One of the first systems I made.

Runs on DAX (15m timeframe)

Backtest: 2006–2026

• 56% win rate

• 1.86 gain/loss ratio

Been trading this live since 2018.

No losing years so far.

Because the goal isn’t to fit the past perfectly, it’s to survive new data.

A wise trader once said "Make it fit like a mitten, not a glove" and that quote has stuck with me since forever.

Most overfitted systems look great on one dataset, the trick is to make it look great OOS

Then I optimize the strategy independently on each segment.

Instead of picking the single “best” parameter I look for stability across all datasets.

If a parameter is optimal at:

• 11 in dataset 1

• 10 in dataset 2

• 12 in dataset 3

I’ll choose something in that range.

2/3

How I avoid overfitting when building trading algos 🧵

When I’m ready to optimize a system, I don’t just run it on the full dataset.

I split the data into multiple segments.

Typically:

• First 40% of the data

• Middle 40%

• Last 40%

(Yes, they overlap)

1/3

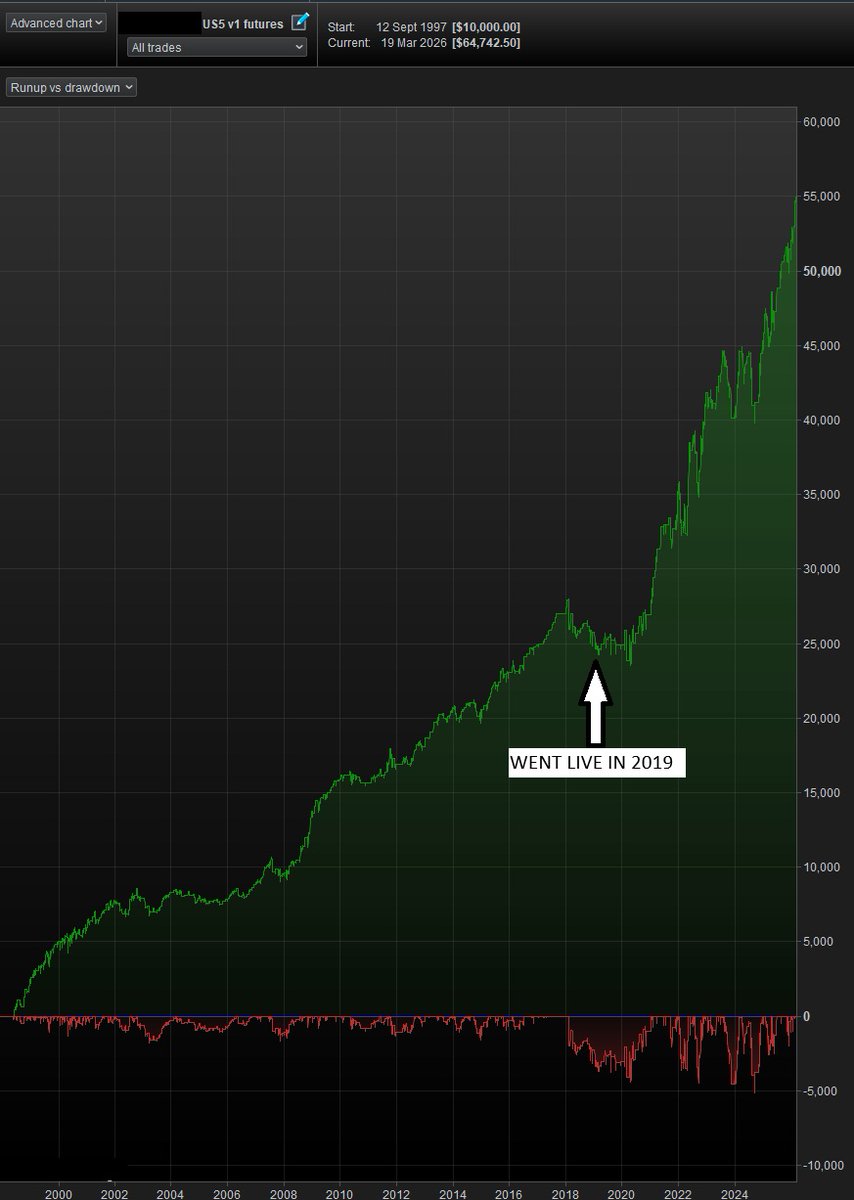

Been running this algo on S&P 500 futures since 2019.

2019–2026:

• 73% win rate

• 1.86 gain/loss ratio

Backtest 1997–2019:

• 73% win rate

• 1.92 gain/loss ratio

Behavior is consistent across periods, doing what it’s supposed to do.

(2 contracts, MES)