Author of the “Pngfund” Substack publication. Long-only quality growth investor who likes to share insights into wonderful businesses run by wonderful managers.

$TDG is one of the best compounders in recent decades.

It's a company I keep a close eye on so I can buy when prices drop.

Here's the company in a nutshell:

1. Sole-Source Monopolist at Scale: TransDigm is the only supplier for 75% of what it sells, across ~100 acquired niche businesses.

No competitor can justify the R&D spend to challenge a product that generates maybe $1,000 in annual revenue per unit for the OEM.

2. The Aftermarket is ~⅓ of revenue but 75% of adjusted EBITDA. FAA regulations lock part designs in for the life of the aircraft, turning every new plane win into a multi-decade, sole-source replacement contract.

3. TransDigm has incredible pricing power. It raises prices up to 40% per year on certain products. It works because a $1,000 part is immaterial to a $100M aircraft.

There was even a DoD investigation that found 112 of 113 contracts exceeded the government's "fair and reasonable" 15% margin cap. Some of them by thousands of percent. Yet, due to the lack of alternatives, nothing happened. This is a risk, but it also shows the enormous pricing power of TransDigm.

4. TransDigm has done about ~100 acquisitions, and zero of them were losers. Every deal requires a 20%+ IRR and a 5-year money-double.

The concept is to buy a business and immediately pull the pricing lever and focus on the high-margin business units. That often improves margins from 15% to nearly 40% in a few years.

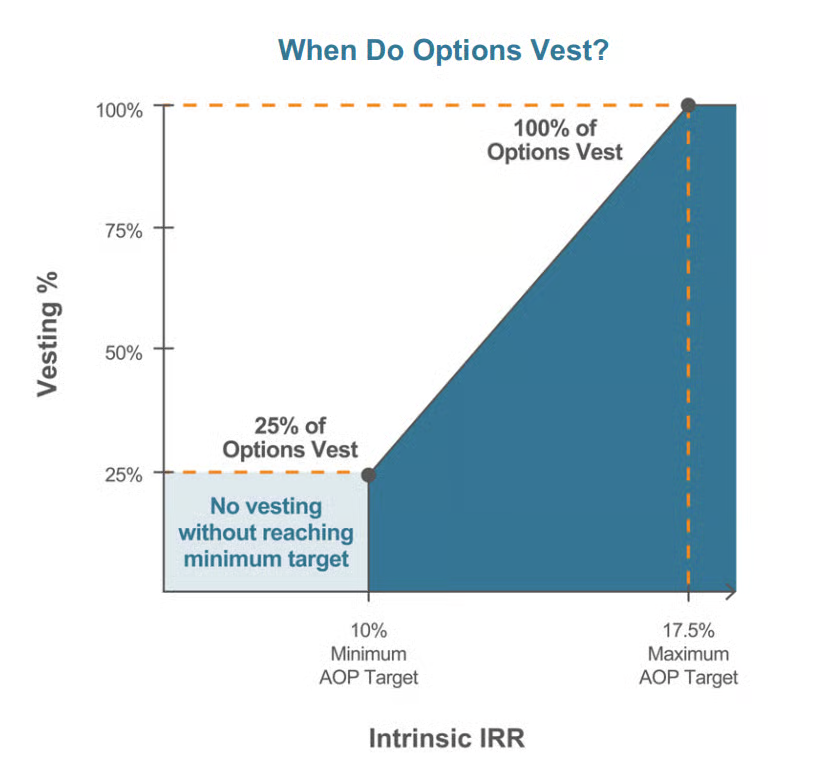

5. 80–90% of exec pay is performance-based. Stock options only fully vest at a 17.5% annual stock CAGR. The base salary for top executives is just over $1M. The rest is earned alongside shareholders.

6. 6x Net Debt/EBITDA is the target, currently at 5.7x after a $5B debt issuance. It's manageable because ~75% of revenue comes from the aftermarket, which is effectively non-discretionary.

Airlines can delay new plane orders, but they cannot skip maintenance on planes already flying. Even during COVID, this hasn't been a problem.

Air travel fell more than 50%, and commercial aftermarket revenue dropped 40%+. Total revenue and EBITDA still declined by only ~10%, underscoring just how resilient the model is under extreme duress.

7. Aging fleet = more aftermarket dollars. The average age of active aircraft has risen sharply due to delivery delays by Boeing and Airbus. Older planes require more frequent component replacement across exactly the subsystems that TransDigm dominates.

8. Only 3% penetrated in a $60B market — Global airline maintenance spend is ~$850–900B per year; ~15% is maintenance. TransDigm is active in 47% of that pool (~$60B addressable), but currently captures only ~$1.7B in commercial aftermarket revenue. The market remains highly fragmented with thousands of acquisition targets.

9. Interest expense is the one number to watch. Interest expense as a % of revenue has been creeping up and now sits at 17.5%, with the long-term trend clearly moving higher as cheap pre-2022 debt matures and gets refinanced. TransDigm still covers interest 2–3x, but this is the key variable that could compress the leverage arbitrage over time.

UBS expert call on with former m&a director at Constellation Software

- No change in strategy. Mark Miller has been at CSU since 1995 and is executing the same playbook

- Gen AI will allow CSU to offer product delivery times much faster

- we have long term relationships with all our clients and they are using our expertise to implement AI into existing software

-given our vast access to data, GEN AI will allow us to improve sales and marketing

- most acquisitions completed at the division level

- no change to our diligence, hurdle rates or guidelines for acquisitions.

This is one of the cleanest ways to think about what actually makes a stock investable.

Not just a moat. Not just great management. Not just forecastability.

You need all three – and you need to avoid the traps in between.

Source: Ensemble Capital (check out the blog, which is no longer active as they got acquired, but still a treasure trove of great investing content)

$CSU acquires TECVIA — a European leader in driver education, offering software, digital learning, simulators, and industry media to driving schools and mobility sectors. It serves millions of students and thousands of schools across Europe — very niche!

$CPRT has been a public company for 32 years

- 68% of those years have been positive, and the stock has delivered more than 40% annual returns in 11 different years.

- 11% of the company is Cash

- The company has no debt.

- On average, every 25 minutes someone uploads a YouTube video about Copart. (I haven’t checked TikTok, which probably has higher engagement.)

$CSU $CSU.TO

Mark Leonard retires from

Constellation Software. Hope he has a speedy recovery and sad to see him go.

No one is better suited for the role than Mark Miller.

Susan Li, $META CFO in rare inverview with @collision

Zuck once gave her an EBITDA hat as a gift.

She smiled, wore it on Zoom a few times… but then made her own hat: “Free Cash Flow” and gave them out to her team like candy saying “This is the hat that matters.”

$META is run by killers lmao.

https://t.co/IOPIPTFbCs

$V Exec: "We have nearly 14,500 financial institutions who have issued 4.8 billion Visa credentials that can be used at more than 150 merchant locations globally. This is fully supported by VisaNet's 99.9999% of reliability and the seventh most valuable brand in the world as well as our more than 31,600 employees who wake up every day like me obsessing about our customers."

Why you should be long America 🇺🇸 according to Thomas Peterffy $IBKR:

🌎 Geography – two oceans, endless resources

📖 Constitution – freedom codified

👬 People – restless, inventive, always renewing

Add it up and 🇺🇸 equity markets keep pulling global capital - and he thinks that won’t change any time soon.