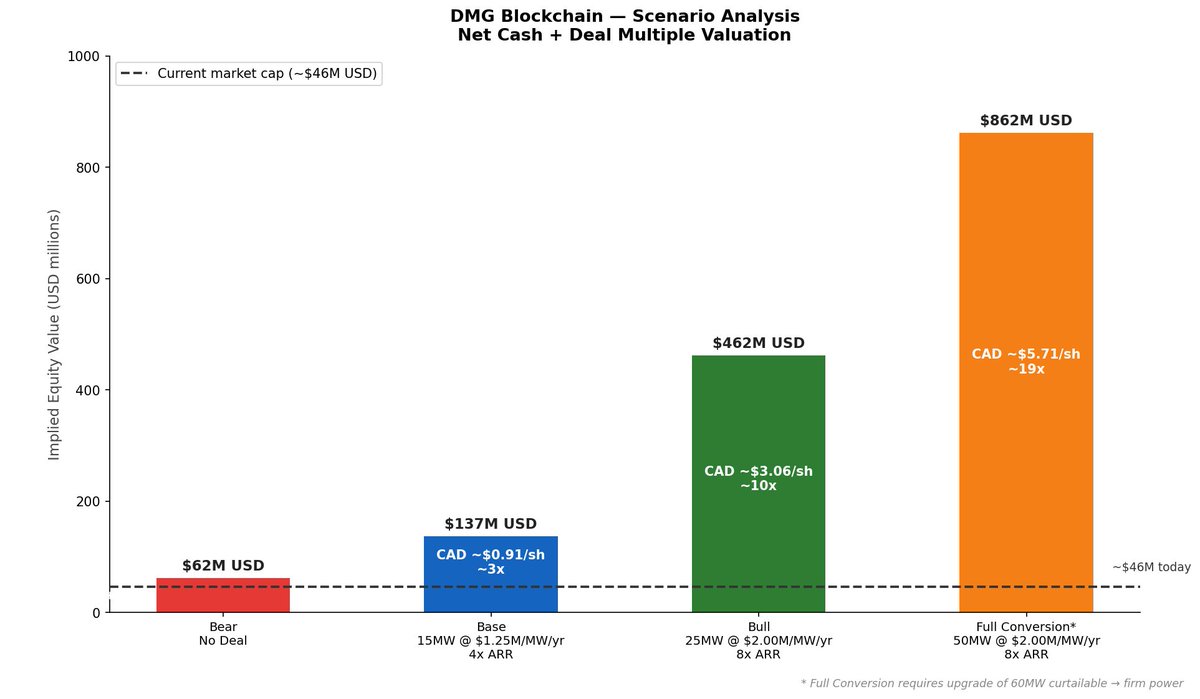

$DMGI trades at $46M USD.

A single AI colocation deal puts the implied market cap at $137M–$462M.

It has happened before: $IREN $RIOT $DGXX all repriced on AI deals.

Ran through a few valuation scenarios. Full deep dive attached

Very few people know about $DMGI in the AI infrastructure space, so here’s a break down of the last week:

$HUT $IREN $WULF $SLNH $RIOT 📖

- 50MW LOI signed for their Christina Lake Facility. Large company, NDA, company will backstop funding. Have applied for an additional 150MW from their utility for that site.

That site have mirrored substations setup, 75MW each. The company owns the infrastructure, 33 acres, and the building.

They already have 12MW of cooling on site. They also have Nat Gas transmission lines running on the property, 50MW for potential back up. First GPUs active this year.

- The have a utility MOU and a 30MW MOU with the @malahatnation. CEO said updates on that partnership can be expected in the coming quarter.

- Canada just announced their AI strategy. DMG has met with defense procurement already and CEO said the Feds called the company this Monday.

- They own SCIF rated modular data centers rated for defense sector grade AI. 2MW already on site, looking at buying 8MW more. CEO said after they signed their LOI for the 50MW, they have received increased interest for the SCIF units.

- 2nd Canadian site and Oregon site, CEO said updates on those sites could be expected in the coming quarter.

- Also, wholly owned digital asset trust, updates expected.

- The company has expressed numerous times that they will not dilute to pay for buildout, as the deal is backstopped. CEO said financing entities were already contacting the company after the LOI.

- The company trades at UNDER ASSET VALUE. Others have run the numbers for fair market value of their MW deal, comes to $5-$7 for just the 50MW.

- 400 BTC HODL, still mining.

- 206M shares outstanding.

$DMGI is still being priced like a former crypto miner — while it’s actively repositioning into AI infrastructure.

As the market starts benchmarking this against AI comps instead of legacy mining peers, multiple expansion becomes inevitable.

Rerating is coming📈

@Maxixm99 Exactly. And the rerating will be unstoppable once $DMGI receives its first payments from the HPC segment. That's when the market can no longer ignore the transition. Numbers don't lie. Thanks for sharing 🙏

Just to catch up with its peers. $DMGI $DMGGF should be trading mininum between 1$ to 1,50$. (And I stay conservative, because smallcaps could be even more explosive.)

It’s a x2-3 from here.

And this is just the beginning.

There’s a lot in the pipeline…

$KEEL $RIOT

$DMGI up ~45% today on the 50 MW LOI announcement.

A few days ago I wrote up the investment case. The setup was interesting then, it is still interesting now.

The LOI matches exactly the full conversion scenario from my article: 50 MW with an investment-grade backstop. At $2M/MW/yr and an 8x ARR multiple that implies ~$862M USD in equity value, or roughly CAD $5.71 per share.

Even after today's move there is significant upside if the definitive agreement follows.

@RayofLi62785906 I know it, also on my list. Any company with compute capacity and power secured is well positioned if they can execute. Haven't gone deep on $SLNH yet though. Worth a closer look you think?

@RayofLi62785906 Thanks! On dilution, management was clear on the last earnings call: financing for the buildout will primarily be debt tied to the client contract. So dilution is not the plan here.

The re-rate has just begun.

You are not bullish enough. Potentially $1B + deal.

$78M market cap…. $DMGI.V

Worth a look…. Long way to go. This is huge news.

$IREN $CIFR $HUT $KEEL $WULF

Starts the trading day up 15% on triple the average volume. $DMGI

$50M market cap, trading at 60% asset value, and just signed a LOI for 50MW data infrastructure for 12 years, with option to expand.

$IREN $WULF $CIFR $KEEL $HUT

@Darmian67190216 It means the tenant has a strong enough credit rating to guarantee the payments. Think large corporations or institutional players. For DMG it reduces the risk that the tenant defaults on the contract.

$DMGI just announced a 50 MW AI data center LOI at Christina Lake.

The tenant is under NDA but will provide an investment-grade backstop. That was always the non-negotiable requirement and it is part of this LOI. 12 year initial term with renewal options, first phase targeted by end of 2026, financing primarily through debt.

Until a definitive agreement is signed Christina Lake keeps running as a Bitcoin mining facility. So no revenue impact yet, but the direction is clear.

Still a non-binding LOI. The definitive agreement is the next milestone to watch.

Step by step the picture is getting clearer. Full breakdown here: https://t.co/CKUHyVTVin

Press release: https://t.co/3iQ0N57usc

$DMGI Q2 2026 Earnings Call - notes and my conclusion.

Notes:

Malahat

Sheldon visited a few weeks ago. Definitive agreement expected in the near future. Plan is to use the Malahat relationship to fill the 2 MW SCIF units first, then scale toward 30 MW.

Power

The 50 MW AI plan does not need the 150 MW firm power approval. Existing 75 MW is enough. Non-firm can be structured as synthetic firm for offtakers. The 150 MW application is a multi-year process and not part of the near-term plan. Near-term additions: natural gas and more non-firm capacity.

SCIF units

Arrived at Christina Lake in March, setup targeted by end of 2026, revenue generation further out. Option to buy additional 8 MW still being considered.

Offtake

Multiple ongoing discussions confirmed. Investment-grade offtaker or backstop is the non-negotiable requirement. Management spending over 80% of their time on AI sales and marketing.

2nd Canadian site

Ontario and Toronto area on their radar.

No cloud ambitions

Colocation only. "We don't plan to be a new cloud and risk our balance sheet hoping somebody will buy GPU hours."

My conclusion:

Management has the right strategy but one criticism remains: they are not doing enough to get their story out. The asset is real, the power position is real, but too few people know about it and that does not help the stock.

The underlying opportunity has not changed. One deal with the right partner and this becomes a very different story.

One thing worth saying: this is a small, asymmetric position for me. The risk here is real and the timeline is uncertain. Make sure you understand your own exposure before getting involved and size it accordingly.

I'll keep monitoring $DMGI and will continue posting updates as things develop. For the most up to date $DMGI coverage give @DMG_Investors a follow, he tracks this one closely.

I'll stay invested as long as the thesis holds. The research I do for my own portfolio I plan to share going forward. Not just DMG, but new investment theses and ideas across different companies. If you're interested in following along, more is coming.

Correct. 50 MW full conversion is the orange scenario. $2M per MW per year was my assumption. The multiples the market applies could of course differ, but the LOI announced today is exactly what that scenario was built around.

Still a LOI for now, so no binding commitments yet. But this is exactly what I want to see the $DMGI management is delivering🤝

$DMGI trades at $46M USD.

A single AI colocation deal puts the implied market cap at $137M–$462M.

It has happened before: $IREN $RIOT $DGXX all repriced on AI deals.

Ran through a few valuation scenarios. Full deep dive attached

Huge technical set up for $DMGI $DMGGF.

The chart is not lying. Something big is cooking. 🚀🚀🚀⚡️⚡️⚡️

50MW LOI

NDA confirmed.

Potential 27 years deal. These guys are serious!

Pssst still 66M$ MC 🤫🫢

Moon next!

@GlobalCollapse Yeah management is painfully slow.

But revenue is not the metric I am watching here. As long as it is 100% mining it just moves with BTC. What I am waiting for is a signed deal. That would be one of the things that actually changes the story.

Exactly, podcasts, interviews or just good own content would give the stock a lot more attention.

A larger dilution outside of what is already outstanding would most likely only happen for a bigger infrastructure buildout. But management was clear on that: "the bulk of our capital raising would most likely be debt instruments tied to client contracts." So that only moves once a deal is signed.

@OnlyKlans1 Cheers! PR is definitely something they need to work on. Agreed on the risk/reward, the assets are real. Hoping BTC holds up so the mining side does not come under even more pressure.

@TheRealG0och Understandable. Personally I feel comfortable with my position as it stands. The assets are undervalued any way you look at it. If there is a bigger pullback or some price action I might even add. But waiting for execution before doing so is definitely sensible.