This is absolutely insane.

$MRVL is up 71% in 6 weeks since we flagged the heavy Congressional buying.

We will keep tracking insiders. Turn on notifications so you do not miss the next one.

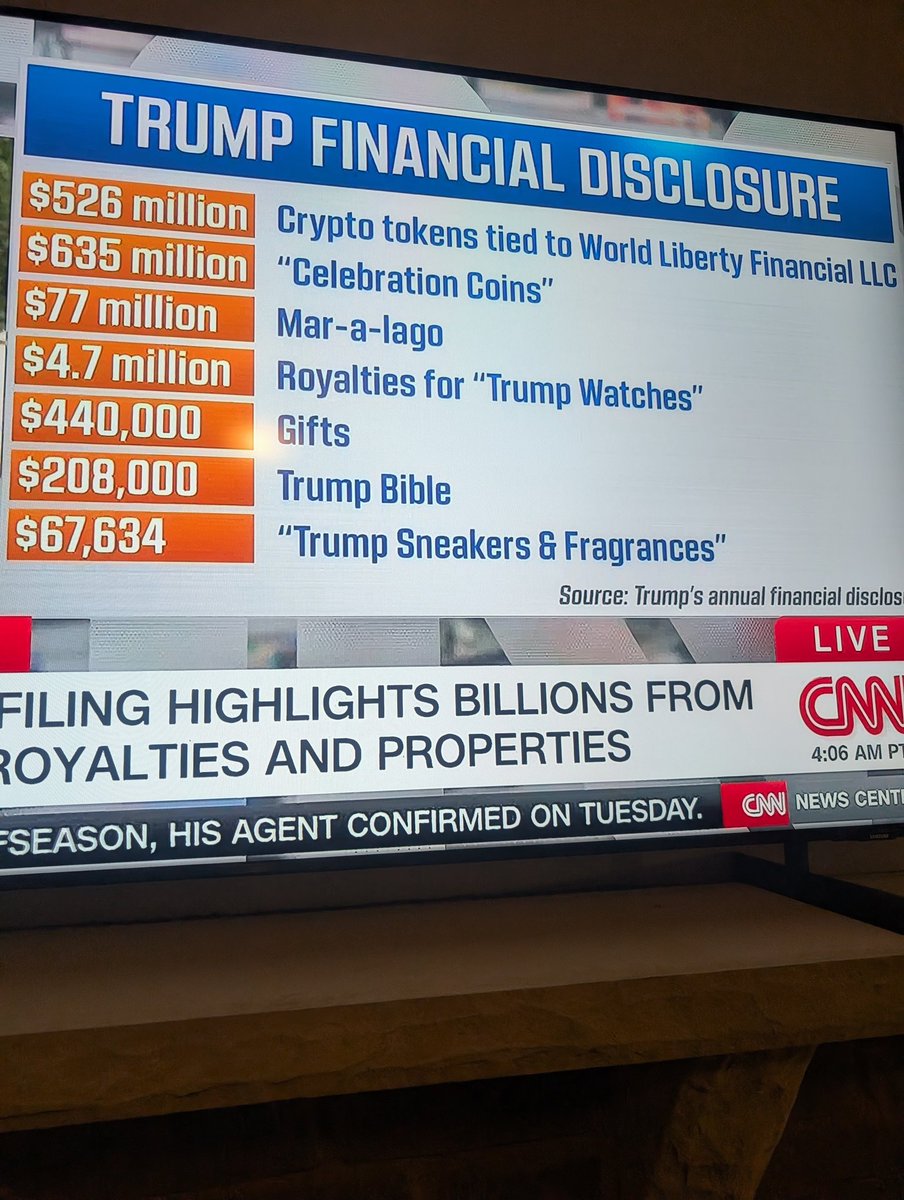

When asked about the $2.2B he personally raked in last year while President, Trump replied, “Everybody is profiting.” Trump made $1.4B in crypto alone, but most of the people who bought tokens or meme coins he sold lost money. Maybe he meant everybody named Trump is profiting.

Trump just reported $635 million in meme coin income.

Meanwhile…

- Barron reportedly made around $80M from crypto at 19.

- Trump calls himself the “crypto president” while his words move markets.

- Barron holds billions of WLFI tokens in the family project he reportedly pushed to launch.

- A massive short appeared just before Trump’s tariff announcement, and people immediately questioned whether someone close to Trump knew in advance.

- Then a random Chinese trader suddenly claimed it was his trade.

- Eric Trump’s wealth reportedly exploded from about $40M to roughly $750M in a year.

- Trump has now reported billions tied to crypto.

And somehow we’re all supposed to act like none of this deserves serious scrutiny.

Imagine if Obama was directly connected to Epstein, made $2 billion off crypto scams, grifted a $400 million plane form Arab Royals, and started and lost a war with Iran.

You owe the IRS $100,000

They'll take $5,000 and close your file. Permanently. Balance goes to $0

It's called an Offer in Compromise. Form 656. The IRS approved 42% of them last year. Application fee: $205

Here's the exact formula they use to decide your number and how to reverse-engineer the lowest possible offer

The IRS doesn't want to chase you for 10 years. Collection employs 78,000 people. Each agent costs the agency $89,000/year in salary and overhead. Liens require court filings. Levies require processing. Garnishments require administration. They'd rather take your $5,000 check today than spend $120,000 in administrative costs over a decade trying to squeeze $100,000 out of someone who will never have it

They literally built a math formula to calculate the minimum they'll accept. Here it is:

RCP = (monthly disposable income x remaining collection months) + (net realizable equity in assets)

Monthly disposable income: your gross monthly income minus IRS-allowed living expenses. They don't use YOUR actual expenses. They use standardized tables published at the irs website standards. These tables set exact allowances by county for housing, food, transportation, healthcare, and out-of-pocket expenses

If you earn $4,200/month and the IRS allowable expense table for your county totals $3,900, your disposable income is $300/month. If you earn $3,800/month and the table allows $3,900, your disposable income is negative and the IRS considers it $0

Remaining collection months: for a lump sum offer (paid in 5 months or less), multiply disposable income by 12. For a periodic payment offer (paid over 6-24 months), multiply by 24. The lump sum multiplier is lower, which means a lump sum offer will always be cheaper than a payment plan offer. Always choose lump sum if you can

Net realizable equity in assets: bank accounts, investments, vehicles, real property. BUT they subtract allowances. Your primary car: exempt up to the IRS local standard (roughly $6,000-$10,000 in equity depending on area). Household furnishings: fully exempt. Retirement accounts: partially exempt and heavily discounted (the IRS applies a "quick sale value" of 60-80% of actual value because they know selling retirement accounts triggers penalties)

Real calculation:

Income: $4,200/month

IRS allowed expenses: $3,900/month

Disposable income: $300/month

Lump sum multiplier: 12 months

$300 x 12 = $3,600

Assets:

Bank account: $2,100

Car equity: $4,800 (below IRS exemption, counts as $0)

401k: $18,000 (quick sale value at 60% = $10,800, minus 10% early withdrawal penalty = $9,720, minus taxes at 22% = $7,582)

Household goods: exempt

But here's the part most people don't know: you can CHOOSE to exclude retirement accounts from the RCP calculation by checking a specific box on Form 433-A (OIC). The IRS has an internal policy (IRM 5.8.5.24) that allows exclusion of retirement assets for taxpayers under age 65 if liquidating those assets would cause economic hardship. Your tax preparer should know this. Most don't

Revised RCP without retirement: $3,600 + $2,100 = $5,700

Your offer: $5,700 on $100,000 in tax debt. 5.7 cents on the dollar

The nuclear part:

While the OIC is being reviewed (6-24 months), ALL collection activity legally stops. No levies. No new liens. No wage garnishment. The IRS cannot collect a single dollar from you while your offer is pending. This is codified in IRC Section 6331(k)(1)

And if the IRS fails to make a determination within 24 months of receiving your application, your offer is AUTOMATICALLY ACCEPTED. Two years of silence = you win by default. IRC Section 7122(f). They built an auto-accept clause into the law that most taxpayers never invoke because most taxpayers never file an OIC

The forms you need:

Form 433-A (OIC): complete financial disclosure for individuals. Every bank account, every asset, every income source, every expense. 8 pages. Fill it out accurately because they cross-reference against IRS records, DMV records, and financial institution reports. Lying on this form is a federal crime under 18 U.S.C. 1001

Form 656: the actual offer. Your amount, your payment terms, your signature

$205 application fee (waived if income is below 250% of federal poverty level, which is $38,100 for a single person in 2026)

Initial payment with the application: 20% of your offer for lump sum. On a $5,700 offer that's $1,140

A woman owed $213,000 across 4 tax years (2019-2022). Hadn't filed 2020 or 2021. Hadn't paid any of them. Receiving CP504 notices (intent to levy) every month. We filed the delinquent returns first (required before OIC submission), then calculated her RCP at $8,400. Submitted OIC with $1,680 initial payment

IRS accepted 9 months later. $213,000 settled for $8,400. 3.9 cents on the dollar

She went from getting levy notices every month to a $0 IRS balance. Then we fixed her credit (the tax lien had destroyed it). Then we stacked $120K in 0% business funding. She opened a cleaning company 4 months later. The same IRS that was garnishing her wages is now processing her quarterly estimated tax payments from a profitable business

the IRS is the scariest creditor in America. they can garnish without a court order. seize your bank account with 30 days notice. lien every asset you own. but they also built a form where they calculate the minimum they'll accept using a formula you can reverse-engineer, and if they don't respond in 2 years your offer is automatically approved. the math is public. the formula is published. the form costs $205. the difference between paying $100K and paying $5K is knowing it exists lol

(we fix credit and build capital stacks. if you owe back taxes, handle that first. then we get you funded. link in bio)

There’s somebody making $22,000/year in rural America going to bed right now that sincerely believes Donald Trump spent his whole day fighting for them.

🇷🇺🇨🇳🇺🇦🇺🇸 KASPAROV SAYS CHINA WANTS PUTIN’S WAR TO CONTINUE

Garry Kasparov 🇷🇺 - "This is a global war. China stands behind Putin and wants the conflict to continue because it weakens the West, drives a wedge between America and Europe, and drains Russia."

Kasparov’s point is that Russia’s war against Ukraine is no longer just a European battlefield. It is part of a wider contest where Beijing benefits from Moscow bleeding itself while the West is forced to spend political, military and economic capital.

For China, a weakened Russia is useful, a divided West is useful, and a long war that tests American and European unity is useful. That is why helping Ukraine win is not only a Ukraine policy. It is a global security policy.