I went through the top crypto neobank cards

& ranked them by real onchain volume.

RedotPay leads with $5.8B.

Crypto cards are no going mainstream with

MoM growth at 12.8% 🆙 and May vol at $750M

X Articles are quietly becoming the new blog

I went from a new account to 300K+ views in a week by writing about what I love and understand

So I wrote a small article on why X articles are best way to build your audience 👇👇

few days ago I wrote

Eth looks dead, but the rails are getting stronger

now Tom Lee says ETH can hit $250K

the number is wild, but the thesis is real

wrote a deeper article on why eth is hard to ignore

Neobanks are just shiny frontends.

The real stablecoin rail is P2P.

Messy, local, decentralized, and built for where banks stop.

A small article on how no one is building on established p2p rail with over $300+ billion in yearly settlement with 50% yoy growth 🧵🧵

Next bank will be a stablecoin wallet - i can bet

A Complete Guide to Crypto Neobanks, Wallet Banks, Cards, and Borderless Accounts

The first neobanks gave people better banking apps.

The next neobanks will give people global money accounts

Shared my fav neobanks as well 🧵🧵

ETH looks dead.

But

// Stablecoins < 50% of all stablecoins on eth ~ $166.95B >

// L2s,

// RWAs,

// smart wallets

Are quietly turning Ethereum into the settlement layer for internet money.

Maybe the chart looks weak because the rails are getting stronger

1000s of new neobanks are coming.

But they won’t look like banks.

They’ll look like wallets, cards, apps, dashboards, checkouts, and AI agents.

The future bank may not hold your money. It will simply move it

I sent $1,000 from New York to Lagos through 8 payment rails. The best delivered ₦1,400,000. The worst delivered ₦1,323,000. That ₦77,000 gap = one month of groceries for a family in Lagos.

Yesterday's rail comparison got sharp feedback. The strongest critique: "Try this on a low-liquidity corridor. I bet stablecoins don't look the same."

Fair. So I redid the experiment on the hardest corridor I could find: Nigeria.

𝗪𝗵𝘆 𝗡𝗶𝗴𝗲𝗿𝗶𝗮 𝗯𝗿𝗲𝗮𝗸𝘀 𝘁𝗵𝗲 𝘂𝘀𝘂𝗮𝗹 𝗻𝗮𝗿𝗿𝗮𝘁𝗶𝘃𝗲:

The Naira isn't one currency. It's two.

→ The official CBN rate: ₦1,345 per USD. Banks, SWIFT, Wise, Western Union must use it.

→ The parallel market rate: ₦1,400 per USD. It's where real dollar supply meets real demand.

That 4% gap isn't a fee. It's the government pricing the naira higher than anyone is willing to pay for it.

𝗪𝗵𝗮𝘁 $𝟭,𝟬𝟬𝟬 𝗮𝗰𝘁𝘂𝗮𝗹𝗹𝘆 𝗱𝗲𝗹𝗶𝘃𝗲𝗿𝗲𝗱 𝗶𝗻 𝗟𝗮𝗴𝗼𝘀:

🥇 USDT P2P: ₦1,400,000 (30 sec, $0.01)

🥈 Yellow Card: ₦1,393,000 (2 min)

🥉 Bitcoin: ₦1,393,000 (~10 min)

4️⃣ Sendwave (International Remittance): ₦1,372,000 (15 min)

5️⃣ Wise: ₦1,344,000 (CBN rate)

6️⃣ Swift: ₦1,344,000 (3-7 days, $50 fee)

7️⃣ Western Union: ₦1,330,000

8️⃣ PayPal Xoom: ₦1,323,000 (5.5% hidden spread)

𝗛𝗲𝗿𝗲'𝘀 𝘄𝗵𝗮𝘁 𝘁𝗵𝗲 𝗰𝗼𝗺𝗺𝗲𝗻𝘁𝗲𝗿𝘀 𝘄𝗲𝗿𝗲 𝗿𝗶𝗴𝗵𝘁 𝗮𝗯𝗼𝘂𝘁:

That USDT P2P rate only exists because someone, somewhere, holds naira and wants dollars. The P2P desk IS the off-ramp. It's real infrastructure, with real liquidity risk.

But here's what they couldn't see on the Paris–NY corridor:

In a dual-rate economy, stablecoins aren't just faster. They give you access to a different price. The real price.

Nigeria has the world's 2nd-largest P2P crypto volume. Not speculation. Access to the actual dollar rate, without flying to Lagos with a suitcase.

The next decade's fintech question isn't "will stablecoins replace SWIFT?"

It's "what happens when 2 billion people in dual-rate economies realize they can bypass the official channel?"

₦77,000 on $1,000 tells me the question is worth asking.

PS: I'm the founder of @subyhq and I weekly posts on payments, stablecoins, and building across borders. Follow for more.

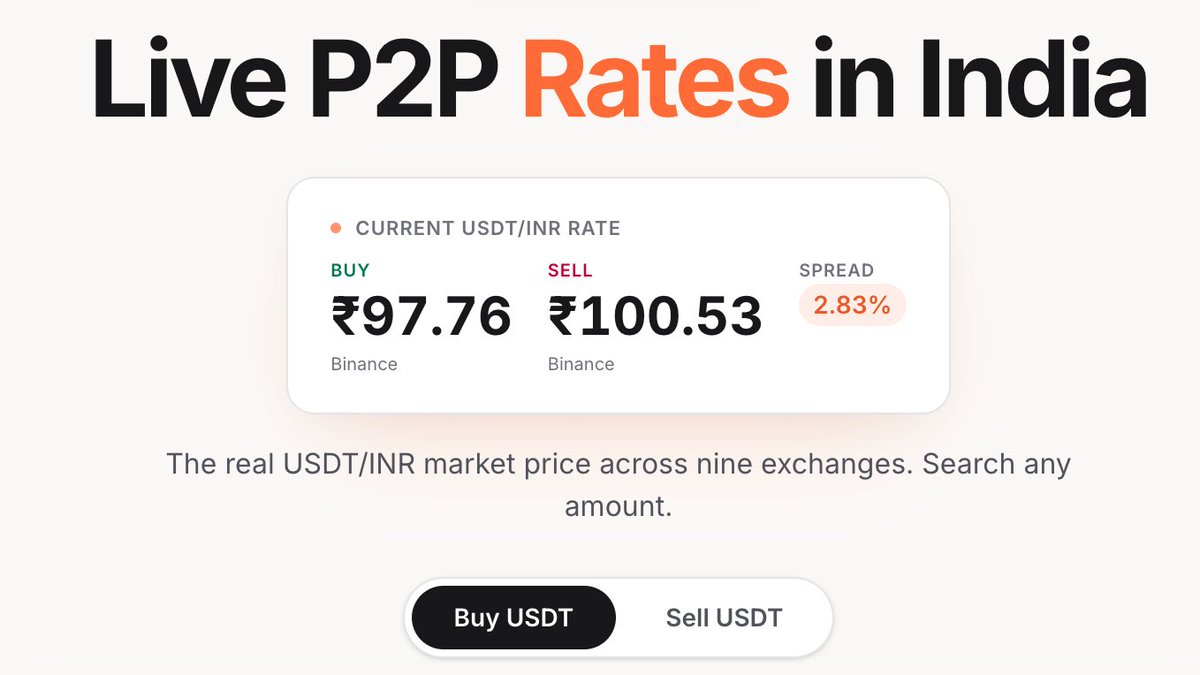

If you’re not tracking this, you’re leaking money every trade.

https://t.co/paObxbsaop shows the cheapest rates in real time.

Small % saved = massive edge over time.

If you’re not tracking this, you’re leaking money every trade.

p2prate.(live) shows the cheapest rates in real time.

Small % saved = massive edge over time.