- Stanley Druckenmiller -

"I'm constantly fighting my bearishness about the world. One of the great hedge fund managers of all rime, Bob Wilson, greatest short seller ever, said he made 90% of his money on the long side, the math just works against you. If you're perfect on a short, you can double your money. But if you're wrong on a short, you can lose 10 times your money. If you're dead wrong on a long, you lose your money. But if you're right, you can make 10 times your money. It's a mathematical inverse of that with shorting. You don't have to be a rocket scientist. I know, therefore, that if you have a bearish bias, you have to be very aware of it. You have to work around it. And I always have."

Thoughts from Michael Hartnett | Post-bubble roadmap

Zeitgeist quote: “Buy on the cannons, sell on the trumpets”, Baron Rothschild

The current AI-driven equity rally increasingly resembles a late-stage speculative bubble: extremely narrow market leadership, stretched valuations (S&P trailing P/E ~29x), euphoric positioning, collapsing volatility, massive IPO supply ahead, and excessive concentration in mega-cap tech. He argues that central banks still remain too loose globally, which is prolonging the bubble, but once policy tightening meaningfully bites, the unwind could resemble prior historic post-bubble rotations.

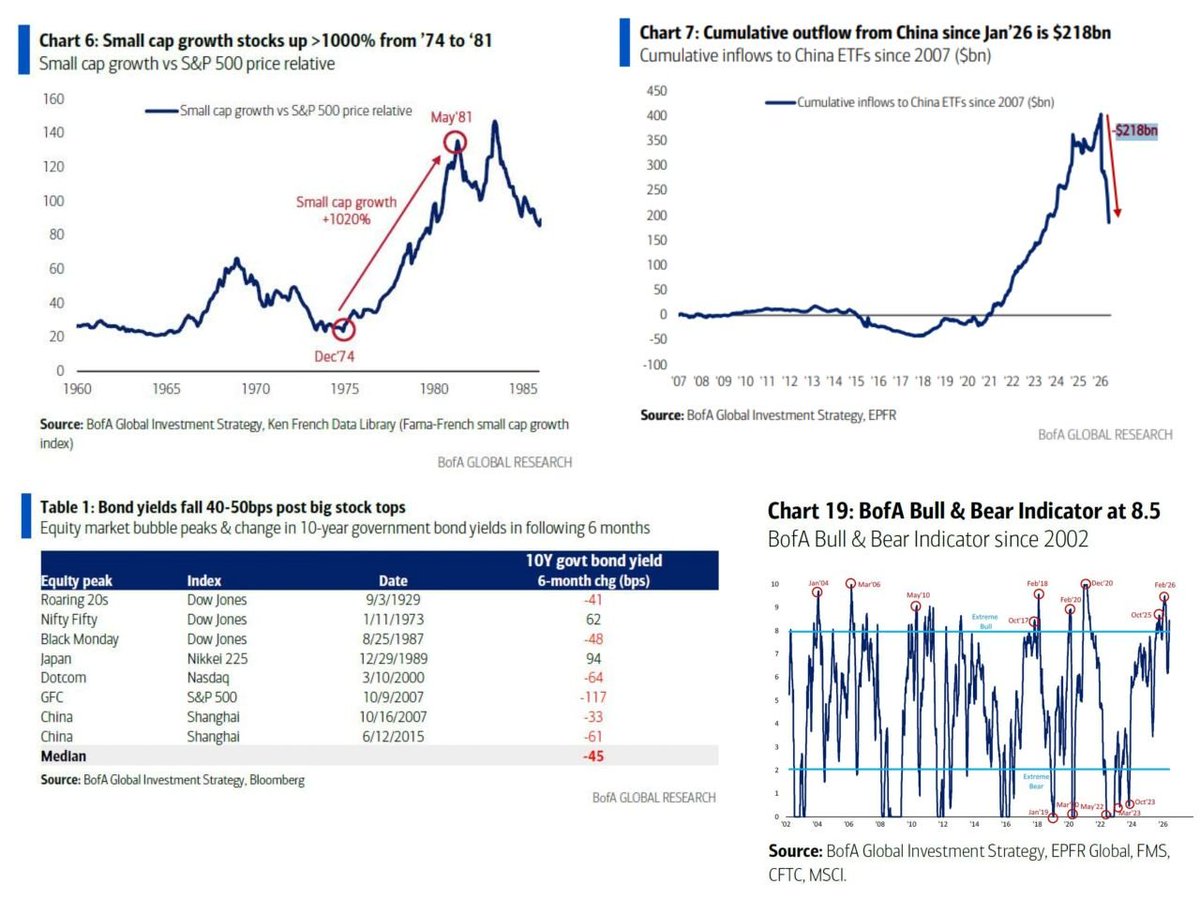

“Post-bubble roadmap” is heavily based on historical analogs (1929, Japan 1989, Dotcom 2000, China 2007). Historically, after bubbles burst:

- long-duration government bonds tend to outperform (10Y yields usually fall ~40–50bps within 6 months),

- the bubble leaders underperform sharply,

- and previously “humiliated” sectors outperform (“long humiliation, short hubris”).

The likely winners after an AI bubble unwind would be:

- defensive sectors (staples, healthcare, some financials),

- oil-sensitive consumer plays,

- small-cap growth / AI adopters rather than AI infrastructure “builders” (e.g. semis),

- and opportunistic, low-leverage alternative asset managers able to acquire distressed assets.

Warning signals:

- only a tiny fraction of stocks are making new highs despite index records,

- BofA Bull & Bear indicator is at extreme bullish levels (8.5),

- breadth indicators are approaching historical sell-signal territory,

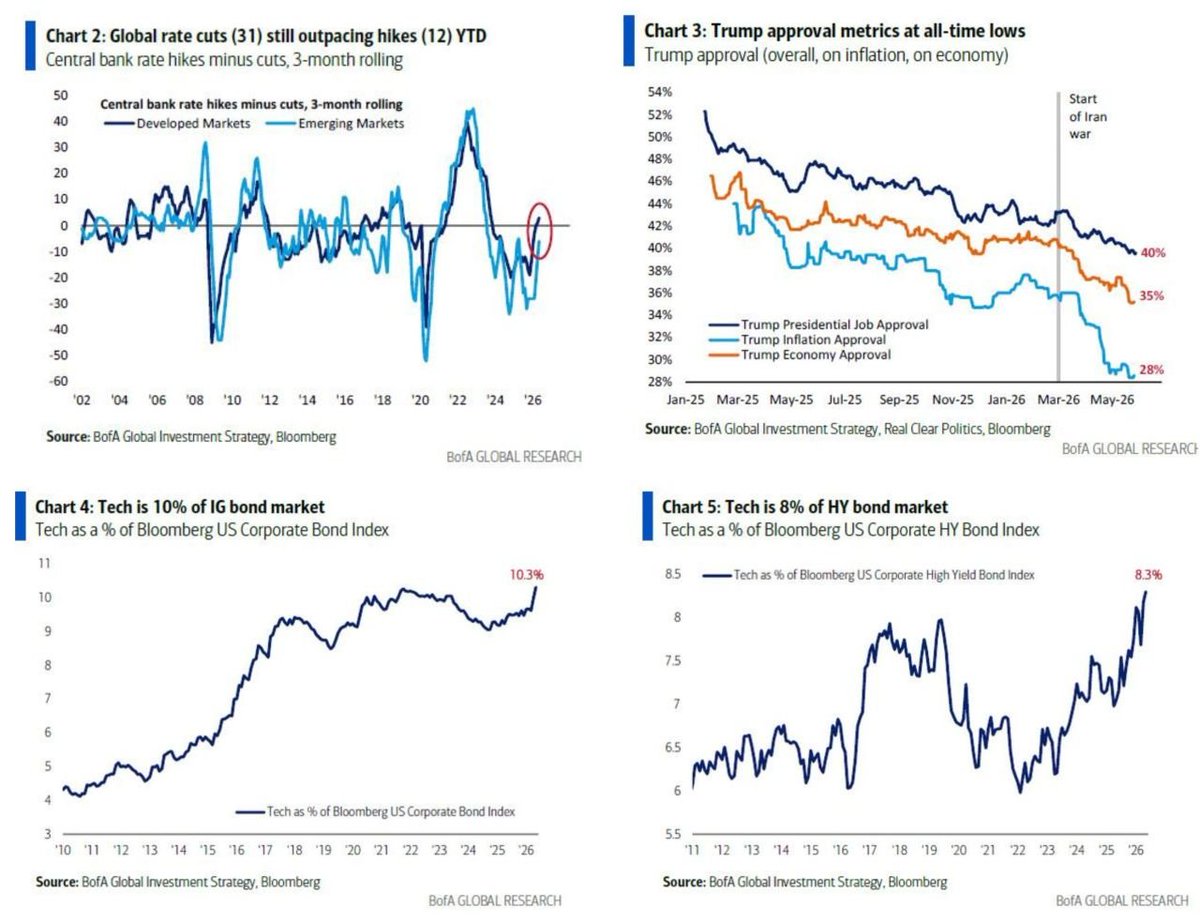

- tech now dominates both investment-grade and high-yield bond markets,

- and June is packed with macro/event risks (CPI, central bank meetings, large issuance, geopolitics).

Thoughts from GS | Late-Cycle Speculation?

The explosive rise in leveraged single-stock ETFs tied to AI winners such as NVIDIA, Tesla and SK Hynix is being viewed by Goldman Sachs as a sign of increasingly speculative and crowded market behavior, with investors aggressively chasing amplified exposure to the AI trade.

While AI fundamentals and DRAM demand remain extremely strong for now, the rapid inflow into leveraged products suggests a potentially unstable momentum-driven environment that could unwind sharply if sentiment weakens, positioning reverses, or expectations around AI growth begin to disappoint.

Thoughts from Michael Hartnett, BofA | This Is The Biggest Bubble Since The Railroads

The current AI-driven market rally resembles one of the biggest speculative bubbles in history, comparable to the Nifty Fifty or dot-com era, but investors are unlikely to aggressively sell before two catalysts occur: a major OpenAI/SpaceX-style IPO cycle and a clear Fed policy tightening shock tied to rising CPI from tariffs and inflation.

•AI mega-caps now dominate market concentration, with the “AI bubble” larger than past railroad, Japan, and dot-com bubbles by some metrics.

•Bond yields are the main warning signal: the rise in long-term yields and global cost of capital seen as dangerous for risk assets, especially leveraged consumers, private equity, housing, and emerging markets.

•Several macro stress signals are flashing: weak Asian currencies (KRW, JPY, INR, IDR), widening high-yield spreads, EM outflows, and BofA’s Bull & Bear Indicator hitting a contrarian “sell” level.

•Historically, speculative IPO waves (Alibaba, NTT, Visa, etc.) often marked medium-term market tops rather than immediate crashes.

•Current gains are very narrow (“wealth effect, not wage effect”), while equal-weight consumer stocks remain weak versus the S&P 500.

•Despite near-term bubble concerns, structurally bullish on emerging markets and commodities.

•Preferred post-bubble opportunities would be consumer stocks and smaller AI adopters/disruptors rather than dominant mega-cap AI platforms.

•Geopolitics, energy, AI competition with China, and inflation are increasingly interconnected themes shaping markets.

Zeitgeist quote: “Everyone is now convinced that equities are the best inflation hedge.”

Feedback from recent London trip, main soundbites:

•“we’re long and paranoid,”

•“wants/needs to de-escalate Iran, and stocks pop, yields drop on deal,”

•“if UK gilts find love, everything finds love,”

•“European electorate shifting decisively right, Farage in UK, Le Pen in France, and you watch the AfD in Germany will win Saxony-Anhalt in September, their first state election,”

•“the fear in bonds is nowhere near as strong as greed in equities,”

•“Warsh will be rhetorically hawkish but practically dovish over the summer,”

•“US actions in Venezuela, Ukraine, Iran, Greenland, Cuba should be viewed through single strategic lens competition with China in AI, which can only be won by securing access to critical resources.”

Dam I miss a lot of my brothers extra today! Take a shot today for all those that paid the ultimate price for us to the call this beautiful country home

🇺🇸🇺🇸 GOD BLESS AMERICA 🇺🇸🇺🇸

Thoughts from Scott Rubner | Citadel Securities

💥 Flow Fragility 💥

The setup today looks materially different from where we stood in late March. The market is no longer under-owned, under-positioned, or heavily hedged. Many of the flows that fueled the rally now appear significantly more mature. Higher long-end rates are starting to compete with equities once again.

Our framework for evaluating the current setup breaks down into 10 key themes across fundamentals, flows, positioning, and market internals:

1. Fundamentals: Q1 earnings confirmed the rally, delivering the strongest reporting season since the post-COVID recovery, with AI increasingly becoming a genuine earnings story rather than simply a narrative.

2. Flows: Passive inflows, buybacks, retail participation, and levered ETF exposure have all surged alongside the rally — but many of these same flows now leave the market increasingly exposed to a short-term unwind should momentum begin to fade.

3. Positioning: Systematic exposure has rebuilt sharply, demand for downside hedging has collapsed, and the market has increasingly shifted into a “spot up, vol up” regime driven by upside call chasing.

4. Internals: Breadth remains historically narrow, the rally stays heavily concentrated in mega-cap technology, and the market no longer appears well-hedged beneath the surface.

Thoughts from Michael Hartnett, BofA | Door To Doom Has Opened

Markets are entering a dangerous late-cycle “melt-up” phase similar to 1999 (dot-com bubble) and 2009, driven by a combination of:

•rapidly rising US Treasury yields (10Y and 30Y above key resistance levels)

•persistent inflation risk (US CPI potentially moving back above 5%)

•extreme concentration and valuation in AI/semiconductor stocks

•a widening disconnect between stocks and bond markets.

•Once long-term yields break higher decisively, a bond market shock could trigger a sharp correction in equities.

•Semiconductor stocks are behaving similarly to historical bubbles, with the SOX index trading far above long-term averages.

•Current market behavior resembles prior speculative peaks where both stocks and yields surged together before instability followed.

•US household wealth has been massively inflated by equities, reinforcing a self-sustaining “boom loop.”

•Political backlash from inflation and inequality could eventually shift capital away from AI/chips toward more consumer-focused sectors.

The market is not necessarily at immediate collapse, but the combination of high yields, sticky inflation, AI euphoria, and stretched valuations creates conditions historically associated with bubbles and elevated systemic risk.