A traditional nuclear plant is not expensive because the fuel is rare or the technology is exotic (it is however for SMR's). It is expensive because almost all of the cost is paid upfront, long before a single kilowatt hour is sold. You spend billions first, then wait years before revenue starts. During that time, capital is not idle. It accrues interest. i'll walk you trough it:

The metric that matters is WACC, the weighted average cost of capital. In simple terms, WACC is the minimum return investors demand to lend money or provide equity. The higher the perceived risk, the higher the WACC. Nuclear projects typically face much higher WACC than wind or solar, not because they produce worse power, but because the timeline is longer and the downside is asymmetric.

A wind farm might be built in 2 years. A nuclear plant often takes 10 years or more. Every extra year adds interest on top of interest. A 1 year delay does not just shift cash flows forward. It permanently raises the total cost of the project. This is why schedule risk dominates everything else.

To see how sensitive this really is, reduce the problem to 1 euro.

Assume 1 euro is invested today, at time 0. No revenue comes in until year 10, when the plant finally starts producing power.

At a 6% cost of capital, that 1 euro grows to about 1.79 euros by year 10. That is the minimum amount that must be recovered just to break even.

At a 9% cost of capital, that same 1 euro grows to about 2.37 euros over the same 10 years.

Nothing changed technically. Same project. Same build. Same output. Yet the required recovery is roughly 32% higher at 9% than at 6%, purely because interest compounded for longer.

Now add a 2 year delay.

Cash flow starts in year 12 instead of year 10. At 6%, the original euro now grows to about 2.01 euros. At 9%, it grows to roughly 2.81 euros.

The gap is no longer 32%. It is now about 40% higher for the exact same euro invested upfront.

This difference does not come from inefficiency or mismanagement. It comes from time. When construction is long and revenue is delayed, small increases in WACC and small delays in schedule compound into large differences in total cost. That is why a project that works on paper at 6% can become unfinanceable at 9% even if nothing goes wrong operationally.

Private capital understands this well. That is why traditional project finance rarely works for nuclear. Banks do not like assets that take a decade to complete, cannot be easily abandoned halfway, and face political and regulatory risk throughout construction. Without guarantees, investors either demand very high returns or walk away entirely.

Governments have tried to bridge this gap using contracts and guarantees. One approach is a long term fixed price contract for electricity. This removes market risk but not construction risk. Another approach is loan guarantees, where the state absorbs part of the downside if things go wrong. A more aggressive model allows investors to earn regulated returns during construction, reducing the period where capital earns nothing.

All of these tools have the same goal. Lower the effective WACC by shifting risk away from private investors. When this works, projects move forward. When it does not, projects stall, overrun, or collapse under their own financing costs.

There is a second layer that is often overlooked. Fuel supply. New reactor designs increasingly depend on enriched uranium that is not widely available today. If investors are unsure whether fuel will be available at stable prices 10 years from now, they price that uncertainty into capital costs today. Fuel risk becomes financing risk.

This is why comparisons with wind and solar are misleading. Renewables start generating cash quickly. Nuclear does not. Even if nuclear produces reliable power for 60 years, the first 10 determine whether it ever reaches operation. Finance is front loaded. Risk is front loaded. Returns are delayed.

Recent policy changes help, but they do not change the core math. Tax credits reduce total cost, but they do not eliminate schedule risk. Loan guarantees help, but only if political support remains stable, thats why I look into the political changes more directly than the costs of Uranium for example.

The liquid cooling pick is live!

See Markos his post for the details.

Any questions about TAM and/or peer multiples, you can tag or DM me!

$IREN

$NBIS

$CRWV

$VRT

$NVDA

$AMD

Liquid cooling pick💧

full investment paper live✍️

(It is in my portfolio also)

I already talked a while ago about liquid cooling and what’s happening in that sector. As you can see below, we think the importance and cruciality of this trend is still not recognized well enough by the market, especially when you look at the different cooling techniques now emerging.

We are still at the very beginning of a major adoption curve for liquid cooling. As most people interested in the AI sector already know, upcoming AI infrastructure generations explicitly require liquid cooling to function efficiently. Cooling is increasingly becoming a crucial layer in the AI build-out from performance guarantees to reliability, insurance, uptime, and everything in between.

We found and thoroughly investigated a very overlooked company in this space, and we just published a 40+ page deep dive on both the company and the broader industry. I personally own it also.

Inside:

• Bottom-up TAM build two-phase sub-segment alone: $25M → $9.1B by 2030

• The physics: why single-phase breaks and two-phase doesn’t

• PUE/WUE economics: same grid connection, ~71% more deployable GPU capacity

• The $24–25B data center insurance market by 2030 that quietly mandates two-phase for actuarial reasons

• why this company has a unique positioning

• full valuation and TAM capturing

• aquisition comparison in a aquisition heavy sector

And much more. Full

Pdf available on our discord which you can acces trough SS. Link in bio👆

$IREN $NBIS $CRWV $VRT $NVDA $AMD

AI is causing massive content inflation. Everyone can now produce a 2000-word essay in 30 seconds, and it shows. Feeds are getting flooded with technically competent but soulless writing that all sounds the same.

The weird part is that AI is simultaneously raising and lowering the floor. Bad writers now produce mediocre content. Mediocre writers produce decent content. But great writers? They're still great, and now they stand out way more because the median has collapsed into beige slop.

My prediction for X and Substack: the next 2 years will be brutal for middle tier creators. The bottom gets automated, the top gets amplified, and everyone in between gets squeezed.

The winners will be the writers with actual taste, opinions, and a willingness to be wrong in public. AI can mimic competence but it cannot fake results.

Curious what others are seeing in their feeds.

TLDR: What to do about content inflation on my feed?

Very excited to announce the new addition to the AAIG team💪.

One of the most technical hires we could’ve made especially in this huge AI-build-out cycle. I came in contact with fellow dutchie Mark and we where both excited to bring his investing and operational knowledge to AAIG. Mark has 15 years of hands-on operational experience designing and delivering the exact infrastructure that is crucial to understand. He managed datacenter builds at Equinix, Interxion (now Digital Realty), and SmartDC in the Netherlands. Then joined Google to design their future datacenters across EMEA. Currently building a hyperscale DC in Scandinavia.

This is operational depth in power, cooling, rack density, grid interconnects, site selection. All the physical bottlenecks throttling AI buildout. He’s lived it.

AAIG is in full build mode. We’re heads-down constructing a multi-analyst, high-depth research platform.

Welcome to the team @mvanbeijeren

Join us trough the SS link in bio on the journey💪. (Discord link is there also)

$NBIS $IREN $MSFT $META $AMZN $CRWV $GOOGL

We’ll have to see the S curve convert next quarter (si-28 final delivery) and S-1 spin-off. Uplifting of the kazach investment is at least nice to see!

If we get comfirmation from Pelindaba we will fly….

Nuclear enrichment is one of many themes ASP isotopes is positioned well in. They have their fingers in much more commercial interesting sectors. All with significant tailwinds and hitting hard ceilings where $ASPI can fully benefit from. Management execution has been lagging tho. Something that we watch closely. $LEU $SLX

Currently we see some reversal from the downwards technical trend they are in. Not confirmation yet. Full big thesis on what $ASPI does, positioning, milestones that we watch, name it all available on the platform in bio.

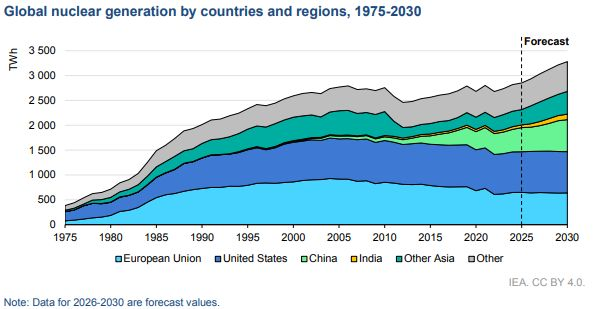

Global nuclear generation set an all-time record in 2025, per the @IEA's recent Electricity 2026 report. Strong growth projected through 2030 & beyond. Coming soon: a big increase in demand for enriched uranium...

I spent a lot of time putting together a deep dive on one of the most misunderstood themes in AI hardware today: glass core substrates and glass interposers.

Link in the comments below.👇

This is one part of what we’re building at AAIG: system-level research across the AI and memory stack, focused on where supply chain themes overlap and what is actually investable today.

The market seems increasingly interested in the idea that glass could be the next step in advanced packaging.

That may well be true.

But there’s a big difference between a technology that matters in the long run and one that is investable today.

In this piece, I break down:

* Why glass core substrates and glass interposers are fundamentally different theses

* Why the physics is compelling, but yield, reliability, and manufacturing scalability still matter

* How incumbents like ABF substrates are responding

* What signals would suggest this theme is moving from expectation to reality

I tried to keep this readable even without a deep semiconductor background.

Part 2 is out today.

This one shifts to the fuel cycle: where the bottlenecks are, why they matter, and how investors can position around them.

It’s meant as a high-level overview, with deeper breakdowns to come. I’ve also covered parts of this before on this account.

Can be found by link in bio + comments

@emadtechfan Physical teust vs equities is included: demand outlook in terms of HALEU also (not the amount of SMR’s because output varies wildly! Utility contracting cycles is more @MarkosAAIG and @GyujinAAIG their sector!

Tomorrow i will post part 2 (the follow-up) of the Uranium thesis on Substack. It will be about big players in the market, enrichment and its effect on Uranium prices and in the end some possible ways to play it. Would there be other things about uranium you would be interested in to read about?

@martijnde_boer Will cover them next time!

Commercialization of HALEU (Fuel that TerraPower uses) is already a bit described in my X-Articles

Substack is in link in bio!

Isotopes are hard - Haleu is very hard

But completing phase 1 and full ramp-up phase 2 is not only at least several months (years) with execution problems but also the helium market could recover in the meantime.

But agree with you people expecting short-term profits exploding do not understand the nature of the business.

@baclofino@MarkosAAIG Understand your point

But Russia downblending and selling to the west is imo done after US ban on import + current geopolitics.

Also downblending would just push the gap forward and make it even bigger.

Spent a while putting together a two-part deep dive on what I think is one of the more underappreciated supply stories out there right now in the perfect storm: the uranium crunch behind the AI-nuclear buildout. Link in the comments below.

Part 1 is out now. It covers:

– Why Big Tech has quietly committed 12.5 GW of nuclear power in under 18 months

– What Fukushima actually did to the uranium supply chain (hint: it's worse than most people think)

– Why new mines take 10–20 years to build, and why that matters a lot right now

I tried to keep it accessible, no finance background needed. That said, I kept it focused and didn't go into every detail. For the people who read my earlier articles here on X, it is very readable and maybe basic info. It is my first post on Substack and would love feedback or posts you would like to read.

If you have questions or want me to go deeper on anything, drop them below@ happy to answer 👇

To jump in:

Obviously clinical growth is lowballed. Problem here is they probably do not have sufficient data to say something about the decline of the behavioural. If conversion stays at 30% there is no problem because ARPU is about 5x. But it surprised me they were this restrained in their explanation on forecast