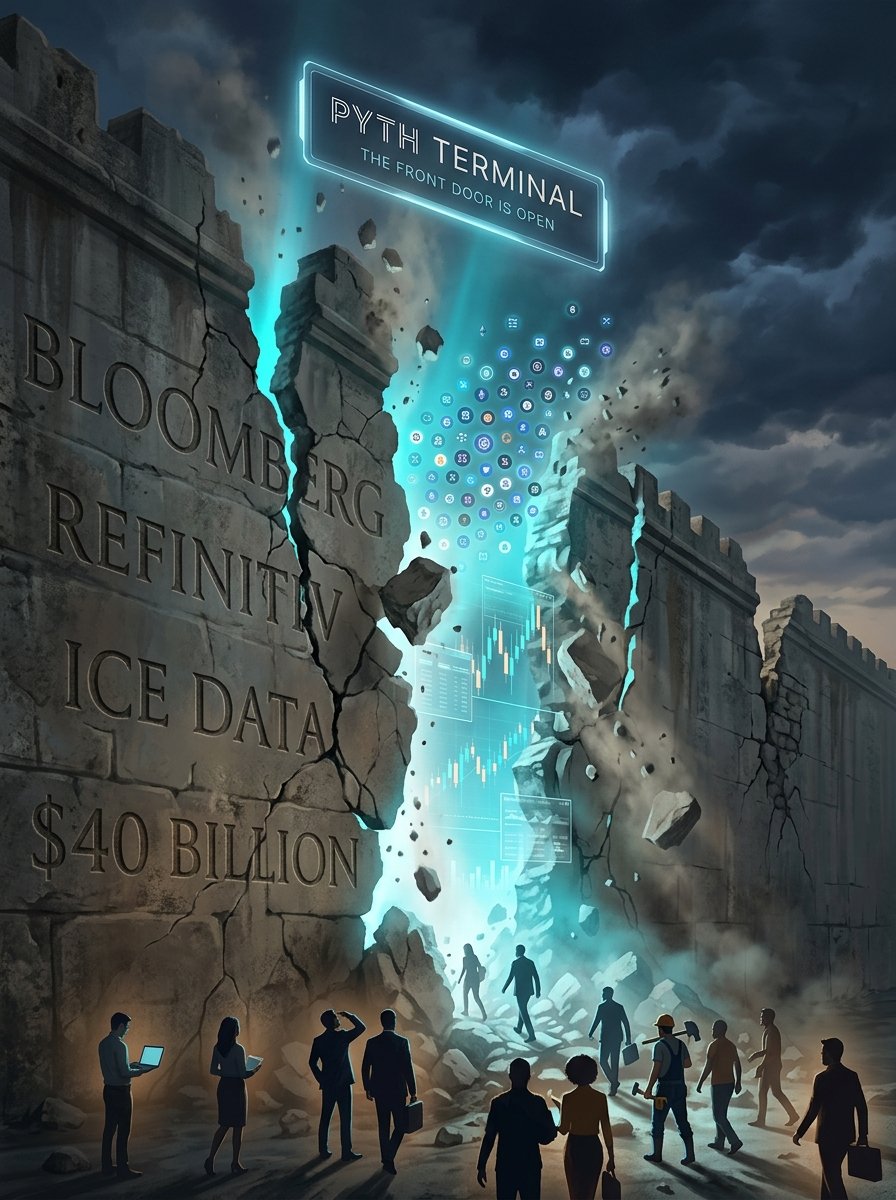

Bloomberg generates approximately $13 billion per year selling access to data behind a wall.

Pyth just put the same data on a public website with live charts, publisher-level transparency, and a free tier.

I've spent the last week thinking about how to frame this for people who don't follow financial infrastructure closely, and I keep coming back to the same observation. We are watching, in real time, the moment a $40 billion industry's pricing model becomes structurally indefensible.

Let me spell out exactly what just happened.

For 40 years the market data industry operated on three assumptions. First, that aggregating institutional pricing data required massive capital expenditure on exchange licensing, technology infrastructure, and global compliance, which justified high enterprise pricing. Second, that buyers wouldn't or couldn't evaluate the product before purchase, which justified opaque sales processes. Third, that switching costs were high enough that even mediocre data products could retain customers through inertia, which justified annual price increases without proportional product improvement.

The Pyth Terminal undermines all three assumptions in a single product launch.

It undermines the first assumption because the cost structure of onchain first-party data is fundamentally lower than legacy aggregation. Publishers like Jane Street, Cboe, Jump, Two Sigma, and Virtu push their prices directly. There's no aggregator layer. There's no third-party node operator. The cost per feed scales radically better than legacy infrastructure.

It undermines the second assumption because the product is fully visible before purchase. You can verify the data quality, audit the construction logic, and stress test the system before paying anything. The information asymmetry that justified opaque pricing is gone.

It undermines the third assumption because the integration is API-based rather than terminal-application based. Switching costs are dramatically lower for any developer team that's willing to point their data calls at a different endpoint. Lock-in via proprietary keyboard, proprietary chat, and proprietary workflows doesn't apply when the customer is a smart contract or a quant model rather than a human trader sitting at a desk.

Three structural advantages stacked on top of each other. Each one is enough to chip at the incumbent. All three combined is the kind of compound disruption that reshapes categories.

The Pyth Terminal is not going to kill Bloomberg in 2026. Bloomberg has 40 years of accumulated workflow integrations, institutional relationships, regulatory positioning, and brand trust that won't unwind in a year or even five. The terminal application itself is a real product with real value for human traders who spend their days inside it.

But Pyth doesn't need to kill Bloomberg. Pyth needs to capture the next decade of new builders, new protocols, new fintechs, and new use cases that never had a Bloomberg seat in the first place and never will. Every onchain prediction market. Every crypto-native perp DEX. Every multi-asset structured product on a blockchain. Every fintech startup that needs institutional pricing without institutional cost. Every quant team that can finally backtest exotic strategies without negotiating individual data licenses.

That's where the future revenue of financial data is going. Not at Bloomberg's installed base. At the next generation of products that are getting built right now, on top of self-serve infrastructure, by developers who never had access to the legacy stack in the first place.

The Terminal is how Pyth captures that generation. By giving them a front door. By letting them see the product before paying for it. By treating builders the way every other software category has treated builders for the last 20 years.

The walls cracked. Walk through.

3,000+ feeds. Crypto, equities, FX, commodities, metals. Live publisher transparency. Free tier. Public pricing. https://t.co/xy9zN4ixxP.

The next decade of financial infrastructure is going to look very different from the last one. We just saw the front door open.

Most people will read this and scroll past. A small number will open the Terminal, click around, and start building things that didn't exist last week.

Which one are you. @PythNetwork

There's a single phrase Pyth keeps using in their messaging and I want to spend a few minutes explaining why it matters more than most people are reading into it.

"The price of everything is coming onchain. One feed at a time."

On the surface this sounds like marketing copy. It is not. It's a mission statement, and it's one of the most ambitious statements any infrastructure project in crypto has made in years.

Let me unpack what "everything" actually means in the context of global financial markets.

There are roughly 200,000 actively priced instruments in the global financial system. Every equity on every major exchange. Every government bond on every issuer. Every corporate bond with active secondary trading. Every major FX pair and cross. Every commodity futures contract on every major exchange. Every meaningful ETF. Every major REIT. Every active derivative on any of the above. Every cryptocurrency with non-trivial liquidity.

Add to that the long tail: private equity valuations, real estate price indices, art market estimates, intellectual property valuations, carbon credit prices, weather derivatives, freight rates, electricity prices by grid region, water rights, and dozens of other markets that price continuously somewhere but don't show up in retail data products.

Total addressable price feed universe: roughly 200,000 to 500,000 instruments depending on how you count.

Pyth Pro currently has 3,000. That's roughly 1% of the addressable universe.

Now here's the part that should reshape how you think about this project. The growth rate is not linear. Pyth shipped 1,000 feeds by early 2025 and tripled the catalog in about 15 months. New feeds are launching weekly. Each new asset class added (livestock last week, energy a few months ago, equities earlier this year) opens an entire new category that gets densely populated within 6 to 12 months.

If the cadence continues, Pyth Pro reaches 10,000 feeds within 18 months, 30,000 within 4 years, and approaches the full addressable universe sometime in the next decade.

That timeline sounds long until you realize what that endpoint actually means. It means a single onchain endpoint, accessible to any developer, anywhere, with no enterprise contracts, that returns institutional-grade pricing for every meaningful financial instrument that humans trade. With first-party publishers. With confidence intervals. With cryptographic verifiability. At a fraction of the cost of any legacy data vendor.

That is not an oracle. That is the global pricing layer.

If Pyth executes this mission to even 30% completion in the next decade, the entire architecture of how the world prices assets shifts. Every fintech, every neobank, every retail brokerage, every DeFi protocol, every quantitative fund, every pricing-dependent application in any vertical becomes a potential downstream consumer of a single onchain endpoint.

That's a $40 billion industry being slowly reorganized around a single piece of infrastructure. Not in months. Over years. Quietly. One asset class at a time.

Last week the asset class was livestock and softs. Next week it'll be something else. The week after, something else again.

Most of crypto is still trying to figure out which token will pump in the next 30 days. @PythNetwork

Pyth is building the pricing layer for the next 30 years.

Watch what gets shipped. Count what gets added. The thesis is in the cadence.

The price of everything is coming onchain. Live cattle was just one feed in a very long list.

Season 1 is in full swing, and there's still over 6M $BCN up for grabs🫡

Haven't started yet? Now's the time!

Get 30% off Premium for the next 48 hours, jump right in, and start getting rewards.

Play now! 👇

https://t.co/2nlOshswVk

Season 1 is just getting warmed up! 🧙♂️

Week 2 is here, Zone 2 is open, and over 7M $BCN still on the table.

The dungeon isn't going to clear itself! ⚔️

https://t.co/2ux4vZxhp9

There's a single phrase Pyth keeps using in their messaging and I want to spend a few minutes explaining why it matters more than most people are reading into it.

"The price of everything is coming onchain. One feed at a time."

On the surface this sounds like marketing copy. It is not. It's a mission statement, and it's one of the most ambitious statements any infrastructure project in crypto has made in years.

Let me unpack what "everything" actually means in the context of global financial markets.

There are roughly 200,000 actively priced instruments in the global financial system. Every equity on every major exchange. Every government bond on every issuer. Every corporate bond with active secondary trading. Every major FX pair and cross. Every commodity futures contract on every major exchange. Every meaningful ETF. Every major REIT. Every active derivative on any of the above. Every cryptocurrency with non-trivial liquidity.

Add to that the long tail: private equity valuations, real estate price indices, art market estimates, intellectual property valuations, carbon credit prices, weather derivatives, freight rates, electricity prices by grid region, water rights, and dozens of other markets that price continuously somewhere but don't show up in retail data products.

Total addressable price feed universe: roughly 200,000 to 500,000 instruments depending on how you count.

Pyth Pro currently has 3,000. That's roughly 1% of the addressable universe.

Now here's the part that should reshape how you think about this project. The growth rate is not linear. Pyth shipped 1,000 feeds by early 2025 and tripled the catalog in about 15 months. New feeds are launching weekly. Each new asset class added (livestock last week, energy a few months ago, equities earlier this year) opens an entire new category that gets densely populated within 6 to 12 months.

If the cadence continues, Pyth Pro reaches 10,000 feeds within 18 months, 30,000 within 4 years, and approaches the full addressable universe sometime in the next decade.

That timeline sounds long until you realize what that endpoint actually means. It means a single onchain endpoint, accessible to any developer, anywhere, with no enterprise contracts, that returns institutional-grade pricing for every meaningful financial instrument that humans trade. With first-party publishers. With confidence intervals. With cryptographic verifiability. At a fraction of the cost of any legacy data vendor.

That is not an oracle. That is the global pricing layer.

If Pyth executes this mission to even 30% completion in the next decade, the entire architecture of how the world prices assets shifts. Every fintech, every neobank, every retail brokerage, every DeFi protocol, every quantitative fund, every pricing-dependent application in any vertical becomes a potential downstream consumer of a single onchain endpoint.

That's a $40 billion industry being slowly reorganized around a single piece of infrastructure. Not in months. Over years. Quietly. One asset class at a time.

Last week the asset class was livestock and softs. Next week it'll be something else. The week after, something else again.

Most of crypto is still trying to figure out which token will pump in the next 30 days. @PythNetwork

Pyth is building the pricing layer for the next 30 years.

Watch what gets shipped. Count what gets added. The thesis is in the cadence.

The price of everything is coming onchain. Live cattle was just one feed in a very long list.

the largest token unlock in Pyth's history just happened on May 19. 2.13 billion PYTH. roughly $94 million in fresh supply. 36.96% of the entire circulating supply hitting the market in a single cliff release.

if the protocol had nothing under it, this is the kind of unlock that ends projects.

i've watched dozens of L1s, L2s, and DeFi protocols get unwound by exactly this scenario. team unlock hits, market wasn't pricing it in cleanly, sell pressure overwhelms organic demand, chart goes vertical down, narrative dies with the price, community moves on. you can map the exact moment when most failed projects in 2024 and 2025 got terminal damage and it's usually a major unlock during a weak market.

and yet, in the same month Pyth absorbed this unlock, the following happened:

on May 22, three days after the unlock, the protocol had a five-hour outage that paused half of DeFi on multiple chains. the post-incident reaction wasn't migration away from Pyth. it was a wave of teams publicly committing to keep using it because nothing else gives them institutional-grade first-party data at sub-second latency.

last month, Polymarket integrated Pyth Pro as the resolution source for traditional asset prediction markets. Apple, NVIDIA, gold, silver, stock indices — all now resolve through Pyth feeds. that's a multi-year structural revenue contract from one of the largest prediction markets in the world.

in April, Pyth launched its Data Marketplace with major financial institutions. the same trading firms that publish prices are now structurally positioned to monetize that data through the marketplace, with revenue flowing back to the protocol.

OIS emissions ended on April 22. weekly emissions of roughly 1.93M PYTH that had been hitting the market for the entire history of the token went to zero, removing structural sell pressure on top of the buyback flow from the DAO Reserve.

500 price feeds. 100+ blockchains. 120+ data publishers including Jane Street, Cboe, Jump Trading, Two Sigma, and Virtu Financial. Cardano shipped with Pyth pre-integrated in December.

and the chart is still trading near range lows.

think about that for a second. this is a protocol that has absorbed the largest unlock in its history, survived its biggest outage, ended its emissions program, signed its largest integration deal, launched a new revenue product, and the price barely moves either direction. that's not weakness. that's a market that has stopped caring about news and is waiting for something else.

the unlock was the loudest bearish event of the year. it's still not enough to bend the structural thesis. that tells you something important about what's actually compressing under the chart.

most tokens get unwound by their unlocks. some absorb them.

a smaller number absorb them and then quietly start a new leg up six to nine months later because the structural buyer (in this case the protocol itself, via revenue-funded buybacks) keeps showing up every single month with cash flow from real customers.

watch which bucket Pyth ends up in. the only signal that matters now is whether revenue keeps growing month over month. if it does, the unlock becomes a footnote. if it doesn't, the bears were right.

i've made my pick. integration count goes up. publisher count goes up. revenue lines keep expanding. that's the trade.

the rest is noise.

the largest token unlock in Pyth's history just happened on May 19. 2.13 billion PYTH. roughly $94 million in fresh supply. 36.96% of the entire circulating supply hitting the market in a single cliff release.

if the protocol had nothing under it, this is the kind of unlock that ends projects.

i've watched dozens of L1s, L2s, and DeFi protocols get unwound by exactly this scenario. team unlock hits, market wasn't pricing it in cleanly, sell pressure overwhelms organic demand, chart goes vertical down, narrative dies with the price, community moves on. you can map the exact moment when most failed projects in 2024 and 2025 got terminal damage and it's usually a major unlock during a weak market.

and yet, in the same month Pyth absorbed this unlock, the following happened:

on May 22, three days after the unlock, the protocol had a five-hour outage that paused half of DeFi on multiple chains. the post-incident reaction wasn't migration away from Pyth. it was a wave of teams publicly committing to keep using it because nothing else gives them institutional-grade first-party data at sub-second latency.

last month, Polymarket integrated Pyth Pro as the resolution source for traditional asset prediction markets. Apple, NVIDIA, gold, silver, stock indices — all now resolve through Pyth feeds. that's a multi-year structural revenue contract from one of the largest prediction markets in the world.

in April, Pyth launched its Data Marketplace with major financial institutions. the same trading firms that publish prices are now structurally positioned to monetize that data through the marketplace, with revenue flowing back to the protocol.

OIS emissions ended on April 22. weekly emissions of roughly 1.93M PYTH that had been hitting the market for the entire history of the token went to zero, removing structural sell pressure on top of the buyback flow from the DAO Reserve.

500 price feeds. 100+ blockchains. 120+ data publishers including Jane Street, Cboe, Jump Trading, Two Sigma, and Virtu Financial. Cardano shipped with Pyth pre-integrated in December.

and the chart is still trading near range lows.

think about that for a second. this is a protocol that has absorbed the largest unlock in its history, survived its biggest outage, ended its emissions program, signed its largest integration deal, launched a new revenue product, and the price barely moves either direction. that's not weakness. that's a market that has stopped caring about news and is waiting for something else.

the unlock was the loudest bearish event of the year. it's still not enough to bend the structural thesis. that tells you something important about what's actually compressing under the chart.

most tokens get unwound by their unlocks. some absorb them.

a smaller number absorb them and then quietly start a new leg up six to nine months later because the structural buyer (in this case the protocol itself, via revenue-funded buybacks) keeps showing up every single month with cash flow from real customers.

watch which bucket Pyth ends up in. the only signal that matters now is whether revenue keeps growing month over month. if it does, the unlock becomes a footnote. if it doesn't, the bears were right.

i've made my pick. integration count goes up. publisher count goes up. revenue lines keep expanding. that's the trade.

the rest is noise.

@clithecreator What's the bear case for commodity DeFi, why hasn't this category taken off in previous cycles despite the same infrastructure being available?