What to Expect from the Markets this Week – 20th July 2026

Nigeria's financial markets navigated the week amid improving domestic macroeconomic indicators and an increasingly uncertain global environment. While headline inflation eased marginally to 15.91%, the first decline in three months, persistent food inflation underscored that supply-side constraints remain the dominant driver of consumer prices. At the same time, the return of the Composite PMI to expansion territory and the CBN's rollout of a real-time Bureau de Change transaction monitoring platform reinforced confidence that macroeconomic conditions are gradually stabilising.

In the fixed-income market, investors maintained a preference for short-dated instruments, with Treasury bill and OMO yields edging lower amid abundant system liquidity. The NTB auction highlighted continued demand for duration, as investors aggressively subscribed to the 364-day bill in anticipation of a stable monetary policy environment. Attention now shifts to the July Monetary Policy Committee meeting, where the moderation in headline inflation, alongside easing core inflation, is expected to strengthen the case for another policy hold despite persistent food price pressures.

The equities market, however, paused after its recent rally as investors locked in profits across industrial and consumer stocks. Even so, the banking sector continued to outperform, supported by earnings expectations and sustained institutional demand. The listing of additional shares by Sterling Financial Holdings also boosted market capitalisation, underscoring that capital-raising remains an important feature of Nigeria's evolving financial landscape.

The coming week is expected to be shaped by the outcome of the @cenbank's Monetary Policy Committee meeting, second-quarter corporate earnings releases, and key global central bank decisions, particularly from the @ecb and the People's Bank of China.

While improving domestic liquidity and resilient investor confidence provide a supportive backdrop, elevated food inflation, exchange-rate, and geopolitical developments will remain critical drivers of market sentiment.

Read more: https://t.co/wEMGcmoe8K

Contact Us:

To list your events, e-mail [email protected], WhatsApp 0902-407-5284

For feedback, further information, enquiry or clarifications, contact [email protected] or [email protected] Tel: 0700PROSHARE (070077674273).

Follow us @proshare@ecopoliticsNG@TheAnalystNG and @Personalfinng on Twitter and @proshare across other social media platforms

Follow @webtvnigeria for coverage and updates.

Check out our Events Calendar for event details as the week unfolds. Yours to Serve!

🔗 https://t.co/d0Azv7iuxV

What to Expect from the Markets this Week – 20th July 2026

Nigeria's financial markets navigated the week amid improving domestic macroeconomic indicators and an increasingly uncertain global environment. While headline inflation eased marginally to 15.91%, the first decline in three months, persistent food inflation underscored that supply-side constraints remain the dominant driver of consumer prices. At the same time, the return of the Composite PMI to expansion territory and the CBN's rollout of a real-time Bureau de Change transaction monitoring platform reinforced confidence that macroeconomic conditions are gradually stabilising.

In the fixed-income market, investors maintained a preference for short-dated instruments, with Treasury bill and OMO yields edging lower amid abundant system liquidity. The NTB auction highlighted continued demand for duration, as investors aggressively subscribed to the 364-day bill in anticipation of a stable monetary policy environment. Attention now shifts to the July Monetary Policy Committee meeting, where the moderation in headline inflation, alongside easing core inflation, is expected to strengthen the case for another policy hold despite persistent food price pressures.

The equities market, however, paused after its recent rally as investors locked in profits across industrial and consumer stocks. Even so, the banking sector continued to outperform, supported by earnings expectations and sustained institutional demand. The listing of additional shares by Sterling Financial Holdings also boosted market capitalisation, underscoring that capital-raising remains an important feature of Nigeria's evolving financial landscape.

The coming week is expected to be shaped by the outcome of the @cenbank's Monetary Policy Committee meeting, second-quarter corporate earnings releases, and key global central bank decisions, particularly from the @ecb and the People's Bank of China.

While improving domestic liquidity and resilient investor confidence provide a supportive backdrop, elevated food inflation, exchange-rate, and geopolitical developments will remain critical drivers of market sentiment.

Read more: https://t.co/wEMGcmoe8K

"There's no coherent continental approach towards engagement with other continents."

Director of Research, Proshare Nigeria, @TeslimShittabey, says Africa's biggest challenge is not external partnerships but the absence of a coordinated continental agenda.

In Part II of The @Nigel_Farage Wager, Professor @anthonykila argues that durable democracies rest on three equally important pillars: electoral legitimacy, constitutional legitimacy, and civic legitimacy. While elections determine who governs, they do not replace the rules, institutions, and standards that hold public officials accountable.

Using the Nigel Farage case as a lens, the article explores a broader question confronting democracies worldwide: can political popularity be allowed to supersede constitutional restraint?

https://t.co/fMgwfr05jq

In this piece, @collinsnweke argues that a nation's security performance has become a defining factor in investor confidence, international credibility, and economic diplomacy. Using recent developments in U.S.–Nigeria relations, he contends that governance at home increasingly shapes how countries are perceived abroad.

The article makes a compelling case that the President's role now extends beyond Commander-in-Chief to Chief Economic Diplomat, where every improvement in security, governance, and institutional effectiveness strengthens Nigeria's competitiveness and investment appeal.

https://t.co/f6a0WZPFu7

Brent crude continues to trade near US$86 per barrel even as Hormuz tanker transits approach zero, US-Iran hostilities widen to include strikes on civilian infrastructure, and Tehran extends retaliation to a Kuwaiti power and desalination facility. This apparent disconnect between physical supply risk and price behaviour should be read by investors and policymakers as a market still pricing residual confidence in eventual de-escalation, not as evidence that the risk has passed.

https://t.co/ERWOlUY7DY

.@myaccessbank has secured an unprecedented 16 honours at the prestigious Euromoney Awards for Excellence 2026, marking one of the strongest performances by any African financial institution this year and underscoring its emergence as one of the world’s most respected banking brands.

https://t.co/PcNitfgOiE

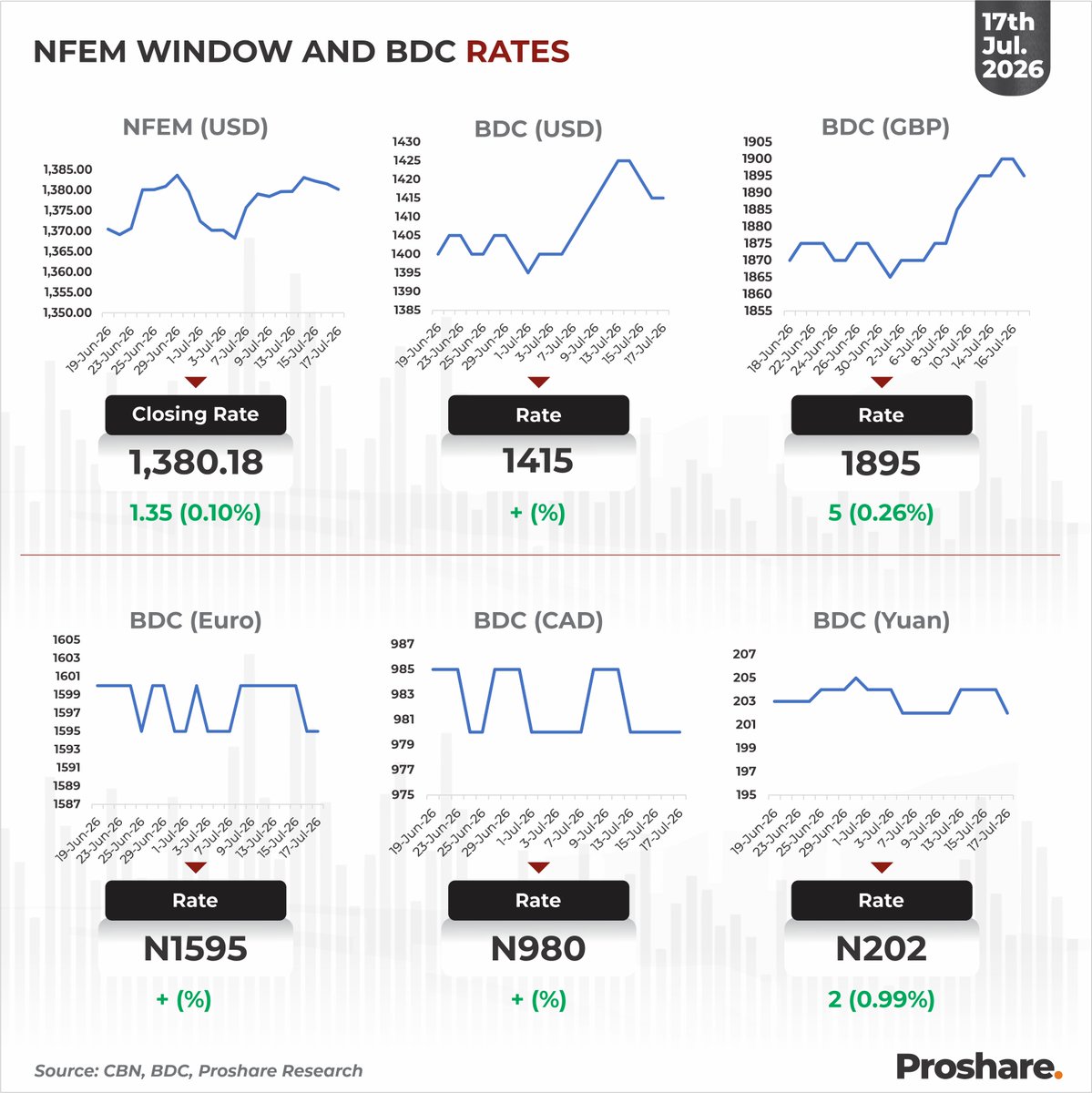

Banking Stocks Lift NGXASI 0.54% as Market Snaps Two-Day Losing Streak; BDC Rate Closed Flat at N1,415/US$1

The Nigerian equities market rebounded on Friday, July 17, 2026, snapping a two-session losing streak as renewed buying interest in banking and other large- and mid-cap stocks lifted the benchmark index and boosted investors' wealth.

Read more: https://t.co/mjQ5e6oyCI

Nigeria’s crude oil production increased to an average of 1.56 million barrels per day (mbpd) in June 2026, marking the highest monthly crude oil output since April 2020 and exceeding Nigeria’s 1.5 mbpd OPEC production quota by approximately 4.0%.

https://t.co/oNQ92hb1fR

Weekly Snapshot on the African Economy as 17th July 2026

Africa's economic landscape this week reflected a continent balancing structural reforms with evolving global headwinds. Across several regions, governments continued to strengthen macroeconomic fundamentals through higher external reserves, fiscal reforms, debt restructuring, capital market development, and infrastructure investment, while persistent inflation, geopolitical tensions, and commodity price volatility remained key risks to the outlook.

In West Africa, Nigeria dominated developments as headline inflation eased marginally to 15.91%, external reserves rose to US$51.5bn, crude oil production exceeded its @OPECSecretariat quota for the first time in years, and business activity returned to expansion. These positive indicators were complemented by regional efforts to deepen cocoa value addition through the Abuja Declaration. However, #Dangote Refinery's transition to dollar-denominated fuel sales highlights the continued vulnerability of domestic prices to exchange-rate pressures.

Ghana moved closer to completing its external debt restructuring, strengthening prospects for renewed market access, while Togo and Liberia advanced fiscal inclusion and development initiatives. East Africa continued to emerge as a regional growth engine, with Kenya's equity market reaching record highs, Ethiopia accelerating financial sector reforms, and Rwanda reinforcing fiscal transparency.

Southern Africa also attracted attention as Zimbabwe posted record FDI inflows, South Africa secured multilateral financing for critical infrastructure, and Tanzania advanced plans to reposition TAZARA as a regional trade corridor. In North Africa, Egypt, Morocco, Algeria and Libya sustained reform momentum through stronger reserves, renewable energy investments, privatisation programmes and infrastructure expansion.

Africa's medium-term outlook remains cautiously optimistic. Improving macroeconomic fundamentals, expanding infrastructure investment, stronger commodity production, and ongoing policy reforms are expected to support growth and attract investment. Nevertheless, elevated food inflation, exchange-rate volatility, tighter global financial conditions, and renewed geopolitical tensions, particularly their impact on energy prices and supply chains, remain significant downside risks.

The pace of reform implementation, fiscal discipline, and the ability to mobilise private capital will be critical in determining whether the continent can translate current resilience into broad-based, sustainable economic growth during the second half of 2026.

Read more: https://t.co/Bl39aODWmc

Nigeria's federally collected revenues continue to climb. FAAC distributed N2.6trn to the three tiers of government in June 2026, up from N2.3trn in May, driven by a N550bn MoM surge in statutory revenue to N1.8trn.

https://t.co/pmyQbdONt9

.@NaicomNG has dismissed as "false, mischievous and grossly misleading" a publication issued by individuals claiming to represent @Niger_Insurance, reaffirming that the insurer remains in receivership and is prohibited from underwriting new insurance business.

https://t.co/7ILdw45Trf

Over 64% of Nigerian adults are financially included, yet only 6% access formal credit. That gap is costing the economy dearly. - Sola Bickersteth of FIC Professionals Network Plc

https://t.co/YbukJTOOzw

"The whole non-interest finance industry is based on people's confidence and belief that there is compliance with the principles of non-interest finance.

In this edition of #IslamicFinanceWeekly, we engaged Prof. Bashir Aliyu Umar @baumar277, the Deputy Chairman of the Financial Regulation Advisory Council of Experts (FRACE), to discuss "Unlocking the Potential of Non-Interest Finance in Nigeria: The Role of Regulation."

Watch full video: https://t.co/AOSR6s3G2m

#FinancialInclusion

#NonInterestFinance

LIVE TODAY | 5:00 PM WAT

Proshare’s Director of Research, @TeslimShittabey, will be live on @NewsCentralTV to examine:

“UK Aid Cuts: Is Britain Abandoning Africa or Redefining Its Global Role?”

The discussion will assess what Britain’s changing development-aid priorities could mean for Africa, international partnerships and the UK’s evolving global influence.

📅 Friday, July 17, 2026

⏰ 5:00 PM WAT

📺 DStv Channel 422 | StarTimes Channel 274 | YouTube Live

Tune in for an informed and timely conversation.

After three consecutive months of mild acceleration, headline inflation finally eased by two basis points to 15.91% year-on-year in June 2026, down from 15.93% in May. The move is marginal, but its composition matters: the deceleration was driven almost entirely by a sharp cooling in core inflation, which fell to 15.92% from 16.82%, even as food inflation reaccelerated for a fifth straight month to 17.52%. The reading reads less as a decisive reversal than as the stall of the previous three months beginning to break in the right direction, with energy-price relief doing the heavy lifting while food-supply pressures persist beneath the surface.

@cenbank has framed recent inflation dynamics as transitory, holding the Monetary Policy Rate (MPR) at 26.50% at its May meeting and anchoring its outlook to expected external relief. The June print lands days ahead of the 306th Monetary Policy Committee meeting on 20–21 July 2026, against a backdrop of a fragile US–Israel–Iran ceasefire, oil prices holding near US$85 amid lingering Strait of Hormuz conflict risk, pre-election spending in view, and food inflation diverging sharply across states, from -3.54% month-on-month in Borno to a 53.02% year-on-year inflation rate in Kogi.

This @Econassociates-Proshare June 2026 inflation update sets out what the data signals for markets, policy, and households over the months ahead. In this review, we highlight the key takeaways from the data.

Read more: https://t.co/infV3b93zg