Everybody is busy thinking about how $GME is going to put together the money for the $EBAY acquisition, how the equity roll-in is going to work, and where they are going to find a therapist for their non-stop crying. But there is one possibility nobody has seriously considered and I’m quite shocked that they haven’t: maybe GameStop won't need ANY financing.

Why am I shocked? Look at the playbook Ryan Cohen already ran in the past. In 2020, RC Ventures quietly began acquiring shares of a struggling, mismanaged retailer, first a 9% stake, then about 12.9%. He wrote an open letter torching the board's internal incompetence, demanded a strategic review, and leveraged his shareholder position into three immediate board seats in January 2021. Within months the entire executive suite was cleared out, the board was flipped, and he took over.

He never needed to buy GameStop outright because he bought control and let governance do the rest. Fast forward to 2026, GameStop already holds roughly 9% of eBay and is still accumulating, and Proposal 4 on eBay's June 17 ballot would lower the special meeting threshold from 20% to 10%, a proposal that has already cleared 47% support three separate times. If it passes, Ryan only needs to reach 10% ownership to call a special meeting, force a board vote, install his people, and be effectively running eBay before the ink is dry on a single acquisition document.

From there he either accumulates the rest of the float over time like Buffett did with GEICO, or engineers a merger once he controls both sides of the table. That is Icahn's ferocity fused with Buffett's patience, and it is the one scenario nobody on Wall Street or Main Street has modeled. Have a good weekend 🍻

$GME GameStop new 13D filing now owns 9% of $EBAY

•827,648 shares as of June 5, 2026

•GameStop purchased the 827,648 shares for a total purchase price of $91,004,145.37 excluding fees and expenses. The source of funds used by GameStop to purchase such shares of Common Stock was cash from its working capital.

•39,046,658 shares of Common Stock underlying Put/Call Pairs

•The Put/Call Pairs have strike prices ranging from $84.739414 to $118.275965.

•Together, the 827,648 shares of Common Stock beneficially owned directly and the shares of Common Stock underlying Put/Call Pairs constitute approximately 9.0% of the outstanding shares of Common Stock

•In the event of physical settlement of the Put/Call Pairs, GameStop would have the sole power to vote or direct the vote of the shares of Common Stock underlying such Put/Call Pairs.

13D filing: https://t.co/g7waTkX2J2

Trading Data: https://t.co/vYhdndp2Mf

GameStop reports highest quarterly net income in company history of $389.6 million. Highest first quarter operating income in GameStop’s history of $143.3 million. Net sales grew 14% year-over-year, driven by collectibles. Cash, marketable securities, digital assets and related receivables, and collateral pledged for derivative asset of $9.7 billion.

https://t.co/BAu3T6V9w4

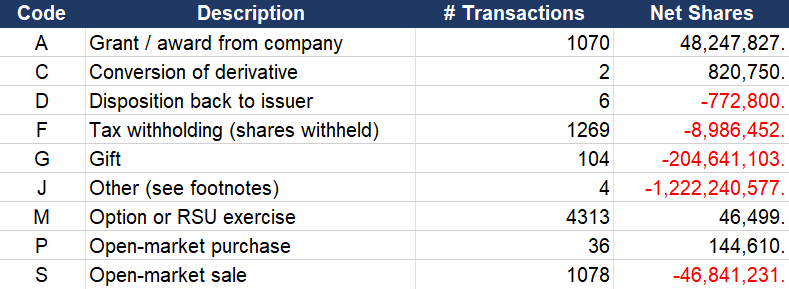

I just downloaded every single insider trade for $EBAY since I am planning on making an insider trading indicator. I aggregated everything and here are the numbers.

Since the stock started trading in 2003, there have been a total of 144,610 shares purchased on the open market.

48,247,827 shares were awarded to insiders (how the execs get their shares in the first place)

46,841,231 shares were sold on the open market.

All of these $EBAY insider sells are significantly below the all-time-high $125/share offer from GameStop. Make it make sense. What a bunch of fiDOUCHEiaries!

As always, my man nailed it again.

As he outlined, eBay’s board won’t deploy a poison pill or invoke Delaware’s 3-year business combination moratorium against Cohen, for two specific reasons I’d like to discuss.

First, institutional shareholders.

eBay’s shareholder base is over 90% institutional, and I think they are observing carefully. And as noted in previous posts, these same institutions are also significant GME shareholders, so they sit on both sides of this trade simultaneously.

The board has already rejected a 46% premium over the unaffected price. Every day that passes without a deal is a day those institutions are leaving money on the table. Adopting a poison pill to physically block shareholders from ever voting on an offer that could double their investment would be an act of open warfare against the very people the board is supposed to serve.

The institutional backlash would be immediate and severe. Proxy advisory firms like ISS and Glass Lewis would likely recommend voting against every sitting director at the next annual meeting.

Second, breach of fiduciary duty.

In Delaware, where eBay is incorporated, the board owes a duty of care and a duty of loyalty to shareholders, not to itself. Rejecting a 46% premium is legally defensible if the board can articulate a credible standalone plan. But adopting defensive measures specifically designed to prevent shareholders from ever voting on a transformational offer crosses a very different legal threshold.

A class action in that scenario would be almost inevitable, and individual directors could face personal liability and they know this.

This is why the real battle will be fought at the shareholder level, not at the board level. Cohen doesn’t need the board’s permission, he needs 10% of eBay’s shares to call a special meeting, or 20% if the June 17 threshold proposal fails.

The clock is ticking for eBay.

Still learning. Still sharing. Not financial advice. $GME $EBAY

Besides multiple updated $GME 13D/As in the coming weeks (Ryan is buying and has a lot of dry powder), we are going to see a Schedule TO filing here soon directly to $EBAY shareholders.

To formally launch a hostile bid, GameStop must file a Schedule TO with the SEC, which triggers a full disclosure regime including source of funds, terms of transaction, and all prior negotiations with eBay, etc. Because half the consideration of the current proposal is GME stock (this proposal might change), GameStop would also have to file a Form S-4 to register those shares (if any new are going to be issued for this deal), which adds ~4-8 weeks of SEC review time before the offer can even go live. They also need binding financing locked in and detailed in the Schedule TO filing, since the current structure relies on ~$9.4B in cash, a $20B TD Securities debt commitment, and a yet-to-be-determined stock issuance for the equity roll-in piece.

Once the Schedule TO is filed, eBay gets 10 business days to file a Schedule 14D-9 recommending shareholders accept or reject the offer, and they can also deploy a poison pill or do things like invoke Delaware’s 3-year business combination moratorium to freeze GameStop out if it crosses the 15% ownership threshold at that time (they won’t). GameStop currently sits at just 7.55%, meaning they are yet to have the leverage needed to call a special shareholder meeting and force a vote (currently 20% according to eBay bylaws, but there is a proposal being voted on in their annual meeting to change it to 10%, put forward by John Chevedden). Since the Schedule TO has not been filed yet, so we are still in the pre-commencement phase, and the real fireworks have not started yet. There are some dip buying opportunities coming up for eBay in the immediate future, as they are about to distribute their quarterly dividend this Friday.

I bought 1 share of $EBAY earlier this month.

That means I’ve bought more shares than the people running the company have in the last 5 years combined.

🤯

Did Ryan Cohen $GME - in his personal capacity, buy something in October of 2024? Probably wasn't private shares of $SPCX right? Cause that would be legendary.