$NTNX looks even more attractive after earnings.

Not a hypergrowth SaaS anymore, but a reasonably valued infrastructure software compounder with strong FCF, no typical high-dilution SaaS profile, and mid-teens growth supported by VMware/Broadcom migration, external storage and AI infra.

The AMD partnership adds another upside layer.

Technically, it is now pushing into the 200W SMA and looks close to finishing its correction. I don’t expect 30% overnight moves here, but steady compounding from a healthy software infrastructure name.

Good spot for those still not positioned.

$ZS reported pretty much in line with expectations.

The market didn’t like the lower FCF outlook, but the reason seems to be higher investments in future growth — and that almost never ends well in after-hours trading.

Personally, I don’t have a problem with a company investing in its future, especially in cybersecurity, where AI should only increase the need for strong enterprise-grade protection.

For me, the $145–155 range looks attractive enough to add to my position.

Not blindly, not aggressively — but as part of building a long-term position in one of the more interesting cyber names at a much more reasonable valuation.

I believe power / energy / nuclear will be the next major cycle after semis.

AI infrastructure was first priced through chips, networking and data center hardware. But the next bottleneck is becoming obvious: power.

$SMR looks like an interesting spot to start a position.

Volume is rising, a higher low seems to be forming (hammer candle on weekly), and MACD has already made a golden cross. The trend is not fully confirmed yet, as price still needs to reclaim the 200W SMA.

For me, this could be a good place for a small starter position, with room to add after confirmation.

I believe power / energy / nuclear will be the next major cycle after semis.

AI infrastructure was first priced through chips, networking and data center hardware. But the next bottleneck is becoming obvious: power.

$SMR looks like an interesting spot to start a position.

Volume is rising, a higher low seems to be forming (hammer candle on weekly), and MACD has already made a golden cross. The trend is not fully confirmed yet, as price still needs to reclaim the 200W SMA.

For me, this could be a good place for a small starter position, with room to add after confirmation.

$VST and $TLN are both at critical technical moments.

Neither chart looks easy right now. Both need confirmation, both are testing important levels, and both can still shake people out before the next real move starts.

But fundamentally, I still deeply believe in both stories.

$VST probably looks more attractive from a valuation perspective here, especially after the recent weakness. The chart is painful, but the long-term risk/reward is becoming very interesting again.

$TLN, on the other hand, still has better price dynamics. It already made a higher high above $400, and the current move looks more like a retest than a full breakdown — as long as the key structure holds.

The bigger picture remains the same for me:

👉AI power producers will have their time.

Semis were the first obvious bottleneck. Power may be the next one. You can build more chips, more racks and more data centers, but at some point the question becomes very simple - where does the electricity come from?

That is why I still want exposure to this theme.

The charts are at critical levels, but the long-term thesis is not broken.

For me, $VST and $TLN remain two of the most interesting AI infrastructure plays outside semiconductors.

@BourbonCap At current prices, $VST looks more attractive, but $CEG is getting there as well.

I’ve been accumulating $VST around $140–150 and added more in the $130s. For $CEG, I’m still waiting for the 05/01/2025 gap to fill before getting more interested.

$NTNX, $ZS, and $RBRK are up around 50% since this tweet.

$TMDX is unfortunately down about 50%, but I don’t mind adding to this name at these levels.

Overall, adding during the Anthropic-driven SaaS/cybersecurity slaughter proved to be the right move back then.

For the record, today I added to $RBRK, $ZS and $NTNX, but not to $ZETA.

I’m getting very close to moving the whole $ZETA position into $TMDX.

If there is an area where AI can really cause disruption, it is commerce, marketing, and of course automation.

$VST is inching closer to closing the gap around $130, and $TLN is getting closer to the $270 area.

I liked $VST at $150, so I definitely won’t complain if I get a chance to add around $130.

Same with $TLN. I liked it at $330, but around $270 — right near the 100W SMA — the risk/reward would look even better.

Can’t wait for both.

As for $CEG, the gap around $223 is the level where I’d finally become interested in opening a position.

AI power producers are still one of my favorite long-term themes and one of obvious bottlenecks for years to come.

And regarding $SOFI ...in my opinion, all rate-sensitive fintech names — even those that look extremely undervalued on the numbers, like $PGY — are likely dead money until bond yields finally move lower. So is it worth accumulating? Long term, probably yes. But the opportunity cost...

@mathlonning I mentioned $MELI because they’re being punished right now for a similar reason as $NU.

I’ve been watching $SOFI for some time, but I haven’t decided to step in yet.

@mathlonning I’m accumulating both $MELI and $NU with a long-term view. Margins are clearly under pressure right now, but in my opinion this is more like compressing a spring than a structural problem.

Definitely worth listening to. https://t.co/LDuPnltA5m

Que joyita de $NU sacaron ayer.

Lago, Jeremy & Tyler te explican como a un niño como hay que ver provisiones contables de un book de credito que crece rapido desde la optica de un investor. Sound familiar? Y si porque es lo mismo que le pasa a $MELI.

You can’t make this shit up.

De paso te explican como usan IA para credit underwriting. De acuerdo a Bain & Co el revenue pool de global banking van a ser approx 15- 17 trillion USD para 2030. Es la industria mas grande del mundo. Y BTW credit es el ~60% -70% del profit pool total. Osea si no haces credito bien no existis.

No tiene desperdicio. Los mejores 30 minutos gastados un sabado.

Yeah, that actually makes sense. Since April, most stocks outside of space/rockets and AI basically haven’t moved much, while many of them remain fundamentally attractive.

Now software/SaaS is finally starting to move, and hopefully others will follow. I’m also waiting for the end of the correction in semis, because it should get interesting there again pretty soon.

Another day when this approach proved to be the right one.

Profits from semis and AI infrastructure are working for me in $HROW, $TMDX, healthcare, and SaaS names like $ZS, $RBRK, $NTNX, $RDDT, and $OSCR.

Still waiting for energy producers like $VST and $TLN — but their time will come.

The recent heavy drops in two of my Top 5 conviction stocks, $HROW and $TMDX, made me rethink the portfolio structure.

Both companies delivered negative surprises and were punished hard, but if the long-term theses remain intact, the sell-offs pushed them into very attractive territory (like $OSCR some time ago)

At the same time, my semis / AI infra picks — $NBIS, $MRVL, $ALAB, $CRDO, $NVTS, $AMKR, $GLXY, $CIFR — had tremendous runs in a very short period of time. With $SPY and $QQQ overbought for weeks, I expect this group to take a breather.

So I decided to close and take profits in semis / AI infra and keep monitoring them for re-entry.

I already increased $HROW and $TMDX and will look to add more on the right occasions.

👉I’m keeping $ZS, $RBRK, $NTNX, $RDDT, $OSCR, $VST and $TLN, as I believe the best is still ahead there. I also plan to keep adding to the names I decided to leave in the portfolio when the setup is right.

👉I’m also keeping beaten-down consumer-facing fintech, payments and ecommerce names — $FOUR, $DLO, $PGY, $NU, $MELI, $SE, $CPNG — as I think many of them are winding the spring for the next cycle and future margin expansion.

The cycle for payments / fintech may come a bit later than cybersecurity / software, but I believe it will come. So yes, there may be some opportunity cost in holding them now, but investing is also about positioning for the next cycle before it becomes obvious.

In parallel, I’ll keep looking for rare earth, metals, SaaS and power provider names.

$CEG is definitely not my favorite name in this group.

I like it much less than $VST and $TLN, mainly from a valuation perspective.

Technically, just like $VST and $TLN, it is also sitting at an important level. But to me, the chart already looks like it may have crossed the river to the wrong side.

If $CEG fails to hold this trendline, the next level to watch is around $245.

And if price then makes a lower low, the downside could open much further — potentially all the way toward closing the April 2025 gap.

So for now, I still prefer $VST and $TLN as my main AI power producer plays.

$VST and $TLN are both at critical technical moments.

Neither chart looks easy right now. Both need confirmation, both are testing important levels, and both can still shake people out before the next real move starts.

But fundamentally, I still deeply believe in both stories.

$VST probably looks more attractive from a valuation perspective here, especially after the recent weakness. The chart is painful, but the long-term risk/reward is becoming very interesting again.

$TLN, on the other hand, still has better price dynamics. It already made a higher high above $400, and the current move looks more like a retest than a full breakdown — as long as the key structure holds.

The bigger picture remains the same for me:

👉AI power producers will have their time.

Semis were the first obvious bottleneck. Power may be the next one. You can build more chips, more racks and more data centers, but at some point the question becomes very simple - where does the electricity come from?

That is why I still want exposure to this theme.

The charts are at critical levels, but the long-term thesis is not broken.

For me, $VST and $TLN remain two of the most interesting AI infrastructure plays outside semiconductors.

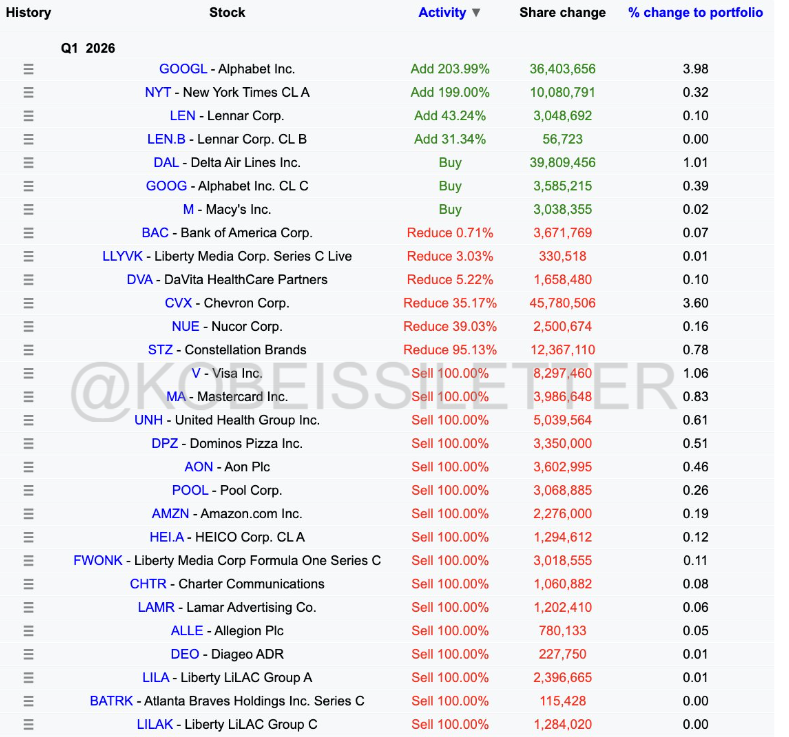

BREAKING: Berkshire Hathaway discloses new purchases of Alphabet, $GOOGL, Macy's, $M, and Delta Airlines, $DAL.

Berkshire Hathaway has also exited its entire position in Amazon, $AMZN, UnitedHealth, $UNH, and Dominos Pizza, $DPZ.

The news of the day is that the CEO and CFO of $HROW bought 13,500 shares after the recent drop.

Seems like my plan to go overweight both $HROW and $TMDX might actually make sense.

Today’s green day for SaaS and cybersecurity, despite $SPY being down around 1%, also shows that the rotation might be working.

The recent heavy drops in two of my Top 5 conviction stocks, $HROW and $TMDX, made me rethink the portfolio structure.

Both companies delivered negative surprises and were punished hard, but if the long-term theses remain intact, the sell-offs pushed them into very attractive territory (like $OSCR some time ago)

At the same time, my semis / AI infra picks — $NBIS, $MRVL, $ALAB, $CRDO, $NVTS, $AMKR, $GLXY, $CIFR — had tremendous runs in a very short period of time. With $SPY and $QQQ overbought for weeks, I expect this group to take a breather.

So I decided to close and take profits in semis / AI infra and keep monitoring them for re-entry.

I already increased $HROW and $TMDX and will look to add more on the right occasions.

👉I’m keeping $ZS, $RBRK, $NTNX, $RDDT, $OSCR, $VST and $TLN, as I believe the best is still ahead there. I also plan to keep adding to the names I decided to leave in the portfolio when the setup is right.

👉I’m also keeping beaten-down consumer-facing fintech, payments and ecommerce names — $FOUR, $DLO, $PGY, $NU, $MELI, $SE, $CPNG — as I think many of them are winding the spring for the next cycle and future margin expansion.

The cycle for payments / fintech may come a bit later than cybersecurity / software, but I believe it will come. So yes, there may be some opportunity cost in holding them now, but investing is also about positioning for the next cycle before it becomes obvious.

In parallel, I’ll keep looking for rare earth, metals, SaaS and power provider names.

$CLPT — even on deep red days like today, the bigger picture still shows improving strength when you look at the main weekly indicators like RSI and MACD.

MCDX also suggests that institutions have been accumulating.

Technically, the price reclaimed the 200W SMA, but then rejected from the 50W SMA from below. At the same time, it is still holding above the 20D EMA, so the range between these key levels is getting tighter and tighter.

Fundamentally, $CLPT is still very much a “future story.”

I have been in this position since early 2025, so I participated in both the big run and the big drop after the $QURE drama. I have also been adding below the 200W EMA.

Given the most likely recent changes around the FDA setup, the potential rerate could be very sharp once the market starts pricing in a better regulatory environment.

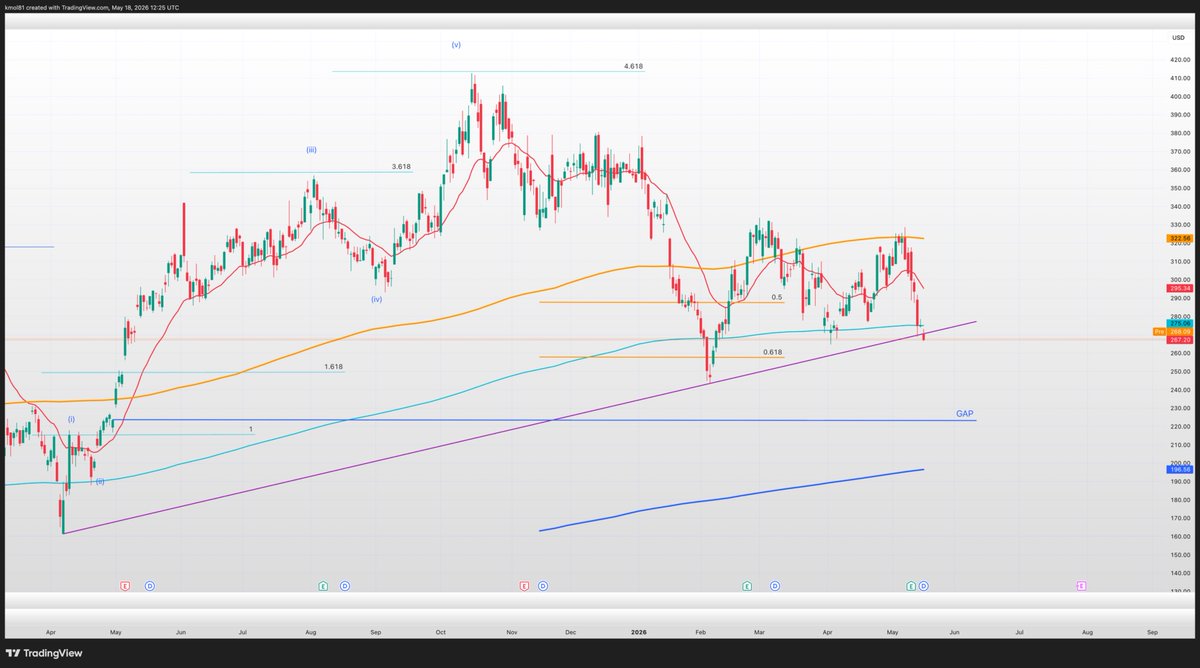

$VST is now forming a small hammer candle right around the 0.618 retracement. Looks like a make-or-break level.

If it doesn’t hold, the next stop is most likely the 2025 gap around $130.

Power / energy providers look completely deserted right now and have been beaten down after the hot CPI print, which may create a good opportunity for long-term buyers.

Keep in mind that $VST now trades at around 16x NTM EPS, while EPS is expected to grow at roughly a 50% CAGR over the next two years. And the current guidance still does not fully reflect potential upside from Cogentrix or parts of the Meta PPA, which should start contributing more meaningfully from 2027.

Fundamentally, the story still looks very attractive to me as a long-term buy. I’ve been accumulating since February.

Technically, however, the setup is not great yet. RSI remains weak and MACD is still weak as well, although the 0.618 retracement continues to hold for now.