Acorn Holdings has partnered with Absa Bank Kenya and Co-operative Bank Group to launch the Zinduka Graduate Enterprise Programme, linking student accommodation financing with start-up capital.

The programme targets 5,000–10,000 new enterprises annually, with eligible graduates accessing business loans of KES 200,000–KES 500,000, while students can access unsecured housing loans with monthly repayments from KES 4,000.

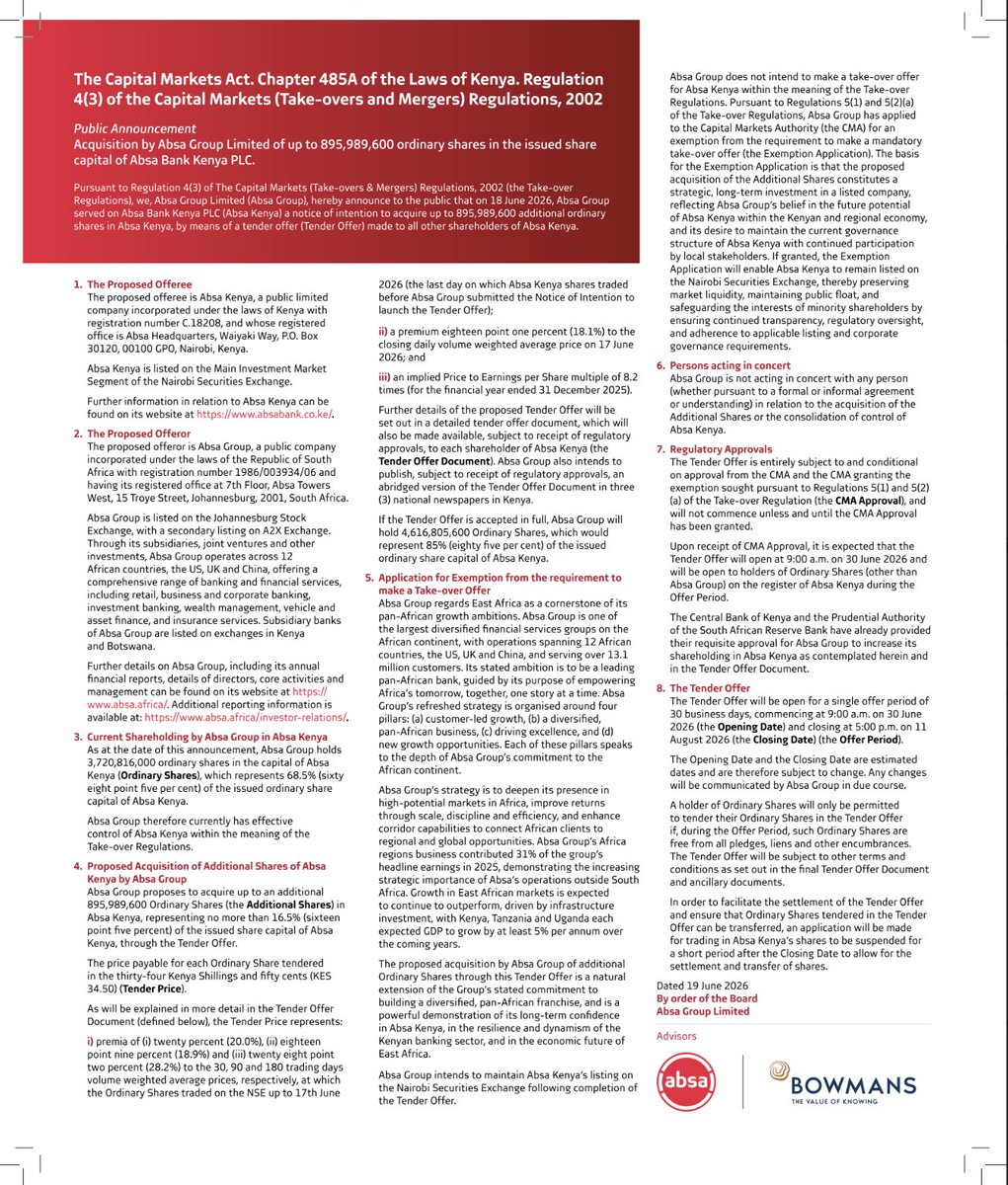

Absa Group has announced a tender offer to acquire up to 895.99M additional shares in its Kenyan subsidiary, Absa Bank Kenya, at KES 34.50 per share, valuing the offer at up to KES 30.9B.

—Absa Group currently owns 3.72B shares, or 68.5% of Absa Bank Kenya, and full acceptance would raise its holding to 4.62B shares, or 85.0%.

—The KES 34.50 tender price represents an 18.1% premium to the 17 June 2026 closing VWAP and implies an 8.2x P/E multiple based on Absa Kenya’s FY25 earnings.

—The offer is subject to CMA approval and an exemption from the requirement to make a mandatory takeover offer.

—Absa Group says it intends to keep Absa Bank Kenya listed on the NSE after the transaction, with the offer expected to open on 30 June 2026 and close on 11 August 2026.

The National Assembly has passed the Finance Bill, 2026, with 122 MPs voting in favour against 40 opposed, and no abstentions.

MPs have also passed the Appropriation Bill, 2026.

They now go to the President for Assent.

TRIFIC Green USD I-REIT offer results:

—The unrestricted offer closed at 103.3% subscription, with investors applying for USD 30.82M against USD 29.83M available, implying excess demand of about USD 0.98M.

—The offer cleared the USD 20.5M minimum subscription threshold by about USD 10.32M, giving the REIT enough demand to proceed with the listing of 37.29M units on the NSE at USD 1.00 per unit.

—The promoter will take up 7.46M units in exchange for transfer of the initial asset, TRIFIC North Tower, while applications of USD 1M and below will be allotted at 100%, and larger applications will be prorated.

—The listing and commencement of trading are scheduled for 29th June 2026.

🎙️ Don't forget to join us tonight at 8:00 PM EAT on #MwangoSpaces as we unpack the AAR Insurance FAARMILY Suite.

We'll be joined by Justine Kosgei, CEO & Principal Officer, and James Kamau, Group Head of Distribution at AAR Insurance, for a conversation on health insurance, coverage options, and what the FAARMILY Suite offers Kenyan families

Set a reminder and join the conversation here: https://t.co/zSp7byXP9o

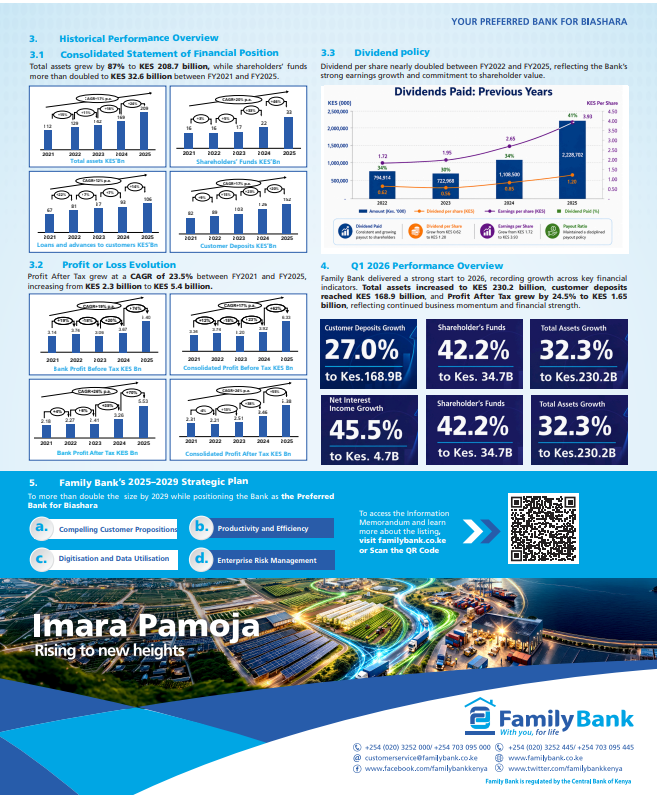

Family Bank has received CMA approval to list by introduction on the NSE Main Investment Market Segment, with trading expected to begin on 23 June 2026.

— The bank will list up to 1.66B issued and fully paid-up ordinary shares at a reference price of KES 18.00 per share.

— Family Bank had total assets of KES 208.7B and deposits of KES 151.9B as at FY2025, serving 1.3M+ customers through 96 branches across 32 counties.

— FY2025 profit after tax rose to KES 5.3B, up from KES 2.4B in FY2021, while total assets grew from KES 113.1B to KES 208.7B over the same period.

— Q1 2026 momentum remained strong, with assets up 32.3% to KES 230.2B, customer deposits up 27.0% to KES 168.9B, shareholders’ funds up 42.2% to KES 34.7B, and net interest income up 45.5% to KES 4.7B.

Kakuzi avocado sales rose to KES 3.8B in 2025 from KES 3.1B in 2024, recovering strongly but still below the 2023 peak of KES 4.1B

— UK & Continental Europe remained the core market, accounting for KES 3.4B of 2025 avocado sales.

— Kenya contributed KES 382.2M, up from KES 314.4M in 2024.

— Since 2013, Kakuzi’s avocado sales have grown from KES 862.8M to KES 3.8B, reflecting the company’s long-term shift toward export-led avocado revenue.

Credit Bank has earmarked KES 1B in 2026 to support SME growth in Kenya through financing, trade finance, insurance, investment, payments and transactional banking solutions.

One beneficiary is Xana Kenya, a retail and healthcare company combining pharmacies, supermarkets and wholesale outlets, which plans to expand from 6 outlets to 12 by end-2026, 52 in 2027 and over 400 nationwide.

Parliament has invited public memoranda and hearings on four Bills:

—The Sovereign Wealth Fund Bill 2026,

—The Finance Bill 2026

—The Central Bank Amendment Bill 2026

—The KRA Amendment Bill 2026.

Written submissions are due by Monday, 8 June 2026 at 5:00 p.m., while public hearings will run across 13 counties from 2 to 8 June 2026.

Tax season wisdom from Ushuru:

Your side hustle may be a side hustle to you. To KRA, it's income.

Upwork, Fiverr, freelancing, consulting, and remote work earnings are generally taxable if you're a Kenyan tax resident. More information here: https://t.co/UT0JNYyF27

Equity Group’s 22nd AGM will be held on Wednesday, 24 June 2026 at 9:00 AM, with special business including approval to incorporate three insurance subsidiaries:

— A microinsurance company in Kenya under Equity Group Insurance Holdings Limited, with capital of KES 192.0M for share capital and operational expenses.

— A life insurance company in the Democratic Republic of Congo under Equity Group Insurance Holdings Limited, with capital of USD 12.0M for share capital and operational expenses.

— A general insurance company in the Democratic Republic of Congo under Equity Group Insurance Holdings Limited, with capital of USD 13.37M for share capital and operational expenses.

The resolutions also authorise the Board to complete all regulatory, shareholder, documentation, fee, and operational steps required to set up and run the three insurance businesses.

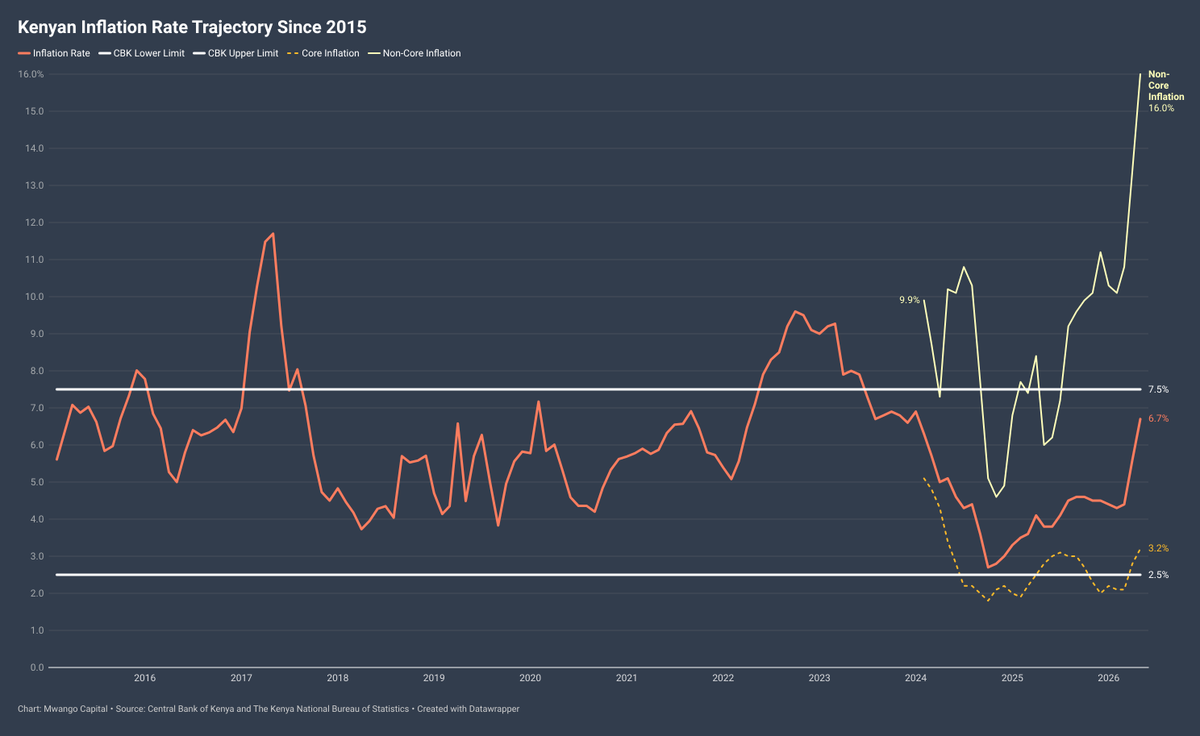

Kenya’s inflation rate rose sharply to 6.7% in May 2026, up from 5.6% in April and 3.8% a year earlier, marking the highest reading in over a year.

The acceleration was driven by a surge in transport costs, with transport inflation reaching 16.5%, alongside continued pressure from food prices, which rose 9.4% year-on-year.

Underlying pressures also intensified, with non-core inflation jumping to 16.0%, compared to 13.4% in April and 6.0% in May 2025, highlighting the growing impact of fuel and other volatile costs.

FYI:

—TotalEnergies Kenya operates 28 EV charging and battery-swapping units for two-wheelers and 2 EV charging units for four-wheel vehicles as of 2025.

—The network is supported by partnerships with Ampersand, Roam and Arc Ride, using TotalEnergies Kenya’s service stations to provide charging and swapping access for electric motorbikes and EVs

Today at 11 am, Co-op Bank is hosting a free webinar on digitizing businesses for the digital age.

Come learn how businesses can streamline operations, reach more customers, and build resilience for growth through digital tools.

Register here: https://t.co/rXnhZI3kwm

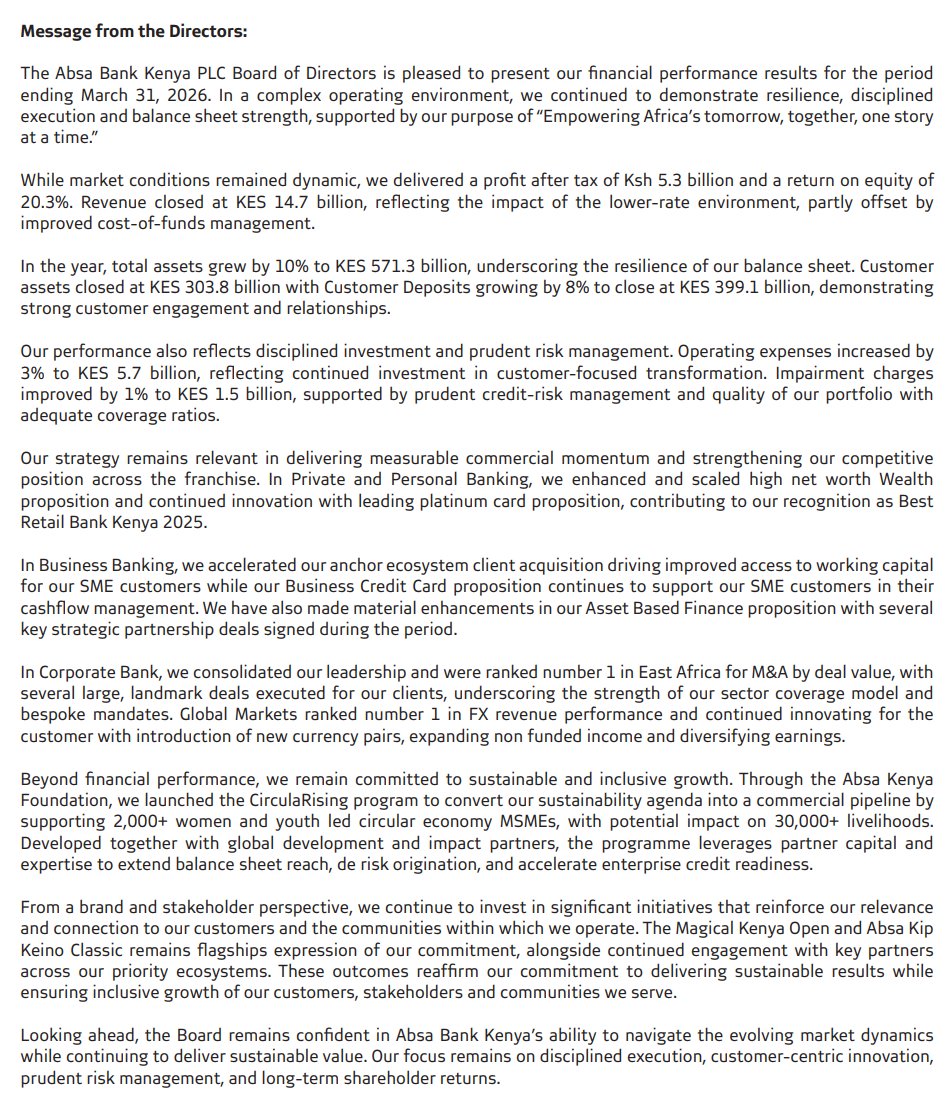

Absa Kenya Q1 Management Commentary:

—Management said revenue closed at 14.7B, reflecting the impact of the lower-rate environment, partly offset by improved cost-of-funds management.

—Customer assets closed at 303.8B, while customer deposits rose 8% to 399.1B, which management linked to stronger customer engagement and relationships.

—Operating expenses increased 3% to 5.7B, driven by continued investment in customer-focused transformation.

—Impairment charges improved by 1% to 1.5B, supported by prudent credit-risk management and adequate coverage ratios.

—Private and Personal Banking scaled the high-net-worth wealth proposition and continued innovation around the platinum card proposition.

—Corporate Banking ranked number one in East Africa for M&A by deal value, while Global Markets ranked number one in FX revenue performance.

Credit Bank Q1 26 Results [KES, YoY]:

—Total Assets: +7.8% to 28.47B

—Customer Deposits: +18.4% to 22.91B

—Total Interest Income: -34.4% to 766.1M

—Net Interest Income: -55.4% to 260.2M

—Net Loans & Advances: -6.6% to 15.87B

—Total Operating Income: -44.6% to 359.0M

—Non-Funded Income: +50.2% to 98.8M

—Loan Loss Provisions: -99.8% to 0.5M

—Total Operating Expenses: -34.0% to 387.1M

—Profit Before Tax: -28.1M [62.0M]

—Profit After Tax: -28.1M [62.0M]

—Total Equity: +0.9% to 3.10B

—Gross NPLs: +19.6% to 16.48B

Summary: Credit Bank slipped into a Q1 2026 loss of 28.1M from a 62.0M profit a year earlier, as net interest income fell 55.4% to 260.2M and total operating income declined 44.6% to 359.0M, despite a 50.2% rise in non-funded income to 98.8M.

The balance sheet expanded modestly, with total assets up 7.8% to 28.47B and customer deposits rising 18.4% to 22.91B, but net loans fell 6.6% to 15.87B while gross NPLs rose 19.6% to 16.48B.

![MwangoCapital's tweet photo. Credit Bank Q1 26 Results [KES, YoY]:

—Total Assets: +7.8% to 28.47B

—Customer Deposits: +18.4% to 22.91B

—Total Interest Income: -34.4% to 766.1M

—Net Interest Income: -55.4% to 260.2M

—Net Loans & Advances: -6.6% to 15.87B

—Total Operating Income: -44.6% to 359.0M

—Non-Funded Income: +50.2% to 98.8M

—Loan Loss Provisions: -99.8% to 0.5M

—Total Operating Expenses: -34.0% to 387.1M

—Profit Before Tax: -28.1M [62.0M]

—Profit After Tax: -28.1M [62.0M]

—Total Equity: +0.9% to 3.10B

—Gross NPLs: +19.6% to 16.48B

Summary: Credit Bank slipped into a Q1 2026 loss of 28.1M from a 62.0M profit a year earlier, as net interest income fell 55.4% to 260.2M and total operating income declined 44.6% to 359.0M, despite a 50.2% rise in non-funded income to 98.8M.

The balance sheet expanded modestly, with total assets up 7.8% to 28.47B and customer deposits rising 18.4% to 22.91B, but net loans fell 6.6% to 15.87B while gross NPLs rose 19.6% to 16.48B.](https://pbs.twimg.com/media/HJeFzl8bUAAe8Qg.jpg)

![MwangoCapital's tweet photo. Sasini H1 2026 Results [KES, YoY]

— Revenue: +1.7% to 3.01B

— Gross profit: +8.2% to 617.0M

— Operating loss: 214.8M [H1 25: 107.5M loss]

— Net finance cost: +435.2% to 56.2M

— Net loss: 170.8M [H1 25: 113.1M loss]

— EPS: -0.75 [H1 25: -0.49]

— Total assets: +9.0% to 28.27B

— Cash balance: -79.9% to 112.1M

— No interim dividend](https://pbs.twimg.com/media/HJg5UoMawAAWpQm.jpg)

![MwangoCapital's tweet photo. Credit Bank Q1 26 Results [KES, YoY]:

—Total Assets: +7.8% to 28.47B

—Customer Deposits: +18.4% to 22.91B

—Total Interest Income: -34.4% to 766.1M

—Net Interest Income: -55.4% to 260.2M

—Net Loans & Advances: -6.6% to 15.87B

—Total Operating Income: -44.6% to 359.0M

—Non-Funded Income: +50.2% to 98.8M

—Loan Loss Provisions: -99.8% to 0.5M

—Total Operating Expenses: -34.0% to 387.1M

—Profit Before Tax: -28.1M [62.0M]

—Profit After Tax: -28.1M [62.0M]

—Total Equity: +0.9% to 3.10B

—Gross NPLs: +19.6% to 16.48B

Summary: Credit Bank slipped into a Q1 2026 loss of 28.1M from a 62.0M profit a year earlier, as net interest income fell 55.4% to 260.2M and total operating income declined 44.6% to 359.0M, despite a 50.2% rise in non-funded income to 98.8M.

The balance sheet expanded modestly, with total assets up 7.8% to 28.47B and customer deposits rising 18.4% to 22.91B, but net loans fell 6.6% to 15.87B while gross NPLs rose 19.6% to 16.48B.](https://pbs.twimg.com/media/HJeFzzwagAALu0Z.jpg)