This is the tough lesson that a lot of people are learning the hard way

AI might have made building apps a lot easier, but it also set the barrier to entry at zero

Because anyone can do it, there is no moat left

The only edge left in the future will be sales and marketing

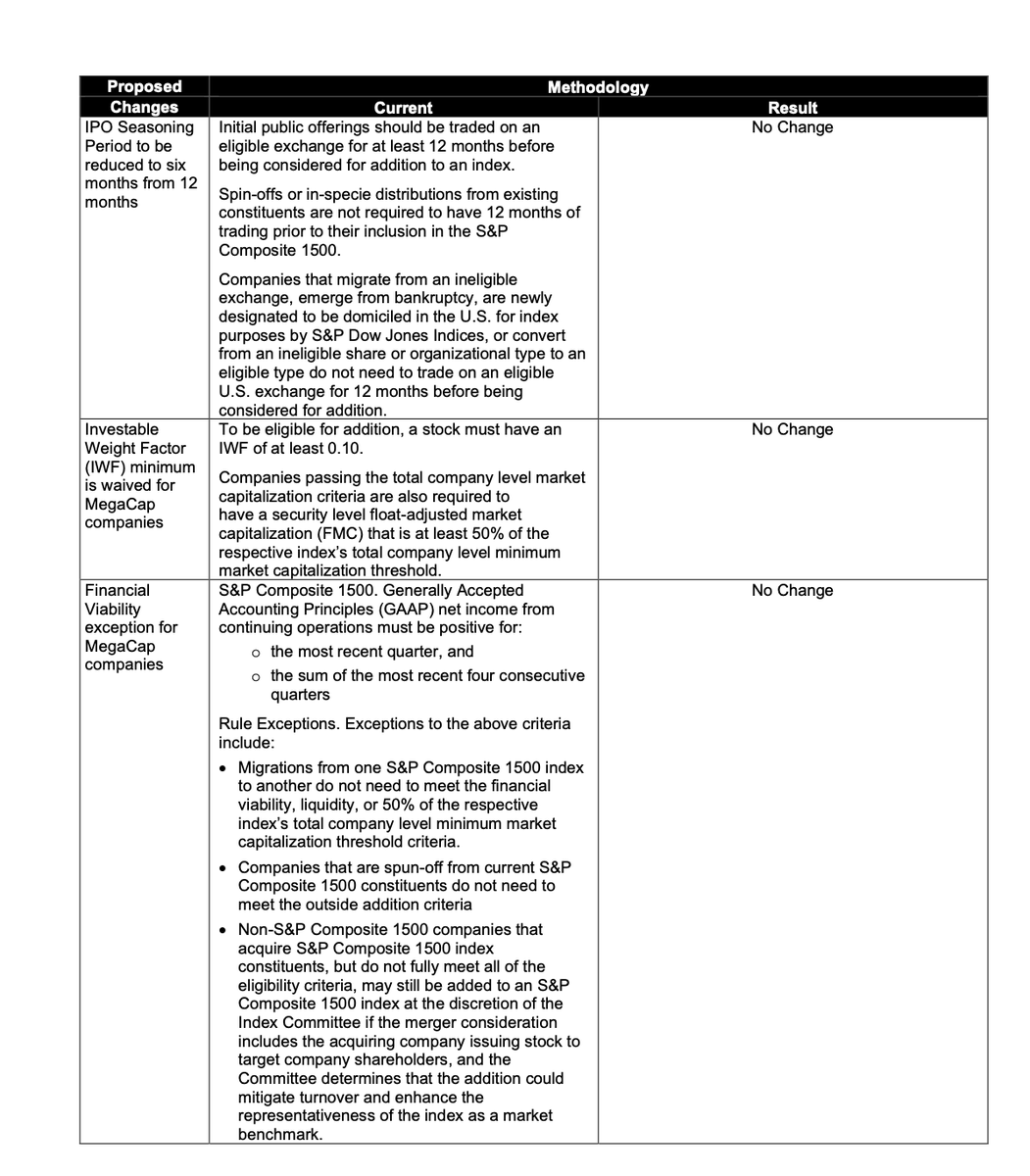

Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

Collected thoughts on $GOOG:

1) Significant chunk of the ATM will be used for employee SBC tax obligations (screenshot).

2) Ruth Porat is a very savvy financier and zero chance she was not involved in this in some way, meaning how this was structured (specifically: equity vs. debt) was very deliberate.

3) All the hypers can see future capabilities, cloud pipelines etc. you cannot, and are making investment decisions accordingly h/t @GavinSBaker@TMTLongShort

4) The entire supply chain is strained and $NVDA is showing that the only real way to continue your lead is to throw money around that nobody else can match to secure supply. $GOOG can also play that game, and given #3... they probably should.

5) For $GOOG, this is existential. Larry Page stated internally he'd rather go bankrupt than lose this race. During Google's early days the vision for Google was AI that understood the web, it's no surprise they would pull every stop out with that kind of outcome in sight, and relatively few competitors who can credibly compete.

Rule changes for the SpaceX $SPCX IPO:

Index providers waived the profitability requirement and cut the seasoning window from 90 days to 5.

This forces over $30 trillion in passive 401k and retirement money to buy SpaceX at IPO valuations.

Bloomberg Intelligence estimates S&P 500 funds must absorb 19% of SpaceX's float within 6 months.

Russell 1000 and Nasdaq 100 funds will absorb 24%.

The rules built to protect passive investors:

1. S&P 500 has required 12 months of trading and 4 quarters of GAAP profitability since 2002. Both waived.

2. Nasdaq cut its inclusion window from 90 trading days to 15.

3. FTSE Russell cut its to 5.

All three benchmarks are now structured to buy SpaceX at IPO pricing.

I bought $INTU

Seems extremely cheap at mid teens economic earnings, high quality, growing DD, and likely an AI beneficiary.

Quickbooks is 60% of revenue, and growing twice the rate of Turbotax (which itself is still growing Mid to HSD).

What am I missing?

@varrock They’re not losing money on it, it’s break even for them. Costco isn’t walmart, they hate loss leaders and view it as an insult to the customer

@BeanerOfSnow Costco absolutely hates the idea of loss leaders so i very much doubt they’re losing money on this. Think the only loss leader they allow is the hot dog

Think it's maybe not as appreciated as it should be that the NPV of an EUV sale = upfront sale + 20 years+ of upgrade + service revenues (~93% or something around that of all ASML machines ever sold still in service).

The current semi capital build is incredibly accretive to ASML beyond the impact to current near term ests.