The more people tell me how much more time I should be spending in Claude and other AI tools the more I find myself wanting to spend more time physically present with actual people.

Just sent @Groupon management a live product redesign and working codebase to unlock the massive potential in company.

@dusenn@ranakash@viktorbezdek@prerit_munjal@jansromek

GitHub: https://t.co/VIRsvPsC3p

Live beta: https://t.co/wZGHGo7wfG

$GRPN

Well, I’ve never met him. My first experience was Valeant — a puzzle for me early in my financial analysis years. That was a great one

I do think he knew exactly what market reactions to his words would be and that he could smash a grab by exaggerating some of his claims. And bully stocks.

I just think it sucks because most people think activist short selling is all smash and grab

Vs a healthy component of the market and the marketplace of ideas

@CodfishJohnny@muddywatersre Dude look at his tweets and statements about companies

Directionally the verdict was right. Especially if you coordinate with hedgefunds

@DeLaMurphy Not really. There’s very few left

And my view is that Left ended short-selling careers being extremely hataeable and often blatantly wrong on core facts later in his career.

Made a hard business even harder

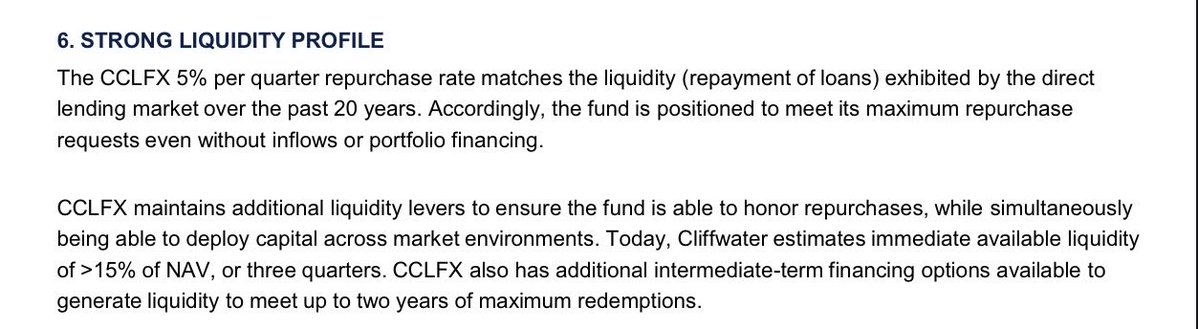

It’s appalling Cliffwater says they have 2 years of liquidity. Here are the facts:

Latest annual report:

Cash: $581m Unfunded loan commitments: $6.1B + Annual fees/expenses: $1.0B Net assets: $31.3B 5% quarterly gate: ~$1.6B Q2 redemption requests: ~17%, or ~$5.3B

So cash covers ~10% of unfunded commitments and ~0.4 quarters of the gate.

They can borrow about $4.4B more on committed facilities, increasing leverage on a ~1.5x look through.

The SEC doesn't ask whether a liquidity presentation is optimistic.

It asks whether it's complete.

Investors should demand a reconciliation from headline liquidity to net liquidity after unfunded commitments, fees, and expected credit losses.

Potential areas to reference:

1. Investment Company Act Rule 22e-4 (Liquidity Risk Management) — if a fund presents liquidity in a way that could be materially misleading relative to actual redemption capacity.

2. Securities Act Rule 156 — prohibits materially misleading statements in investment company sales literature.

3. Exchange Act Rule 10b-5 — prohibits omissions of material facts necessary to make statements not misleading.

4. Investment Advisers Act Sections 206(1) and 206(2) — anti-fraud provisions covering misleading disclosures to clients.

$CCLFX

$CCLFX HAS UNFUNDED COMMITMENTS to the managers of their Private Investment Vehicles of:

$6.84 BN as of March '26

THIS NUMBER IS UP $2.16bn from the March '25 number of $4.68bn.

What happens when/if these managers draw on these commitments during the next year?

Blackstone is the worst ‘S tier’ lender.

If they want to slow down outflows somewhat, ask:

“Well, are you looking to allocate to Cliffwater ?”

If “maybe” :

“You realize ~15% of their loans are underwritten by us. And we don’t give them access to every loan.”

@blackstone

Hunter Biden is a dime a dozen in an AA meeting. He’s telling jokes you’ll hear from a dude with a face tattoo in a church basement on any given Tuesday afternoon. You guys just don’t know any drug addicts.

In March, Blackstone paid every BCRED redemption to reassure clients.

In Q2, 10% wanted out. The cap is back to 5%.

The reassurance lasted one quarter.