There are two ways to touch 8 billion lives: acquire 8 billion individual customers, or build the infrastructure for the institutions that already serve them.

We chose the latter.

Today we're announcing OpenFX’s $94M Series A from @Accel, @atomico, @FactionVC, @M13Company , @northzoneVC, @PanteraCapital, and with support from existing investors @flybridge and @hash3xyz.

It’s fitting to announce our acquisition as the industry comes together in Amsterdam for @money2020 Europe.

@openfx_ acquires Embed, an Amsterdam-based payments infrastructure company. It’s our first acquisition, a major step in our European expansion, and a clear statement about how we think financial infrastructure should be built.

Many companies claim to operate across Europe. In practice, many are reselling someone else’s license, relying on a partner’s BIN, or sitting one step removed from the regulated rails their customers depend on.

That can work for a while. But when a corridor breaks, a partner changes terms, or a customer needs certainty, the difference between renting access and owning the regulated layer becomes very real.

With Embed, OpenFX is moving deeper into that regulated layer.

Embed holds two licenses that matter: a Dutch PI regulated by DNB and a UK EMI regulated by the FCA. The transaction is subject to regulatory approval, but once complete, OpenFX will have regulated entities in two of Europe’s most important financial jurisdictions.

For our customers, that means more control, more resilience, and a stronger foundation for moving money across markets.

We’re also building the team locally. We now have offices in London and Amsterdam, with 20 people across Product, Engineering, Compliance, and Go-To-Market.

With backing from European investors, including @northzoneVC and @atomico, and $60B in annualized TPV across the network, Europe has become our largest commitment outside the United States.

We’re here to build locally, own the infrastructure that matters, and make global money movement more reliable from the ground up.

https://t.co/CPzbbPnuu0

“The blockchain solved cross-border payments, and anyone still struggling just hasn’t adopted them yet.”

This is basically nonsense. A common sentiment, and not entirely unjustifiable, but basically nonsense.

Sit in any payments company pitch in 2026 and you'll hear "instant blockchain settlement" within the first five minutes. People nod along because it’s partially true. We all pretend that moving stablecoins between wallets was the thing that needed solving.

But we all know there is more to it than that.

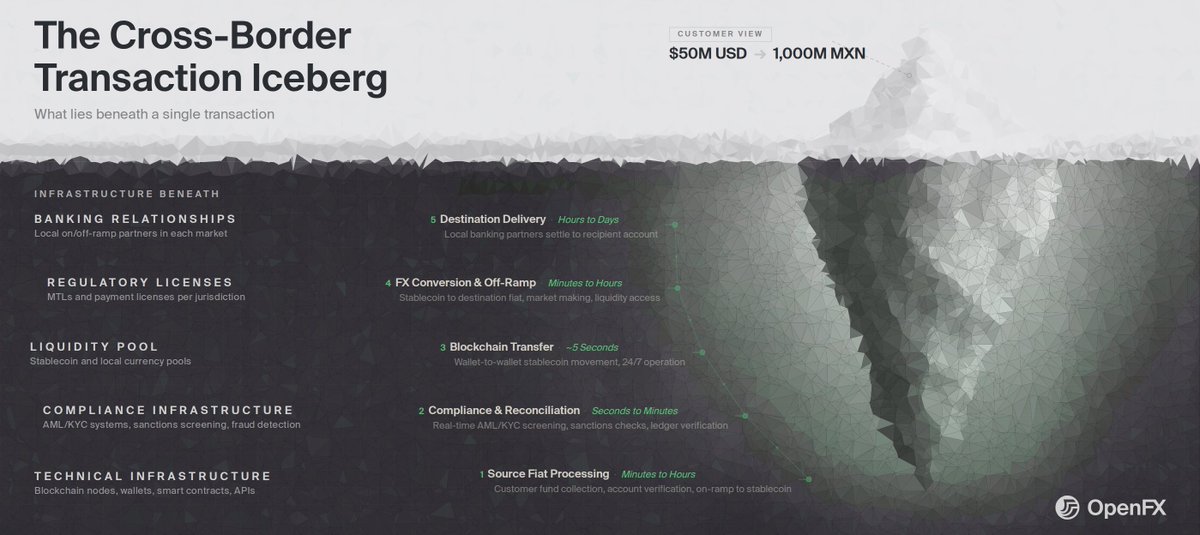

If you've ever actually tried to get $50 million through an exotic corridor on a Saturday night, you know the blockchain transfer is the least of your worries. Maybe 1% of the problem.

Here's what everyone knows but rarely talks about in the marketing copy:

Before that five-second transfer can happen, you need to clear that $50M through domestic banking rails. Run compliance screening. Handle the edge cases that trigger manual review. Get the money on-chain in the first place.

After that five-second transfer, you need liquidity in the target currency. Not thin liquidity that slips when you execute at size, but actual depth. That makes banking partners willing to take your calls after getting home from their kid’s soccer game.

Then you need to navigate local payment rails that work differently in every jurisdiction. Then you need to land the funds in a bank account that's willing to receive them.

The blockchain transfer sits in the middle of all of this – fast, commoditized and largely irrelevant.

Exotic corridors don't fail on-chain. They fail at the off-ramp. They fail because not many people have those kinds of banking relationships. They fail because liquidity doesn't exist at the depth you need between BRL and AED. They fail because for a long time everyone was worried about moving G3 dollars a micro-second faster, and almost no one focused on building rails the rest of the world could use.

Here at OpenFX we say that we want to "move money like data.”

But what does that mean?

That means caring about every part of the transaction – the iceberg, above and below the surface.

It also means caring more about emerging markets and exotic corridors, where these problems are even more acutely felt.

Blockchain as a selling proposition is over. Wallet-to-wallet transfers are fully commoditized.That part of the game has been won, what matters now is whether the money wallets move actually lands in the account your supplier can access, in the currency they need, on the timeline you promised.

That's an operations problem. An infrastructure problem. A relationships problem.

The kind of hard problem we were built to solve.

We're at Consensus Miami May 5-7 and holding time for in-person meetings.

If you're moving cross-border volume (or building rails for someone who is), grab 30 minutes with us, on-site or nearby.

We'll cover live corridor pricing for your pairs, give you a sandbox account, and explain where stablecoin settlement actually moves your balance sheet.

Book time here: https://t.co/kzJHLD75rM

It's Saturday night. The Peso just dropped 4%.

Your company has $40 million exposed and the hedge you meant to place Friday is stuck in queue.

You're texting your RM. He's at a birthday party. He's really sorry.

This is how trillion-dollar FX infrastructure actually works.

Bloomberg terminals and 2-5 day settlement times, assuming nothing gets held.

We've stopped noticing how insane this is because for a long time the world did not move fast enough for it to matter.

If the last several years has taught us anything, it is that this is no longer the case.

Once-in-a-generation shocks show up quarterly, a system that can't handle a 4% Friday move won't survive what's coming.

To keep up, cross-border payments will increasingly need to be automated.

Routine work is migrating to systems that don't sleep. And human treasurers are increasingly called on to exercise judgement, and provide transparency.

We're building our tooling with that future in mind, APIs and automated treasury systems that help treasury desks survive this future.

Read more here: https://t.co/KELt3mnynV

The most misleading phrase in global finance: “instant settlement.”

In most corridors, money doesn’t simply jump from the vendor to the recipient, arriving in their hands instantly after the transfer is initiated. It passes through sometimes dozens of hands, where it is screened, run through a compliance gauntlet, and converted between one or more intermediary currencies.

At every step, fees and the risk of slippage mount. @openfx_ understands this problem deeply at each phase of the payment process and has started with FX conversion to improve.

I wrote a quick, practical explainer with numbers and a mental model you can reuse to understand this process.

#MoneyManagement #CrossChain #remittance

https://t.co/afzTzrEbaA

Our Founder @prabhakar2reddy had the opportunity to sit down with Atomico to discuss his entrepreneurial journey.

In this clip, he describes how he decides which ideas to pursue, and the personal story that led him to start OpenFX.

Some of the key take-aways:

- Have a clear vision of the future, of what is possible.

- Double down in those domains where this future meets your unique abilities.

- Invest in others who can carry the torch in those areas outside of your expertise.

This is a part of a much longer interview that you can see if you visit @atomico's page.

According to J.P Morgan, in 2024 there was over $200 trillion in annual cross-border payment volume. And it's expected to surpass $300 trillion within the next several years.

@openfx_ is tackling one of the largest market opportunities that exits.

Don't miss my interview with @prabhakar2reddy to learn more about OpenFX and how he see's OpenFX changing the way money moves around the world.

That is why OpenFX has built on a “global HQ” model, assembling a team of world-class operators across Miami, London, Dubai, and Bangalore, led by regional experts.

We are distributed because the problem is.

Our Founder wrote the blueprint. Read it here: https://t.co/XLjniOR3wk

In the 1990s, construction workers in Dubai stood in long lines to pay a 7% fee just to send their paychecks home.

In 2022, after a tech revolution that put supercomputers in our pockets, those exact same lines were still there.

Why?

But you cannot build a global, real-time system using a 50-year-old hub-and-spoke model. The conceit that what works in a New York boardroom works equally well in Singapore is exactly what broke the system in the first place.

This is a huge job, and we think that it will require a huge shift in the way people see FX, a shift beyond even stablecoins. We're building toward a future where the treasury becomes programmatic. Where software manages cash flows at 3am on a Sunday and the infrastructure just works.

A world where money moves as easily as a text message or a cat meme.

More on where we're headed here: https://t.co/hWWcUPoMjW

We came out of stealth nine months ago at $8B in volume. As of February we crossed $45B. Revenue is up 10x.

This week we raised a $94M Series A.

@Accel, @atomico, @FactionVC, @northzoneVC, @M13Company, @PanteraCapital, some of the biggest names on both sides of finance chose to back us.

You might be wondering why.

Fixing cross-border FX is more than just moving money faster for G7 economies, despite how much of the industry marketing frames it. Cross-border payments are how actual people across the globe, many of them highly vulnerable, get paid.

Payroll for remote teams. Remittances back home. Suppliers waiting on invoices. When settlements take days and fees eat the margins, real people feel it.