An interesting phenomenon: Most protocols optimize "rewards," but few seriously design the "path after a loss."

However, from a system perspective, what truly determines whether a user stays is often not how much they gain, but what happens when they lose.

Origo is addressing this neglected path.

#Origo #DeFi #Insurance #SystemDesign

Insurance hasn’t evolved as fast as digital markets have.

Origo is building a decentralized protection layer for both on-chain and real-world risks — designed to be more transparent, efficient, and automated.

#OrigoInsurance#Web3#DeFi

Most people enter the crypto market to make more money.

But few ask: Who will cover losses if they occur?

Origo exists to provide the answer to this question.

#Origo#DeFi#Insurance#Crypto

In the crypto world, most people make decisions quickly: enter, trade, exit.

But few stop to consider one crucial thing—what if things go wrong?

Origo doesn't influence your decisions,

it prepares answers for "after the decision."

#Origo#DeFi#Insurance#UserFocus

If "security" had a shape in the crypto world,

it might look like this—stable during market volatility,

reacting before risks materialize.

Origo's attempt isn't to eliminate your worries,

but to make your worries meaningful.

#Origo#DeFi#Insurance#Protection

What is the purpose of insurance?

Is it to compensate for losses, or to provide confidence?

At Origo, we focus more on the latter—to allow users to make decisions with less hesitation.

In the crypto world, what kind of risk do you think most needs to be protected against? 👇

#Origo #DeFi #Insurance #Community

Risk never truly disappears;

it's simply redistributed.

What Origo does is allow the weight of risk to be shared by more people.

This isn't avoidance, it's balancing.

#Origo#DeFi#Insurance#RiskManagement

Volatility is the norm in the market,

but control is a systemic capability.

Origo cannot eliminate risk,

but it can stabilize the value in your hands when risk arises.

Over the past few weeks, we completed system stability testing, and the verification of the new insurance types has also passed smoothly.

Now, we are entering a new phase—more users, higher liquidity, and broader coverage.

The IPO plan is also progressing simultaneously.

🚀 Big news!

#Origo is preparing for its initial public offering (IPO) on an exchange—

But which one? 👀

We've been in talks with several major platforms,

and the final announcement is coming soon.

Leave a comment below 👇

Take a guess, and you might find out the result in advance.

#Origo #CryptocurrencyIPO #DeFi #Insurance

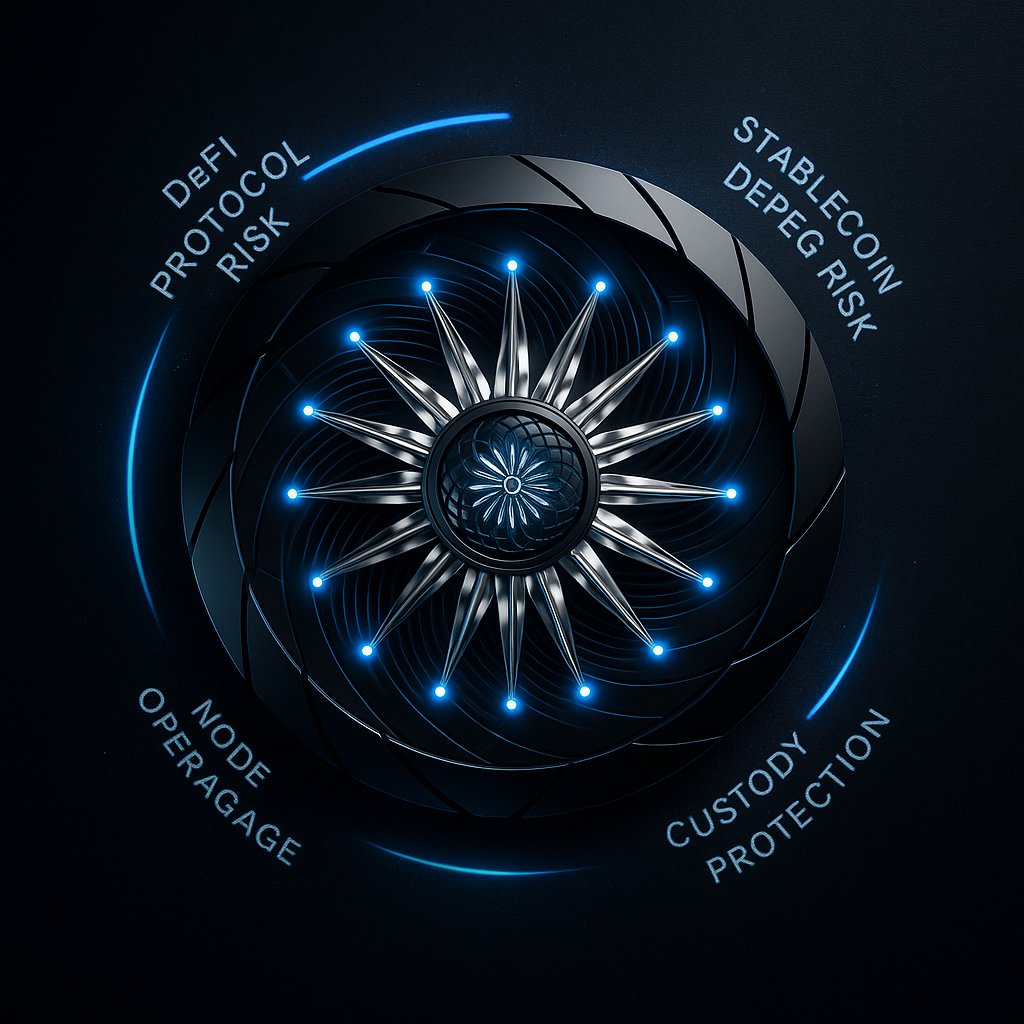

Over the past few weeks, Origo's system testing has entered a new phase: More insurance types have been integrated and verified.

Currently covered:

🔹 DeFi protocol risks

🔹 Stablecoin de-pegging risks

🔹 Custodial asset protection

🔹 Node malfunction protection

A new round of contract testing is also underway, and the scope of coverage is gradually expanding from "on-chain events"

to "real-world financial triggers".

Budgeting helps us control spending and alleviate financial pressure.

In the financial world, this is called "risk management."

Origo does the same thing:

it simply moves the budgeting logic onto the blockchain—ensuring that every flow of funds is within a controllable range,

making unexpected costs predictable.

A central Georgia insurance agency owner and former Alfa insurance agent of the year must serve more than two years in prison after he pleaded guilty to bank fraud and misusing more than $220,000 in... https://t.co/DFUy0mFev2

The purpose of regulation is not to restrict innovation,

but to give innovation boundaries.

Traditional insurance relies on regulations to maintain order,

#Origo puts order into code.

It's not about circumventing regulation,

but about making regulation more transparent and real-time.

In the traditional insurance system, regulation is often lagging—an accident occurs first, a report is submitted later, and accountability only begins last.

Data is closed off, and layers of inter-agency communication make transparency a luxury.

#Origo's regulatory logic is different: every claim record, risk event, and fund flow is publicly available and verifiable in real time.

This is not a rebellion against "regulatory absence," but rather a return of regulation to its rightful place—immediate, transparent, and credible.

Traditional insurance regulation is increasingly resembling "post-event management": documents, approvals, and accountability, but rarely real-time transparency.

User trust is diluted by layers of institutions, and claims efficiency is hampered by procedural delays.

#Origo's goal is not to replace regulation,

but to enable rules to self-enforce on the blockchain,

transforming regulation from passive oversight to proactive verification.

UBS Group AG’s chairman warned against looming risks in the US insurance industry, citing weak and complex regulations amid an unprecedented boom in private financing. “We’re... https://t.co/xK2i03jUQA