Our $ALLT update article is live. Record backlog coverage and unprecedented $VZ promotional activity for the Allot-secured My Biz Plan and 5G Business Internet hint at a strong Q1 and barn burner 2026: https://t.co/VX8b0Pm1Wb

$CVNA director Michael Maroone accidentally bought 5 shares of stock in January (via a 3P manager)....but "has since implemented measures to prevent future occurrences." Selling $CVNA stock as a director is one thing, but buying it is not condonable.

@GenXPolitico1@FilingSniperx $PANW is a bit rich compared to $ALLT agreed...jk. We like $PANW. Think there is mutual respect between the two companies btw. $ALLT has been evangelizing / seeding a market (mass market network native zero-install SECaaS) that is just now taking off w AI as huge tailwind.

Reminder that $ALLT SECaaS ARR grew 60% organically in Q1. $PANW did same but ex- $CYBR and Chronosphere deals organic growth is in 20s. We love Paly but $ALLT priced at 2x sales with this growth is just silly and borderline offensive!

@PandaLivermore It looks quite conservative — Q1 was 71%. Q2 is a tough comp lapping launch of $VZ My Biz and $VOD UK expansion, but we think $VZ NARR is accelerating and $VOD added 900k more users to SecureNet in May. It will decel from 71 but should stay well above 40

$ALLT continues to periodically sell off for no reason despite business firing on all cylinders ($.21 of FCF in Q1, $2 net cash, 71% SECaaS growth). Allot's Q226 SMB Survey Report is out ($VZ participated as a webinar partner case study): https://t.co/zFswb8ytCQ

Nice win for $MGNI as it continues to extend its dominance in CTV SSP and Ad Server with JioHotstar. Management presented yday at Evercore and sounded upbeat with 25% - 30% CTV growth the new normal. $GOOG remedies next catalyst on deck https://t.co/HaxvsDUgau

We thought something would happen sooner too, but carveouts / asset sales with a complex cap structure and parallel track processes plus business inflection plus space trading makes sense timeline pushed out. The recent transaction comps in 911 and S&S are pretty robust. They haven't had a gun to head to act for almost a year now given the turnaround and debt amendments.

@EggMasonValue Yeah it's only 50% space shitco and 50% NG911 so you have to cut them some slack. Hopefully it ends up crushing those names the rest of year though!

A reminder that $CMTL's biggest win -- the EDIM program replacing thousands of legacy $VSAT EBEM modems -- is still yet to contribute. S&S has been at a $22 - $25m EBITDA run rate which we think moves higher this Q from $LHX A3M, with WAMS and EDIM driving future upside.

One of the key upside drivers for $CMTL S&S highlighted in our report is the US Army's EDIM program. In addition to a revenue opportunity worth potentially hundreds of millions, we believe $CMTL remains the only modem supplier capable of shipping "DIFI." https://t.co/kFd8I2sxMl

$CMTL to report Q3 by Tuesday 6/16. Heightened attention from the $SPCX IPO creates a nice stage for management to showcase the continued turnaround in S&S. Should be first Q of material contribution from next gen modems with continued FY27 ramp. https://t.co/faFJtgJ5tD

Nice to see $ALLT focusing on the Aussie market where multiple tier 1s (Optus, Telstra, TPG, Aussie Broadband) are great prospects. The Aussie government has been very focused on promoting cybersecurity at the telco level.

A great way to wrap up day 1 at CommsDay Australia ✨

The CommsDay Edison Awards dinner was a fantastic evening and great atmosphere, great conversations, and even better company across the telecom ecosystem. Always a highlight to step away from the sessions and connect on a more personal level.

From industry veterans to new perspectives, it’s clear the region continues to push forward on innovation and collaboration 👏

At our dinner table: Philip Britt (Aussie Broadband founder & former CEO), Jilyut Wong (ex-Spark NZ), Peter Chan (Chairman Vodafone American Samoa / ATH), and Bevan Slattery (Founder & CEO, Subco). From Allot -

Ratinesh Kumar , Chen Rozen, Weiming Li and Moti Goldshtein

Also catching up with the Allot team at the event were Paul Fletcher (ATH Chairman, former Australian Minister for Communications & Cybersecurity), Tom Sykes (GM Business Products & Marketing, Vocus) and April Cooper (Chief Executive Consumer, Vocus)

Looking forward to another exciting day.

#CommsDay #Telco #Cybersecurity #Allot

Huge kudos to Moti Goldshtein for a fantastic keynote at CommsDay 👏

A strong message that really resonated: the telcos winning today are the ones building cybersecurity into the network and not bolting it on.

Great to see this perspective getting the spotlight it deserves! 💪

#CommsDay #CyberSecurity

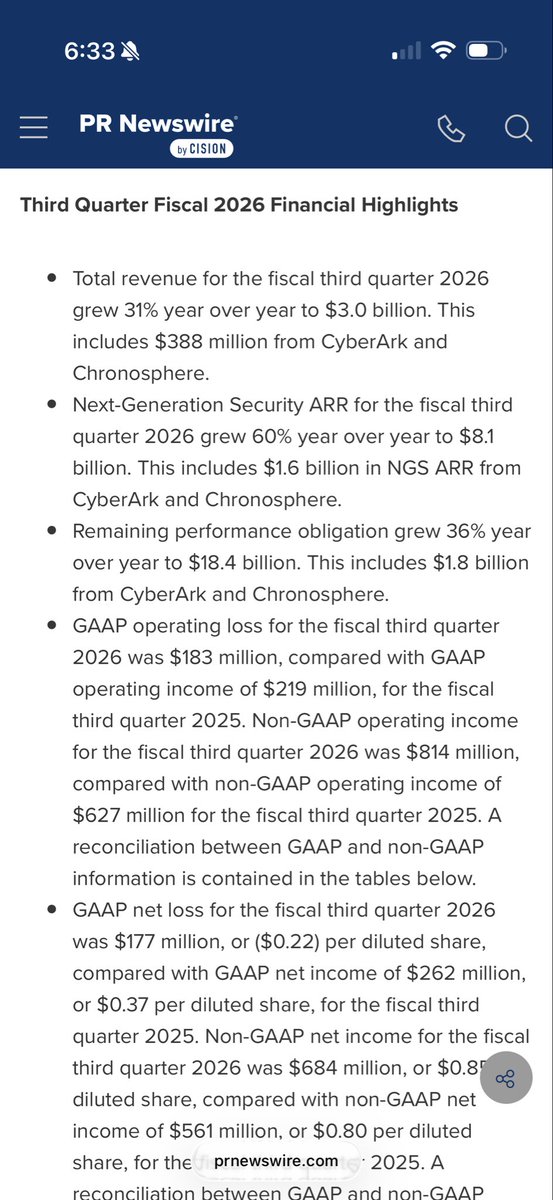

The $PANW earnings call yesterday -- during which @nikesharora took a justified victory lap for strong results after BTD'ing $10m of Paly stock on the Mythos selloff -- was a strong rejoinder to cybersecurity bears.

As $PANW brings real-time, in-line security to the enterprise to meet the agentic threat paradigm (both internal attack surface and external actors leveraging agentic tools), so $ALLT brings these capabilities to its telco partners to protect their consumer and SMB customers on a white label basis. To quote Allot CEO Eyal Harari, "We are taking concepts that are invented into the enterprise space and making them autonomous and simple and affordable into the small business area."

Both $PANW and $ALLT grew next-gen security ARR at 60% last quarter -- the difference is $ALLT did it organically vs. $PANW inorganic (organic ARR growth was in the 20s). Of course, $PANW is a 100x larger company so we're not throwing shade, just noting how impressive Allot's growth rate in SECaaS is as it benefits from the same drivers as Palo Alto but in the SMB and consumer end market where the adoption of network native, zero touch solutions is more nascent.

We think $PANW is a good investment from here, but $ALLT should be a great investment. For $ALLT's 60% ARR growth, at $8.18 you're paying approximately 2x consensus sales estimates for 2027 vs 18x for $PANW.

What about profitability / cash flow / deferred? $ALLT just put up a $.21 FCF quarter (~13% uFCF yield run rate) with current deferred revenue up 90% YoY and CRPO was up 67% YoY at YE2025 (they disclose annually rather than quarterly), nearly 2x'ing $PANW 38% growth (which again, isn't all organic). In fairness, RPO and deferred are metrics tied to $ALLT's "legacy" Deep Network Intelligence business, but in this environment that product line is thriving too as Allot feasts on a weak competitor and leverages its strong cybersecurity products to help win network intelligence deals (and vice versa).

We see scope for material multiple expansion as the Street gains appreciation for what Allot is building, and also anticipate positive revisions to estimates. With $HACK hitting all time highs and $ALLT still sitting at $8 after a year of impressive progress, the stock has never been more of a screaming buy in our opinion.

Apollo noting that new US business formation has been surging lately, likely driven by AI and LLMs reducing the cost and complexity of starting a company:

As we said $PANW $FTNT $ALLT are beneficiaries of AI, not victims. $HACK up 50% since this post, $ALLT still dirt cheap at 2x sales with 59% SECaaS ARR growth.

Vulnerability management stocks have been pricing in this risk for some time now $RPD $TENB. Pure play network security $PANW $FTNT $ALLT have nothing to worry about here, in fact as good as AI can be at detecting patch failures, it’s as good or better at creating attacks!

Another positive $CVNA experience.

Bought a new car yesterday at a dealer. Pre-negotiated all the terms before I arrived, thinking it would save me time. Still took over 2.5 hours, most of which was sitting around waiting. This was at the #1 dealer in the country, supposedly.

Sold my car to Carvana today. 5 mins in the app last night, 14 mins at the vending machine for the drop off. Confirmation of funds en route already.

I hope for many reasons Carvana becomes 10x bigger so they have the cars I want every time and I never have to go to a dealer again. The experience is immeasurably better at $CVNA.

@SwingTraderCO Interesting that so many other execs walked away from those existing RSU / option packages. problem with options is they aren't much good if the stock is overvalued by 50%. insiders can't be convertible arbs.

$TTD makes an interesting CFO hire ($PENG, $LOGI) but no AdTech experience is a red flag, particularly given a $10m equity grant and rich cash comp. Likely driving some of the negative reaction with shares down 9% today. Also, there is still only one audit committee member.

News: The Trade Desk has appointed Nate Olmstead as CFO. He becomes the company’s fourth finance chief in roughly a year and will join on July 9, reporting to CEO Jeff Green.

https://t.co/Xsrh9Q8v9D