Why betting on Samsung’s HBM comeback is a long shot 📉

1️⃣ Bonding tech:

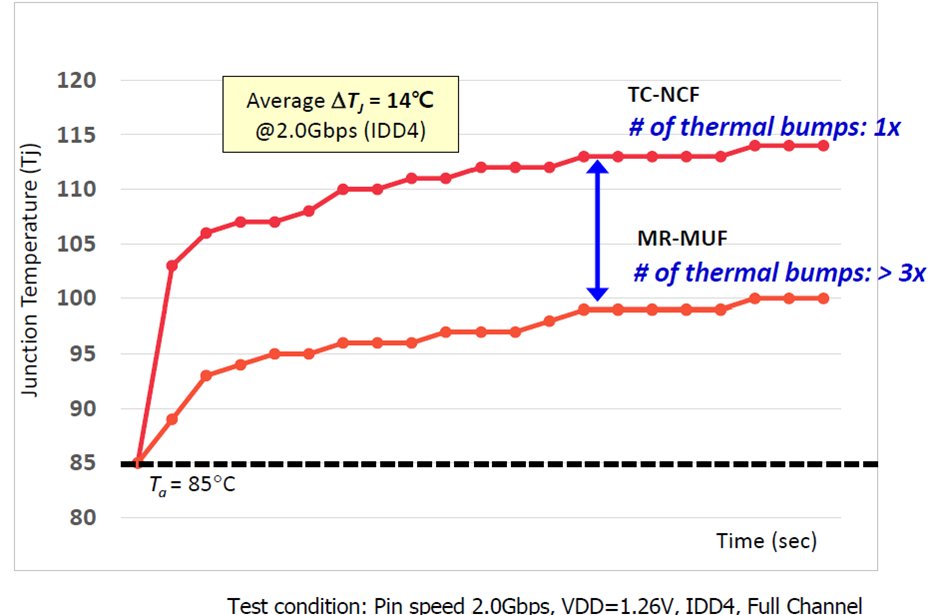

SK Hynix’s proprietary MR-MUF offers better thermal dissipation and a higher yield rate than the TC-NCF technology used by their peers.

2️⃣ 1a nm problem unresolved:

Samsung faces additional issues in its front-end DRAM process since the start of 1a nm. Lower yield rate on the front-end impacts overall HBM yield rate with multiple dies (12-Hi) stacked.

They tried to redesign the base die to meet NVIDIA’s HBM3e 12-Hi qualification, but did not make changes to the 1a nm die. Switching production back to DDR5 is also challenging given their 1a nm process is uncompetitive.

3️⃣ 1c nm is not yet mature:

For HBM4, the use of 1c nm process for DRAM and 4nm in-house foundry process make it hard to believe Samsung can catch up.

Progress in 1c nm has not been smooth and they had to redesign 1c nm process earlier. Samsung’s 1c nm process is not yet mature, while both SK Hynix and Micron are sticking to their mature 1b nm process for HBM4. On the other hand, SK Hynix’s 1c nm has reached mass production readiness.

Time to market is important in HBM as the 1st mover typically gets a big volume share through annual volume contracts lock-in.

4️⃣ Hybrid bonding wildcard:

Hybrid bonding is Samsung’s best chance to catch up in the back-end packaging race. However, the higher cost of hybrid bonding has been delaying the adoption to 2028.

Front-end process remains Samsung’s biggest problem. HBM qualification issue is just a symptom of it.

For deep dive on HBM, check the link 👇

https://t.co/Dfimoms1JH

$mu #Samsung #Hynix #HBM

Why betting on Samsung’s HBM comeback is a long shot 📉

1️⃣ Bonding tech:

SK Hynix’s proprietary MR-MUF offers better thermal dissipation and a higher yield rate than the TC-NCF technology used by their peers.

2️⃣ 1a nm problem unresolved:

Samsung faces additional issues in its front-end DRAM process since the start of 1a nm. Lower yield rate on the front-end impacts overall HBM yield rate with multiple dies (12-Hi) stacked.

They tried to redesign the base die to meet NVIDIA’s HBM3e 12-Hi qualification, but did not make changes to the 1a nm die. Switching production back to DDR5 is also challenging given their 1a nm process is uncompetitive.

3️⃣ 1c nm is not yet mature:

For HBM4, the use of 1c nm process for DRAM and 4nm in-house foundry process make it hard to believe Samsung can catch up.

Progress in 1c nm has not been smooth and they had to redesign 1c nm process earlier. Samsung’s 1c nm process is not yet mature, while both SK Hynix and Micron are sticking to their mature 1b nm process for HBM4. On the other hand, SK Hynix’s 1c nm has reached mass production readiness.

Time to market is important in HBM as the 1st mover typically gets a big volume share through annual volume contracts lock-in.

4️⃣ Hybrid bonding wildcard:

Hybrid bonding is Samsung’s best chance to catch up in the back-end packaging race. However, the higher cost of hybrid bonding has been delaying the adoption to 2028.

Front-end process remains Samsung’s biggest problem. HBM qualification issue is just a symptom of it.

For deep dive on HBM, check the link 👇

https://t.co/Dfimoms1JH

$mu #Samsung #Hynix #HBM

MS on Rubin Timeline

$nvda Rubin is on track: NVIDIA's first Rubin silicon should be out from the TSMC fab this October (first tape-out was in June). Meanwhile, our checks suggest NVIDIA's Rubin engineering sampling (ES) is on track for 4Q25, although the fine-tuning of the Rubin chip design continues. The chips and their system design should be finalized next March, with the chip entering mass production in 2Q26, followed by server racks ramp in 3Q26. So it appears there will be no delay to the Rubin schedule, despite some investor concerns.

Please give Fubon’s analyst credit. He did the channel checks and is reporting data. The alternative is for you to purchase @SemiAnalysis_ Accelerator Model. To me, this reads as glass half-full / half-empty for both $NVDA and $AMD.

This isn’t the first delay, and a 3 months slip doesn’t change the long-term thesis for $NVDA. Take a chill pill. The CoWoS figures still imply FY2027 revenue well above Street expectations. You should be questioning the Street instead.

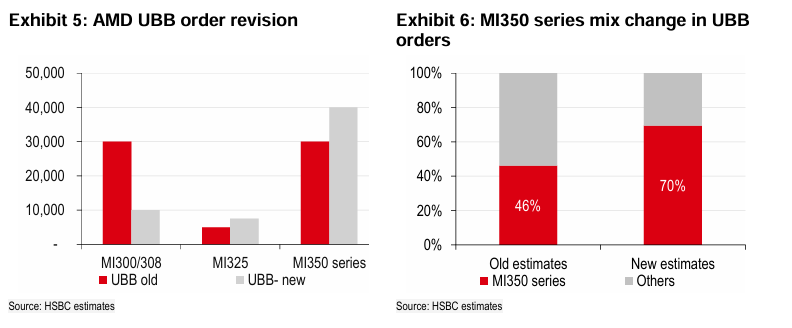

It isn’t particularly bullish for $AMD either. We’ve seen higher CoWoS counts before that were later revised lower. Scale-up is still a big hurdle that remains unresolved.

We need less narrative and more math

1) Rubin redesign leads to more limited volume

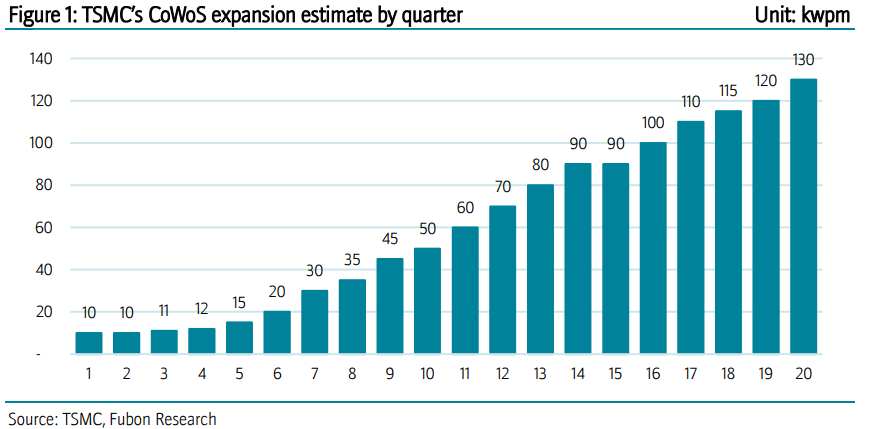

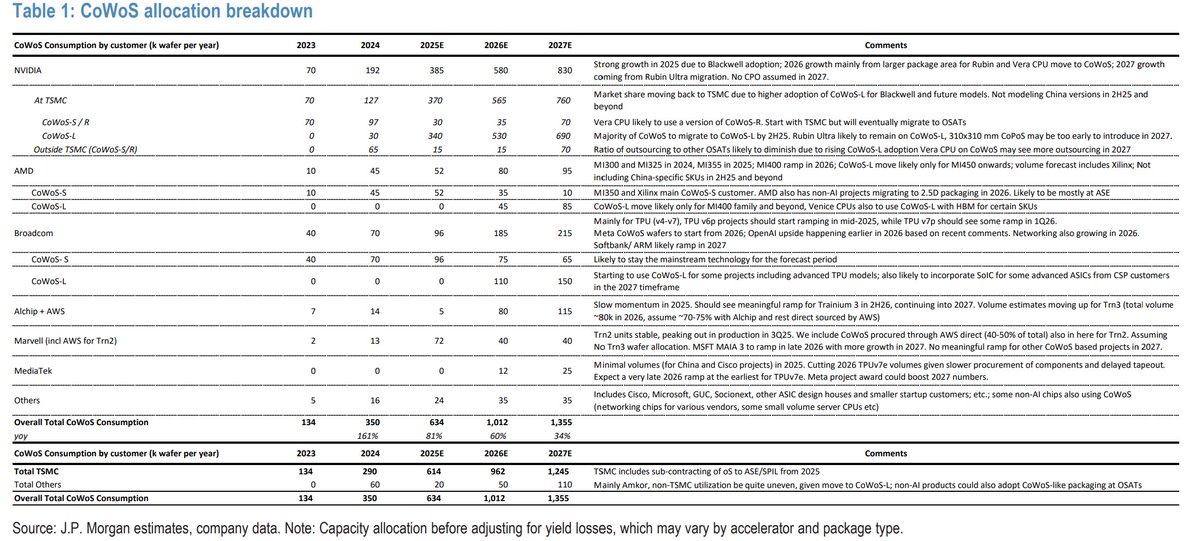

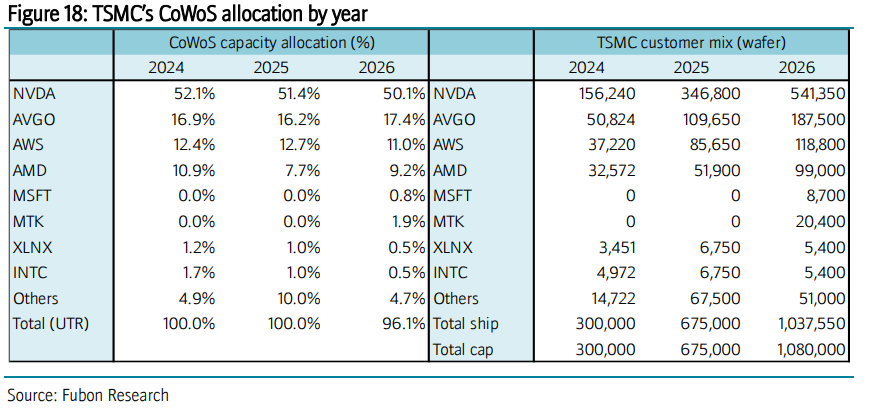

2) TSMC CoWoS capacity to hit 130k in 2027

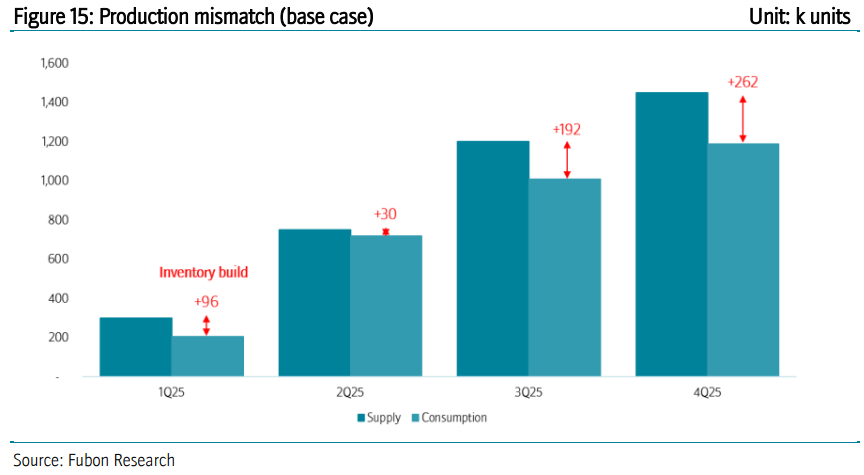

3) Blackwell Volume: 750k in Q1 25, 1.2mn in Q2, 1.5mn in Q3, 1.6mn in Q4

4) Broadcom is fastest growing CoWoS customer in 2026

Source: Fubon

$tsm $nvda $avgo

Precisely, not sure why he is making such a big fuss out of it. Didn't we see a delay with Blackwell previously?

Fubon's CoWoS numbers still give a revenue for Nvidia in 2026 higher than any other sellside. Why not go complain about why the street estimate is too low?

Taiwan analysts are closest to the supply chain, not the West

1) Rubin redesign leads to more limited volume

2) TSMC CoWoS capacity to hit 130k in 2027

3) Blackwell Volume: 750k in Q1 25, 1.2mn in Q2, 1.5mn in Q3, 1.6mn in Q4

4) Broadcom is fastest growing CoWoS customer in 2026

Source: Fubon

$tsm $nvda $avgo