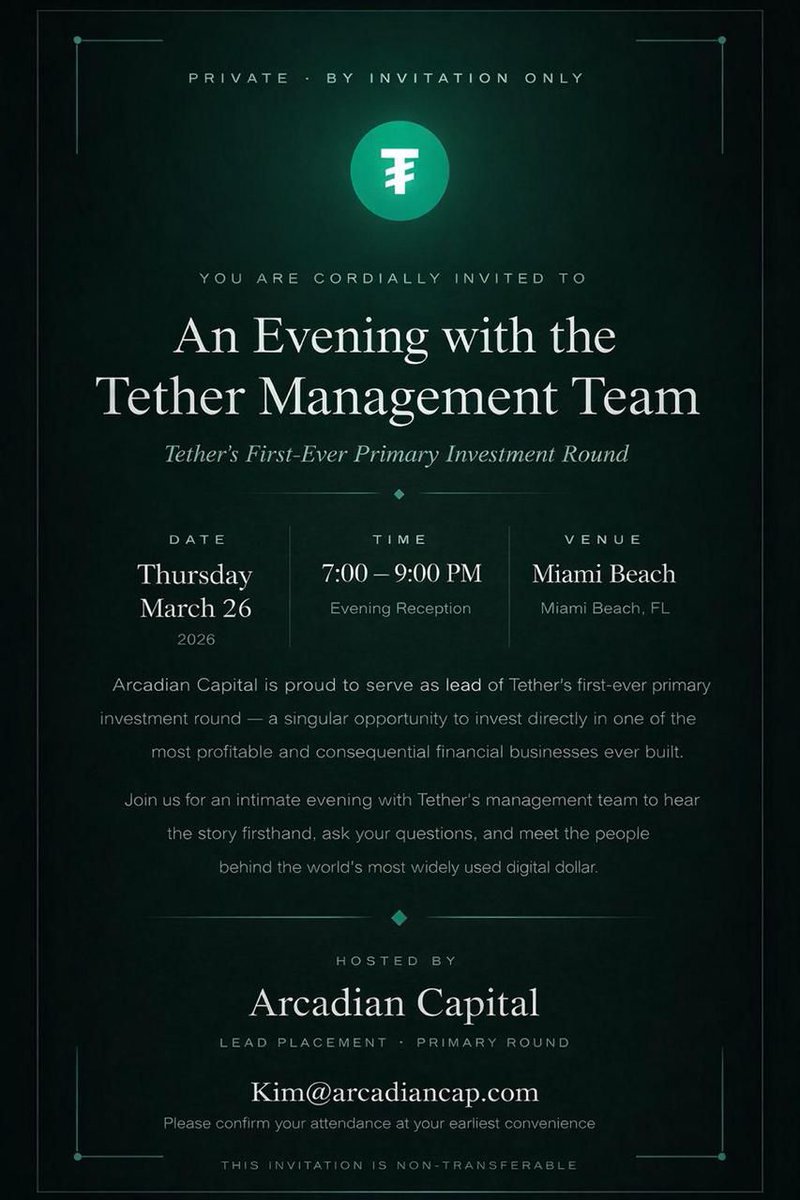

When you spend six months trying to sell a couple percent of your Tether equity at a ridiculous $500b valuation with Cantor and can’t…..

You shift to hawking your stock to retail with some shitty little investment bank nobody has heard of…..

Top 6 Questions for @Tether at tonight's investor pitch in Miami:

1) Why does Tether pretend Paolo @paoloardoino runs the company, when Giancarlo Devasini controls it unilaterally?

2) Is this a growth round, or a liquidity event for insiders? Whose shares are being sold and why? Why does Tether need money if it’s so profitable?

3) Given the numerous claims on underlying assets in various subsidiaries that trickle up to Tether, why should investors accept talk of a reserves audit without a full-company audit, including governance, related-party transactions, and ownership?

4) Did Bo Hines @bohines discuss any future role with Tether while still helping to shape the U.S. stablecoin framework via his role in the White House?

5) Why were Devasini-linked entities buying Northern Data @NorthernDataGrp assets at what an independent report described as a steep discount?

6) How serious is the litigation and shareholder-exposure risk around the Northern Data related-party asset sales, given the allegations that Devasini-linked entities acquired assets at discounted prices?

@BitcoinJuicy Yep. @saylor has issued about 9x more $MSTR common that STRC. MSTR still trades at a discount to its BTC. If you love BTC, own it. Not MSTR

This story with @bdanweiss is built from documents we reviewed put together by internal investigators who uncovered the flows and were later fired by Binance, though the exchange has denied they were terminated for surfacing compliance concerns

https://t.co/DLu0r7mvq0

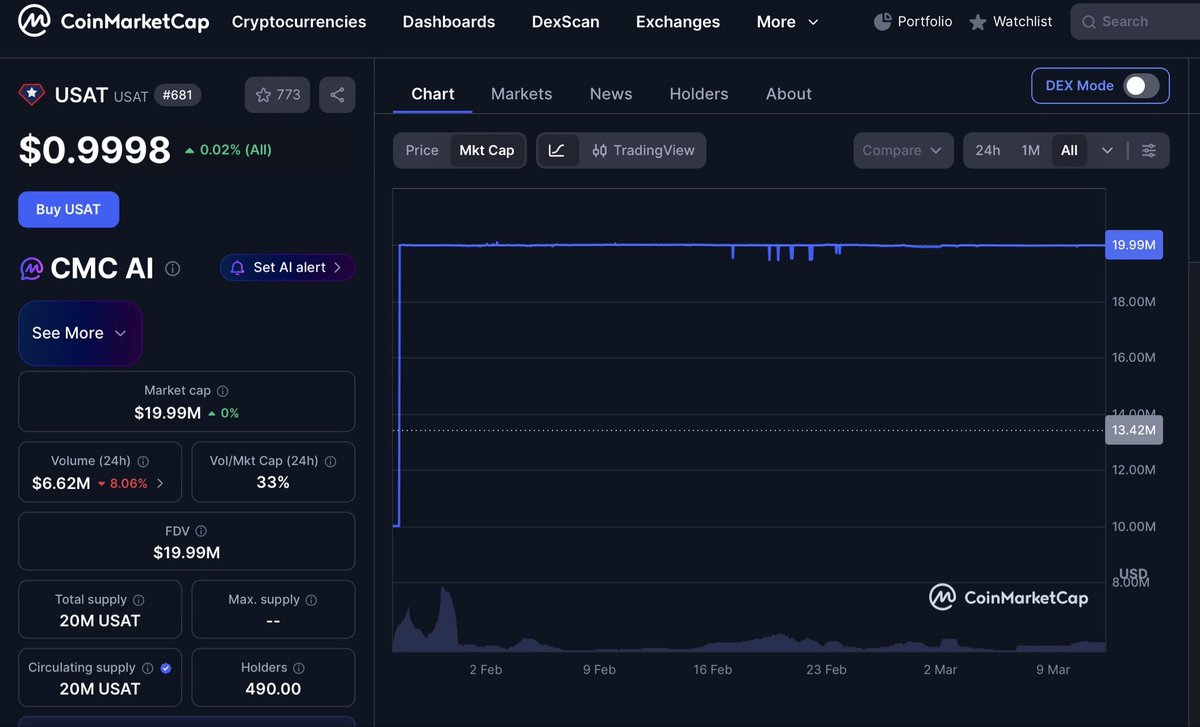

Bad historic analogy. Stablecoins are network businesses, which is why USDT and USDC dominate. Every new stablecoin that has launched has gained virtually no traction. The Tether bulls thought USAT would be a fully fungible on-shore work around for Tether’s refusal to be US-compliant. But Tether is clearly not actively supporting it. They could have minted billions on their own just to give it a market cap boost - but Paolo and team have done zip. And there’s simply zero reason to use an onshore USAT and that’s not going to change with the passage of time.

Tether’s onshore USAT launched in late January and did an initial mint of $20M, and since then they have minted zero new USAT.

Nobody is using it.

Daily volume was an embarrassing $6M yesterday and that was despite USAT having launched on Bitfinex, Kraken, Moonpay, HTX, MEXC, BTSE, Token Pocket, Coin98, Bidget Wallet, Liquid, Hold Station, IMtoken, Rumble Wallet, Alchemy Pay, AEON, Bitqik, Mercado Bitcoin, https://t.co/R7gWQ5CGOw, FoxBit, PDAX, Recurrent, Poloniex and Biconomy.

All the distribution in the world doesn’t make a shitty little stablecoin something other than a shitty little stablecoin.

#USAT

Uh? STRC is a B- rated pref issued by a company that can only fund the dividend by issuing more common. Even with the first weekly sale of any size in STRC, it’s still tiny relative to what @saylor used to issue. And MSTR continues to underperform BTC and it trades at a discount to BTC. If you love BTC, own it. Don’t waste your time with MSTR or STRC.

@UpwardFrood@saylor Price is irrelevant. Issuance is what matters as @saylor needs pref leverage to replace the converts. Yet pref investors don’t like what MSTR is selling……it’s not about anything I say. Just watch the volume of STRC sales..

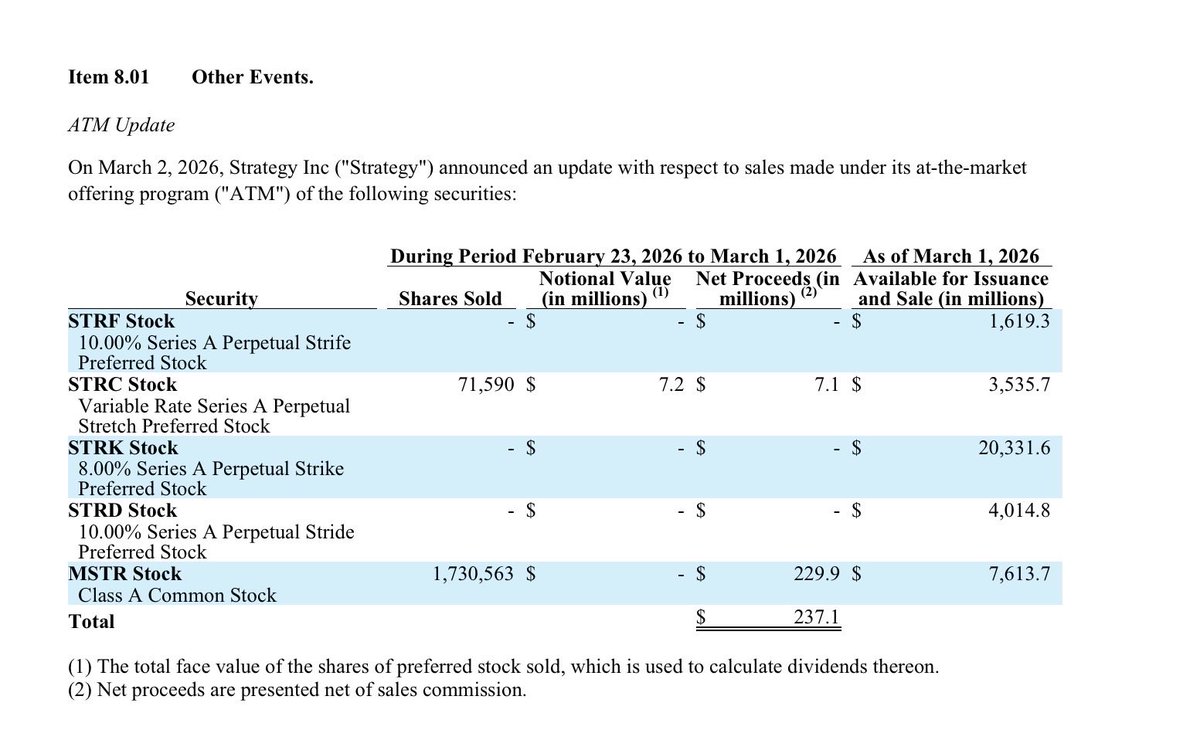

Another Monday check in on $MSTR and its ��digital credit solution”…… $STRC. (Hint, it ain’t credit)

Another underwhelming week. Only $7.1M of $STRC sold. So @saylor falls back on issuing $230M of common.

7 months since launching the $4.2B STRC ATM, 84% remains unsold.

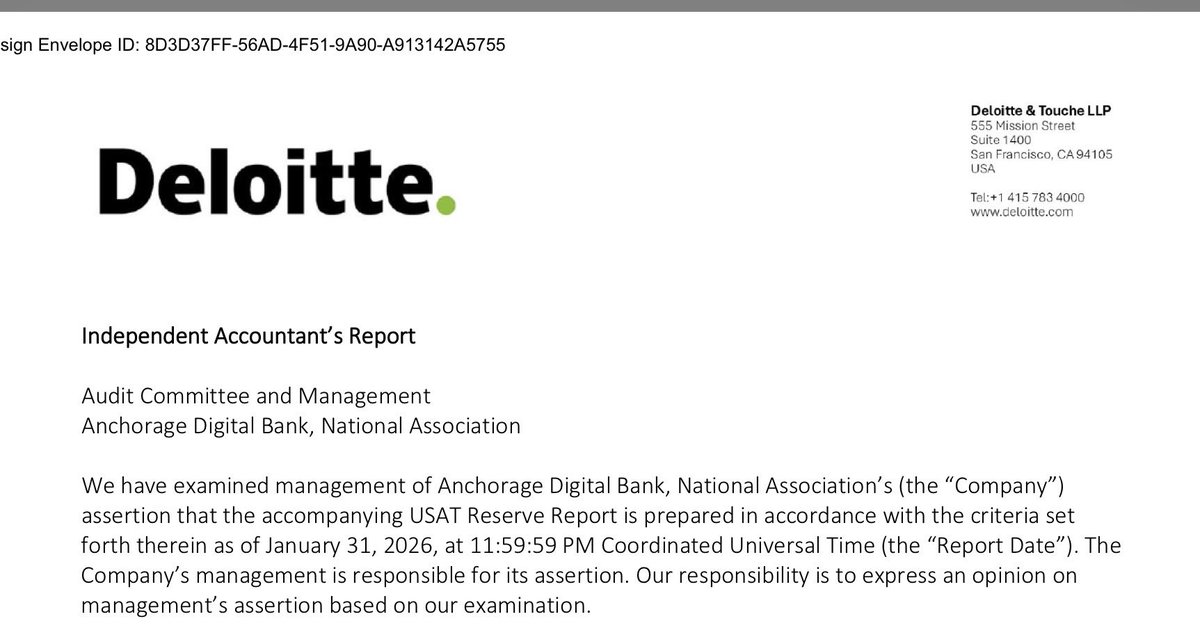

Crypto journalism can be so dumb. Tether didn’t tap Deloitte for the attestation for “rounding error” USAT stablecoin.

Anchorage did.

“Tether” is nowhere on the USAT attestation, only Anchorage who is the issuer. Tether is just the name on the coin.

$STRC is junk rated (S&P ‘B-“) pref equity risk. So it’s worse that junk debt as it sits below all debt in the credit stack. $MSTR has negative operating cash flow, so it can only fund the dividends payable on its pref by issuing common shares. Pref investors don’t like risk like this, which is why $STRC isn’t selling at the pace @saylor clearly expected when he set up the $4.2B ATM

@GoddessDefi Sorry. That’s bull shit. USDC is onshore in the US and regulated. They always respond to court orders, law enforcement requests and OFAC sanctions. Tether viewed all of those as optional until Dec ‘24

Tether has frozen $4.2B of USDT at the request of authorities

I just checked for comparison how much USDC has likewise been frozen:

$117 million.

36x more USDT has been frozen than USDC.

Tether clearly is the leading stablecoin for illicit finance by a wide margin. No wonder they don’t want to go legit and get regulated.

@stansilver2024 Under the El Salvador digital regulations, they are supposed to provide the Salvadoran regulator audited financials by June. I’m not holding my breath

And herein lies the difference in perception. These are traditional preferred equity instruments, not credit. They have a residual claim on any assets but they are behind everyone other than the common holders. That’s why pref investors have always sought safe, cash generative issuers (big banks, utilities). Yet MSTR has negative cash flow and can only fund the pref dividends by issuing more common. That’s a high risk offering of a product that historically is sold to risk adverse yield investors. That’s why STRC simply isn’t selling the the size the @saylor clearly hoped for (you don’t set up a $4.2B ATM for STRC and still have 85% of it unsold 6 months later). I don’t know why the MSTR faithful go nuts over this issue. STRC is a pref equity. By definition that’s equity risk. Not credit.

Strategy Prefs are not credit. it’s that simple. They are traditional preferred equity instruments that are utterly uncollateralized. They simply have a preferred equity claim on and residual assets (so above common holders and below everyone else). It’s not a credit instrument. It’s an equity instrument.

Minor fact check, while Saylor could create a digital credit instrument, he has yet to do so.

All he’s done is try to spin to his faithful that $STRC prefs are “digital credit”

They’re not. they’re straight up unsecured pref-equity with zero claim on any Strategy asset.

If @saylor wants to push digital credit, he could start by actually creating a digital credit instrument and not just bull shitting about one

@WellspringGP The Company’s preferred securities (STRF, STRC, STRE, STRK, STRD) are not collateralized by the Company’s bitcoin holdings and only have a preferred claim on the residual assets of the company.