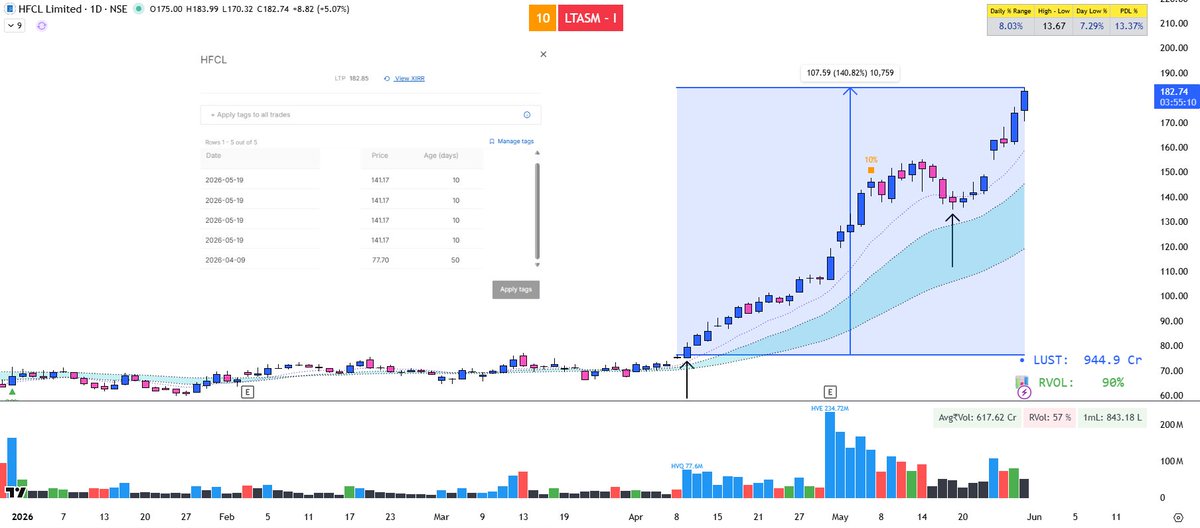

BEST TRADE OF MY LIFE 🙌

I did not wanted to jinx it earlier, so did not post anything related to this

#HFCL completed 50 days in my PF and surpasses 140% from 1st entry (2nd entry on 19may)

Reason for the trade on 9th april - Sister stock trading (STLTECH was up 140% in leg1 and then HFCL received 10kcr OFC order)

Allow me to add another feather to your basket , and make trading more complex 😂

"Me neeche nahi jaaunga" - Denial to go down

- if a stocks denies to go down even after disappointing numbers and street pressure, there is a possibility something which will fold out in coming qtrs

Sharing more examples in thread

THREE reasons why our parent's didn't educate us about insurance.

They are religious/spiritual.

Being religious to many is leaving everything to the will of god. Sab kuch likha hain. Vidhi ka vidhaan. Jo hota hain so hota hain.

They lived in joint families:

The OG buffer. Multiple family members lived under one roof protecting each other, whenever something went wrong.

They were told insurance is money back:

LIC neighbors sold insurance as investment. Insurance ka matlab moneyback tha - so no conversations ever about loss, death, financial security etc, forget insuring them.

It's time.

It's time we change this for our children.

Speak to your kids, whatever their age - educate them about risk management, insurance - how it sounds counter intuitive, yet makes economic sense in the long term.

Health Insurance will be a necessary luxury in the next 10 years.

Premiums will continue to rise.

But insurance will be the only way to get continous access to top private hospitals,

We need to face two realities.

1. There is genuinely no replacement for health insurance yet, unless you are Ambani

2. To afford this luxury through old age, you need to build a separate fund. Just to pay the premiums.

Most people are not aware of the second one.

Here is the math.

A 30 year old couple with one child gets a Rs 1 Cr family floater for around Rs 30,000 a year today.

Premiums in India have been rising 10 to 15% every year.

Take 10% as a conservative average.

At 40, that Rs 30,000 becomes Rs 78,000.

At 50, around Rs 2 Lakhs.

At 65, around Rs 8.4 Lakhs.

At 75, around Rs 22 Lakhs a year.

For one cover.

Why are premiums rising this fast?

Because hospital bills are rising even faster.

There is a supply deficit for top quality hospitals that is going to drive costs up.

Exactly why PE funds have been investing aggressively in private hospital chains across India. And once a hospital becomes PE owned, the metric becomes revenue per bed. Bills go up.

Insurance pays those bills.

Premiums will have to rise to keep up.

Now here is the part most retirement plans miss.

The age you actually need health insurance the most, is the age your salary stops.

You retire at 60. Premium is Rs 5.2 Lakhs a year.

By 70, Rs 13.6 Lakhs.

By 75, Rs 22 Lakhs and rising every year after that.

Most retirement corpuses are built for groceries, rent, travel, weddings, helpers, taxes.

Health insurance premium sits as a tiny line item, often assumed to remain Rs 30,000 a year forever. It won't.

If you don't plan for premiums separately, two things tend to happen at 70.

Either you drop the cover.

Or you keep paying. And eat into your retirement corpus much faster than you planned.

This is why start keep a separate dedicated fund. Just for paying health insurance premiums after 60. Like a kid's education fund.

One of my jobs as a founder, is to give OTPs. Every single day.

For payments, for filing some returns, for logging into services that I had setup when we started.

How have other founders solved this?

Brands on your policy document are changing.

Until 2021, no foreign insurer could control an Indian insurance company.

Today, eight do.

By the end of next year, the count could hit thirteen.

Two rule changes did this.

In 2021, India raised the FDI cap from 49% to 74%.

In December 2025, the cap moved to 100%.

More foreign capital owns more of Indian insurance than ever before.

Here's what it means for you.

The brand on your policy is changing.

Allianz walked out of Bajaj Allianz last year. AXA sold its stake in Bharti AXA before that. Aegon Life is now Bandhan Life. Future Generali is now Generali Central. Reliance Nippon Life is now IndusInd Nippon Life. Reliance General is now IndusInd General. Six big logo swaps in two years. The name on your renewal notice in 2027 may not match the name you signed up with.

It's not entirely bad news, actually.

Foreign partners stuck at 26% or 49% had no real incentive to fix the Indian business. They couldn't run it. Now Prudential, Zurich, Generali, Sanlam, Bupa, Ageas, Aviva and QBE either own the majority or want to.

They've put real money on India working for them.

For a 30-year life or health policy, an owner who's all-in beats a partner stuck in a JV they hate.

But there will trade-offs too.

Foreign-controlled insurers will care about margins.

And we have seen horror stories around health insurance in the USA.

.

Understanding ownership of the company will be an important step in evaluating a long term insurance policy like health or term.

"Which health insurance policy is best?"

Wrong question. The right one is: "Which policy is best FOR YOU?"

We built TruMatch ,a free tool that matches you with the right health plan based on YOUR needs.

No sales pitch. Just honest recommendations.

Full breakdown 👇

#healthinsurance #podcast #healthcare #bestpolicy

Rs 48.5K cataract claim.

Rejected as fraud - without proof.

Stuck with the Ombudsman for ~10 months.

The case came through our Free Claim Helpdesk.

We reviewed the details, offered guidance.

The very next day - the insurer approved the claim.

Here’s what happened 👇

#claimhelpdesk #healthinsurance #insurance #justice

🚨A wife's insurance claim was denied after her husband’s death.

It wasn't a "fake" claim.

It wasn't "late" paperwork either.

But because the insurer thought something was hidden.

#ClaimStories S01E111👇

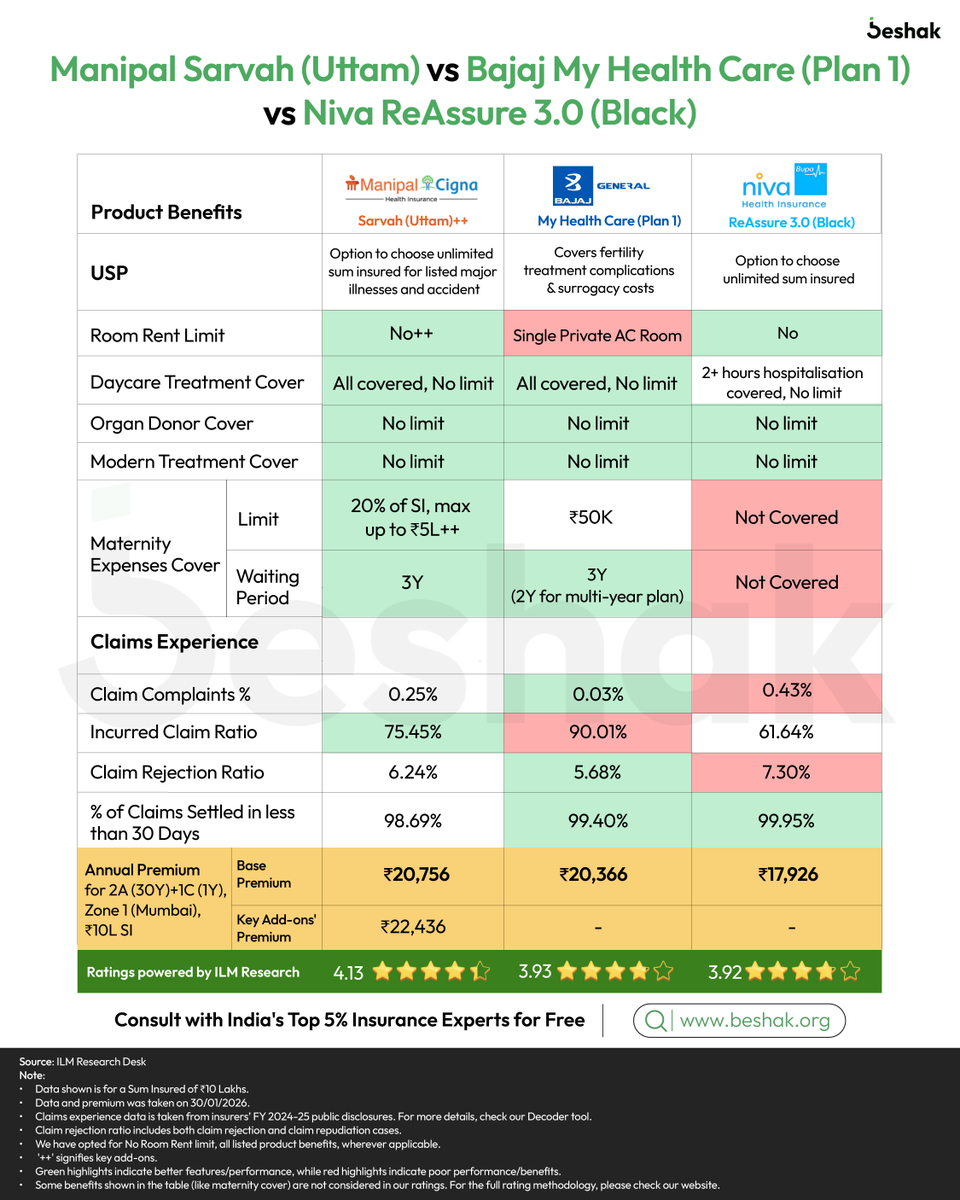

Another week, another decode

Here’s the simplest comparison of these 3 plans 👇

➡️ ManipalCigna Sarvah (Uttam)

➡️ Bajaj General My Health Care (Plan 1)

➡️ Niva Bupa ReAssure 3.0 (Black)

An unbiased comparison of unique features, key benefits, claims experience & premium - so you know exactly what you’re signing up for. 💡

⚠️ Note 1: The overall ratings you’ll see do not include premium ratings – affordability is personal, what’s expensive for one may be affordable for another.

⚠️ Note 2: Green marks the stronger and red marks the poor metric among these 3 plans only. In a full-market view, the highlight may change.

⚠️ Note 3: Ratings are based on multiple factors – check our Decoder tool for details.

⚠️ Note 4: This is a quick overview of a detailed comparison on our website. This should not be solely used to make decisions.

⚠️ Note 5: SI stands for Sum Insured, A stands for Adults, C stands for Child, and Y stands for Years.

⚠️ Note 6: Claims experience data is insurer-specific, not product-based.

#healthinsurance #policy #comparison #ratings #insurance #health

You can change your house.

You can change your job.

You can even change your government.

But your health insurance agent?

Innnsanely difficult.

Every 2nd day, we receive comments, DMs.

"What is the procedure to change my advisor"

Here's a quick take 👇

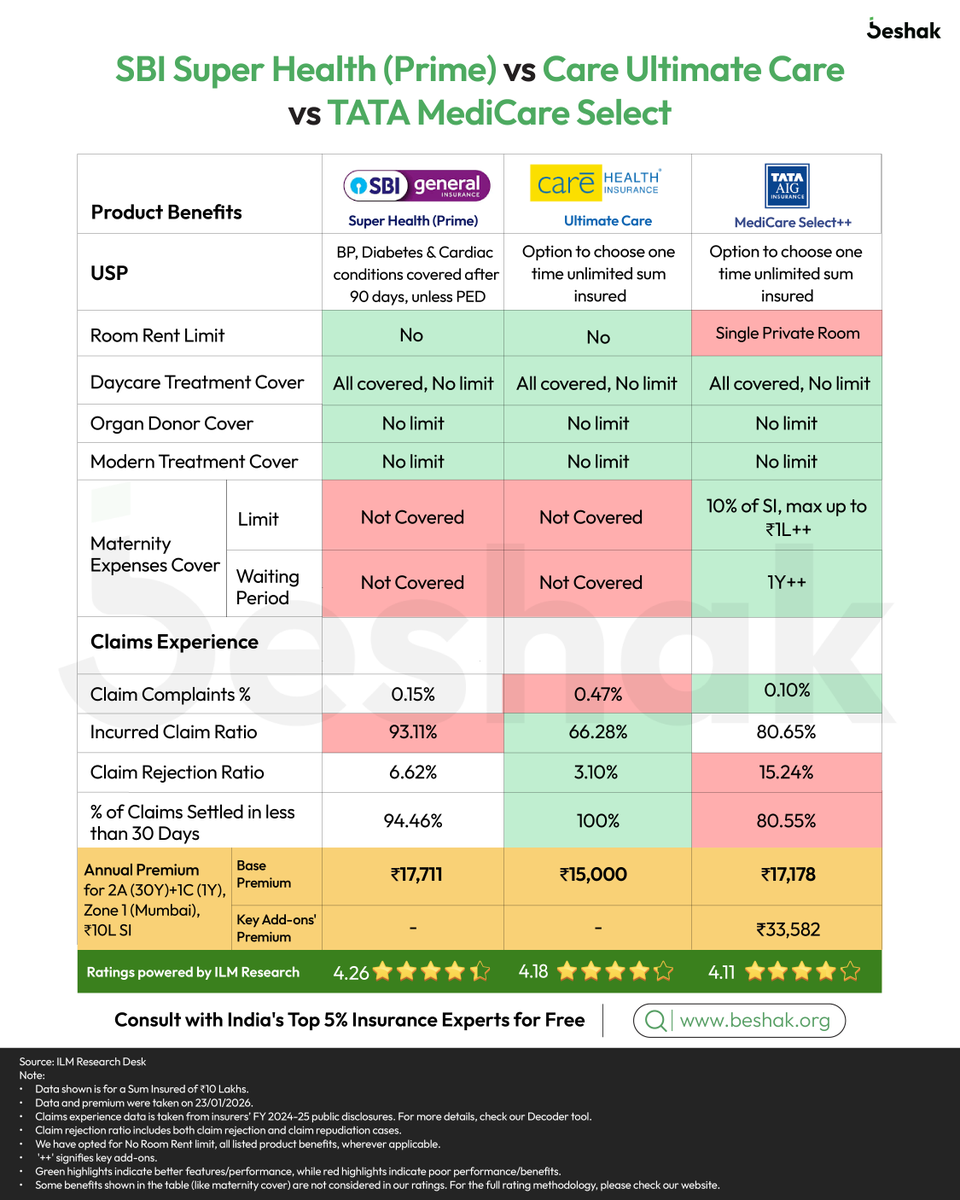

Another week, another decode

Here’s the simplest comparison of these 3 plans 👇

➡️ SBI General - Super Health (Prime)

➡️ Care Health - Ultimate Care

➡️ TATA AIG - MediCare Select

#healthinsurance#comparison#ILMratings#policyreview

I went to Croma to get service for an appliance I bought from Vijay Sales.

Insane right?

It's very clear - why will they serve you - if they didn't earn?

They will simply ask you to go directly to the manufacturer, right?

But we at Beshak have been doing this - without any fee for years now. Without fanfare.

So many DMs - same thing. I bought my policy from Policybazaar - can you help?

Maybe its about scale.

But the thing is we have grown 3.5x in the last one year, with the same team, but we haven't changed our stance.

And we intend to maintain this mission as much as we can.

"Help rebuild people's trust in insurance."

Thanks to everyone who has encouraged/supported us, so far.

Another week, another decode

Here’s the simplest comparison of these 3 plans 👇

➡️ Aditya Birla Activ One (NXT)

➡️ Niva Bupa Aspire (Titanium+)

➡️ Star Health Assure

#healthinsurance#comparison#reviews#ratings

🚨 Big news for govt employees covered under CGHS!

The Finance Ministry has just launched a new optional health insurance plan called Paripoorna Mediclaim Ayush Bima.

It’s designed to complement your existing CGHS benefits. Here’s the full scoop 👇

#newlaunch#healthinsurance #insuranceindia #cghs #news