Gold’s price dance seems mysterious, variously attributed to inflation, geopolitics or central banks.

But one pattern keeps repeating: when populous nations achieve widespread electrification, prosperity surges, and so does gold.

https://t.co/zZf6myjcdl

#goldrevolution#gold

@Arturraposo1R Artur, I believe the commodity upswing was foreseeable well before the prices of scarce metals began to stir in late 2025.

I argue that multi-year commodity upcycles rest on two recurring dynamics: one very ancient, and one modern.

For the argument: https://t.co/JADkfB9dL8

India or commodities?

India’s NIFTY Index has had a stellar decade, tripling since 2016.

However, the chart below suggests a shift is underway.

As India becomes a key driver of commodity prices, do commodities now offer better exposure to its growth?🇮🇳

#Nifty50#IND#Copper

@ayusshsanghi Ayussh, tariffs and AI datacentres are certainly part of the story, but I suspect at this very moment, you may in fact be standing on one of the most significant drivers of the copper up-cycle...

The image below is sourced from 'Gold and Revolution': https://t.co/ix6cBkGGHJ

@Kacper_PK_CH Hi Kacper

While soft commodities have struggled in 2025, bear in mind that they began the decade strongly, driven by major geopolitical shocks.

I am of the view that the rise of the Subcontinental economies is a major tailwind for all commodities metals & ag commodities alike.

In my latest piece of my commodity cycles series, I argue that commodity cycles are shaped by the shift to new stages of economic growth in the globe's populous regions, ultimately driven by electrification. https://t.co/ix6cBkGGHJ #commoditycycle#EconomicGrowth@anil_rohra

@anil_rohra Hi Anil

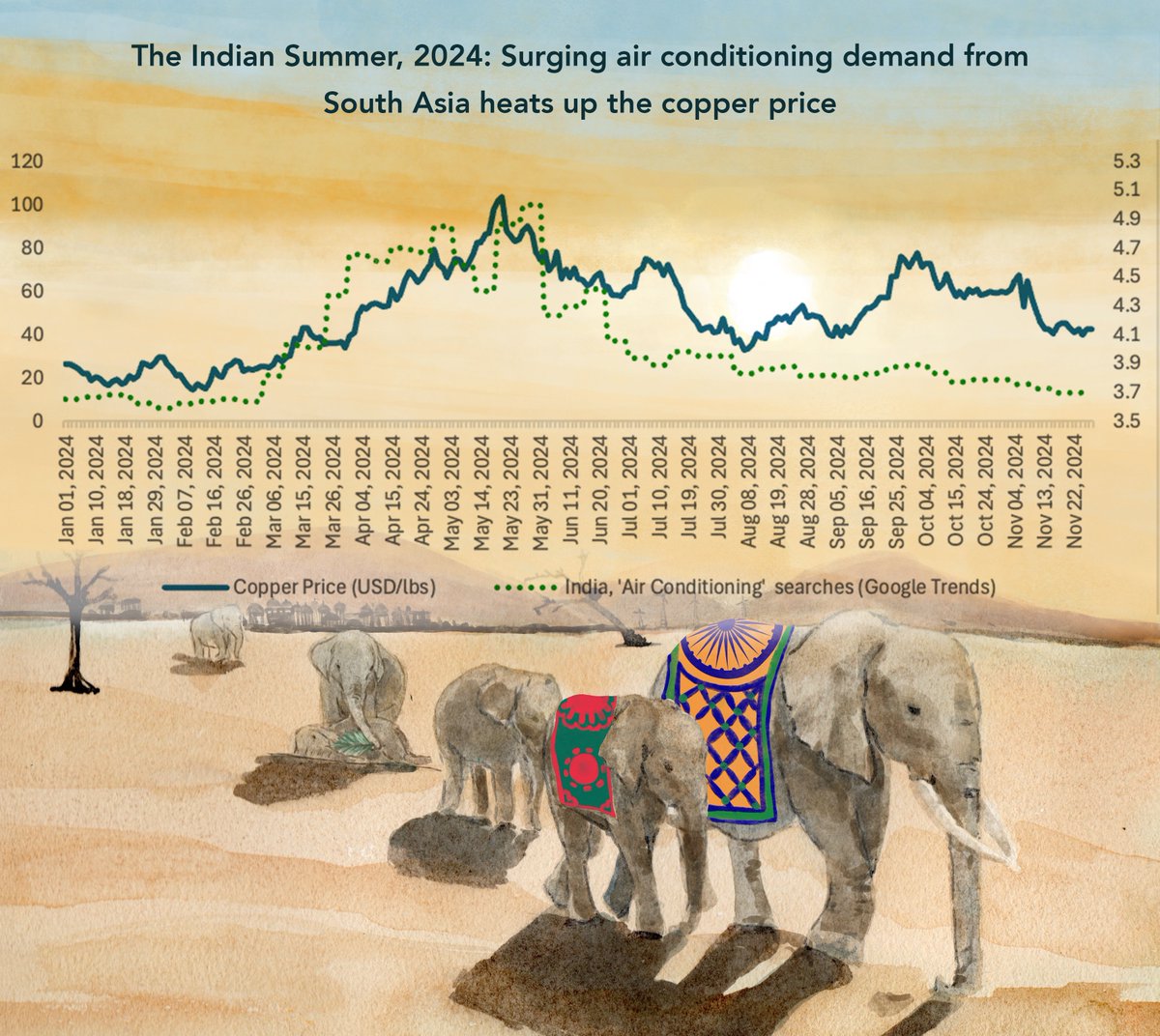

I don't dispute that copper is faced with serious supply side constraints, however, on the demand side, I argue that the primary swing factor are two rising giants of South Asia, who are in a 'copper hungry' phase of growth.

Two Hungry Elephants – Gold & Revolution

Riding the Wave: Why the Next Phase of the Australian Stockmarket Will Be Far From Ordinary | LinkedIn

My recent Linkedin post, in which I argue that the Australian equity market is positioning for its next phase.

#ResourceStocks#ASXInvesting#InvestAustralia

@BryceEdw Hi Bryce

If you have a moment to spare in the near future, would you be able to contact me? My email address is [email protected]

Thanks in advance

Regards

Patrick

More on the above:

1) In 1913, Ford introduced electric conveyers at their Highland Park facility, making possible the moving assembly, dramatically increasing production.

2)In 1980, China’s Sixth Five-year plan aimed to address the country’s deficiencies in electrical capacity.

Two charts, seemingly unrelated, share a common thread.

1) Annual production at Ford's Highland Park factory 1909 to 1922

2) China's GDP, 1960 to 2000

What is true at the factory level, is also true for the national.

Electricity drives exponential growth.

#GDP#Ford#China

Electricty grids = Economic growth

The world's largest electricity grids in 1914 were all located in the United States.

These foundational networks powered the growth of the US economy over the 20th century.

#electricity#EconomicGrowth#futuregrowth

https://t.co/BSQhP88a2t

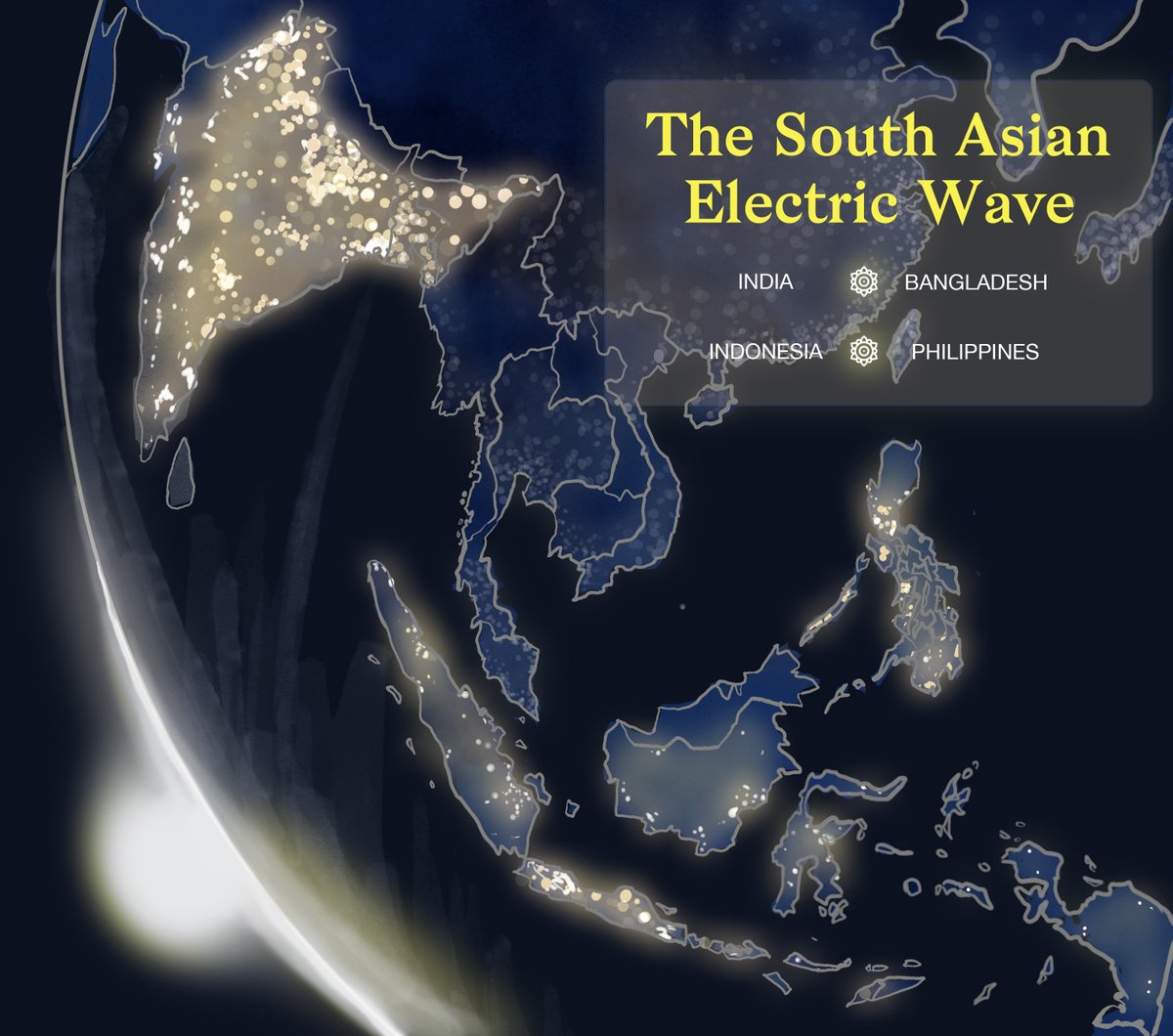

In the early 2020s, four major South Asian nations flipped the switch to full electrification.

In the piece below, we argue that the 'electrification' of South Asia is the most potent trend shaping the world of tomorrow.

#commodities#megatrends#BRICS

https://t.co/BSQhP88a2t

@MinesMinIndia Based on India's current developmental stage, historical trends suggests that India's aluminium output may very well surpass that of China in the years ahead, not unlike how China's production overtook that of Russia in the early 2000s. https://t.co/BSQhP88a2t

A fresh perspective on the Gundestrup Cauldron: Could the plate below be a depiction of a pre-Christian rendition of an Old Irish poem? https://t.co/E2ZrzGZRLy

#archaeohistories#History#Ireland

@Contrarian_WA@DznBkr@respeculator ...Less demand for lead-acid batteries will lead to less demand for lead, a fall in the lead price, and eventually, the closure of many primary lead mines.

Of course, zinc and lead always occur together, and thus when lead mines shut-up shop, it will also impact the zinc supply.

@Contrarian_WA@DznBkr@respeculator Hi Contrarian

My suspicion is that the more significant impact for the zinc price might be in the 'flip-side': Namely, less demand for lead-acid batteries as a swathe of new generation batteries emerge....