If fiscal dominance becomes persistent, bond markets may “take fright” → sharply higher rates → steeper yield curve. Markets may be the last line of discipline.Are we entering a new era of fiscal dominance?#CentralBank#MonetaryPolicy#FiscalDominance

https://t.co/T0eRbydLEW

Is the Fed ready for a more prudent approach to monetary policy?

Join Charles Evans and Armen Nurbekyan, as they discuss next generation frameworks, risk management, what the Fed could learn from Armenia’s strategy.

🕑 2 PM London / 9 AM DC

🔗Register: https://t.co/82wosZlVAi

Those who have followed the lit on monetary policy credibility are unsurprised by the persistence of inflation in response to the delayed reaction by many central banks in the face of stagflation the past couple years. However, the time has come for CBs to change their strategy

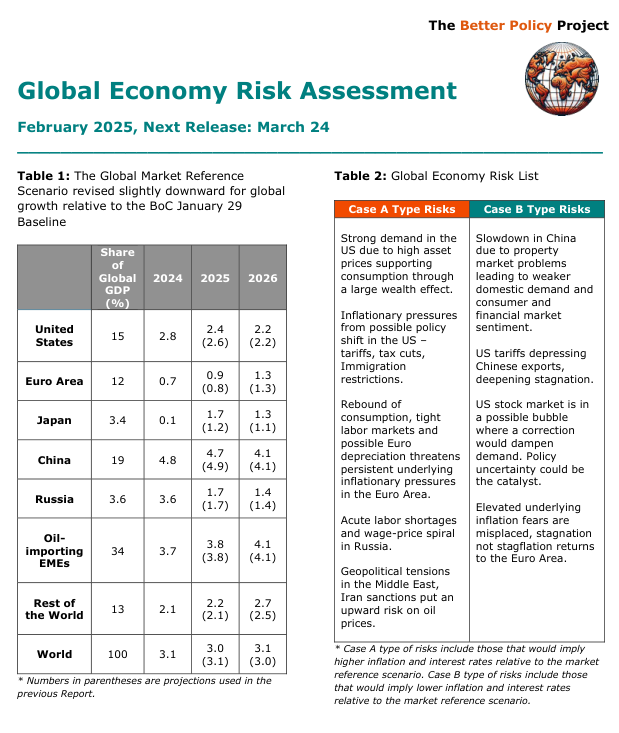

Let us introduce you to the Global Economic Risk Assessment that takes a high level view of the global economy from our pov. Global growth revised slightly lower but stickier inflation continues to plague many countries. Should central banks adopt an undershooting strategy?

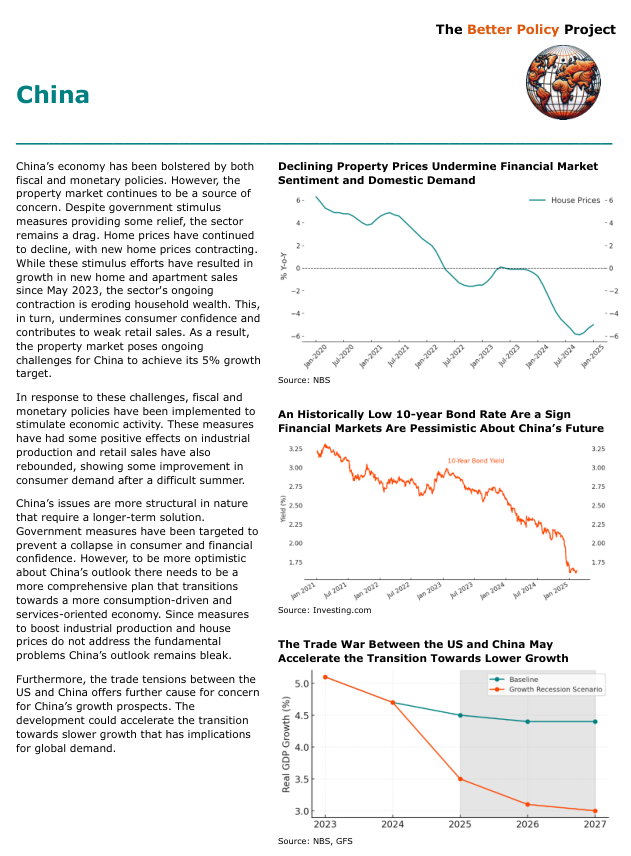

Perhaps the biggest vulnerability to the global economy is China which continues to grapple with its real estate market deflating but so far has been able to stem an outright crisis in confidence

U.S. Consumer Spending Just Hit $20 Trillion—What’s Next?

1/ As of Sept 2024, U.S. nominal consumer expenditures surpassed $20T, a legacy of aggressive monetary & fiscal policies post-COVID. But is this growth sustainable? Let’s break it down. 👇

7/ The continued surge in nominal consumer expenditures makes macroeconomic stability a challenge. Policymakers must balance growth & inflation control carefully.

If you haven’t been invited to Dilijan to attend the ‘AI & Productivity’ symposium from January 22-24, 2025, don’t worry—you haven’t missed it yet! You can still register to attend the symposium online via this link: 👇

https://t.co/eSwl3vWuXT