Market Expertise / Pro Trader, Mentor, Coach in Prop Trading Company for 20yrs+ / Global Trader’s Performance Enhancement Coach - Group and 1-1 sessions

Why are global yields rising? - something retail seams to be blind to..

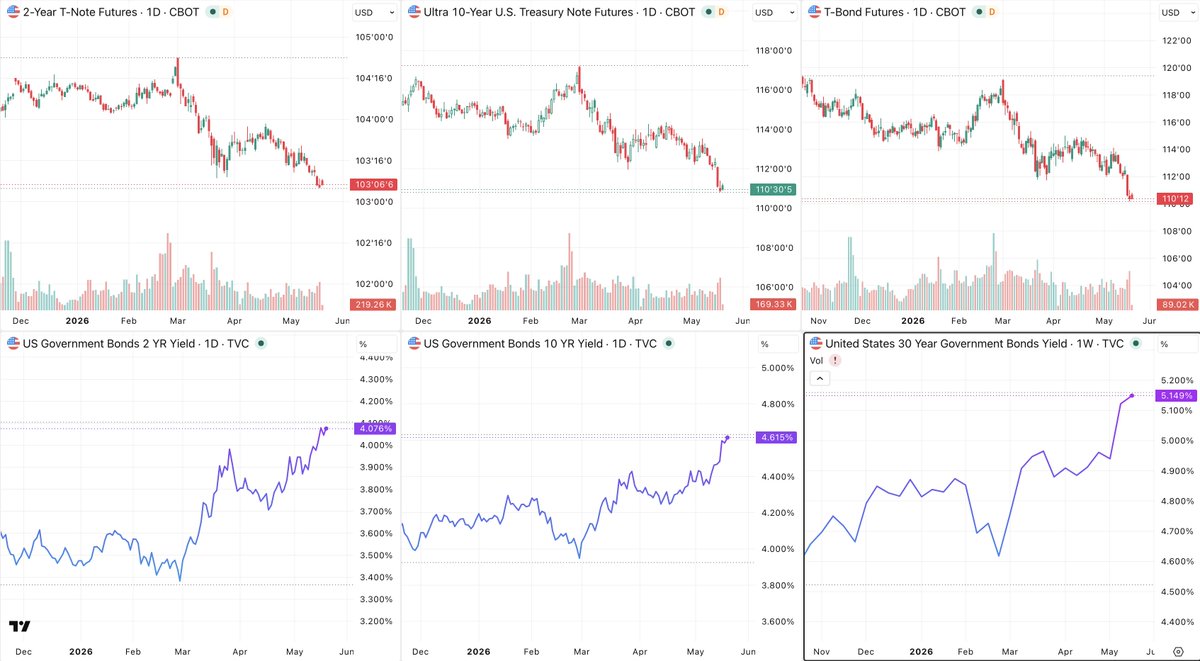

Global yields are rising not only because inflation is rising but because rules of the game are changing - markets are repricing a world with less Fed suppression of bond yields - that’s something that retail seams not to be noticing, relying on another QE from Fed as before..don’t get fooled..

* The Fed “put” is being removed.

For ~15 years, markets assumed the Fed would step in whenever sovereign debt, credit markets, or financial conditions became unstable. That support came through:

• QE — the Fed buying bonds, pushing yields down

• forward guidance — the Fed talking markets into lower-rate expectations

• swap lines / crisis tools — dollar liquidity support for foreign central banks

• implicit coordination with other central banks

Warsh represents a regime shift: less intervention, smaller balance sheet, less willingness to finance government deficits indirectly.

* Without Fed buying, bonds need real buyers at real prices. If the Fed is no longer a reliable buyer/backstop for long-dated debt, private investors demand more compensation to hold it. That means higher yields because investors now need to be paid for:

• inflation risk

• deficit risk

• political risk

• currency risk

• duration risk

• uncertainty about who absorbs huge government bond issuance

So yields rise until bonds become attractive enough for private capital.

* Fiscal dominance is being challenged It means governments have been able to run large deficits because central banks kept borrowing costs artificially low.

If Warsh breaks that entanglement, markets start asking:

“Can governments finance themselves without central bank help?”

That question is hitting not only U.S. Treasuries, but also German Bunds, UK Gilts, and other sovereign bonds.

* Global yields rise because the Fed is the world’s central bank Even though this is about the U.S. Fed, it affects everyone because the dollar system anchors global finance.

For years, foreign bond markets benefited from the belief that the Fed would stabilize global dollar liquidity in crises. If that backstop becomes conditional or weaker, investors demand higher yields on foreign sovereign debt too.

That’s why :

• German 10-year Bunds at 15-year highs

• UK 10-year Gilts at 18-year highs

• U.S. 10-year near recent highs

This is not just inflation noise — it’s a global repricing of central-bank support.

* More volatility is part of the new regime If the Fed stops guiding markets so carefully, bond markets have to discover prices more freely. That means yields can overshoot, move sharply, and respond more directly to fiscal credibility.

In short: yields are rising not just becuase of rising inflation but because markets are losing confidence that central banks — especially the Fed — will keep suppressing long-term rates and rescuing sovereign debt markets whenever stress appears.

#Bonds #Yields #Macro #Fed #Treasuries #QE #Markets

Market digest — Thu Jul 2, 2026

What matters most:

• Japan is the pressure point: weak JGB auction, foreign bond selling, and yen-intervention jitters all point to higher FX/rates volatility.

• AI/tech risk is still moving markets: US tech weakness hit Asian chip stocks, while Washington is moving toward AI model standards.

• Oil risk premium is easing as Hormuz flows improve and US-Iran talks continue.

* Japanese bonds fall as auction demand weakens

Market relevance: JGB stress matters for global yields, yen volatility, and risk appetite.

* Japan shifts to "ambush" intervention tactics against yen shorts

Market relevance: Raises event risk for USD/JPY and yen-funded carry trades.

* US tech rout hits Japan and South Korea chip stocks

Market relevance: AI/semiconductor momentum is wobbling; Meta compute-supply plans add oversupply worries.

* Oil extends drop as more barrels flow through Hormuz

Market relevance: Lower oil eases inflation pressure and could support rate-cut narratives if sustained.

* US job growth likely cooled in June

Market relevance: Payrolls are the next major rates/liquidity catalyst for the dollar, yields, and equities.

* OpenAI proposes handing Trump administration 5% stake

Market relevance: A major public stake in OpenAI would reshape AI policy, competition, and private-market valuations.

* White House accelerates AI model standards

Market relevance: Regulation risk for frontier AI models is moving from abstract to near-term policy.

* Russia launches heavy missile and drone attacks on Kyiv

Market relevance: Keeps Europe defense, energy, and geopolitical risk premia in focus.

* Wall Street ends choppy session lower as tech shares drop

Market relevance: Confirms pressure in the leadership group after a strong quarter.

* US fossil-fuel power spending set to beat China for first time in decades

Market relevance: Data-center power demand is feeding into energy capex, gas turbines, and AI infrastructure themes.

#Markets #Trading #Macro #FX #Rates #Bonds #Yen #Oil #Energy #AI #Tech #Semiconductors #OpenAI #Geopolitics #Ukraine #DataCenters

Market digest — Wed Jul 1, 2026

What matters most:

• Rates/FX are front and center: dollar stronger, gold weaker, yen intervention risk back in focus.

• AI/data-center demand is still driving macro winners: Korea chips exports, US gas-turbine power capex.

• Geopolitics/energy remain active: Iran peace talks and Hormuz traffic are keeping oil contained for now.

* Dollar Gains Ahead of Warsh Speech, Gold Declines

Market relevance: Hawkish Fed-risk and higher-rate bets are lifting the dollar and pressuring gold/commodities.

* Japan's FX Chief Says Past Yen Intervention Had Impact

Market relevance: Yen near four-decade lows keeps intervention risk live across FX and carry trades.

* China Manufacturing Caps Best Quarter Since 2020

Market relevance: Better factory momentum supports China/global growth sentiment, though the report still flags fragility.

* South Korea Exports Surge as AI Fuels Chip Demand

Market relevance: Confirms AI semiconductor demand is still translating into real export strength in Asia.

* US Fossil Fuel Power Spending to Beat China for First Time in Decades

Market relevance: Data-center electricity demand is reshaping energy capex and gas-turbine demand.

* Oil Steadies as Peace Talks Continue, Hormuz Traffic Recovers

Market relevance: Lower Middle East shipping stress helps cap oil risk premium after a weak quarter.

* US Stocks Chalk Up Biggest Quarterly Gain in Six Years

Market relevance: Risk appetite remains strong despite Iran fallout, chip volatility, and mega-IPO activity.

* Gold Heads for Worst Quarter in More Than a Decade

Market relevance: Higher-rate expectations and fading retail demand are breaking a major defensive-asset rally.

* Small Fraction of EU Crypto Groups Hold Licence as MiCA Rules Start

Market relevance: Regulatory pressure may force customer offloads and consolidation across European digital assets.

* Germany Woos Trump With Plan to Make US Weapons in Europe

Market relevance: European defence spending and joint production remain a key policy/geopolitical investment theme.

#Markets #Trading #Macro #FX #Fed #ECB #Bonds #Treasuries #Oil #Energy #AI #Tech #China #Japan #Gold #Crypto #Defense

The Speech That Could Redefine Global Markets

Tomorrow’s speech by Fed Chair Kevin Warsh may be the most important macro event of the week.

Markets are focused on AI, chips, jobs, and rate cuts. They may be watching the wrong thing.

Warsh has already launched a review of the Fed’s policy framework, and the bigger question isn’t just interest rates—it’s whether the Fed is preparing to step back from its role as the world’s central bank.

That would have profound implications:

• Less global monetary coordination.

• Greater reliance on market pricing instead of central bank intervention.

• More pressure on sovereign bond markets—especially in Europe.

Tomorrow, Warsh shares the stage with ECB President Christine Lagarde, whose policy toolkit has relied on years of coordinated central bank support.

If Warsh hints at a new framework, markets may have to rethink far more than the timing of the next Fed move.

Watch for what he says about liquidity, market functioning, the Fed’s balance sheet, and the future of international dollar support—not just rates.

#Fed #FOMC #KevinWarsh #ECB #Macro #Markets #Bonds #Treasuries #Liquidity #Investing

Market digest — Tue Jun 30, 2026

What matters most:

• Yen stress is the clearest macro signal: USD/JPY pushed past ¥162, raising intervention and BOJ-policy-watch risk.

• AI remains the market engine, but leadership is rotating from Magnificent Seven megacaps toward chipmakers and infrastructure beneficiaries.

• Energy risk premium is fading as Hormuz flows improve, with oil headed for a sharp quarterly drop and Morgan Stanley warning on glut risk.

* Yen weakens to 40-year low

Market relevance: FX volatility, Japan intervention risk, and pressure from a hawkish Fed path.

* Stock rally extends as tech rebounds, yen weakens

Market relevance: AI-linked risk appetite is spilling into Asia while currency stress builds in Japan.

* Magnificent Seven shed $2.3tn in tech rotation

Market relevance: Investors are rotating from megacap tech into chipmakers tied to hyperscaler AI capex.

* Oil set for quarterly drop as Morgan Stanley warns of glut

Market relevance: Lower oil eases inflation pressure but flags weakening demand and supply overhang risk.

* US Supreme Court blocks firing of Fed governor

Market relevance: Fed independence gets near-term protection, while broader regulator-firing power could affect markets/crypto policy.

* China economic momentum improves, slowdown still likely

Market relevance: Better-than-expected factory and services activity may temper China-growth fears, but the rebound may be late-cycle.

* China clamps down on higher-yield offshore debt issuance

Market relevance: Tightens financing for municipal-linked borrowers and highlights China credit-risk management.

* UK regulator waters down landmark crypto rules

Market relevance: Easier FCA capital/disclosure requirements may support UK digital-asset activity and listed crypto exposure.

* Maersk raises profit guidance as US tariffs fuel demand

Market relevance: Tariff front-loading is boosting shipping demand, with implications for trade, inventories, and logistics pricing.

* Supermicro Taiwan offices raided in chip-smuggling probe

Market relevance: Server maker shares fell around 8%, another supply-chain and AI-hardware headline risk.

#Markets #Trading #Macro #FX #Oil #Energy #AI #Tech #China #Japan #Crypto

Market digest — Mon 29 Jun, 2026

What matters most:

• Middle East risk is easing at the headline level, but oil/shipping/energy security remain the live market channel.

• China may be nudging liquidity easier while geopolitics with Japan worsens.

• AI remains the dominant cross-asset theme: tech valuations, power demand, private markets, and macro spillover risk.

* US stock futures advance as Iran/oil risk cools

Market relevance: Risk sentiment improved after US-Iran escalation fears eased; oil pared gains.

* Oil pares gains after US and Iran halt attacks

Market relevance: Crude remains the main macro transmission channel from the conflict, especially around Hormuz.

* PBOC's new overnight rate hints at easing

Market relevance: Lower-than-expected liquidity pricing could ease Chinese funding costs and support risk assets.

* Europe risks winter with gas stocks at 15-year low

Market relevance: Raises risk of energy price pressure, industrial stress, and policy intervention.

* Warsh's Fed communication adds rates volatility

Market relevance: Fed messaging uncertainty could keep Treasury and currency volatility elevated.

* China blacklists more Japanese entities

Market relevance: China-Japan tensions add supply-chain and regional equity risk, especially around strategic sectors.

* Freight shipping costs surge ahead of new Trump tariffs

Market relevance: Tariff front-running is pushing shipping rates higher, a potential inflation and margin pressure point.

* AI exuberance risks investment bust, BIS warns

Market relevance: Central-bank warning flags systemic risk from AI capex, valuations, and funding pullbacks.

* AI fuels record $200bn M&A boom in US power sector

Market relevance: Data-center electricity demand is reshaping utilities, infrastructure, and energy M&A.

* Japan retail sales rise for third month

Market relevance: Stronger demand from wages/subsidies matters for BoJ policy expectations and yen rates.

#Markets #Trading #Macro #Oil #Energy #China #Japan #AI #Tech #Rates #FX

Market Digest — Fri Jun 26, 2026

What matters most:

• AI/tech is driving the main risk-off move: Apple price hikes, OpenAI IPO-delay fears, and chip-stock pressure hit Asia hard.

• Hormuz risk is still live: traffic has resumed, but a vessel attack/escort halt keeps an energy-risk premium in play.

• Rates/dollar pressure persists: hawkish Fed expectations are weighing on gold, HKD/Asia FX, and duration-sensitive assets.

* Global markets fall as investors fret about AI demand

Market relevance: Broad tech-led selloff, with Apple pricing and OpenAI IPO-delay concerns hitting risk appetite.

* Korean stocks tumble 9% on chip selloff, triggering trading halt

Market relevance: Shows how concentrated AI/chip sentiment risk has become across Asian equity markets.

* Ship attack in Hormuz halts evacuation/escort plans

Market relevance: Keeps geopolitical energy risk in focus despite oil giving back some war-premium gains.

* Oil down 2% as Hormuz shipments resume, even after vessel hit

Market relevance: Energy markets are balancing reopened flows against renewed security risk near Oman/Hormuz.

* Kevin Warsh’s tough inflation talk reassures investors

Market relevance: Hawkish Fed-chair messaging and lower oil are pulling long-term inflation expectations lower.

* Gold poised for fourth weekly loss on hawkish Fed bets

Market relevance: Stronger dollar and higher-rate expectations continue to pressure precious metals.

* Dollar rides into second half of 2026 on a “winner takes it all” wave

Market relevance: Dollar strength is central for FX, commodities, liquidity, EM pressure, and multinational earnings.

* Samsung readies $648bn bet as AI boom reshapes South Korea

Market relevance: Huge AI/chip capex plans matter for semis, Korean equities, memory supply, and AI infrastructure.

* Rheinmetall hit by Germany’s doomed warship project

Market relevance: A major European defense-program setback could pressure defense shares and Germany industrial sentiment.

#Markets #Trading #Macro #AI #Tech #Oil #FX #Gold #Semiconductors #Defense

The Pareto principle is alive and well in trading. Long-term success comes from a few key factors: sound risk management, disciplined execution, and emotional control—not from chasing the “perfect” trade. If everyone is looking for the same perfect setup, it’s usually too obvious and too crowded to offer a lasting edge.

It also means working smarter, not harder. Stay curious, question your habits, be mindful, and focus on the actions that genuinely improve your edge instead of repeating what’s simply familiar.

The 80/20 Rule states that you get 80 percent of the value out of something from 20 percent of the information or effort. (It's also true that you're likely to exert 80 percent of your effort getting the final 20 percent of value.) Understanding this rule saves you from getting bogged down in unnecessary detail once you've gotten most of the learning you need to make a good decision.

#principleoftheday

Market digest — Thu 25 Jun, 2026

What matters most:

• AI/chip risk-on is back after Micron’s strong outlook, lifting Asian equities and chip names.

• Oil war premium is unwinding fast as Gulf/Hormuz flows normalize, easing inflation pressure.

• Rates/liquidity remain the macro tension point: stronger dollar, gold weakness, PBOC liquidity changes, and Japan bond stress all point to policy sensitivity.

* Stocks get boost from Micron outlook, oil slump

Market relevance: AI optimism plus lower oil is supporting global risk appetite.

* Oil price back at prewar levels as Gulf flows pick up

Market relevance: Falling crude reduces inflation pressure and geopolitical risk premia.

* Insurers slash war premiums for Strait of Hormuz ships

Market relevance: Shipping risk costs are falling as the ceasefire holds.

* US rate-hike bets hold dollar near 13-month highs

Market relevance: Dollar strength and Fed repricing pressure commodities, EM, and liquidity-sensitive assets.

* PBOC plans overnight reverse repo in policy shift

Market relevance: China is changing short-term liquidity management, relevant for rates, yuan, and China risk assets.

* Japan’s $2.3tn investment plan raises fresh JGB concerns

Market relevance: Fiscal expansion risk is adding pressure to Japan’s bond market and yen dynamics.

* BOJ hawk calls for rate hike every few months

Market relevance: Keeps Japan rates and yen intervention/rate-normalization risk in focus.

* SK Hynix targets $29bn US listing as AI demand surges

Market relevance: Major semiconductor/AI capital-markets event, with implications for global chip valuations.

* Anthropic says Alibaba illicitly extracted Claude AI capabilities

Market relevance: Adds regulatory and geopolitical risk to Chinese AI/tech exposure.

#Markets #Trading #Macro #AI #Oil #FX #China #Japan #Semiconductors

Market digest — Tue Jun 23, 2026

What matters most:

• Iran/oil risk is easing at the margin: US waiver lets Iran sell oil, while Hormuz routing confusion still keeps energy/geopolitical risk live.

• Japan/yen remains a pressure point: weak JGB demand and US-Japan FX talks raise BOJ/intervention sensitivity.

• AI/tech momentum is wobbling: Korea chip stocks sold off, SpaceX/AI-linked names under pressure, but AI capex/ads remain major market themes.

* Iran rushes to woo Asia's largest oil importers after US waiver

Market relevance: Potential crude supply relief and lower Middle East risk premium, but fragile if talks fail.

* Conflicting US-Iran advice on Hormuz leaves shipowners adrift

Market relevance: Shipping uncertainty around Hormuz keeps oil, insurance, and inflation-risk premia in focus.

* Bank of Japan normalisation on course for December increase

Market relevance: BOJ path matters for yen, JGB yields, global carry trades, and liquidity conditions.

* Japan's five-year bond sale draws soft demand on rate-hike fears

Market relevance: Weak auction demand reinforces pressure on Japanese yields and yen policy risk.

* US-Japan more aligned on FX after Bessent talks

Market relevance: Currency traders are watching for yen intervention after weakness near multi-decade lows.

* Korean stocks fall more than 4% from record high on tech selloff

Market relevance: Possible stress signal in the AI/chip rally after crowded semiconductor gains.

* SK Hynix ETF assets soar to $17bn, biggest in Hong Kong

Market relevance: Leveraged chip exposure shows speculative intensity around AI hardware trades.

* China pursues austerity with first fiscal gap cutback since 2023

Market relevance: Fiscal restraint amid weak domestic demand could weigh on China growth expectations.

* OpenAI pitches ChatGPT ads to Cannes marketers ahead of IPO

Market relevance: AI monetization and possible IPO positioning remain key for tech multiples and ad markets.

#Markets #Macro #Oil #Japan #Yen #AI #Semiconductors #China

Market digest — Mon, Jun 22, 2026

What matters most

• Oil and risk assets are reacting to signs of progress in US-Iran talks; energy/geopolitical risk remains the main macro swing factor.

• China/US trade tensions are back in focus: rare earth controls, supply-chain fragmentation, and a rebuilt US tariff wall.

• Rates/liquidity watch: Fed guidance uncertainty, BOJ hike path, UK political risk hitting sterling/gilts.

• Oil slides as US-Iran talks show progress

Market relevance: Lower oil eases inflation pressure and supports risk assets, but headline risk remains high.

• Iranian crude exports surge through Hormuz

Market relevance: More barrels moving through Hormuz reduces near-term supply panic and energy-risk premia.

• China restricts trading with some US rare earth companies

Market relevance: Escalates US-China supply-chain risk, especially for tech, EVs, defense, and industrials.

• Trump’s new US tariff wall shakes up winners and losers

Market relevance: Tariff rebuild could affect inflation, margins, global trade flows, and sector leadership.

• Warsh’s push to axe Fed guidance may lift US borrowing costs

Market relevance: Less Fed forward guidance could raise rate volatility and term premia.

• Japan’s PM signals acceptance of latest BOJ rate hike

Market relevance: Keeps yen/rates in focus after BOJ tightening; important for carry trades and global liquidity.

• Pound trades near 2026 low as UK political uncertainty builds

Market relevance: Sterling and gilts remain vulnerable to UK political/fiscal-risk repricing.

• South Korea early exports jump again on AI chip demand

Market relevance: Confirms AI semiconductor cycle strength; relevant for Asian tech and global capex sentiment.

• Korea weighs curbs on leveraged Samsung/SK Hynix ETFs

Market relevance: Regulators are watching speculative AI-chip leverage, a potential volatility trigger.

#Markets #Macro #Oil #Iran #China #Tariffs #RareEarths #Fed #BOJ #FX #AI #Semiconductors

Markets Are Watching the Wrong Fed Story

Focusing too much on the hawkish tone after the last FOMC meeting may miss the bigger shift.

One of the most consequential changes in monetary policy since QE2 may be developing beneath the surface, and markets seem focused on the wrong thing.

The consensus debate is whether the Fed will cut, hold, or hike rates.

The more important question is whether the Fed is preparing to fundamentally change how it conducts monetary policy.

For more than a decade, markets have operated in a world of:

• Forward guidance

• Quantitative easing

• Massive Fed balance sheet expansion

• Heavy central bank influence over asset prices

A different framework is beginning to emerge:

→ Less forward guidance

→ Greater reliance on market signals

→ Continued balance sheet reduction

→ Shorter-duration Fed holdings

→ More emphasis on supply-side analysis

The implication is profound: instead of attempting to manage every aspect of financial conditions through policy rates and communication, the Fed could increasingly allow markets to determine the cost of capital.

That changes how investors should think about future tightening cycles.

If inflation proves more persistent than expected, the response may not necessarily be higher policy rates. Tightening could come through balance sheet policy and liquidity management instead.

The Treasury market appears to be pricing a more hawkish rate path than warranted.

A possible outcome:

• 2-year Treasury yields decline

• The yield curve bull steepens

• Long-end yields remain relatively stable

• Markets begin pricing lower terminal policy rates

Another important observation: recent shocks such as tariffs, geopolitical tensions, and energy price spikes have generated far less inflation pressure in market-based measures than many policymakers feared.

Breakeven inflation expectations remain well contained, suggesting investors continue to view these developments primarily as growth risks rather than sources of sustained inflation.

If this framework proves correct, the biggest monetary policy story of the next few years won’t be the timing of the next rate cut.

It will be the gradual transition from a Fed-driven market to a more market-driven Fed.

The question investors should be asking is not:

“Will the Fed hike again?”

It’s:

“How much influence is the Fed willing to give back to the market?”

#Fed #FederalReserve #FOMC #Treasuries #YieldCurve #Inflation #Markets #Macro #Investing

Totally agree. Success in trading comes not only from identifying patterns in market behavior and executing accordingly, but, more importantly, from recognizing patterns in your own behavior, becoming aware of them, and learning how to make them work in your favor. Trading is primarily a mental game.

Market digest — Fri 19 Jun, 2026

What matters most

• Hormuz/Iran is still the main macro driver: oil is easing as shipping resumes, but tanker flows and possible future charges remain key inflation/risk variables.

• Rates/dollar pressure is back: hawkish Fed expectations are lifting the dollar and reversing EM/commodity FX bets.

• AI capex + tech margins are under scrutiny: Accenture weakness, Meta financing, and AI cost discipline point to changing market leadership risks.

* Oil sinks as Hormuz flows recover

Market relevance: Lower oil reduces inflation pressure and supports risk assets, but the Strait remains a geopolitical chokepoint.

* 80mn barrels of oil sit ready to pass Hormuz

Market relevance: A large near-term supply release could pressure crude prices if transit normalizes.

* Stocks retreat, dollar gains as traders shun risk

Market relevance: Risk-off tone plus stronger dollar can hit equities, commodities, and EM assets.

* Hawkish US rates shift upends currency bets

Market relevance: Expectations of higher US rates are reversing EM and commodity-currency trades.

* Currency traders pile into dollar calls after hawkish Fed

Market relevance: Options positioning suggests stronger-dollar momentum may persist.

* Accenture warning hits Indian software stocks

Market relevance: Adds pressure to global IT services and AI-disruption narratives.

* Companies rein in AI usage as costs strain budgets

Market relevance: AI adoption is still strong, but spend discipline could affect cloud/software revenue assumptions.

* EU delays trade confrontation with China

Market relevance: Reduces immediate trade-war risk, but Europe-China tensions remain unresolved.

* US opens Section 301 probe into Germany over pharma

Market relevance: Raises US-Europe tariff risk and could hit pharma/healthcare trade flows.

* Xi’s China demand push is sputtering

Market relevance: Weak domestic demand keeps pressure on China growth, commodities, and Europe exporters.

#Markets #Oil #Fed #Dollar #AI #China #Macro

Market digest — Thu Jun 18, 2026

What matters most

• Fed tone turned hawkish under Kevin Warsh: bonds sold off, dollar rose, and markets repriced toward possible 2026 hikes.

• US–Iran deal eased oil/Hormuz risk, but fuel/logistics disruption and sanctions details still matter.

• China/AI/critical-minerals headlines remain active: Microsoft/OpenAI in China, G7 minerals alliance, and China clearing a major media merger.

* Fed officials tilt towards rate rise as Kevin Warsh era begins

Market relevance: Hawkish Fed shift pressures bonds/equities and supports dollar/rate-volatility trades.

* Treasury yields rise after Warsh’s debut meeting brings hawkish shift

Market relevance: Confirms bond-market repricing after Fed messaging; key for rates/liquidity.

* Dollar jumps as Fed holds rates but projects one hike later this year

Market relevance: Direct FX impact; supports “US exceptionalism” and weighs on EM/commodities.

* Oil slips again as US, Iran sign peace deal

Market relevance: Lower geopolitical oil premium; affects energy, inflation expectations, and central-bank path.

* Ships divert in hunt for fuel after Gulf conflict hits supplies

Market relevance: Even with de-escalation, supply-chain and fuel bottlenecks can keep energy volatility elevated.

* G7 sets up critical minerals alliance to cut reliance on China

Market relevance: Strategic metals, EVs, defense supply chains, and China-risk premium.

* Microsoft makes big AI inroads in China by selling OpenAI models

Market relevance: AI monetization + US/China tech-policy implications.

* JPMorgan Chase cuts off Anthropic access for its Hong Kong staff

Market relevance: Shows AI adoption colliding with compliance/geopolitical risk in finance.

* Chinese regulators clear Paramount Skydance–Warner Bros Discovery merger

Market relevance: China approval reduces deal risk; relevant for media/tech M&A sentiment.

#Markets #Fed #FOMC #USD #Bonds #Oil #AI #China #CriticalMinerals #Macro

FOMC June 2026 — Key Takeaways

1. Fed held rates steady, but the meeting was hawkish

Federal funds rate unchanged at 3.50%–3.75%.

Decision was unanimous (12-0).

This was the first meeting under new Fed Chair Kevin Warsh.

2. The biggest surprise: the Fed’s outlook turned more hawkish

In March, the Fed expected a rate cut in 2026.

In June, the median forecast shifted to a rate hike in 2026.

The median year-end 2026 rate projection rose from 3.4% to 3.8%.

3. Dot plot flipped from “cut” to “hike”

9 of 18 Fed officials now expect at least one rate hike this year.

6 officials expect two hikes.

The most hawkish member sees rates near 4.5%.

Future cuts are still projected, but only later (2027–2028).

4. Inflation forecasts were revised sharply higher

Interpretation: Fed sees inflation as more persistent while economic growth remains relatively resilient.

5. Major change in Fed communication

Statement was rewritten and significantly shortened.

Language hinting at future rate cuts was removed.

Traditional “data-dependent” and balanced-risk language was largely dropped.

New emphasis:

“The Committee will deliver price stability.”

6. Kevin Warsh signaled a new regime

Focused on restoring anti-inflation credibility.

Rejected any discussion of raising the Fed’s 2% inflation target.

Did not submit his own dot-plot projection.

Indicated broader reviews of Fed communication and operations.

7. Hawkish despite falling oil prices

WTI oil has fallen roughly 40% from its peak.

Yet the Fed became more hawkish.

This suggests policymakers no longer believe inflation is primarily an energy problem.

Concern has broadened to underlying/core inflation pressures.

8. What changed versus March?

March (Powell Fed):

Expected rate cuts.

Inflation seen as manageable.

More balanced communication.

June (Warsh Fed):

Possible rate hikes.

Much higher inflation forecasts.

Removal of easing bias.

Stronger commitment to fighting inflation.

9. Market implication

The key message was:

The Fed did not hike rates, but it told markets that the next move could be a hike rather than a cut.

The “rate-cut trade” that markets were expecting earlier in 2026 has largely been challenged. Under Warsh, the Fed appears willing to keep policy tighter for longer until inflation is clearly moving back toward 2%.

Bottom line for investors

Bullish for the US dollar.

Bearish for bonds (higher yields for longer).

Potential headwind for growth stocks and crypto if markets fully price out future cuts.

The Fed’s reaction function has become more inflation-focused and less supportive of near-term easing.

#FOMC #FederalReserve #Fed #Inflation #USD #Bonds #Stocks #Crypto #Markets

Market digest — Wed, Jun 17, 2026

What matters most

• Oil/geopolitical risk is the big swing factor: US-Iran peace progress, Hormuz reopening, and oil falling below $80 are easing inflation fears.

• Rates/FX remain central: Fed decision ahead, bullish dollar bets returning, ECB/SNB/BOJ/PBOC all in focus.

• AI/tech capital cycle is still hot: SpaceX/Cursor and AI funding headlines keep mega-cap/private-market momentum in view.

Top stories

• Bonds rally ahead of Fed as oil extends slide

Market relevance: Lower oil plus Fed-watch is driving bonds and global rate expectations.

• Oil tankers rush back toward Middle East before Hormuz reopening

Market relevance: Signals normalization of energy flows, potentially easing crude/shipping risk premia.

• Oil sinks below $80 as traders bet Strait of Hormuz flows will return

Market relevance: Brent at a 3-month low reduces inflation pressure and changes energy-equity setup.

• ECB officials say Iran peace isn’t enough to fix energy shock

Market relevance: Europe rates may stay tighter even if geopolitical risk fades.

• Investors pile into bullish dollar bets as ‘US exceptionalism’ returns

Market relevance: Strong dollar positioning ties into Fed path, liquidity, and global risk appetite.

• China’s central bank hints at Fed-style rate-setting shift

Market relevance: A PBOC framework shift could reshape yuan rates, liquidity, and China asset pricing.

• PBOC launches tool to boost yuan use by foreign central banks

Market relevance: Incremental yuan internationalization move with FX/reserve-management implications.

• BOJ keeps market steady with yen volatility at lowest since 2021

Market relevance: Yen calm despite weak levels matters for carry trades and Japan policy risk.

• SpaceX leapfrogs Amazon; announces $60bn Cursor deal

Market relevance: Reinforces AI/tech megadeal momentum and private-market valuation pressure.

• Huawei comeback tests limits of US chip controls

Market relevance: Important for China/U.S. tech competition, semis, and AI supply-chain assumptions.

#Markets #Macro #Oil #Fed #FX #AI #Tech #China #Japan #Geopolitics

Market digest — Tue 16 Jun, 2026

What matters most

• Hormuz/Iran relief is driving risk-on sentiment and lower oil, but FT says shipping normalization may take weeks.

• BOJ hiked to 1%, putting yen/JGB volatility and global rate repricing back in focus.

• China data weakened sharply, with retail sales and investment slumping — a macro risk for global growth and commodities.

Top stories

• Strait of Hormuz reopening optimism cools oil

Market relevance: Lower energy-risk premium supports equities, but shipping uncertainty keeps oil/geopolitical risk live.

• BOJ raises rates to 1%, highest since 1995

Market relevance: Key move for yen, JGBs, global liquidity, and carry trades.

• China retail sales sink; investment slump deepens

Market relevance: Weak China demand hits growth expectations, cyclicals, commodities, and Europe exporters.

• Global stock rally cools after Iran deal relief

Market relevance: Markets are reassessing whether the geopolitical de-escalation rally has already priced in too much.

• Economists expect higher rates as Kevin Warsh takes Fed reins

Market relevance: Fed path and inflation stance remain central to dollar, bond yields, and equity multiples.

• AI fuels major PE windfalls; Kioxia gain in focus

Market relevance: Reinforces AI capital-cycle strength and valuation momentum around chips/infrastructure.

• Nvidia seeks over $25bn in first bond deal since 2021

Market relevance: Tests credit-market appetite for AI infrastructure exposure amid heavy tech borrowing.

• EU says China trained Russian troops for Ukraine war

Market relevance: Raises Europe-China geopolitical risk and potential sanctions/trade-friction headlines.

• Hedge funds short European carmakers on China competition fears

Market relevance: Pressure on Europe autos highlights China EV competition and sector-specific downside risk.

• RBA holds key rate, keeps tightening option open

Market relevance: Adds to global central-bank divergence; relevant for AUD, rates, and Asia-Pacific risk.

#Markets #Macro #Oil #Japan #China #AI #Rates #Geopolitics