AI doesn’t scale where capital flows.

It scales where power connects.

For nearly two decades, U.S. electricity demand was flat.

Now AI is forcing a step change.

But the system it’s hitting — transmission, interconnection, generation — was built for stability, not acceleration.

That creates a structural mismatch:

Demand moves fast.

Infrastructure moves slow.

That gap is where constraints form.

And once constraints show up, everything changes:

– pricing

– location decisions

– capital allocation

This is not a technology story.

It’s an infrastructure story.

I write The AI Grid Report where I break down:

– where capacity actually exists

– where bottlenecks are forming

– what it means for investors and operators

Read here →

https://t.co/LTn2mA17mj

@AndyMasley People love jumping on bandwagons, especially the press and politicians, and people who love the next great social justice cause. Governance needs to catch up.

New York passed the first statewide data-center moratorium in the US — one year, no new permits over 20 MW. ~9,700 MW and 28 projects freeze if Hochul signs.

Maine's governor vetoed a near-identical bill in April. Will Hochul?

I put a market on it. I think it's 40% she signs.

Click below - and maybe someone knows how to get this onto Kalshi..

https://t.co/760JGH3fGA

New York just sent Kathy Hochul something no governor has signed: a statewide pause on new data center permits.

The Responsible Data Center Development Act (S10642 / A11560) passed both houses last Thursday. It freezes new environmental permits for one year on any facility drawing 20 MW or more — but exempts renewals and anything already under construction.

So it does nothing to the in-progress pipeline. It freezes the next cohort. Every site that already holds approvals is sitting in a privileged position.

Hochul hasn’t committed. She’s up for re-election and the Building Trades are lobbying to kill it. Worth watching whose definition of “responsible” survives the summer.

That’s fair. Data centers, like fracking before them, have become a bandwagon for politicians to jump on. No doubt their social media teams, huge users of the AI tools these data centers host, have seen a rich target. I’m not sure Warren has ever seen a problem that taxation can’t solve.

I loved the talented structuring skills the Enron team deployed in their search for shareholder value. Mamdani’s pension contribution restructuring is inspired and, as WSJ pointed out today, owes a vote of thanks to the stock market success of recent years. I’m sure it will all workout well…

US data-center project rejections totaled 49 in all of 2025.

The first 5 months of 2026 produced 89.

AI infrastructure isn’t being stopped.

It’s being filtered.

By permitting. By politics. By utilities. By local resistance.

That changes: where projects land, how power gets priced, and which strategies survive.

New AIGR issue:

“Data Center Opposition Isn’t Stopping the Build. It’s Deciding Who Wins.”

Read here →

https://t.co/cx6TPnbMEQ

AI doesn’t hit one constraint.

It hits a stack.

Generation

Transmission

Interconnection

Equipment

Each layer moves at a different speed.

AI scales in years.

The grid scales in decades.

That gap doesn’t resolve.

It compounds.

Where does it break first?

👉 https://t.co/Ir7f1yELS4

Most people will frame the NextEra–Dominion deal as a utility merger.

It’s really one of the first major AI-era grid positioning acquisitions.

https://t.co/mr2yAq917i

The bottleneck is shifting from GPUs to deliverable electricity, transmission access, and regulated utility territory.

The AI stack is becoming physical.

America is not replacing the grid with the same kind of grid.

Coal has effectively disappeared from new-build attempts.

Solar + storage has become the national default.

But the regions are diverging sharply on one question:

How do you keep the system reliable after the sun goes down?

PJM still leans on gas and long-dated nuclear bets.

ERCOT is trying to firm renewable growth through storage.

CAISO and NYISO are building almost no meaningful new gas at all.

The same continent.

Different bets.

And underneath all of it:

The queue is not delivered power.

AIGR #8 breaks down what America is actually trying to build — and what the interconnection queues may already be revealing about the future shape of the US grid. Read here → https://t.co/8yiYiRN7gc

AI demand isn’t constrained.

Power is.

And that constraint is regional, not national.

Some grids can still absorb load.

Others are already saturated.

That’s what determines where AI actually gets built.

Where does it break first?

👉 Continue reading → https://t.co/K6CQ5ThDYg

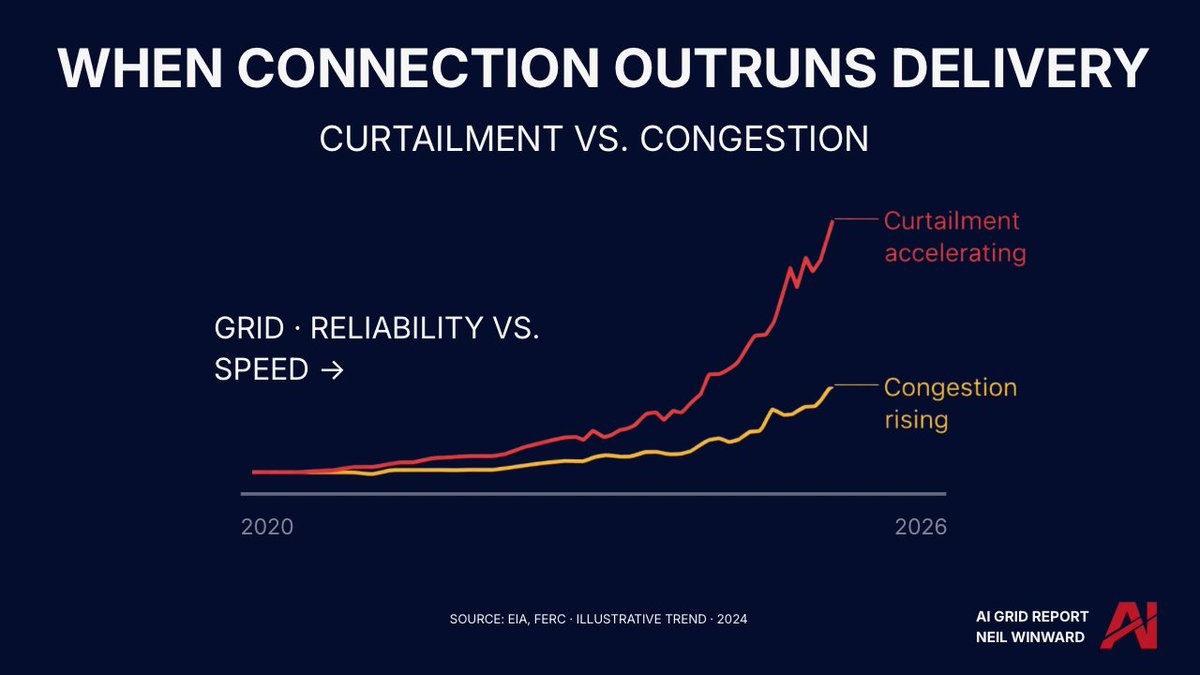

Connection doesn’t guarantee delivery.

As generation increases, curtailment and congestion rise—not because the system fails, but because it fills.

The constraint shifts from approvals to actual delivery. That’s where the stress shows up.

What would you rather your taxes fund - a luxury ballroom project or infrastructure for the AI economy?

That’s increasingly the real question underneath the transferable tax credit market.

Billions are quietly moving into power infrastructure, manufacturing, and grid expansion tied directly to AI-load growth and industrial bottlenecks.

Most investors still think these structures are “just tax strategy.”

They’re increasingly infrastructure capital allocation mechanisms.

→ https://t.co/8o19IvnEa8

The ERCOT queue isn’t just large. It’s complex. Storage, solar, gas, and wind all behave differently under load.

This is not just a function of volume. It is a coordination challenge within the system.

MISO’s problem is usually framed as an auction or pricing story, but the deeper issue is the retirement schedule itself.

Roughly 25 GW of generation is planned to leave the system over the coming years while AI-related load forecasts continue moving higher across the same footprint. The important detail is not simply how much capacity is retiring, but what kind of capacity is retiring.

Much of the scheduled retirement stack is coal and gas capacity built around controllable output during stressed conditions. The replacement queue is large by nameplate MW, but the replacement profile looks very different once accreditation rules, withdrawal rates, timing, and geography enter the equation.

That is where the arithmetic becomes more complicated than the headline queue numbers suggest.

One of the more interesting aspects of MISO is that the system does not initially look constrained if you focus only on aggregate queue totals. The tension becomes more visible when retirements are mapped against actual delivery timing and accredited replacement capacity rather than raw nameplate additions.

Issue 07:

MISO Has a Retirement Problem

→ https://t.co/90EIKPxJv5

utility death spiral isn’t new.

Christopher Johnson (Avanza Energy) outlined it years ago.

But AI is now putting it under real pressure.

Large users leave →

Revenue falls →

Rates rise →

More leave

It doesn’t stabilize.

It accelerates.

Where does this hit first?

👉 https://t.co/HYZQhUIwDJ

ERCOT clears projects faster than any U.S. grid, with a 0% withdrawal rate and shorter timelines.

But demand pressure is the highest in the country at 5.4x, versus 3.0x in PJM.

The constraint didn’t disappear. It moved—from the queue into the operating grid.

Fast doesn’t always mean stable.

Demand pressure measures how much generation is trying to connect relative to system capacity.

ERCOT is at 5.4x. PJM is at 3.0x.

The queue looks clean. The stress shows up elsewhere. That’s where systems tend to break.