June is National Homeownership Month, a reminder that preparing financially before buying a home can make a major difference long term. Building savings, managing debt, and understanding your budget are important steps toward sustainable homeownership.

A new @WSJ report by @djfroschWSJ highlights a trend NFCC has been tracking: more households are relying on credit cards to cover everyday expenses.

As inflation and interest rates continue to pressure budgets, many families are turning to credit just to make ends meet.

The average American carries $6,523 in credit card debt — and at a 21% APR, that could mean more than $1,300 a year in interest alone.

High-interest debt can create long-term financial stress, but there are options that may help.

Read more: https://t.co/2LSwxM9exE

Financial stress is continuing to rise for many Americans.

In a recent @CNBC article, NFCC’s Bruce McClary shared insight on how debt management plans can help consumers regain control and move forward with a plan.

Read the article here: https://t.co/MY8VybU5yW

@KAMARONMCNAIR

A credit freeze is one of the easiest ways to help protect yourself from identity theft and credit fraud. It’s free, can be turned on or off at any time, and may help prevent criminals from opening accounts in your name.

Learn more: https://t.co/ZNseBsRlv8

NFCC's Bruce McClary recently joined ABC7/WJLA in Washington, D.C. to discuss the growing reliance on credit cards and what these debt trends may signal for consumers moving forward.

Watch the interview: https://t.co/puXoLtXOse

@MClarke7News@BruceMcclary

Bruce McClary of NFCC shared in a recent Consumers' Checkbookarticle, nonprofit credit counseling can help consumers review their options, navigate the collection process, and regain financial control.

Read more: https://t.co/c3gXg0B25v

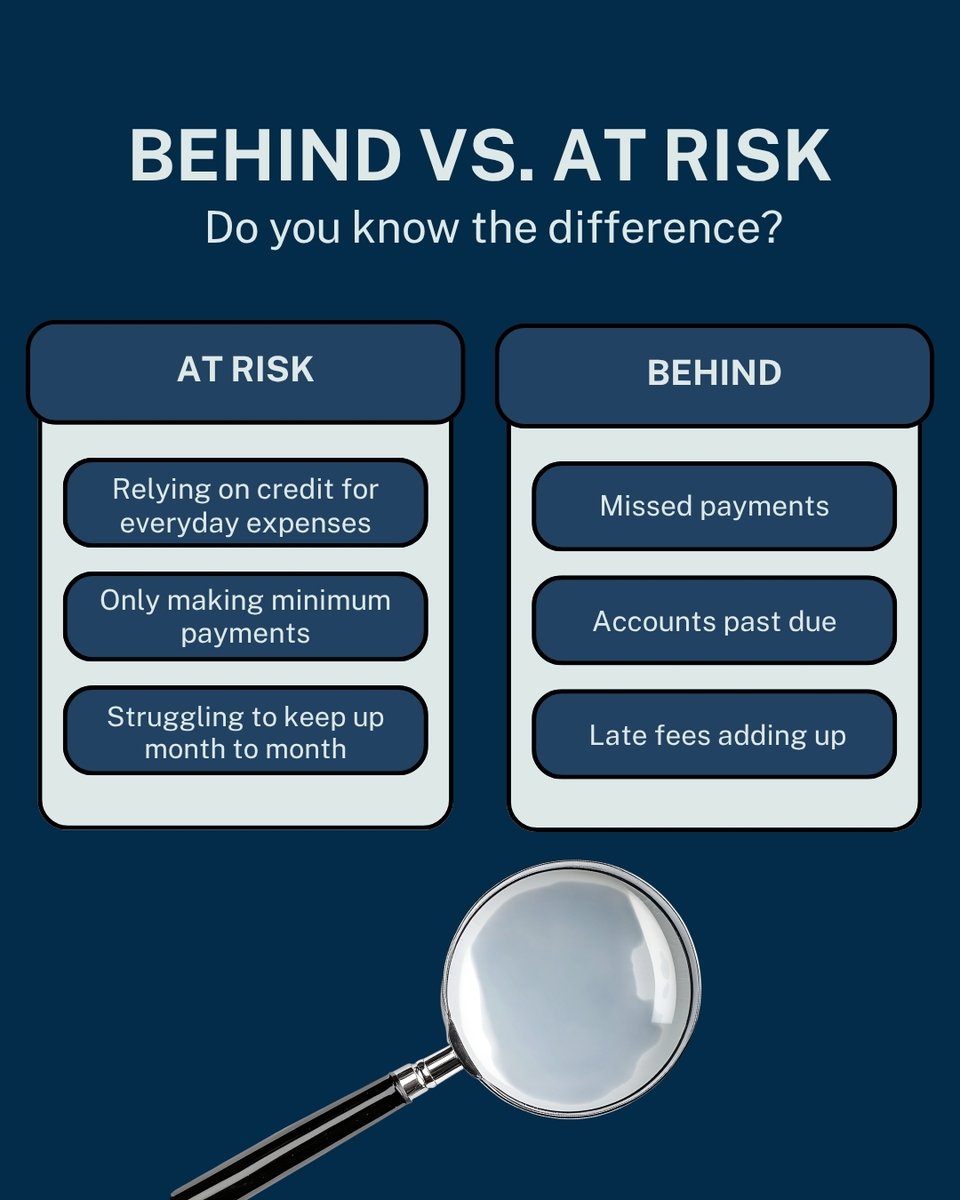

There’s a difference between being behind on payments and being at risk of falling behind. Recognizing the early warning signs, like relying on credit to cover essentials or missing due dates, can help you take action before things escalate. Do you know the signs to look for?

If you’re feeling overwhelmed by debt, you’re not alone, and there are options available. Starting with a clear understanding of your income, expenses, and balances can help you take the first step forward.

Are you ready to take that first step? We're here when you are!

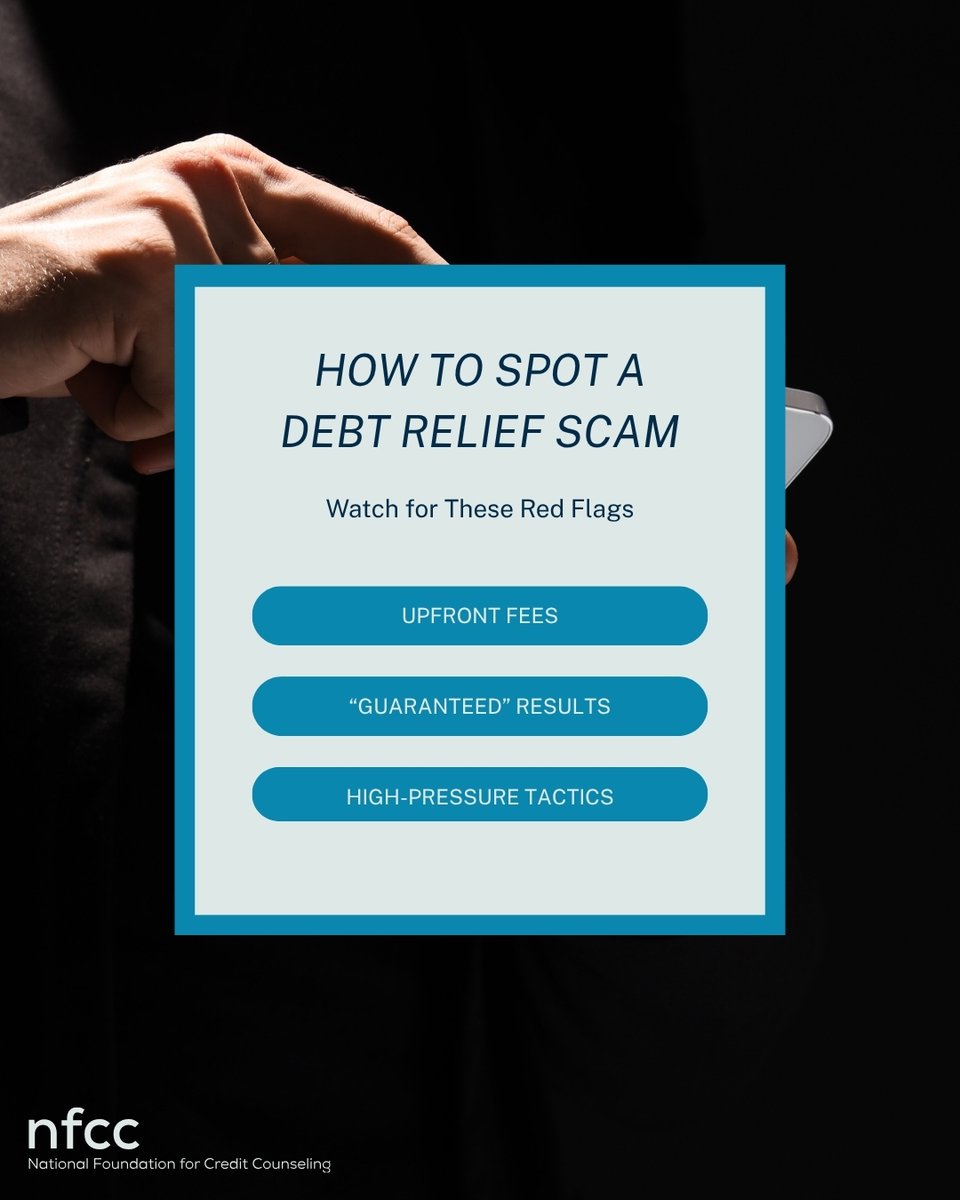

Not all debt relief offers are what they seem. Be cautious of companies that promise to eliminate debt quickly, ask for large upfront fees, or pressure you to act immediately. Taking time to understand your options can help you avoid costly mistakes.

#debtrelief#financialscam

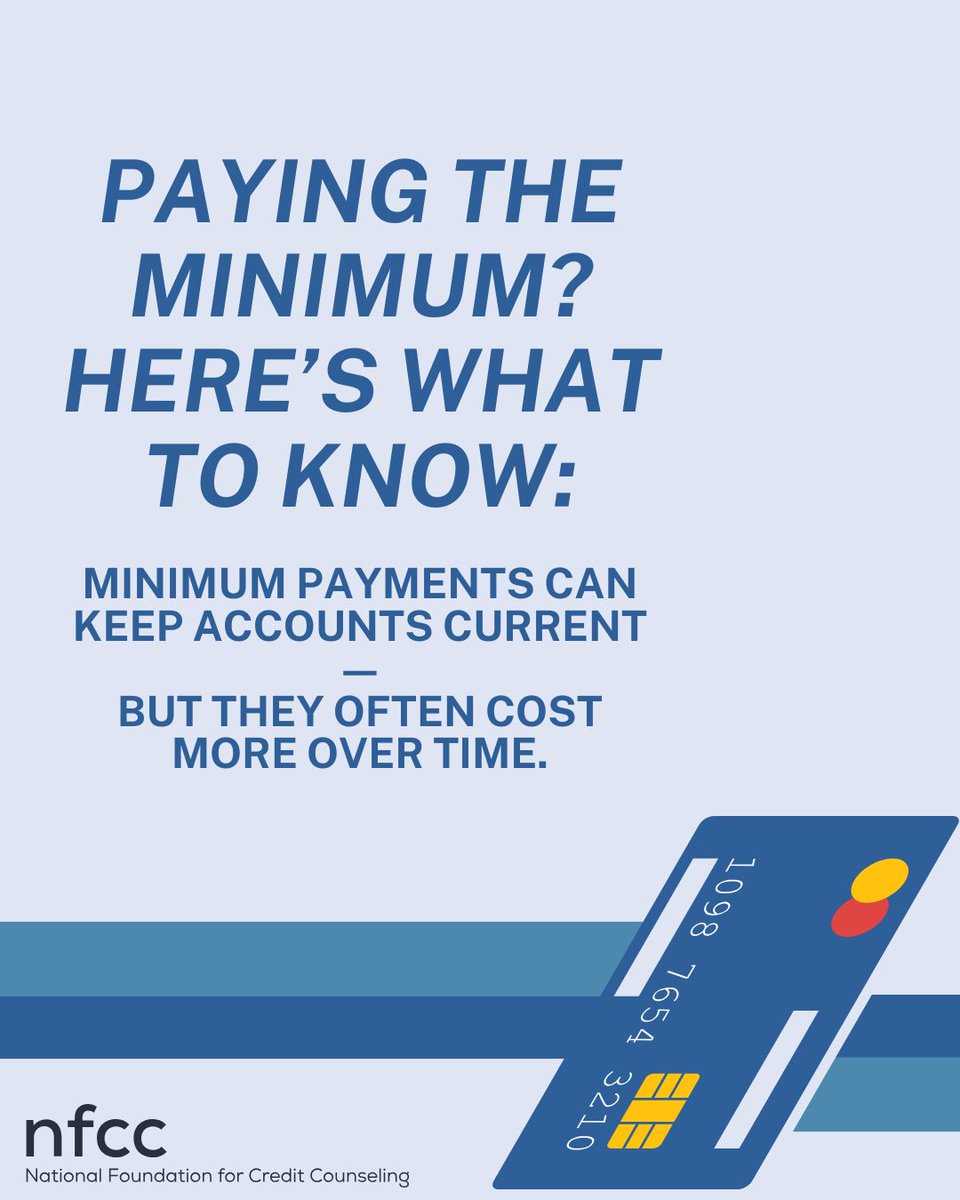

Minimum payments can keep your account in good standing, but they often extend the life of your debt and increase the total cost over time. If you’re only paying the minimum each month, it may be time to explore strategies to pay down balances more efficiently.

Financial stress affects more than just your bank account. For many households, debt can create anxiety, disrupt sleep, and make it harder to focus on everyday responsibilities. Taking the first step toward addressing debt can help restore both financial and emotional stability!

A budget is more than a list of numbers. It is a tool that helps consumers better understand spending patterns and plan for future financial goals. Regularly reviewing income and expenses can provide greater financial clarity and help support stronger decision making over time.

Spring cleaning isn’t just for your home, it’s a great time to reset your finances, too. Small changes now can lead to stronger financial habits year-round.

Looking for guidance? Connect with NFCC to find trusted credit counseling near you: https://t.co/8sDkpSf29N

Synchrony has announced a $2 million commitment to the Empowering Financial Futures program, and we’re proud to be a nonprofit partner in this important work.

Thanks to them for all they do.

@synchrony

How much of your available credit you’re using—known as credit utilization—can play a major role in your credit score. High credit card balances can lower your score and make borrowing more expensive over time. Managing balances and keeping utilization low can help.

#NFCC

Financial stress affects more than just your bank account. For many households, debt can create anxiety, disrupt sleep, and make it harder to focus on everyday responsibilities. Taking the first step toward addressing debt can help restore both financial and emotional stability!