Crypto has created a lot of loud personalities.

Then there’s @RichardHeartWin

Luxury watches. Ferraris. #HEX. #PulseChain. One of the most loyal communities in crypto.

Love him or hate him, nobody ignores Richard Heart.

@graminitha1 breaks it down👇

A genius billionaire representing thousands of consenting shareholders wants to voluntarily buy lots of permissionless Bitcoin from voluntary sellers using voluntary capital markets.

What should happen?

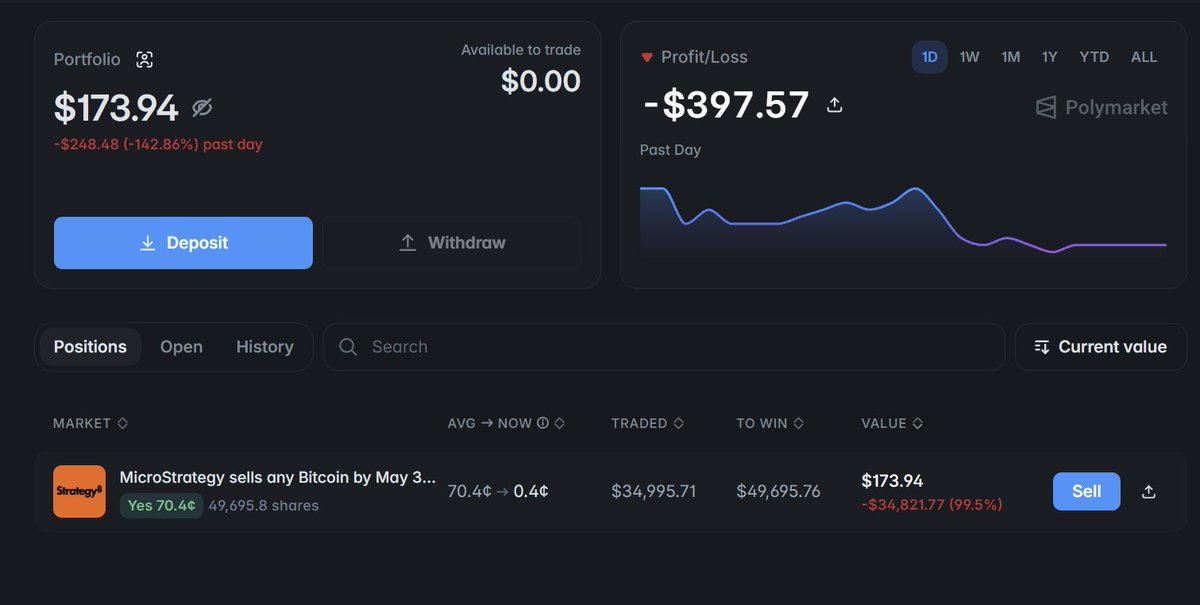

I’m 20 years old, still a university student.

Before this dispute, I was one of the top 10 YES holders in the Polymarket MicroStrategy market. I lost around 35,000 USDC because I trusted the written rule.

The rule said YES if MicroStrategy sold Bitcoin by May 31.

It did not say the sale had to be publicly disclosed by May 31.

That is the whole issue.

If you want to help:

Repost this.

Tag a journalist.

Tag a lawyer.

Send this to a crypto researcher.

Submit your case if you were affected.

https://t.co/pmXUtr9jFD

Silence is what platforms count on.

Don’t give them that.

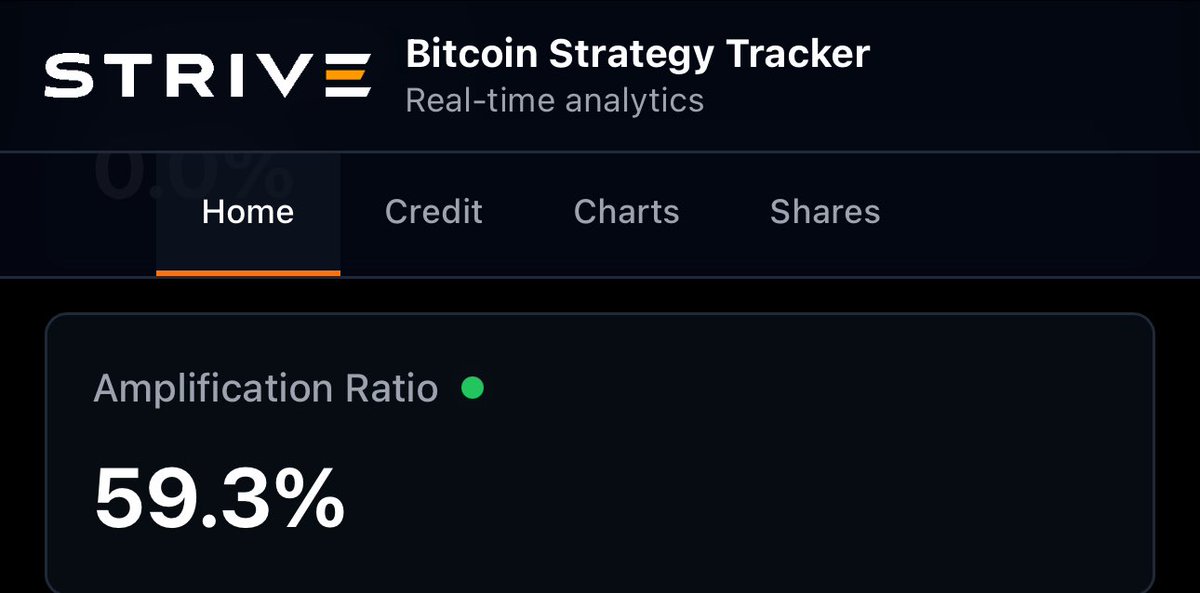

Deep dive this week on risk and how high the data suggests Strive could take amplification given our balance sheet.

The data can almost "feel" uncomfortable, but it's critical to understand and make business decisions based on data, not feelings.

Enjoy!

There is going to be a huge liquidity rush into STRC before the ex. div date on June 15th. As per usual.

But the rotation after that into SATA for the daily dividends is going to be HISTORIC.

Digital credit will provide lots of buying pressure for Bitcoin. Just getting started.

The reason why a lot of people are excited about ASST is that it is a very pure expression of an amplified Bitcoin bet that also has a very clear lane for growth and it has a small denominator.

The small denominator is huge. You cannot ignore base effect math.

Let me explain.

MSTR Bitcoin NAV: $62.28B

ASST Bitcoin NAV: $1.22B

MSTR is roughly 51x bigger. Great. You found the elephant.

But stock price math is:

Stock Price = CEBE/share × BTC Price × CEBE mNAV

And CEBE is:

CEBE = (Total BTC - Senior Claims in BTC) / Shares

So the real question is:

Who can grow common equity Bitcoin exposure per share faster?

Now make the test unfair in MSTR’s favor.

ASST raises $100M.

MSTR raises $1B.

MSTR gets 10x more capital.

Both buy BTC at $73.8K.

BTC rises 30% to about $96K.

Residual BTC created by the fixed-dollar senior capital:

ASST:

$100M × (1 / $73.8K - 1 / $96K) = ~313 BTC

MSTR:

$1B × (1 / $73.8K - 1 / $96K) = ~3,126 BTC

Now divide by each company’s common equity BTC base.

ASST:

313 / 10,675 = +2.93% CEBE lift

MSTR:

3,126 / 573,757 = +0.55% CEBE lift

So even when MSTR raises 10x more money, ASST still gets about 5.4x more CEBE torque.

Why?

Because MSTR’s common BTC base is about 53.7x larger.

53.7x larger denominator ÷ 10x larger raise = 5.37x more torque for ASST.

That is the smaller base effect.

MSTR is the Bitcoin fortress.

ASST is the speedboat strapped to a flaming preferred-stock engine.

If BTC price and CEBE mNAV are held constant, the stock price race comes down to CEBE/share growth.

This is not astrology.

This is denominator physics.

I fully believe ASST is going to $100 in short order.

Here I use the CEBE framework to totally declaw the Strive bear case and project out what the daily SATA dividends are going to do for ASST shareholders:

Value is subjective at the valuation layer.

Claims are measured at the capital stack layer.

Those are not the same thing.

A house’s market value is subjective. Fine.

But if the house is marked at $500k and the mortgage balance is $350k, your equity snapshot is $150k.

The bank’s claim is not unknowable because buyers may disagree on the house’s future value.

Same with CEBE.

The market can debate:

What BTC is worth, what future BTC CAGR should be, what multiple the residual deserves, whether preferreds are scary or brilliant, and whether management can compound exposure.

But the snapshot can still say here is the BTC stack, here are the senior claims, and here is the residual exposure for common under this claim basis.

Bitcoin exposed that most adults have no idea what money is.

They think money is green paper because their dad said so in 1998 while refinancing a split-level ranch and yelling at the grill.

Ask them what backs the dollar and they start making the same face a golden retriever makes when you pretend to throw the ball.

The orange coin broke the spell.

Now everyone has to do monetary theology at gunpoint.

I agree.

We spend a tremendous amount of time thinking about downside risk, stress testing scenarios, and building protections accordingly. In our view, $ASST is not over-amplified. If anything, we believe it remains under-amplified relative to the opportunity set Bitcoin presents.

It’s important to understand that risk management is a constraint, not the objective.

The goal for Strive’s common equity, $ASST, is to outperform Bitcoin and maximize long-term shareholder returns.

Importantly, we are not trying to optimize away every last basis point of risk. There is a meaningful difference between reducing the probability of failure from 10% to 1% and reducing it from 0.02% to 0.01%. The latter may technically cut risk in half, but from an expected value perspective it is immaterial if the tradeoff is materially lower upside.

This philosophy informs every major capital allocation decision we make. We start by protecting against outcomes that could permanently impair shareholder value. Once that threshold has been met, our focus shifts to maximizing expected value.

In our view, risk is not measured solely by the probability of loss. It is also measured by the opportunity cost of failing to fully participate in a highly asymmetric outcome.

That is why we intentionally have no debt, maintain substantial dividend reserves, and run amplification aggressively. We seek to eliminate risks that could permanently impair shareholder value so that we can maximize amplified participation in Bitcoin’s upside.

We believe Bitcoin’s return distribution will continue to be highly asymmetric to the upside. If there is a meaningful probability that Bitcoin compounds dramatically over the coming decades, the optimal capital structure is not the one that sacrifices substantial upside to marginally improve an already remote downside outcome. It is the one that preserves resilience while maximizing participation in that upside.

This is also why we are focused on acquiring as much Bitcoin as we can while it remains below $100,000. We believe Bitcoin is likely to be substantially higher over time and that periods where Bitcoin trades near its 200-week moving average are precisely when amplification should be run as aggressively as prudently possible.

We think in probabilities, expected values, and equity compounding. If you optimize around fixed income math, you should expect fixed income returns.

We built the company we personally wanted to own: an engine designed to maximize Bitcoin per share growth, outperform Bitcoin, and maximize shareholder value across a wide range of bullish Bitcoin outcomes.

MSTR to $3,800 per share.

Assumptions:

$1B/month preferred issuance only

11.5% preferred cost

30% BTC CAGR

1.32x CEBE mNAV, no expansion EVER

common stock sold to pay dividends

zero common stock sold to buy Bitcoin (LOL)

Start:

843,738 BTC

573,757 common equity BTC

163,144 CEBE sats/share

$158.97 implied price

Year 10:

1,424,686 BTC

1,287,186 common equity BTC

285,605 CEBE sats/share

$3,836.60 implied price

That is 24.1x in the model.

The insane part?

Preferred balance goes from $15.5B to $135.5B, yet senior claims fall from 270K BTC to 137.5K BTC.

Why?

Because fixed fiat claims get vaporized when measured against a compounding Bitcoin treasury.

This is Ownership Acceleration.

CEBE sats/share rise 75%.

Common equity BTC rises by 713K BTC.

Bears see “debt” and “dilution.”

The model sees fiat claims being dragged behind the Bitcoin monster truck at 3 AM while Saylor is doing laps around the sovereign bond market.

Even the bearish assumptions make me a very rich man.

CEBE is the scoreboard.

Bullish Strategy.

The little wick to $99.97 getting bought up instantly is the potential to what daily dividends could look like.

Every. Single. Day.

$ASST has a clear growth path to being the fastest growing company in the world and it’s well deserved with what they have built.

It's frankly ridiculous that Strive even has to pay 13% w/ SATA but HEY we live in an insane world.

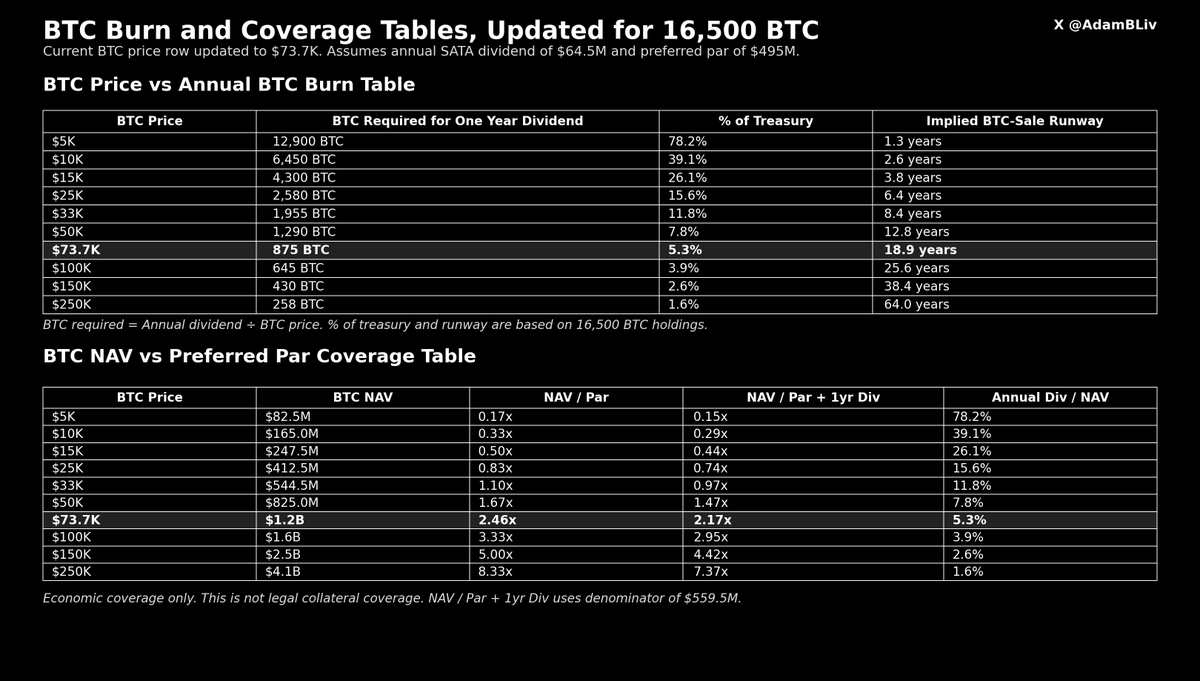

At $73.7K BTC, Strive’s 16,500 BTC treasury is worth about $1.2B.

The annual SATA dividend is roughly $64.5M.

That means one full year of dividends equals:

875 BTC

5.3% of the treasury

18.9 years of BTC-only runway

2.46x economic coverage of preferred par

2.17x coverage of par plus one full year of dividends

This is ignoring their cash reserve.

This is ignoring their STRC.

This is ignoring their ability to raise more cash with ASST sales.

This is ignoring their ability to get more cash w/ BTC derivatives.

It ignores the fact that SATA has no ordinary bond-style maturity wall and no SATA-level forced liquidation mechanism.

If you’re bullish on Bitcoin, how exactly does this break without inventing some apocalyptic tail-risk scenario where Bitcoin permanently dies, capital markets close forever, and every board member starts making decisions like they were hired from a regional bank’s 2023 risk committee?

The BITCOIN NIHILISTS are in shambles.

If the only way SATA fails is by assuming Bitcoin itself structurally fails, then just say you’re not bullish on Bitcoin.

Much cleaner.