A recent interview I did with Bloomberg about risk, volatility, and the VIX, which I co-pioneered with Prof. Menachem Brenner.

“Risk Is Misunderstood by Many Investors, Says VIX Pioneer”, by @YPeterseil

https://t.co/uMvV2yShGa

The followup post with some of our (=@BrennerMenachem and mine) feedback and clarifications with the author of this thread (again - in HEBREW) -

https://t.co/3dvDtTQCOG

#VIX

🚨 לקרוא עד הסוף 🚨

אחרי שפרסמתי את השרשור על הVIX פנה אליי הבן של פרופסור דן גלאי ומסר תודה בשם הפרופסורים על הקרדיט. הוא שאל האם יש משהו שהייתי רוצה לדעת בהרחבה על הויקס. אז שאלתי.

למה הבורסה לאופציות בשיקגו CBOE לקחו את רוברט ויילי ולא פיתחו איתם את המדד? קיבלתי תשובה.

בחזרה לאמצע שנות ה80, כשהם התחילו לפתח את התאוריה, הם פיתחו אותה על מדד הS&P100, עליו היו אופציות עם פקיעה חודשית בלבד. המרכיב המשמעותי שהיה חסר בנוסחה זה סדרת אופציות שפוקעות בדיוק ב30 ימים, אם לדוגמה אנחנו ב10 לחודש אבל יש אופציות שפוקעות רק ב31, איך אתה חוזה תנודתיות ל30 ימים קדימה מה10 עד ה10? הם הצליחו להתגבר על זה עם הרעיון של יצירת אופציה סינטטית שהיא תמיד 30 יום לפקיעה ע״י אינטרפולציה (הרחבה בשרשור).

ביולי 1987 טסו לשיקגו פרופסור גלאי וברנר לפגישה עם המחלקה הכלכלית של בורסת האופציות לשיקגו (CBOE) מטרת הפגישה הייתה להשיק מדד Sigma שישקף את התנודתיות החזויה בשוק. באוקטובר 1987 (יום שני השחור) השוק נכנס למשבר וכל התכניות הוקפאו. בנוסף פרופסור ברנר נפגש עם חברי ההנהלה של הבורסה האמריקאית לניירות ערך AMEX גם להציע להם את הרעיון אך גם פה מסיבות טכניות זה לא הבשיל.

במקביל לזה קרו 2 דברים:

1. פרופסור גלאי עבד עם פרופסור ויילי על תיק אחר ב1988, לאורך העבודה הוא שיתף אותו ברעיון של מדד תנודתיות שמסתמך על אופציות במדד הS&P100. ויילי התעניין והבטיח לפרופסור גלאי לספק להם נתונים על עסקאות בS&P100. הבטחה שלא קויימה.

2. ב1989 פרופסור גלאי וברנר פרסמו את המחקר שלהם על הצורך במדד התנודתיות (מצורף בתגובה).

אחרי שהשיחות לא הבשילו מול הבורסות השונות, באופן לא ברור הCBOE החליטו לשכור את שירותיו של רוברט ויילי ב1992 ומשם הגיע ההשקה של הVIX ב1993.

אני זהיר במילותיי אבל אפשר להסיק באופן די ברור שהקרדיט המלא מגיע לפרופסורים דן גלאי ומנחם ברנר. כנראה שההכרה המלאה כוללת הפרסים הרבים שויילי קיבל לאורך השנים הייתה צריכה להיות שלהם ולא שלו. או לכל הפחות לא שלו לבד.

אשמח שתשתפו כדי להפיץ את הסיפור המלא שגם אני לא הכרתי עד היום ושהם יזכו להכרה בישראל לכל הפחות. הרגשתי חובה אחרי השרשור הארוך שעלה וההתייחסות הקטנה שזה קיבל.

A terrific thread [in HEBREW] about the technicalities and history of the #VIX. In a followup with the author, @BrennerMenachem and I added some color and a few corrections about the origin of the VIX.

If you're a Hebrew speaker, I definitely recommend this thread:

היום נדבר על אחד המדדים החשובים בשוק. מדד התנודתיות (Volatility IndeX) או בשמו הנפוץ יותר מדד הפחד. הלא הוא הVIX.

מתי הוא הומצא, איך הוא מחושב, מתי עולה, מתי יורד, למה היסטורית הוא אינדיקטור מאוד חזק לתחתית בשוק + עובדת בונוס לסיום.

1/10 💰🧵

These are challenging times, and the #VIX is reflecting what's going on in the world, and especially in the US.

The increased volatility over the last 2 weeks is credited to Trump's zig-zag policies, especially re tariffs:

Determining the tariffs arbitrarily

raising them then freezing them, and creating uncertainty in so many countries as well as in the US.

Once, the policies are stabilizing, one way or another, volatility will decline.

#VIX

@unusual_whales The markets are now in the "unknown unknowns" zone. One indicator of the UU zone is VVIX (Vol of Vol) was 152 yesterday, highest in 6 months.

Another indicator is the volume of Out of the Money(OTM) & Deep OTM Puts (e. g. Strike Price 480 & lower) for short maturities.

In Hebrew, so hopefully Google Translate will help!

Shaul Amsterdamski (@amsterdamski2) in @calcalist today writes about the history of the $VIX and its effect on today’s markets (and Israel specifically):

https://t.co/ZTyD1zjLBC

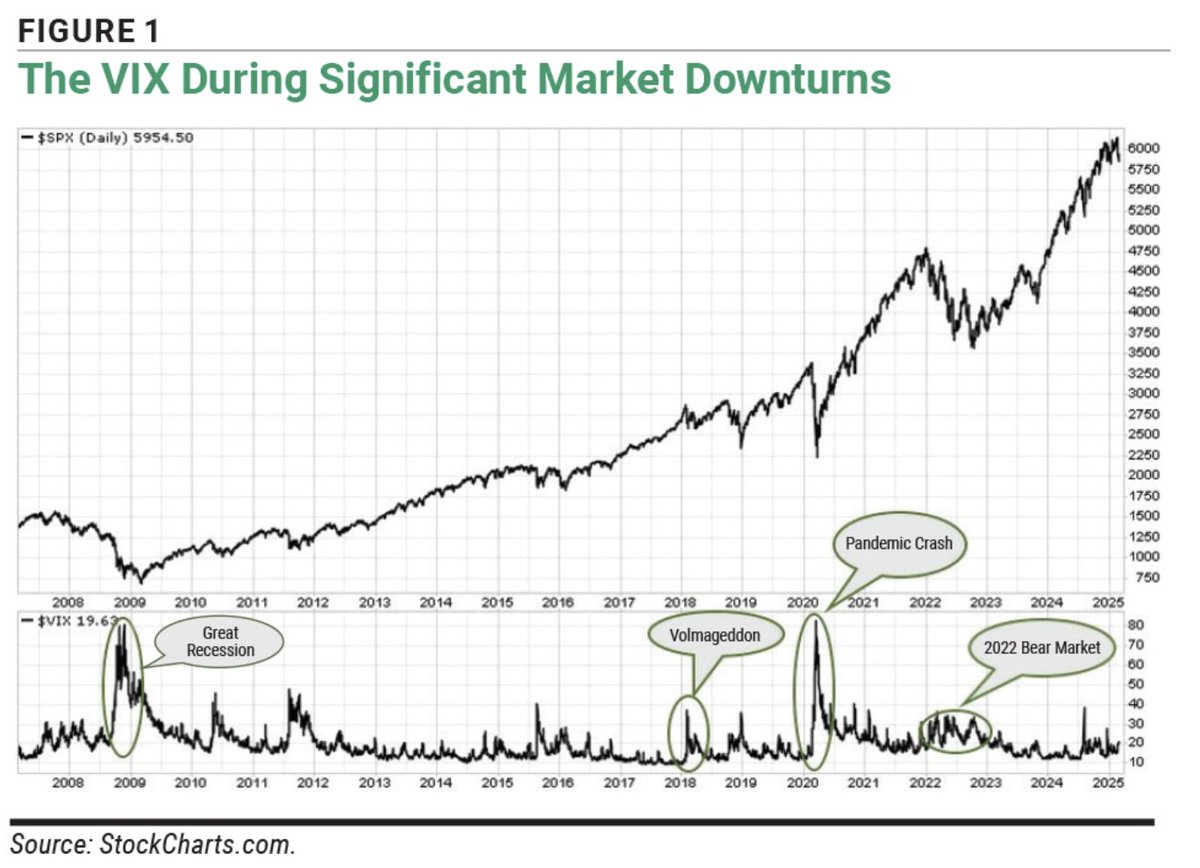

Many are saying that today’s $VIX levels only happened twice in history - during the 2008 financial crisis, and the 2020 COVID.

However - the largest jump was during the Crash of October 87. The implied increase to over 100, and the indexes fell 22%; only it was at pre-VIX time…

@boazweinstein Note that the largest jump was at the time of the Crash of October 1987. The implied increase to over 100, and the indexes fell by 22%; only it was at pre-VIX time…

@zerohedge Note that the largest jump was at the time of the Crash of October 1987. The implied increase to over 100, and the indexes fell by 22%; only it was at pre-VIX time…

@KobeissiLetter Note that the largest jump was at the time of the Crash of October 1987. The implied increase to over 100, and the indexes fell by 22%; only it was at pre-VIX time…

@dougboneparth Note that the largest jump was at the time of the Crash of October 1987. The implied increase to over 100, and the indexes fell by 22%; only it was at pre-VIX time…

Two events that happened 50 years ago have shaped the modern financial markets we have today.

An article (HEBREW) I co-authored with @BrennerMenachem about the impact of the CBOE and Black & Scholes on our world today:

https://t.co/szba8HnFwl

Limited Time Offer: Save 50% on the "Essentials of Risk Management, Second Edition" audiobook. Offer ends 09/20 Michel Crouhy, @profdangalai, and Robert Mark https://t.co/ym6Y8MtCsD

במחקר של @SadeOrly ו @ProfDanGalai מ-@HUBusSchool עולה כשהמוח האנושי לא מותאם להחלטות פיננסיות. אנשים אינם אוהבים להפסיד וסובלים מאוד מהתחושה הזו. הרוב מעדיפים לא לדעת, במקום להתמודד עם הדילמות והאי־ודאות של העולם הפיננסי. איך זה משפיע על החלטות משקיעים וההחלטות היום יומיות שלכם?

The search for your next audiobook is over! For a limited time, save 50% on the "Essentials of Risk Management, Second Edition" audiobook by Michel Crouhy, @profdangalai, and Robert Mark. https://t.co/5wIOkRg0HG