe gerade meine erste Steuererklärung mit dem thailändischen Finanzamt hinter mir. Und ich verspreche euch: das hier ist eine ganz andere Welt.

Lest selbst.

Ich lebe seit anderthalb Jahren in Thailand. Meine Firma sitzt in Hongkong. Hongkong nutzt Territorialbesteuerung. Was außerhalb der Stadt verdient wird, wird mit null Prozent besteuert. Legal, sauber, offiziell. Deshalb sitzt halb Asien dort.

Aber ich lebe nicht in Hongkong. Ich lebe in Thailand. Also musste ich hier eine Steuererklärung machen.

Und ab hier wird es wild.

SCHRITT EINS: STEUERBERATER FINDEN.

In Deutschland eine eigene Disziplin. Wartelisten von zwei Jahren. "Wir nehmen dieses Jahr keine Neukunden auf, melden Sie sich gerne 2027 nochmal." Du flehst den Steuerberater deines Bruders an dich auf eine Empfehlungsliste zu setzen.

In Thailand? Kumpel gefragt. Nummer bekommen. Samstag Abend Mail geschrieben. Drei Sätze, mehr nicht.

Sonntag Vormittag kam die Antwort.

SONNTAG.

Eine einzige Frage stand drin.

Eine.

Wie viel gibst du im Monat aus?

Ich las die Mail zwei Mal. Mein deutsches Hirn fing an zu zucken.

In Deutschland geht so eine Mail anders los. "Bitte senden Sie uns: sämtliche Belege der letzten zwölf Monate, Lohnsteuerbescheinigung, Kapitalertragsbescheinigung, Werbungskosten tabellarisch, Krankenkassenbescheinigungen, Spendenquittungen, Handwerkerrechnungen, Aufstellung außergewöhnlicher Belastungen, sowie eine Übersicht aller in- und ausländischen Konten mit Stichtagsbeständen."

Hier? Wie viel gibst du im Monat aus.

Nicht was ich verdiene. Nicht meine Konten. Nicht ob ich Krypto halte.

Der Grund ist absurd einfach. In Thailand wird nur das Einkommen versteuert das du tatsächlich ins Land reinbringst. Bleibt das Geld in Hongkong, kein Steuerthema. Wise-Karte am Bangkoker Bankomat 1.000 Baht abheben? Reingebracht. Miete vom deutschen Konto? Reingebracht. Restaurant mit Revolut? Reingebracht.

Also nannte ich eine Zahl. Eine. Monatliche Lebenshaltung.

JETZT KAM DER ECHTE SCHOCK.

Ich schrieb zurück: Aber will das Finanzamt nicht meine Kontoauszüge sehen? Belege? Wise-Historie? Restaurantquittungen aus den letzten zwölf Monaten?

Antwort: Nein.

Eine deutsche Steuerprüfung läuft so ab. Der Finanzbeamte will Belege aus 2018 sehen. Du sitzt in einem klimatisierten Büro mit deinem Berater und einem Aktenordner. Du erklärst warum du im März 2019 für 47 Euro essen warst. Der Beamte schreibt mit. Du schwitzt durchs Hemd.

In Thailand? Eine Zahl. Email. Fertig.

Keine Prüfung. Keine Belege. Kein Brief drei Jahre später mit höflicher Bitte um Rechnungen aus 2023. Kein Aktenzeichen das aussieht wie eine Schiffsregistrierung.

Ich überwies die Rechnung meines Steuerberaters. Schickte ihm Reisepass-Kopie, Visa und Mietvertrag. Mehr Unterlagen wollte er nicht.

In Deutschland brauchst du allein für die Anmeldung als Selbstständiger sieben Formulare. Hier: Pass, Visa und Mietvertrag.

Am siebten Tag kam die Mail. Anhang: ein QR-Code. Im Text: 17.000 Baht.

17.000 Baht? 450 Euro!

Für das gesamte Jahr 2025?

Meine letzte deutsche Steuerlast lag zwischen 70.000 und 80.000 Euro.

Ich rechnete dreimal nach. Schrieb meinem Berater zurück: Bist du sicher? Ich habe nichts vergessen?

Antwort: Alles korrekt.

Dann fragte ich wie ich das überweise. Bank, IBAN, Verwendungszweck mit Steuernummer und Veranlagungszeitraum.

Antwort: Geh zum 7-Eleven.

Ich las die Mail drei Mal.

Seven. Eleven.

ZUM KIOSK.

Bin also in den nächsten Laden gegangen. Stand zwischen Wasserregal und Zigarettenregal. Zeigte dem Verkäufer den QR-Code. Er scannte. Piep. Ich legte die Scheine auf den Tresen. Bekam Wechselgeld und einen Bon.

Steuern in Thailand offiziell bezahlt. An der Kasse.

ZUM VERGLEICH:

Deutschland: 70.000 bis 80.000 Euro. Plus Soli bevor er fiel. Plus Krankenkasse die sich anfühlt wie eine zweite Steuer. Plus Steuerprogramm. Plus Berater. Plus Belegsammlung. Plus das Gefühl im Nacken dass dich jederzeit ein blauer Brief erreichen könnte.

Thailand: 450 Euro. Am Kiosk.

Ich erzähle das weil ich selber zwei Jahre gebraucht habe um zu glauben, dass Systeme anders funktionieren können. Wir wachsen mit der Annahme auf dass der Staat im Nacken sitzen muss. Dass Steuern wehtun müssen. Dass Bürokratie dazugehört wie das Wetter. Dass Kontoauszüge ein Naturgesetz sind.

Sie sind es nicht.

Auswandern ist trotzdem keine Lösung für jeden. Hongkong-Firma sauber gründen, Wohnsitz wechseln, deutsche Rückkehrabsicht klären, ein Jahr Aufbau bis das System steht. Das ist kein Klick auf einen Button.

Aber es existiert.

Während ich das tippe sitzen Leute in Berlin und Brüssel und überlegen wie hoch der Spitzensatz noch steigen darf bevor die letzten Leistungsträger das Land verlassen. Sie schreiben Papiere darüber. Sie machen Talkshows. Sie nennen es Gerechtigkeit.

Ich habe heute am 7-Eleven bezahlt.

17.000 Baht. 450 Euro für das Jahr 2025.

WARREN BUFFETT IS WAITING FOR DOWNSIDE.

He now sits on $350,000,000,000 in cash.

He's only moved to cash on this scale twice before in his life.

1. 1999, before the dot-com bust.

2. 2007, before the Great Recession.

Both times, leading stocks crashed 80-90%.

>deutscher Michel

>40h/Woche

>vom Gehalt 45 % Steuern

>mit Rest einkaufen

>Sekt? Schaumweinsteuer

>Bier? Biersteuer

>Kaffee? Kaffeesteuer

>Kippen? Tabaksteuer

>zahle 19 % MwSt auf bereits versteuertes Geld

>40 Jahre lang abgedrückt wie Findom Zahlsklave

>kaufst ne Wohnung

>Grunderwerbsteuer bis 6,5 % obendrauf

>jedes Jahr Grundsteuer, weil du atmest

>Auto? Kfz-Steuer

>tanken? Mineralölsteuer

>Strom? Stromsteuer

>Heizen mit Gas oder Öl? Energiesteuer

>sparen? Abgeltungsteuer

>mit 67 endlich Rente

>Einkommensteuer auf die Rente

>Kinder sollen später erben

>Geld, was schon zigmal versteuert wurde

>Erbschaftssteuer fällig

>Erben müssen Zeug verkaufen für Erbschaftssteuer

>„Fickt euch, ich verlasse Deutschland“

>Finanzamt will Wegzugssteuer auf fiktive Gewinne, die du nie gemacht hast

>mfw der Staat dich melkt, bis du tot bist

>mfw im Grab noch eine letzte Rechnung mit MwSt.

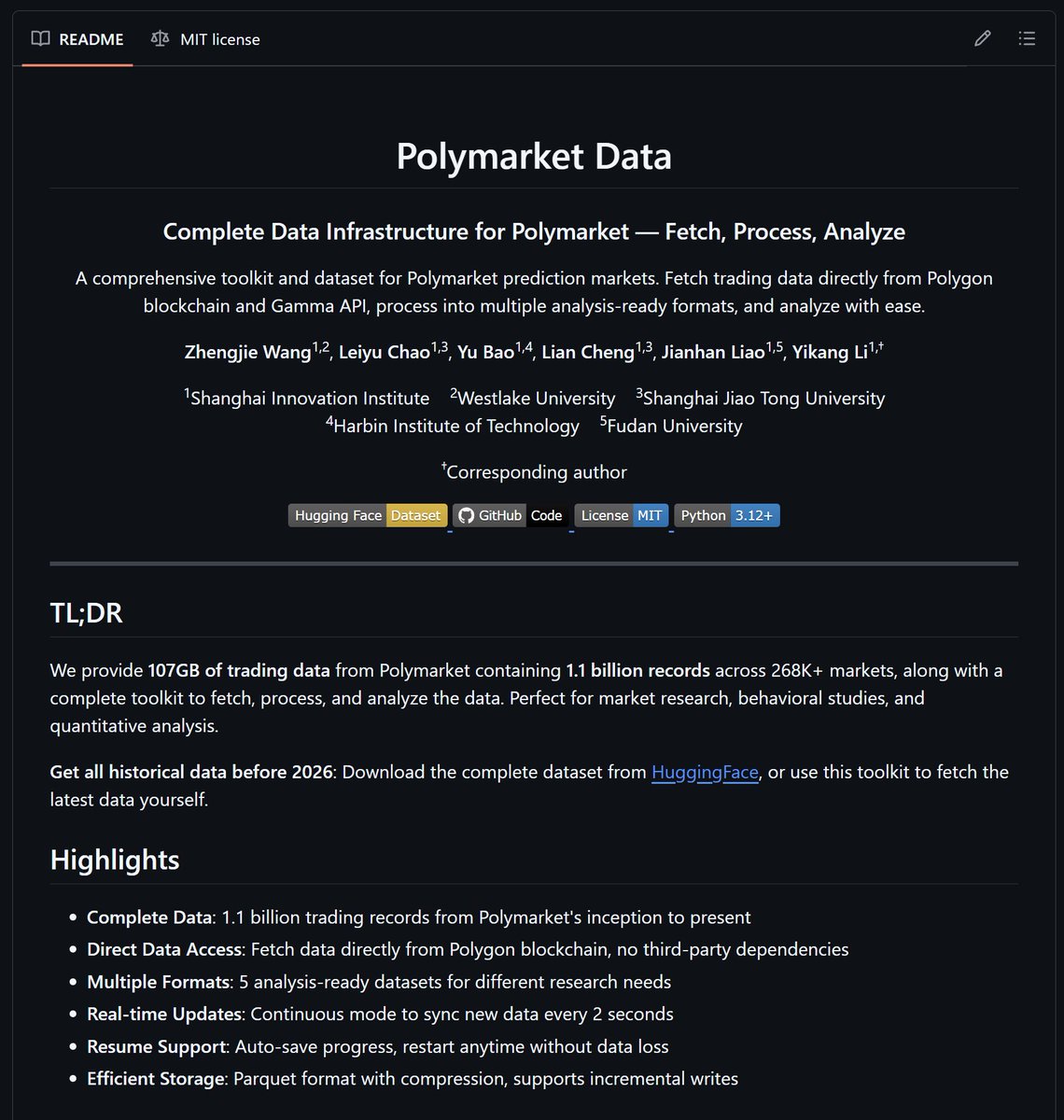

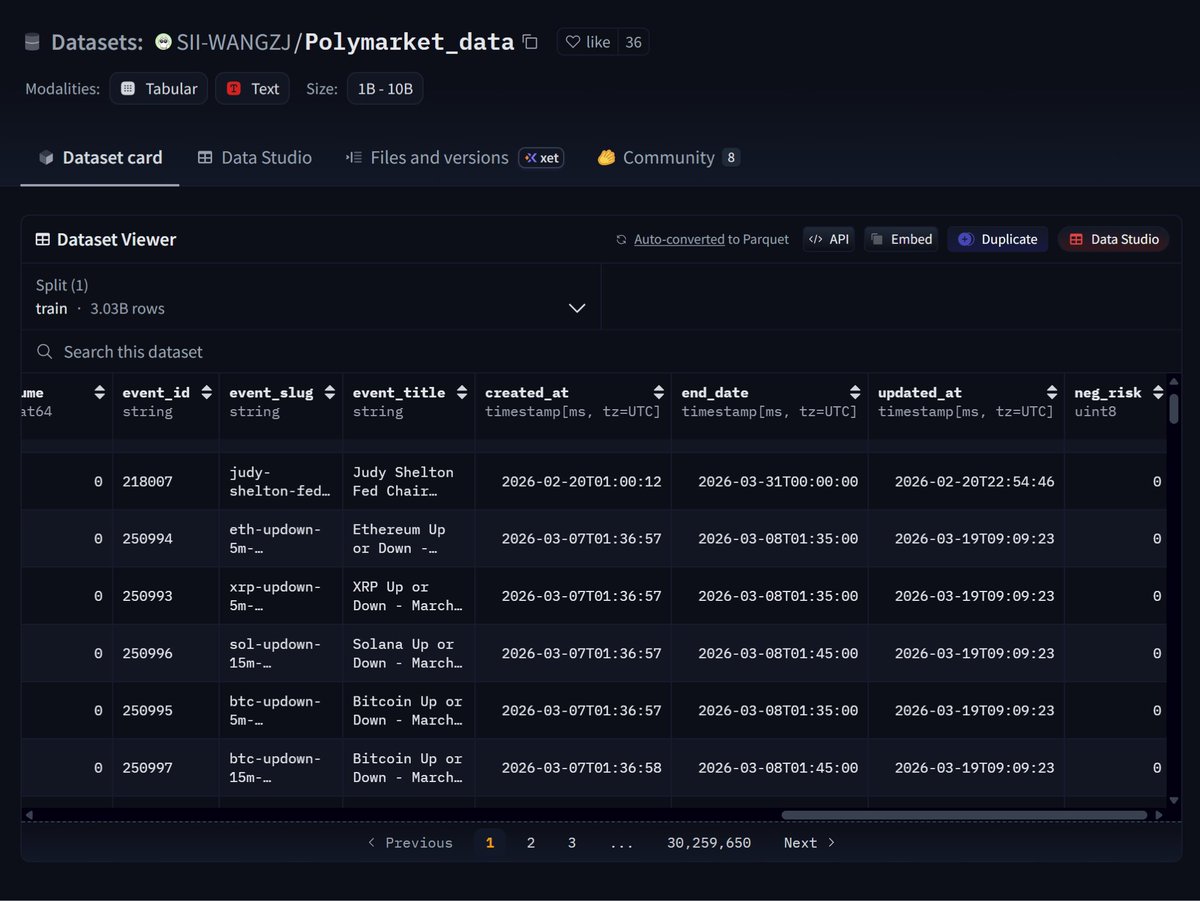

5 students from Shanghai University analyzed over 1.1 billion Polymarket trades across 268K markets, collected 107GB of real trading data and released it for free on GitHub…

This is the largest public prediction market dataset I have ever found.

Here is how you can use it for trading on Polymarket:

This dataset allows you to understand how Polymarket actually behaves and how prices typically move.

You can analyze and compare all markets within the same category to find patterns in price movements that repeat over time.

Lets imagine, while analyzing this dataset, you discover that, for example, most economic markets are less volatile and often have a clear winner right from the beginning (with the highest % probability) - Boom, now this becomes your own proven working strategy.

This way, you can create hundreds of different time tested ideas and strategies based on real historical data.

In addition to the dataset, this repo also provides a full set of tools to work with Polymarket data directly via API, so you can continuously fetch fresh data, process it, clean it and convert it into easy excel format.

This repo: https://t.co/7hj5ZXS6Qi

![0x_Punisher's tweet photo. 🚨 FOR US POLYMARKET BOT OWNERS

(this info will save you THOUSANDS)

If you are running a Polymarket bot from the US, read this:

Cause you are fighting with one hand tied behind your back.

Most people building bots have no idea this structural disadvantage even exists.

Here is exactly what changed and why it matters:

Polymarket now allows KYC-verified colocation for market makers.

It means that professional trading firms can place their infrastructure physically close to Polymarket's matching engine with full authorization.

(mostly Asian and China-based operations)

These setups are running sub-10ms round trip times to the CLOB.

US-based bots sitting on domestic servers are looking at 80-120ms minimum just from geographic latency.

That gap is not closeable with better code.

It is a physical distance problem.

In FIFO queue systems like Polymarket's CLOB so milliseconds determine everything.

First order placed gets filled.

Second place gets nothing.

A bot 100ms slower than a colocated Asian market maker is not competing.

It is consistently arriving after the fill is already gone.

The competitive reality post-KYC colocation is that the most profitable edges in short-window crypto markets are now dominated by foreign professional setups.

With infrastructure advantages that US-based developers simply cannot match from home...

Ireland and Dublin VPS setups are currently the closest viable option for non-Asian developers.

Properly tuned servers there can reach 16-17ms P50 round trip to CLOB.

Not perfect.

But dramatically better than US domestic.

The practical advice is blunt.

If your 5-minute BTC bot was profitable before V2 and is now bleeding, geographic latency combined with increased professional competition is likely the reason.

Look at this guy: [https://t.co/suqyZxusTD]

He made $727k in one month and disappeared right after the update.

Migrate your infrastructure to Ireland or consider pivoting to market types where speed is less critical.

The game changed.

The setups that win reflect that reality.](https://pbs.twimg.com/media/HIjDT_3WYAIubpB.png)